A decade of the euro rescue funds EFSF and ESM

In June 2010, the temporary EFSF was established, followed by the permanent ESM in October 2012. ESM Board of Governors Chairperson Paschal Donohoe and ESM Managing Director Klaus Regling reflect on the past decade and the future of the euro area rescue funds.

Download brochure

Scroll further down to take a ride in the ESM car and discover some of the most memorable road stops of the past 10 years.

Message from the Chairperson of the ESM Board of Governors

The past decade has proven to be a defining phase in the history of European integration; from 2010, with the establishment of the European Financial Stability Facility (EFSF) to address the euro crisis, to 2020, when the coronavirus pandemic struck Europe.

The temporary EFSF and its successor, the permanent European Stability Mechanism (ESM), filled a gap in the European institutional architecture that was not foreseen at the inception of the European Economic and Monetary Union (EMU). In 2010, policymakers moved swiftly to fill that gap in order to reassure markets and mitigate the effects of the crisis. Together with fiscal and structural reforms at both European and national level, the European Central Bank’s (ECB) accommodative monetary policy, and the creation of a banking union, they overcame the crisis and made monetary union more resilient.

The EFSF and ESM are dedicated to safeguarding the stability of the euro area and its members by providing financial assistance to those experiencing or threatened by a crisis. The previous crisis underscored the ESM’s value as a crisis-fighting institution and its importance in the euro area landscape.

We are now facing another challenge, one that no country can overcome alone. Again, the ESM is playing an important role in the European response and stands ready to activate the Pandemic Crisis Support credit line should it be required.

European Union (EU) and national action to tackle the coronavirus pandemic and its economic fallout have been vital and unprecedented. The EU economic policy response represents almost €2 trillion. As part of this, the ESM, the European Commission, and the European Investment Bank will issue more common debt on the capital market – an expression of European solidarity and another significant step forward in European integration.

Strengthening the mandate of the ESM will be central to enhancing the resilience of our monetary union. As we begin to recover from the coronavirus crisis, it is perhaps even more essential now that our institutions and structures are capable of meeting the challenges that lie ahead. Therefore, I consider it necessary that we implement the new tasks and responsibilities of the ESM in order to help it develop to its full potential as a crisis resolution mechanism. I am certain that the ESM will continue to play its role in safeguarding the euro for many years to come.

Paschal Donohoe

Chairperson of the ESM Board of Governors

President of the Eurogroup

Minister for Finance, Ireland

Message from the Managing Director

Ten years ago, the temporary EFSF was created to address a crisis where the survival of the currency union was at stake. Some member states faced the loss of market access, while others began to feel spillover effects. As that crisis gathered steam, it became clear that a permanent response was needed. The ESM was created with the mandate to safeguard financial stability for the euro area as a whole and its member states.

With a solid financial base of €80 billion in paid-in capital, €620 billion in callable capital, €500 billion in lending capacity, and the ability to raise money cheaply on the markets, the ESM provided a convincing answer to the crisis that markets had been looking for. Together with its temporary predecessor, the ESM financed six assistance programmes in five countries: Ireland, Greece, Spain, Cyprus, and Portugal. Today, the ESM and its partners look upon the five programme countries as five success stories.

The mandate of safeguarding financial stability does not mention programme countries’ social welfare, but by granting loans to troubled countries when no one else will the ESM allows a country to spread the adjustment burden over several years, thereby easing the pain for citizens.

After a successful first 10 years, we now turn to the future. The ESM is part of the €540 billion European Covid-19 crisis response. The ESM is evolving; like any crisis fund or institution, it is adapting to the circumstances. Our Pandemic Crisis Support credit line demonstrates yet again our commitment to the mandate of safeguarding the euro.

Klaus Regling

Managing Director, European Stability Mechanism

Drive through history in our ESM car

Click on the blue stops along the winding road to explore some of the most memorable moments in the ESM and EFSF’s journey. Enjoy the drive!

10 years

The EFSF, designed as a temporary institution, is established to tackle the unfolding euro sovereign debt crisis and provide emergency financing to euro area member states.

Euro area and EU finance ministers agree a €67 billion financial assistance package for Ireland, which is suffering an economic crisis. The EFSF contributes €17.7 billion, with loans also provided by the European Commission (via its lending facility, the European Financial Stabilisation Mechanism (EFSM)) and the International Monetary Fund (IMF).

EFSF places its first bond, a 5-year, €5 billion issue to fund country loans. Debt issuance is the only source of financing for EFSF and ESM loans, not taxpayer money.

Portugal starts receiving financial assistance from the EFSF, the European Commission (via the EFSM) and the IMF. Each of the institutions provides €26 billion in loans to support Portugal.

The Treaty establishing the ESM is signed by the then 17 euro area member states; the intergovernmental treaty creates a legal basis for a permanent rescue fund for the euro area.

Euro area finance ministers approve a second economic adjustment programme for Greece financed by the EFSF and the IMF. The EFSF eventually disburses €141.8 billion to the country. This differs from the first programme for Greece in 2010, which was a set of bilateral loans between individual euro area member states and the country.

The ESM is inaugurated and starts operating.

Euro area countries give Greece longer to pay off its debt, cut fees, and defer interest payments. Later, they also ease lending conditions for Portugal and Ireland, testimony to euro area solidarity.

The ESM grants its first financial assistance for the recapitalisation of weak banks in Spain. Of the €100 billion in assistance made available, the country draws only €41.3 billion to repair its banking system.

The ESM launches a programme for Cyprus. Though originally foreseen for up to €10 billion, with the ESM contributing €9 billion and the IMF €1 billion, Cyprus needs only €6.3 billion from the ESM in the end.

The temporary EFSF stops accepting new requests for programmes. However, it continues to operate to receive interest and loan repayments, make payments to EFSF bondholders, and refinance outstanding EFSF bonds. The ESM takes over new requests for programmes.

- Ireland completes the loan programme on schedule. Its success demonstrates that the strategy to grant loans in return for reforms not only works but also ultimately rewards countries with faster growth.

- Programme recapitalising Spain’s banking sector is completed. With the help of the ESM, Spanish banks are restructured and strengthened.

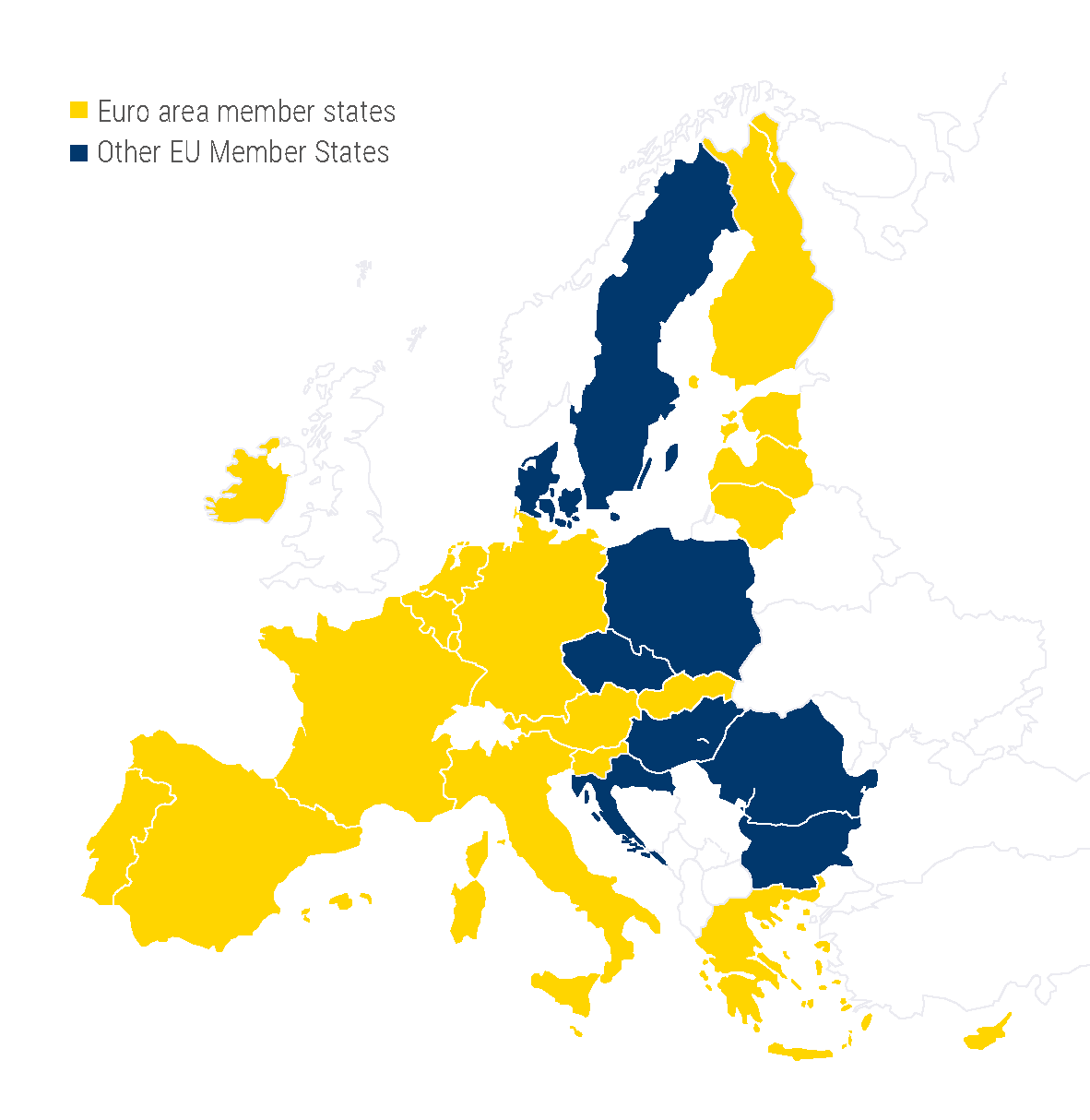

Latvia joins the ESM as first non-founding Member and 18th Member overall.

Founding members fully capitalise the ESM, which reaches the original €80 billion paid-in capital target. Each country contributes according to its population and economic output. The ESM does not use this money to finance its loans. Paid-in capital ensures that the ESM will honour its financial obligations under any circumstances.

Portugal exits the EFSF programme and regains full market access, including a return to regular bond issuance. Portugal has since already paid back its entire loan to the IMF and has started to pay back the EFSF.

Lithuania joins the ESM as 19th Member.

The ESM adopts the third programme for Greece, with up to €86 billion in financial assistance over three years. In the end, the ESM disburses a total €61.9 billion to Greece.

ESM extends its yield curve with its first 40-year bond, after having issued a 30-year bond in October. This allows the ESM to increase the duration of its portfolio and lock in low interest rates, the benefits of which are passed on to ESM’s beneficiary countries.

Cyprus successfully exits the ESM programme. Following programme reforms, Cyprus regains market access and the economy begins to improve.

The EFSF and ESM approve short-term debt relief measures for Greece, by smoothing the EFSF repayment profile, reducing interest rate risk, and waiving the step-up interest rate margin related to the debt buy-back tranche of the second programme for Greece for the year 2017.

The world’s regional rescue funds, or Regional Financing Arrangements (RFAs, hold first annual high-level dialogue.

The first independent evaluation report of EFSF and ESM programmes is published. The report focuses on all five euro area countries that received stability support: Ireland, Portugal, Spain, Cyprus, and the EFSF Greek programme up to its initial expiry in December 2014.

The Eurogroup agrees to medium-term debt relief measures for Greece, with a further abolition of the step-up interest rate margin related to the debt buy-back tranche of the second Greek programme from 2018 onwards; a further deferral of EFSF interest and amortisation by 10 years; and an extension of the maximum weighted average maturity on the above-mentioned portion of EFSF loans by 10 years.

Greece successfully exits the ESM programme. This marks the end of the largest sovereign assistance package in history, comprising three distinct programmes. Thanks to unprecedented financial support, granted under very favourable terms and linked to policy reforms, Greece is able to modernise its economy and regain the trust of investors.

European leaders endorse wide-ranging measures to deepen EMU that broaden the ESM’s mandate.

ESM publishes its history book: Safeguarding the euro in times of crisis chronicling the fund’s inception, journey, and political and economic backdrop.

- ESM launches a programme database on its website. This interactive tool enables users to explore a wealth of information on the five financial assistance programme countries in an easy and accessible way.

- ESM issues the first bond under Luxembourg law.

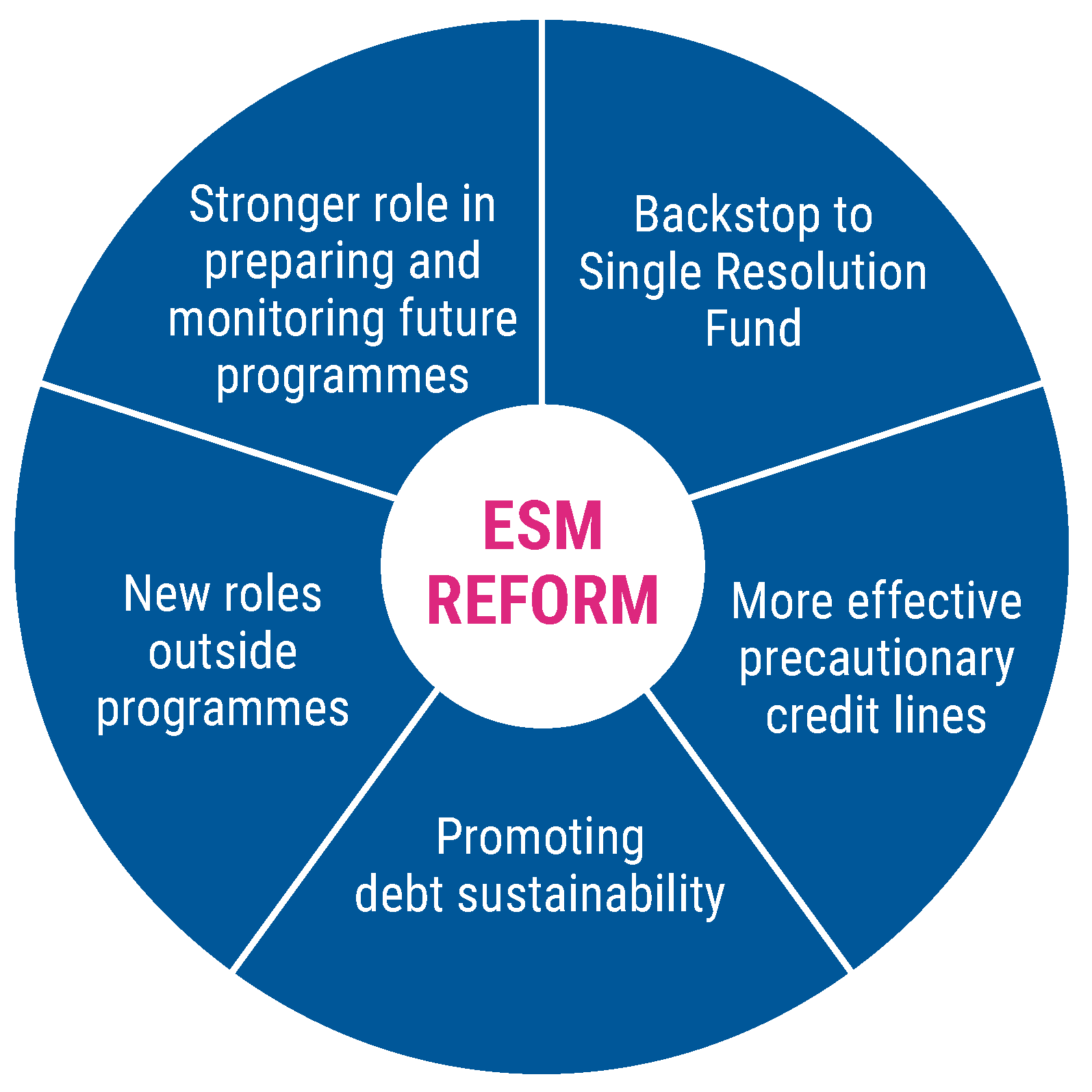

The Eurogroup agrees in principle on ESM reform, subject to the conclusion of national procedures. This includes the further development of ESM instruments, enhancing the ESM’s role, and setting up a common backstop for the Single Resolution Fund.

Coronavirus, the most serious health crisis the world has seen in a century, strikes Europe.

European governments agree on large-scale fiscal and liquidity measures to safeguard jobs, social safety nets, and companies. The ESM’s contribution to the European crisis response is the Pandemic Crisis Support credit line.

Euro area ministers approve ESM’s Pandemic Crisis Support credit line, as part of the overall EU response to protect workers, companies, and sovereigns.

Evaluation report on EFSF and ESM Financial Assistance to Greece is published. It primarily focuses on the ESM programme from 2015 to 2018, while taking into account the preceding EFSF programme and the post-programme developments up to end-September 2019.