How the euro area overcame fragmentation during the pandemic

Europe has successfully overcome the economic fallout from the pandemic. By banding together and relying on its improved crisis resolution architecture, the euro area successfully protected financial and economic stability and set the economy back on the road to recovery.

In this blog, we outline how the institutional efforts like those by the European Central Bank (ECB), were instrumental in containing the risks of financial instability in the euro area during the pandemic.

How the ECB helped to contain fragmentation, a key challenge for the euro area, during the pandemic and what lessons can be drawn upon for the future are explored in a recent ESM working paper.

Sometimes a shock is so sudden and severe that financial markets need immediate large-scale intervention. Especially when the shock has little to do with domestic fundamentals, as was the case with the Covid-19 pandemic. Investors promptly shed assets that were deemed risky, market liquidity dried up, and borrowing costs across members states diverged abruptly.

In response, the ECB, along with national central banks, embarked on asset purchases on an unprecedented scale and pace. The ECB augmented the pre-existing Asset Purchase Programme and launched the Pandemic Emergency Purchase Programme (PEPP).[1] In March 2020, the Governing Council announced a €750 billion envelope to purchase private and public sector securities, which was subsequently increased by €600 billion on 4 June 2020 and by €500 billion on 10 December that year to reach €1,850 billion in total.

The ECB's asset purchases, along with the broader European policy response, helped reduce market uncertainty and prevented fragmentation. Our working paper documents the PEPP’s impact on euro area sovereign spreads – the difference in borrowing costs of sovereigns – which is the most common measure of fragmentation.

The PEPP came with much more flexibility than the ECB’s previous asset purchase programmes in terms of pace, composition, and maturity of purchases. To better understand the impact of the asset purchases on financial markets, we exploited this variability and traced their effects over time and across countries from the moment rumours start circulating about possible intervention through the day of announcement and to actual implementation.

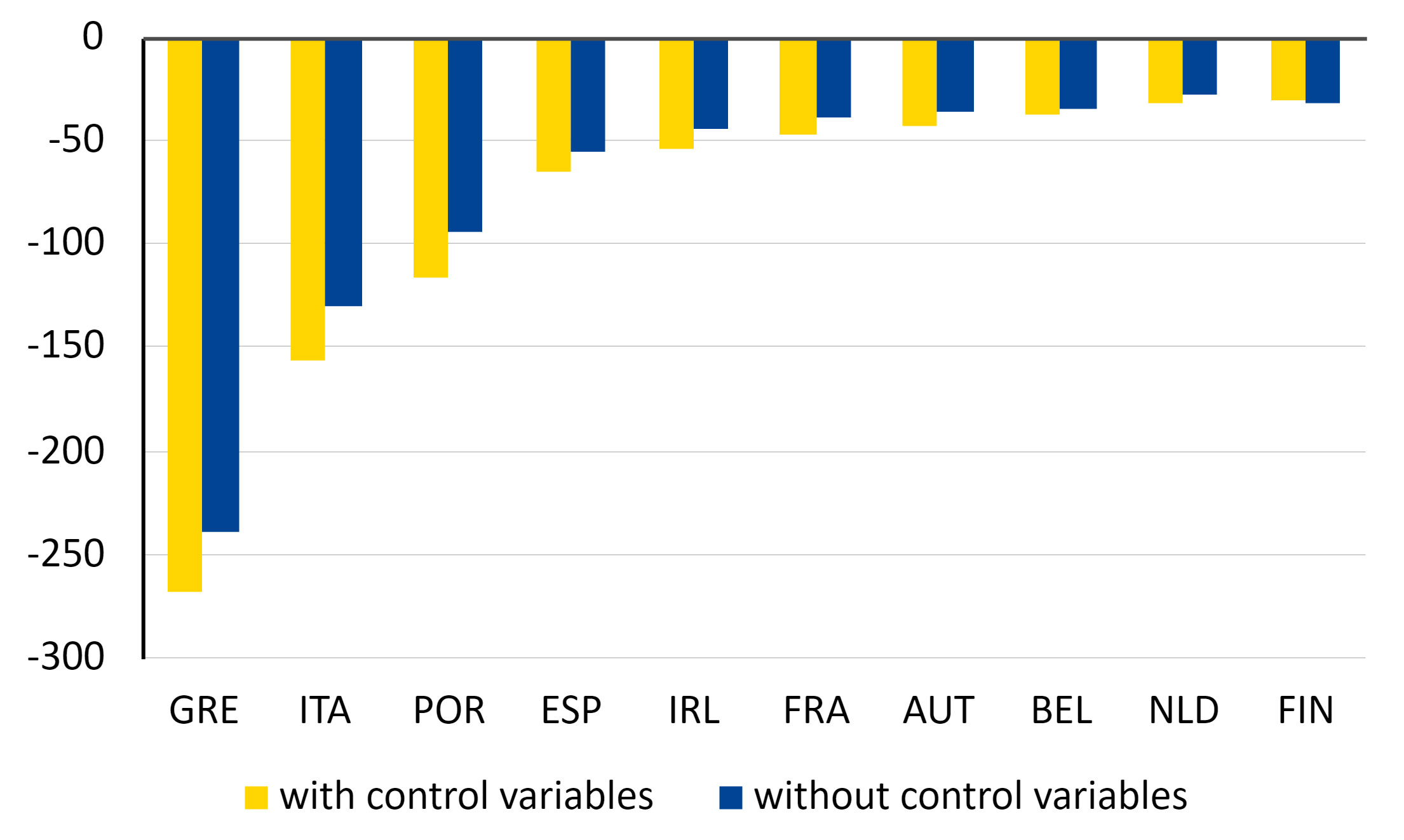

We found that ECB asset purchases were indeed instrumental in reducing the difference between the borrowing costs of member states (Figure 1). However, this impact changed over time and across countries. The impact was largest on days of public announcements about the asset purchases, and countries with lower credit ratings witnessed larger declines in spreads.

Figure 1: Cumulative impact of ECB asset purchase announcements on 10-year sovereign bond spreads vs German Bunds

(basis points)

Source: ESM based on Bloomberg data

Notes: The cumulative effect is measured from the coefficient beta of the OLS regression on event dates as in equation (1) of the Working Paper for each country. The estimates are based on two different specifications: with and without the control variables described in the previous section. Detailed country regression results are in the Annex of the working paper.

Expectations about the final size of ECB asset purchases (‘the stock’) and realised purchases (‘the flow’) both affected spreads. But both effects were transient and mainly materialised in the first few weeks following the inception of the PEPP, when financial markets were under stress.

The ECB’s new tool, along with the broader European policy response to the pandemic, quickly established credibility. Following the initial period of heavy ECB intervention, the additional impact of purchases became smaller. The ECB, along with the measures taken by other European institutions, guided market beliefs to a “good equilibrium.” Worries about self-fulfilling debt crises had been dispelled, and financial markets stabilised.

This experience is reminiscent of 2012, when the establishment of the ESM and the announcement of the ECB’s Outright Monetary Transaction tool, which is linked to an appropriate ESM instrument, helped stabilise financial markets. The euro area’s institutional framework has showed time and again that it can address the risk of market tensions, reduce volatility, ensure sovereigns’ market access, and thereby help in various ways to safeguard financial stability in the entire euro area both against domestic and external shocks.

Acknowledgements

The authors would like to thank Cédric Crelo, George Matlock and Rolf Strauch who contributed to this blog post.

Further reading

Placing a new value on EFSF bond prices

Navigating the euro area through a slowing global economy

How ESM’s AAA bonds weathered the pandemic storm

Outside of the Box: Euro a magnet for central banks, again

How Europe’s pandemic response reduced market uncertainty

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors