The euro on the global stage - speech by Klaus Regling

Klaus Regling, ESM Managing Director

“The euro on the global stage”

3rd Max Watson lecture, St Antony's College, University of Oxford

Online, 21 October 2021

(Please check against delivery)

Good afternoon from Luxembourg,

It is a special honour, both personally and professionally, to speak here tonight. Max Watson was my former boss, later my colleague – but even more so, he was throughout all these years my dear friend.

For 30 years, I had the privilege to work side by side with Max, a truly outstanding economist: first, at the International Monetary Fund (IMF) in Washington and then later, at the European Commission in Brussels.

Max’s foresight, his sharp analytical assessments and his intuition for economic developments were unique. I think, Max was what John Maynard Keynes would have described as a “master-economist”.[1]

Last time I spoke in Oxford was in 2013. In his introduction, Max called me the “mid-wife of the euro project”. So, I think, if Max were here with us tonight, he would not be surprised that I will speak about the euro.

The euro has been part of my professional journey for four decades. I am a convinced European. I believe that the euro is an essential element of European integration and that its role is crucial for strengthening European sovereignty.

The challenges of dollar dominance

During the years Max and I worked at the IMF, we witnessed the vulnerability of the international financial and monetary system, which depends mainly on the US dollar.

The US dollar has been the dominant global currency throughout the past decades, and it continues to serve as a point of reference for international borrowers and investors. But an excessive reliance on the US dollar entails clear drawbacks.

In the 1980s and 1990s, we saw how the dominance of the dollar contributed to and exacerbated the debt crises in Latin America and Asia. The reliance on dollar funding makes emerging markets vulnerable to swings in US financial conditions and to changes in monetary policy.

Following an increase in interest rates and an appreciation of the US dollar, several emerging markets could not roll over their external debt and faced difficulties paying for their imports. They had to go through a painful adjustment and their economies went into recession, while the international banking system was shaking.

By now, it is well documented how US monetary policy can induce shocks to global financial markets. Not surprisingly, monetary policy decisions of the Federal Reserve are – by law – based on economic developments in the United States. However, given the prominence of the US dollar in the international monetary system, these decisions also affect the rest of the world. The impact on capital flows to and from emerging markets is often particularly large. Valuation effects on foreign debt denominated in one major currency can be devastating.

The euro’s initial weaknesses

The launch of the euro was a milestone not only in the history of European integration, but also in the evolution of the international monetary and financial system.

Now more than 20 years in existence, the euro has become a symbol of European integration. Over 340 million European citizens use the euro every day across the euro area. And with 79% of citizen support, the euro is today at its peak of popularity since 2004.

The euro is also a project to advance Europe in the global economy. That is why its external dimension, i.e. the international role of the euro, has become more important. The euro is a symbol of Europe on the world stage. It is a currency that has achieved a global standing and contributes to the stability of the global economy and the international financial system.

But, already in the early days of the euro, Max put his finger on one weakness of the European monetary union that had to be addressed for the euro to become a stable and viable alternative on the global scene. In a report by the European Commission that Max co-authored in 2006 well before the euro crisis, he found that the macroeconomic imbalances in the euro area were destabilising countries’ competitive positions.

This diagnosis proved right on the mark: a few years later, the euro came under such severe threat that some economists and market analysts were predicting its collapse. This was a consequence of two crises that hit Europe. First, we had to deal with the U.S. subprime crisis, which entailed a credit crunch and caused great upheaval among banks, including in Europe. Some of which had to be bailed out by governments. Soon afterwards, the euro area went through a home-grown crisis, the sovereign debt and competitiveness crisis.

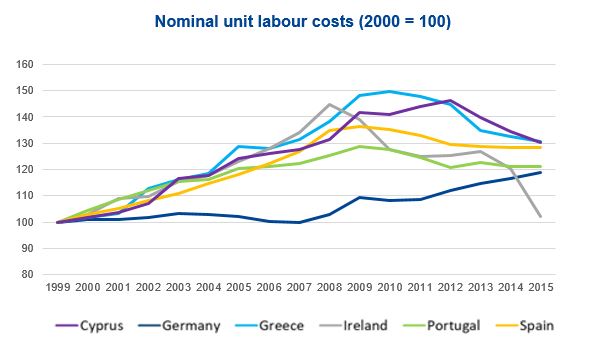

As Max had correctly cautioned, ill-designed economic policies led to a loss of competitiveness in several euro area countries. Wages and salaries had been growing much faster than productivity. And unit labour costs increases were 20-40 percentage points higher than in Germany.

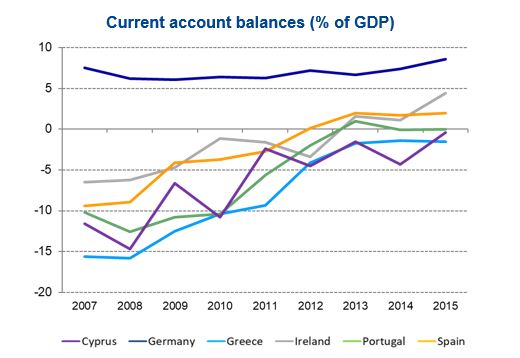

Current account deficits grew unsustainably large. Real estate bubbles emerged in some countries.

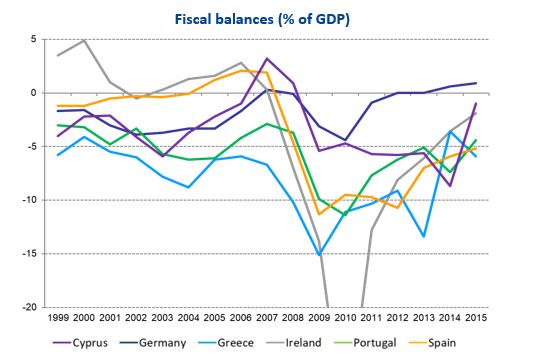

The crisis also highlighted the risk and devastating effects of the so-called “doom-loop”: unsustainable sovereign debt could have a severe impact on banks, and a weak banking sector could have a significant impact on a sovereign. Some states had run fiscal deficits for a long time and became therefore highly indebted.

Before the crisis emerged, markets did not differentiate sovereign risks across countries, as illustrated by the extremely tight spreads against the German Bund. As the crisis unfolded, markets woke up – the risk premium they were requesting for lending money to the affected countries became prohibitively high. Market access was lost or unaffordable.

In the original institutional architecture of our Economic and Monetary Union (EMU), there was no lender of last resort for euro area countries. Once a country had fulfilled the Maastricht criteria and adopted the euro, it was unthinkable it could lose market access.

Then early last decade, the unthinkable happened. Several euro area countries lost market access and needed urgent financial assistance to cover fiscal deficits and to refinance maturing debt. However, the only existing international institution at that time with a mandate to act – the International Monetary Fund – had insufficient resources to cover the affected countries’ financing needs.

For this reason, it was necessary for the euro countries to establish a crisis fund that could provide emergency financing to its members. We discovered that there was an institutional gap in the architecture of EMU: there was no lender of last resort for sovereigns in the euro area.

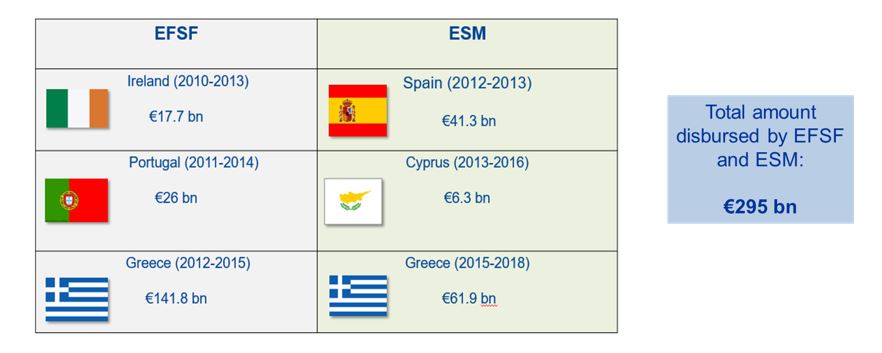

The first institution of this kind was the European Financial Stability Facility, or EFSF, established on a temporary basis in 2010. The first financial assistance programme provided by the EFSF was for Ireland. At this point, as head of the EFSF, I was well aware of the problems in the Irish banking sector, because Max and I had co-authored a report in early 2010 on the sources of the banking crisis there.

Soon it was understood that the EFSF would not be sufficient and that a permanent institution was needed. Two year later, in 2012, a permanent crisis resolution fund, the European Stability Mechanism (ESM), was created.

Together, these two institutions provided a total of nearly €300 billion in loans to five countries: Ireland, Portugal, Greece, Cyprus, and Spain.

To finance these loans, the EFSF and ESM had to borrow the money first. This was done by issuing bonds, which are purchased by investors, mainly institutional investors such as banks, insurance companies, and pension funds but also central banks around the world.

The ESM can borrow money at very low rates, because its bonds are backed by €700 billion in capital from our Member States, of which €80 billion is actually paid in cash. This serves as security for bond holders as it reassures our bondholders that they will be repaid when the bonds mature. For this reason, we have a AAA rating and can raise money well below the rates borrowing countries would be charged by investors.

EFSF and ESM financial assistance to the five countries was linked to conditionality: this means that in exchange for money, the countries had to carry out reforms to fix their economies. The problems that had led to the loss of market access needed to be tackled. This happened in all five countries. All of them managed to regain market access, and to grow above the euro area average after they left their EFSF/ESM programme, until the pandemic hit us early last year.

The creation of the two rescue funds for the euro area was an essential step in restoring confidence and financial stability during the euro crisis. The ESM was a key contributor in overcoming the crisis: the financial assistance it provided gave the beneficiary countries time to do their homework and tackle the problems that led to the loss of market access. They tightened their budgetary policies, implemented structural reforms and regained competitiveness.

What Max had been prescribing five years earlier, became the mainstream policy thinking. In particular: “Internal devaluation”, cuts in nominal income, happened to restore competitiveness quickly. With the correct remedies, the macroeconomic imbalances that were a main cause for the euro crisis were sharply reduced.

However, other important actions were needed in parallel to get out of the euro crisis:

- The European Central Bank (ECB) introduced unconventional monetary policy instruments, such as asset purchase programmes, to support the monetary policy transmission mechanism.

- The EU introduced new rules to prevent the build-up of macroeconomic imbalances from happening again; surveillance and economic policy coordination were strengthened.

- Furthermore, efforts were made to make the banking sector safer, as it was the source of some of the problems that contributed to the euro debt crisis. When a government needs to bail out systemically important banks to protect its banking sector, it has a major impact on its fiscal balance and the level of its public debt. In other words, a weak banking sector can lead to a substantive use of taxpayers’ money.

- The establishment of a banking union brought about centralised supervision of systemic banks based on a single rulebook. It also introduced a bank resolution mechanism.

A lot has happened in the years following the euro crisis. We had recognised the weaknesses of the monetary union and gradually compensated for them. Thus, several new institutions were created to improve the prevention and management of crises.

The temporary rescue fund EFSF was created at the height of the euro crisis in 2010, the permanent ESM followed two years later.

In 2011, the European Banking Authority (EBA) was established as well as the European Systemic Risk Board (ESRB), which monitors the European Union's financial system, mainly to prevent or limit macroprudential risks.

The following year, the European Securities and Markets Authority (ESMA) was added to the institutional set up.

With the start of the banking union, the Single Supervisory Mechanism (SSM) was created in 2014. It directly supervises the 130 systemically important banks in the euro area, banks whose failure could threaten a country's economy and financial system (see slide 6).

Since 2015, the Single Resolution Mechanism (SRM) has ensured that financial institutions threatened with insolvency can be resolved with the least possible impact on the economy and on public finances.

The creation of these new institutions has significantly strengthened the institutional foundation of the monetary union. Subsequently, over the past decade, progress in the reduction of internal imbalances has reinforced the stability of the euro area.

The euro area did not break up as expected by some observers. On the contrary, the number of its member states has increased. Currently, 19 of the 27 EU Member States use the euro. But by 2024, that number could increase to 21 as Croatia and Bulgaria entered into the Exchange Rate Mechanism II (ERM II) – which serves as a transitional mechanism before a country can join the euro area.

Where does the euro stand in the international monetary system?

So, where does the euro stand today in the international monetary and financial system? Despite the crises a decade ago, the euro firmly established its status as a key international currency. It is commonly used for trade invoicing, cross-border payments, securities trading, and bank loans. It is among the top currencies used for trading and for central bank reserve holdings, and it established itself as a standard for some managed exchange rate regimes.

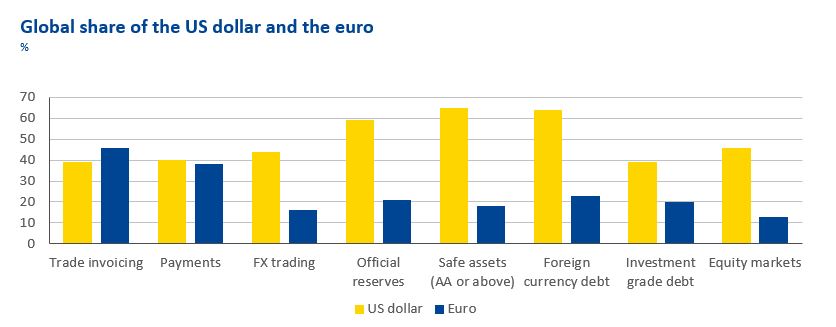

Overall, the euro’s international role today reflects its share in the world economy and global trade. It is on par with the US dollar in terms of international trade invoicing and payments, although it remains behind the dollar on global financial markets.

The euro’s share in global import and export invoicing is 46% and almost 40% of global payments[2] are made in euros, both broadly on par with the dollar. Sixty countries outside the European Union have linked their currencies to the euro in one way or another[3], in addition to the EU Members Denmark, Bulgaria and Croatia.

However, the dollar’s predominance remains deeply entrenched on global financial markets and the euro remains a distant second in terms of importance. Inertia across the international monetary and financial system explains the difference in part, together with a traditional reliance of global investors and other countries on the dollar as a reference currency. The US dollar remains the world’s leading currency on foreign exchange markets, with 44% of foreign exchange trades in 2019, whereas the euro’s market share stood at 16% that year.[4]

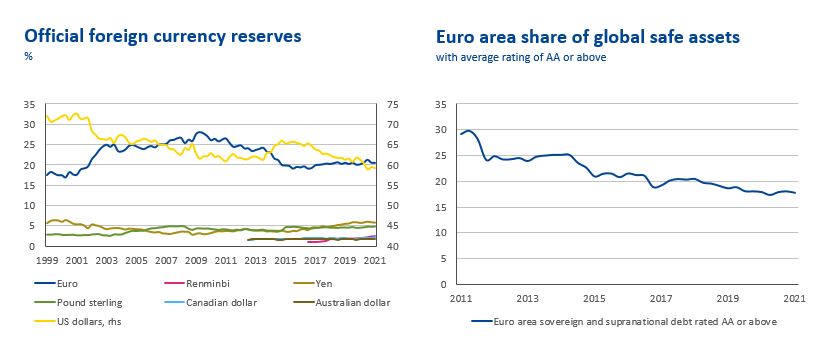

The US dollar is also the top currency in terms of official foreign exchange reserves, but its share dropped by 12% points since 1999, from 71% to 59%, while the shares of other currencies have been increasingly gradually. The euro’s share in reserves is now at 21%, higher than twenty years ago, although it has not yet fully recovered to its peak before the sovereign debt crisis.

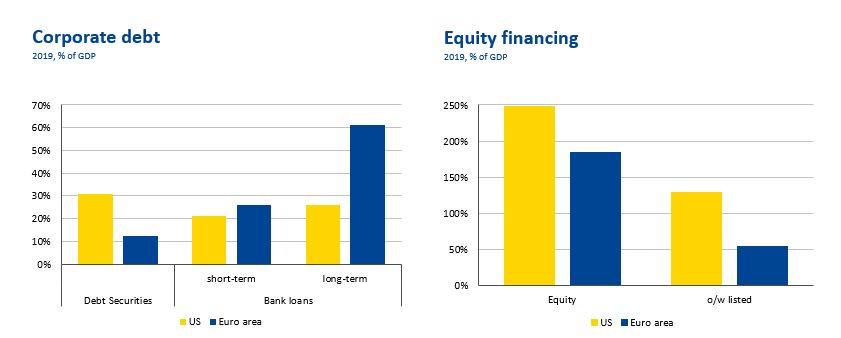

Foreign investors hold less debt in euros than in US dollars. In part, this might be due to the shortage of euro-denominated safe assets compared to US Treasuries. For instance, if we set the threshold at an average AA rating for sovereign debt as safe assets, we can see that the share of the euro area out of global safe assets dropped from around 30% to below 20% over the past ten years. But foreign investments in dollar-denominated assets is not restricted to safe assets. US companies also issue more corporate bonds: the stock of debt securities issued by US corporates is more than three times larger than in the euro area.

A similar picture emerges looking at equity markets. US companies’ equity financing is more than double its GDP, while in Europe it is considerably less than that. The euro area financing model relies much more heavily on banks than that of the US, and this limits European financial market size and liquidity. The euro area reliance on bank funding, rather than bond or equity financing, means a larger share of outstanding corporate debt registers as unmarketable assets on bank balance sheets, and is not available as assets for foreign investors.

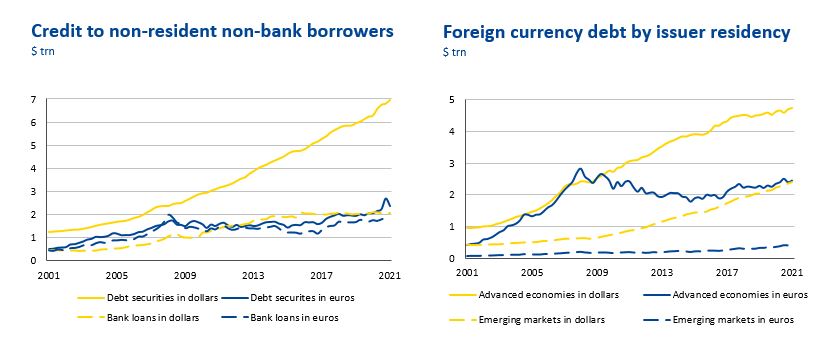

The euro is also well behind the US dollar on international debt markets. The euro represents less than a quarter of the value of outstanding stock of international debt securities, while the share of dollar-denominated debt is over 60%[5]. Similarly, the share of the euro-denominated securities out of global investment grade debt is only about 20%[6].

The dollar’s dominance on international debt markets is partly driven by the increasing importance of emerging markets as issuers of foreign currency debt. Their traditional preference for the dollar as a funding currency has driven dollar-denominated debt issues and cemented the dollar’s position as the main financing vehicle. The issuance of euro-denominated international bonds has picked up recently, but it is too early to say whether this is the beginning of a new trend.

The benefits of a multipolar system

The question is: if the dollar is the clear dominant currency and the euro a strong second, what could be the benefits of moving to a multipolar currency system? In my view, the international monetary system could function better if it relied less on only one currency. I touched on that in the beginning. A more diversified mix of global currencies would allow borrowers and investors to diversify their assets and liabilities, enable effective risk sharing and hedge against volatilities induced by changes in US monetary policy that lead to capital flow fluctuations. This is what triggered the Latin American debt crisis in the early 80s and the Asian debt crisis in the late 90s. Having more than one leading currency would make the world economy less vulnerable to shocks linked to one specific currency.

Hence a more prominent international role for the euro – and one or two other currencies – would lend greater stability to the international financial system as a whole. A wider use of the euro for financial transactions and investments can also promote diversification across the international monetary and financial system.

We also have to be mindful that, in the face of the dollar’s dominance, China is determined to elevate the renminbi globally with the opening up of Chinese financial markets and with the authorities’ active policy support. And, of course, we should not forget about the British pound sterling. Today, its share in official reserves and foreign exchange markets is still well above the renminbi’s, but the renminbi is catching up strongly from a low level.

Therefore, to address these concerns, the goal should be a multipolar currency world, with the broader use of the euro, renminbi and possibly other currencies complementing the US dollar, contributing to global financial stability.

The euro is well placed to play a stronger international role, as it is backed by a large economic area, relatively low currency volatility, an independent central bank with a clear price stability mandate and a prohibition of monetising government deficits, and a credible legal system.

The euro area demonstrates its strong external position with a persistent current account surplus since 2012. Its broadly balanced international investment position shows that the monetary union can attract foreign investors, including those seeking a safe haven, and it can support investment in the rest of the world as a capital exporter.

To strengthen the euro’s international role further, Europe still has some homework to do.

The homework for Europe – how we can contribute to the move towards a multi-polar currency system

“Policy makers in the euro area have today two tasks: stabilising the current situation and completing monetary union.” These were my words at the start of my last presentation in Oxford.

Today, almost ten years later, this message is as relevant as before, although, fortunately, the emphasis has moved from the former to the latter. And the ongoing reforms to complete and strengthen European Economic and Monetary Union also support the euro on the international scene.

The key requirements for the euro to expand internationally cover policies that are also needed domestically. The global role of a currency effectively relies on two key characteristics, namely stability and liquidity.

The bedrock of a currency’s international status is the strength of the underlying economy and the stability of the financial system, underpinned by credible institutions. Thus, reforms to strengthen the growth potential in euro area member states and the functioning of the financial system overall are crucial.

Supporting growth requires addressing longer-term economic challenges and enhancing the perception of the euro globally. It also helps to mitigate risks of social and political conflict undermining euro area cohesion.

In this context, measures taken during the pandemic crisis go a long way to support the international role of the euro. The EU’s recovery fund “NextGenerationEU” addresses macroeconomic instability with intra-regional transfers and structural reforms. The fund, together with substantial ECB purchases of government debt, helps mitigate sovereign credit risk in high-debt countries, which has enhanced market confidence.

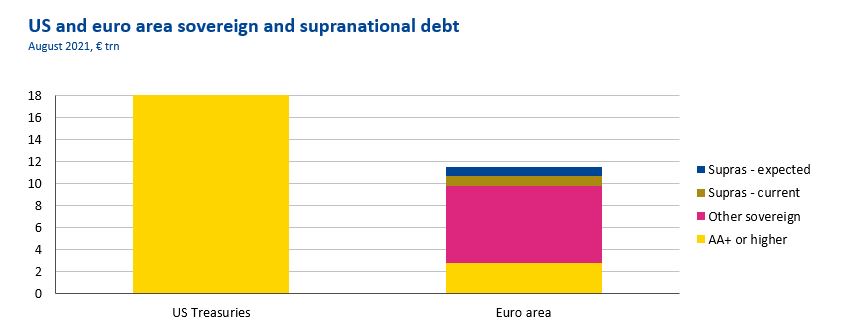

The EU debt issuance in response to Covid-19 will also expand the pool of euro-denominated safe assets over the coming years (see slide 15). A big part of the EU’s pandemic support, namely the new EU bond issuance by the Commission, the EIB financing of their support to businesses, and – if called upon – the ESM’s pandemic crisis support, will increase the pool of European safe assets.

The EU is on the way to becoming one of the largest issuers in the euro area and to expand the supply of euro-denominated safe assets: by 2026, a total of €850 billion new EU bonds could be issued. These policy measures together with the existing supranational debt (of around €800 billion) could result in almost €2 trillion European supranational debt over the next five years. Adding the highly-rated national debt could increase safe euro assets from 25% to almost 40% of euro area GDP (more than 5€ trillion). This is a considerable increase, but still less than half the comparable US numbers.

An ample supply of safe assets can help to stabilise European sovereign debt markets, and dampen price fluctuations during times of stress. More safe assets would also support financial stability by allowing European banks to substitute their holdings of national government bonds with European safe asset. Such diversification would help reduce the spillover of risks between the sovereign and the banking sector. Other benefits of more safe assets include an improved monetary policy transmission mechanism, potentially higher interest rates in core countries, smaller spreads, and more interest from international investors in the euro.

While progress has been striking in some areas during the pandemic, the euro area still needs more economic risk-sharing – via market channels as well as via public channels. A fully integrated financial market would mitigate cyclical divergences between member states through the markets and thus improve convergence. In terms of private risk-sharing, much remains to be done to complete banking union and capital markets union. These can help improve the stability and liquidity of euro-denominated financial markets, which in turn can make the euro area more attractive for global investors and elevate the euro’s global use.

A banking union and a single market for financial services – a capital markets union – would have many benefits: fewer obstacles to cross-border investments can facilitate a more efficient use of capital, open up new ways of financing companies, strengthen competitiveness and contribute to stronger growth in Europe. This is particularly important now to help the euro area economy grow again in the recovery phase after the pandemic.

Some difficult decisions still need to be taken to complete banking union, including a common deposit insurance scheme, but also improved cross-border integration of the banking sector and diversification of sovereign bonds on bank balance sheets.

The next important step towards the completion of banking union is the ESM backstop to the Single Resolution Fund. This backstop is an important element of the ESM reform, which will come into force at the beginning of 2022 and help to further improve financial stability in the euro area.

Besides banking union, the capital markets union is the other major project to strengthen risk-sharing in the currency area.

At present, however, the euro area consists of 19 national capital markets with their own rules and barriers to cross-border investment. A prerequisite for a capital markets union is the partial harmonisation of national insolvency laws, a common corporate tax base, and further supervisory convergence. The euro area would also benefit from more economic risk-sharing via public channels. There is some of that already today, through the EU budget, through loans from the European Investment Bank, through the financial assistance of the ESM and through “NextGenerationEU” in the coming years. However, “NextGenerationEU” is limited in time and tailored to the needs of all EU countries, but not the euro area.

For the euro area, there are other possible options on how to share risks more extensively.

Countries in a monetary union need more fiscal emergency buffers than countries with their own currency. This is because the countries, which share a currency have given up two important macroeconomic instruments: monetary policy and exchange rate policy. Thus, fiscal measures are the only macroeconomic tool left for these countries to counteract an external shock – such as a pandemic.

A central fiscal capacity would supplement national budget buffers of member states in a crisis with a European budget buffer to cushion economic downturns. The ESM could take on this additional task.

Finally, there is an area what I would call “financial plumbing”, that is, the infrastructure for payment and settlement within the euro area and with international markets. This also plays a role in determining the preference of markets for a currency. Work is underway to upgrade Europe’s payment system infrastructure. Examples include the launch of the ECB’s securities settlement platform TARGET2-Securities, a new platform for instant payments, and the upgrade of the large-value transactions TARGET system. The ECB is also currently working on the creation of a digital euro, which could improve the efficiency of payments as well.

A word on green and digital trends: Starting back in 2007 with the first “Climate Awareness Bond” of the EIB, Europe became over time the most important issuer of green bonds, also thanks to a stronger EU’s commitment to clearly defined criteria. Almost half the world’s green bond issues are today euro-denominated and this strengthens the euro’s international role.

Finally, the ECB is currently working on how to design and implement the digital euro. The investigation phase will start this October and last for about two years.

Over time, these innovations will offer international market participants easier access to the euro. With a broader use of the euro and a more developed infrastructure, Europe can reduce its dependence and enhance its strategic autonomy also in the financial sphere.

Conclusion

In its more than 20 years of existence, the euro has become a symbol of European integration. While it is still an ongoing project, it has provided a foundation for euro area member states to achieve stability and economic growth.

Safeguarding financial stability is an important element of the ESM’s work. We believe that a stronger euro – underpinned by a solid banking and capital markets union – would not only be advantageous for the euro area but for the global financial system as a whole.

To build a project like the euro, you must “study the present in the light of the past for the purposes of the future” as Keynes said[7]. Max talked and wrote about all this already 15 years ago. We are now catching up.

Thank you.

Accompanying slides

References

Anev Janse, K., Strauch, R. (2021), "Momentum builds for Europe’s capital markets union", ESM Blog.

Arslanalp, S., Simpson-Bell, C. (2021), "US Dollar Share of Global Foreign Exchange Reserves Drops to 25-Year Low"

Bank for International Settlements (2019), "Triennial Central Bank Survey – Foreign exchange turnover in April 2019"

Boz, E. et al. (2020), "Patterns in Invoicing Currency in Global Trade", IMF Working Paper, No. 20/126.

Carney, M. (2019), "The Growing Challenges for Monetary Policy in the current International Monetary and Financial System", Speech.

Cœuré, B. (2019), "Central bank digital currency: the future starts today", Speech.

Cœuré, B. (2019), "The euro’s global role in a changing world: a monetary policy perspective", Speech.

Dombrovskis, V. (2021), Keynote speech by Executive Vice-President Dombrovskis on euro accession for Croatia, Speech.

European Central Bank (2020), "The International Role of the Euro"

European Commission (2020), Standard Eurobarometer 94, Winter 2020-2021

European Commission (2006), "The European Economy", Watson, M. (ed.), No. 6/2006

Gopinath, G., Stein, J. C. (2018), "Banking, Trade, and the Making of a Dominant Currency", Working Paper 24485.

Habib, M. M., Stracca, L. (2011), "Getting beyond carry trade: what makes a safe haven currency?", ECB Working Paper, NO. 1288.

Hudecz, et al. (2021), "The euro in the world", ESM Discussion Paper.

Hardy, D. (2009), "ECB Debt Certificates: the European counterpart to US T-bills", Appendix I.

Hudecz, G., (2021), "Strengthening the international role of the euro", SUERF Policy Brief, No. 88.

McCauley, R. N. (2021), "The Global Domain of the Dollar: Eight Questions", Atlantic Economic Journal, Volume 48.

Miranda-Agrippino, S., Rey, H. (2020), "U.S. Monetary Policy and the Global Financial Cycle", The Review of Economic Studies, Volume 87, Issue 6.

Regling, K. and Watson, M. (2010), "A Preliminary Report on The Sources of Ireland’s Banking Crisis"

Regling, K. and Watson, M. (2008), "Financial Markets in the euro area – realising the full benefits of integration" in: Building the Financial Foundations of the Euro: Experiences and Challenges.

Regling, K. (2020), "Why we need to boost the euro’s international role", ESM Blog.

Regling, K. (2013), "Restoring Confidence in the Euro Area", presentation.

Strauch, R., Hudecz, G. (2021), "Strengthening the international role of the euro", ESM Blog.

Strauch, R. (2019), "The geopolitics of European financial markets", Speech.

Footnotes

Author

Contacts