The geopolitics of European financial markets - speech by Rolf Strauch

Rolf Strauch, ESM Chief Economist

“The geopolitics of European financial markets”[1]

Investmentforum

Salzburg, 27 March 2019

(Please check against delivery)

Dear ladies and gentlemen,

I am happy to speak today in this impressive, historical hall. It is a great setting to present to you a topic, which is perhaps no less important and impressive for you as investors: the euro and its role in the international monetary system.

From the beginning, the euro has been a project to advance Europe in the global economy. That is why the external dimension, i.e. the international role, has always been important for the European currency. The euro is a symbol of European unity on the world stage. It is a tool to secure global standing, to contribute to the stability of the global economy and the international financial system.

It is the mandate of the European Stability Mechanism (ESM) to ensure financial stability in the euro area. As an international issuer and as part of the global financial safety net, the ESM has an interest in a stronger international role of the euro.

I will speak about the international role of the euro and the developments that increase the strategic importance of the geopolitics of European financial markets. A more important role of the euro and that of the European financial infrastructure is worth pursuing as it carries a number of benefits. Overall, it can enhance the economic sovereignty and resilience of the euro area, increases the ability to counteract potential financial or trade policy actions from other international powers, and contributes to a stable international financial system. Before I conclude, I will outline what measures are currently being discussed that aim at increasing the importance of the euro and the European financial markets.

The euro is a strong second

While the euro is a young currency, it is the world’s second-most important currency after the US dollar. The euro is used in around 36% of international payments, just behind the dollar with almost 40%. This is above the weight of the euro area in international trade. Currently the euro area jointly contributes about 26% to global exports of goods.

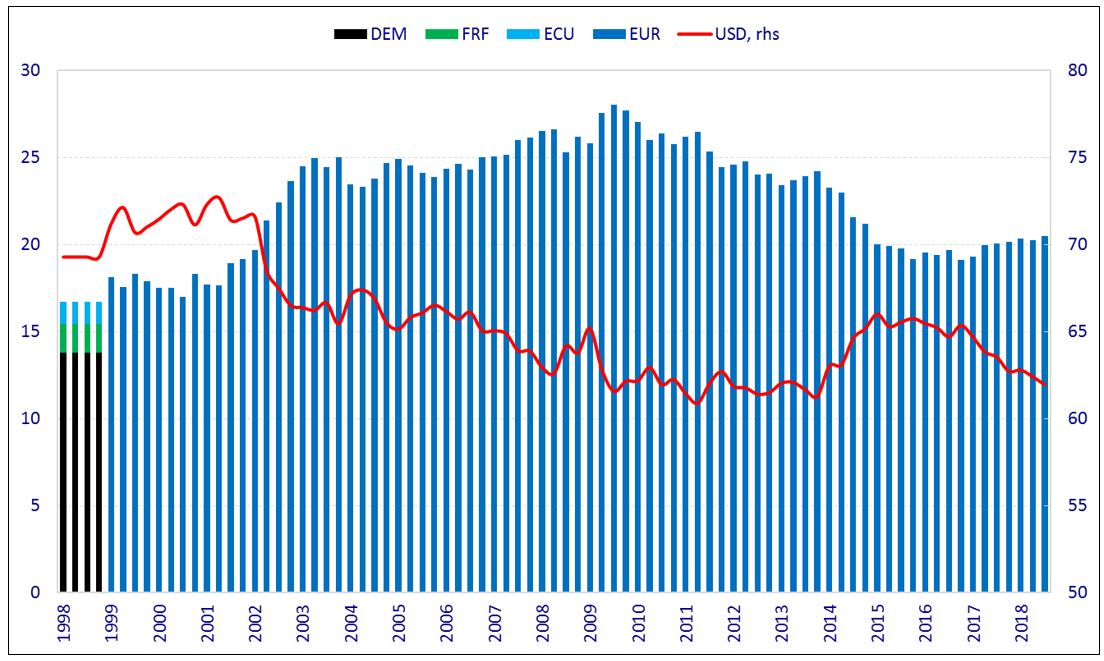

Despite this, the role of the euro suffered during the euro crisis. As a result, it is no longer stronger than the “sum of its parts”. Looking at Graph 1, the German Deutsch Mark and the franc comprised slightly more than 15% of global reserves before the introduction of the euro. The euro’s share rose to 27% until 2007, implying a 10% “euro area premium.” The crisis precipitated a reduction in the euro’s share of foreign exchange reserves to 20%.

Graph 1: Shares of Allocated Foreign Exchange (FX) Reserves (%)

Source: ESM based on IMF currency composition of official foreign exchange reserves (COFER) data.

In the meantime, the US dollar punches strongly above its weight, particularly as a reserve currency and when it comes to global debt issuance. This development was not only driven by emerging markets accumulating reserves, but also by other countries’ dollar-denominated debt.

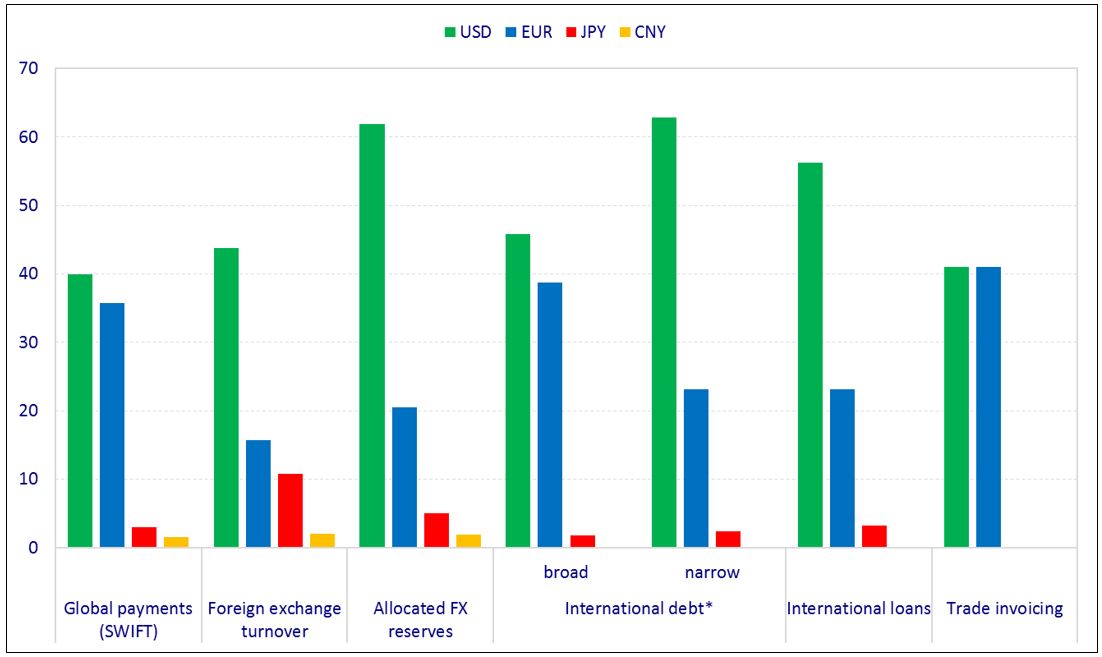

Graph 2: The international role of the euro (shares in %)

Source: BIS, ECB, IMF, SWIFT latest available and Gopinath, Gita (2016), “The International Price System.” Jackson Hole Symposium Proceedings.

Note: "Broad” definition includes domestic issuance of international debt, while “narrow” definition is based on foreign currency principle.

Also in foreign exchange trading, the euro lags behind: the proportion of foreign exchange trading is 44% in dollars but only 16% in euros (see Graph 2). Foreign exchange markets are dominated by US banks. And when it comes to conversion of foreign currencies to euros, triangulation via the US dollar is still common, as it’s cheaper in many cases and as the Dollar market is more liquid.

New landscape: Geopolitical uncertainty and technological trends

We are now confronted with new challenges. Strengthening the role of the euro and European financial markets matters as the geopolitical, technological, and financial landscape are changing.

First, we face a retreat from multilateralism with the political stance of the US. In the current geopolitical environment, financially strong emerging economies such as China may use their financial power to advance political and strategic objectives. And also the US may use its financial strength for foreign policy purposes. Therefore it was necessary, for example, to build a parallel payment vehicle in Europe in order to offset US sanctions that are not in line with a multilateral agreement to which Europe adheres.

Second, over the past decades we have observed how a small number of firms in the IT sector can dominate services on a global scale. Large companies are building up their own sales networks and payment services, and they are also entering the financial sector as service providers (e.g., retail payments). In emerging markets, sales platforms now offer loans and enter financial intermediation. This development seems important, along with the emergence of the fin-tech industry. We know that these companies can hoard considerable amounts of information about clients. And information means market power, when it can be analysed with the support of artificial intelligence. At the same time, the strong EU data protection laws seem ineffective as long as the data are stored outside the EU, and foreign jurisdictions reserve the right to have access to these data.

Third, the European financial sector is at a crossroads. A decade after the financial crisis, the banking sector is much safer thanks to higher capital ratios, improved regulation and institutional infrastructure, but it still faces major challenges. Although European bank profits in 2018 were the best since 2007, on average banks still do not cover their cost of equity. The low interest rate environment, volatility in banks’ revenues from financial markets, increased competition from new entrants like FinTech and BigTech companies and high operating costs have made banks’ business models outdated and depress profitability. Despite the good progress in the reduction of the stock of non-performing loans (NPLs) in the euro area, the level of NPLs in some euro area countries remains elevated and negatively affects banks’ profitability.

Benefits of a global reserve currency

I would argue that strengthening the international role of the euro and our European financial infrastructure also matters to you, as institutional investors. Let me list a few benefits of a global reserve currency:

A reserve currency can ensure more stable financing. International currency issuers can build on a broader investor’s base and issue debt to non-resident investors. This means lower interest costs also for the European economy. At the same time, a stronger role as global reserve currency helps to stabilise demand over time.

A stronger international role of the euro can lead to efficiency gains. Scale effects in financial intermediation can lead to lower transaction costs. Size and liquidity effects may support the financial sector.

Reserve currencies can provide insulation from exchange rate shocks. If imports are invoiced in the domestic currency, exchange rate pass-through to domestic prices declines. In other words, a lower percentage of exchange rate changes is passed-through into destination market prices. At the same time, the risk to companies in global trade is reduced.

I think Europe should try to reap these benefits. Moving towards a multipolar currency system, in which several currencies have a comparable role, including the dollar, euro and over time the renminbi, could improve the functioning of the international monetary system. A balanced multipolar system is less prone to the economic fluctuations of a single reserve currency because it offers options for diversification.

What can be done to strengthen the role of the euro?

The global role of a currency effectively relies on two characteristics, namely stability and liquidity.

Stability

We need to ensure stability by improving the resilience of the Economic and Monetary Union (EMU). European interest in the international role of the euro intensified in 2018. It is part of the reform initiatives to deepen monetary union and to strengthen European integration. Europe is implementing decisions to further deepen the monetary union, complete banking union, to strengthen the ESM and to develop new fiscal tools.

Completing banking union is an essential step, but not enough. Although banks are safer, they need to adapt business models to compete effectively with new market entrants and to operate in a more harmonised banking market. Barriers to cross-border banking should be reduced and removed to promote a more integrated banking union. When providing financing to the real economy, resilient banks can act as investors in capital markets and advance new technologies. That is why Europe has to move towards a broader financial union. More integrated financial markets will be more resilient to external interference.

Reform initiatives: What does this mean for the ESM?

First, the ESM will take on the role of a backstop in bank resolutions carried out by the Single Resolution Board (SRB). This is an important step forward in the completion of banking union.

Second, the ESM will play a stronger role in future economic adjustment programmes.

Third, the ESM’s toolbox is modified to make precautionary credit lines more effective.

And fourth, the December Euro Summit decided to strengthen the role of the ESM in matters of debt sustainability.

In addition, the Summit mandated the Eurogroup to work in two areas where Member States have very different views so far: The completion of banking union through a common European deposit insurance and a euro area budget.

Introducing a European deposit insurance scheme to complete the banking union would reduce the overall risk and the costs of any crisis we would face because it lowers the risk of bank runs. Looking back, in the past crisis, a significant amount of ESM loans had to be used for banks suffering also from liquidity losses through deposit outflows.

But before a European deposit insurance can be introduced, legacy problems must be tackled first. This includes a further reduction in NPLs and a reduction of the high proportion of domestic government bonds in bank balance sheets.

Alongside the European deposit insurance, a capital markets union (CMU) would add to the euro area’s resilience by diversifying funding sources. I will come back to this topic in a moment.

Regarding the euro area budget, the Summit mandated “the Eurogroup to work on the design, the modalities of implementation and timing of a budgetary instrument for convergence and competitiveness”.

This is a positive step in my view as it will encourage structural reforms and strengthen competitiveness in the euro member states. This will also enhance the resilience of the monetary union as a whole. Details of this budgetary instrument are currently being worked out, the financial amount is undecided for the time being. It is clear that this instrument will be developed in the context of the EU multiannual financial framework.

In our view, it is important that the budget can also serve to counteract asymmetric shocks and help stabilising economies in the short run. Following the European elections, we can hopefully broaden the discussion to consider a revision of the fiscal rules, to make them more effective, and a stabilisation facility at the euro area level operating outside a crisis situation. But this is beyond the current political mandate.

Liquidity

Deep and liquid markets are another crucial characteristic supporting the status of a currency. Financial markets in the EU are far smaller and less liquid than those in the US, as well as more fragmented. There are 19 national financial markets today in the monetary union, not one integrated market. This prevents risk-sharing across the markets, which works in the US and ensures macroeconomic stabilisation.

As a result of the crisis, investors do not look at the euro area as a whole but rather at individual countries. Without more integrated and liquid financial markets, the euro cannot take a stronger role in the global currency system. More open and liquid European financial markets go hand in hand with a stronger international role of the euro.

There are a number of policy initiatives to reinforce the European financial sector.

One of them is the capital markets union I mentioned a moment ago. The capital markets union would help to create a deep and liquid market for euro-denominated assets, such as equities and other financial products. As part of this agenda, bankruptcy, tax and corporate laws need to be harmonised. This is a complex, but necessary, process that will eventually encourage cross-border investment and open up new ways to finance businesses.

Stronger demand for euro assets – internally and globally – is a necessary precondition for a stronger international role of the euro. The US capital market is also more sizable because people invest more savings on the capital market. By contrast, euro area pensions are less capitalised and pension funds play a lesser role. If pension funds could see stronger demand, capital market size would increase in the euro area. In addition, incentives for Asian investors to invest in euro bonds may strengthen the role of the euro.

Europe also has to be open to capital from abroad. Global investors often used the City of London as a gateway to European financial markets, but this is challenged by Brexit. Euro area financial centres have to be ready for the forthcoming changes. It implies strategic decision as to which areas of the financial markets should remain in London and which alternative financial structures should be set up in the euro area.

Expanding the supply of European safe assets could also strengthen the global role of the euro in the long run. At the moment, German Bunds are effectively the most important safe asset in the euro area, followed perhaps by bonds from a few other highly rated sovereigns and supranationals, such as the ESM. But that is not enough, particularly now that supply from Germany is continuously declining due to the constitutionally balanced budget rule. As Graph 3 and 4 show, both the outstanding volumes and new issuance of highly rated dollar bonds are much larger.

Graph 3: Outstanding stocks of bonds rated AA- or higher

Source: ESM based on Bloomberg and Dealogic.

A European safe asset would be a crucial step towards integrating Europe’s financial markets. And it would make the euro more attractive for international investors. With a safe asset in the euro area, the safe-haven status of the US government bond market would be less dominant. A European safe asset would also allow Europe’s banks to diversify their sovereign debt portfolio, and attract international capital to Europe.

Graph 4: New bond issues rated AA- or higher

Source: ESM based on Bloomberg and Dealogic.

Sectoral initiatives

The European Commission is looking into market practices for invoicing in dollar-dominated markets, such as aviation and energy. The US dollar dominates a relatively large share of global trade volumes – and this is particular significant in some sectors. In other words, exporters choose to invoice their products in dollars, even when the US is not a party to the transaction. The share of trade invoiced in dollars exceeds the amount of trade with the US in most countries. Dollar invoicing tends to be the highest for trade in commodities and among less developed economies.

There is no apparent regulatory, legal or accounting obstacle to a broader use of the euro in payment transactions. And still, the difference remains striking. More than 90% of US imports are invoiced in US dollars, while less than 50% of extra-euro area imports are invoiced in euros. The European Commission is looking into promoting a wider use of the euro in the energy, commodities and aviation sectors. It is clear that the purpose cannot be to regulate and change market behaviour on a large scale if this works safely and efficiently. But there may be some space to try and influence the behaviour of public institutions in this market, which could set the stage for others to follow.

Safety of the financial infrastructure

The infrastructure of European financial markets also needs further development. Europe has a very efficient system for euro payments in central bank money and a central bank money settlement system for the real-time transfers of securities. The systems are, however, limited to payments functions and do not cover the full range of the investment services chain. The services remain splintered, with a multitude of central securities depositories acting according to their own rules, legal provisions, and links to other such depositories and customer banks. This may be a obstacle, particularly for non-European investors and investors in smaller euro area countries.

The primary market for government bond distribution and settlement requires enhanced digital technologies and a comprehensive front-to-end central infrastructure. A single distribution service for public debt issuance would provide greater efficiency, transparency, and lower execution cost, as well as help to drive harmonisation. This infrastructure would allow easier access for investors to EU public debt issuances, independent of the issuer’s location within the euro area. The same would apply to the issuers’ outreach to international investors. Public issuers also need to reduce their dependence on private sector infrastructure, in particular based outside Europe.

A strong infrastructure for public sector issuance would reduce dependence and increase stability of financial markets in times of crisis. The ECB and the ESM are discussing the creation of such modernised primary market infrastructure. It should help to harmonise the primary market for European public debt with other public issuers, banks, and investors.

And finally, Europe should also work to reduce its dependence on a small group of providers that dominate the information technology infrastructure market. This reliance implies systemic and data protection risks. If an outage hits just one company, this could affect the entire system. The market needs to be open to new entrants to become more diverse and competitive.

Conclusion

Let me conclude. The euro is a strong second when it comes to the role of the reserve currency. Despite being a young currency, it has already weathered two crises. We now face geopolitical, technical and financial challenges that heighten our awareness regarding the benefits of a strong international role of the euro and a safe infrastructure for European financial markets.

I have outlined a few policy actions that can be done.

It is important to continue deepening the Economic and Monetary Union, completing banking union and opening up capital markets, because our economic weight in the world continues to decline. Europeans should work together, to ensure their influence in the future. The benefits resulting from a stronger international role of the euro are convincing in my view.

Thank you.

References:

Efstathiou, K. and Papadia, F. (2018). The Euro as an international currency, Bruegel policy contribution issue n°25, December 2018. Available at: https://bit.ly/2CsS1FB

European Central Bank (2018). Strengthening the European financial industry amid disruptive global challenges, speech by Yves Mersch, 3 September 2018. Available at: https://bit.ly/2Pu1AbK

European Central Bank (2019). The euro’s global role in a changing world: a monetary policy perspective, speech by Benoît Cœuré, 15 February 2019. Available at: https://bit.ly/2YfWCEH

European Commission (2018). Deepening Europe’s economic and monetary union, factsheet. Available at: https://bit.ly/2FjoHCe

Gita, G. (2016). The International Price System. In Jackson Hole Symposium Proceedings.

Author

Contacts