How Europe’s pandemic response reduced market uncertainty

The eruption of the Covid-19 pandemic resulted in large market movements, as investors feared the financial and economic consequences of the crisis. A swift European policy response restored market confidence, and data from the fixed-income options market has vividly demonstrated this return to stability.

Implied uncertainty in European government bond futures, extracted from option prices, has declined sharply since March, following rapid and powerful European Central Bank (ECB) intervention and a coordinated fiscal response at national and European level. The range of probable outcomes for long-term yields, extracted from option prices, has narrowed, and market uncertainty, as measured by new implied volatility indices for European bond markets, has returned to low, pre-pandemic levels. This blog is based on a recent ESM Working Paper, where my co-author Jan Voříšek and I describe some practical ways to measure bond market uncertainty using options, and discuss how this could be useful for investors.

Why measuring uncertainty matters

Market prices reflect where supply and demand meet. However, they do not reveal what different buyers and sellers may be anticipating. Individual investors have diverse views which market prices aggregate and show as an average. The level of conviction about expectations varies in time as well. Sometimes larger price moves are expected, other times prices are expected to remain stable. This anticipated market volatility cannot be observed directly in bond or equity prices either. Option prices can shed light on these blind spots. Options have desirable features: they are forward-looking, they show how much market uncertainty is priced in, and they capture the whole range of outcomes, from less to more probable.

In this blog, we look at the impact of recent policy measures on market implied uncertainty, based on option prices, and introduce new volatility indices, which measure implied volatility in the European government bond futures market. We show that the European policy response to the pandemic restored confidence and brought calm to the market at record speed.

March spike in uncertainty quickly recovered

When the ECB announced its unscheduled bond-buying package[1] on 18 March 2020 to support countries and economies hit by the pandemic, an impressive risk rally followed. Government bond yields dropped and the difference between the yields of euro area countries’ bonds contracted sharply. One less frequently monitored part of financial markets, the options market, staged an even more striking recovery.

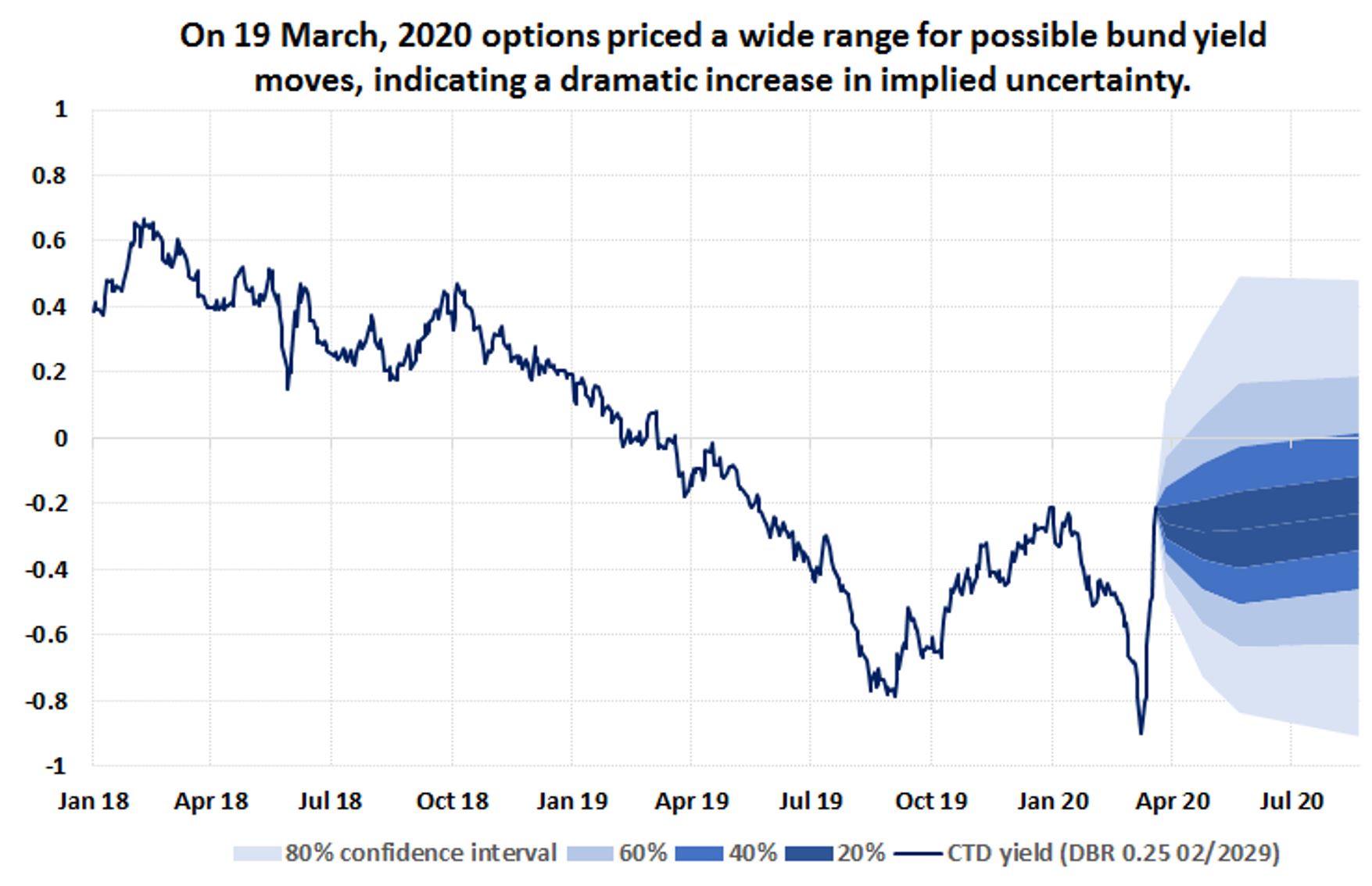

During a dramatic market decline in March, option-implied uncertainty in long-term German bond futures reached a multi-year peak. At the height of the crisis, options maturing on 24 April 2020, about one month ahead, showed the range of possible moves in Bund yields - the benchmark yield for the euro area - between +27 basis points and -35 basis points, with 60% probability. At 80% probability, the range spanned over 100 basis points. Such uncertainty suggests that the market experienced a tail risk event in March (Figure 1).

Figure 1: Historical cheapest-to-deliver bond yield of Bund futures and their option-implied quantiles as of 19 March 2020.

Source: Bloomberg, authors’ calculations.

Many parts of the financial market were temporarily disrupted in March as investors rushed into cash and short-term safe and liquid assets. The ECB successfully launched a number of flexible measures to restore market functioning and to provide liquidity to both shorter and longer-term funding markets.[2] The measures in concert achieved the goal of calming markets, decreasing volatility, and easing financial conditions.

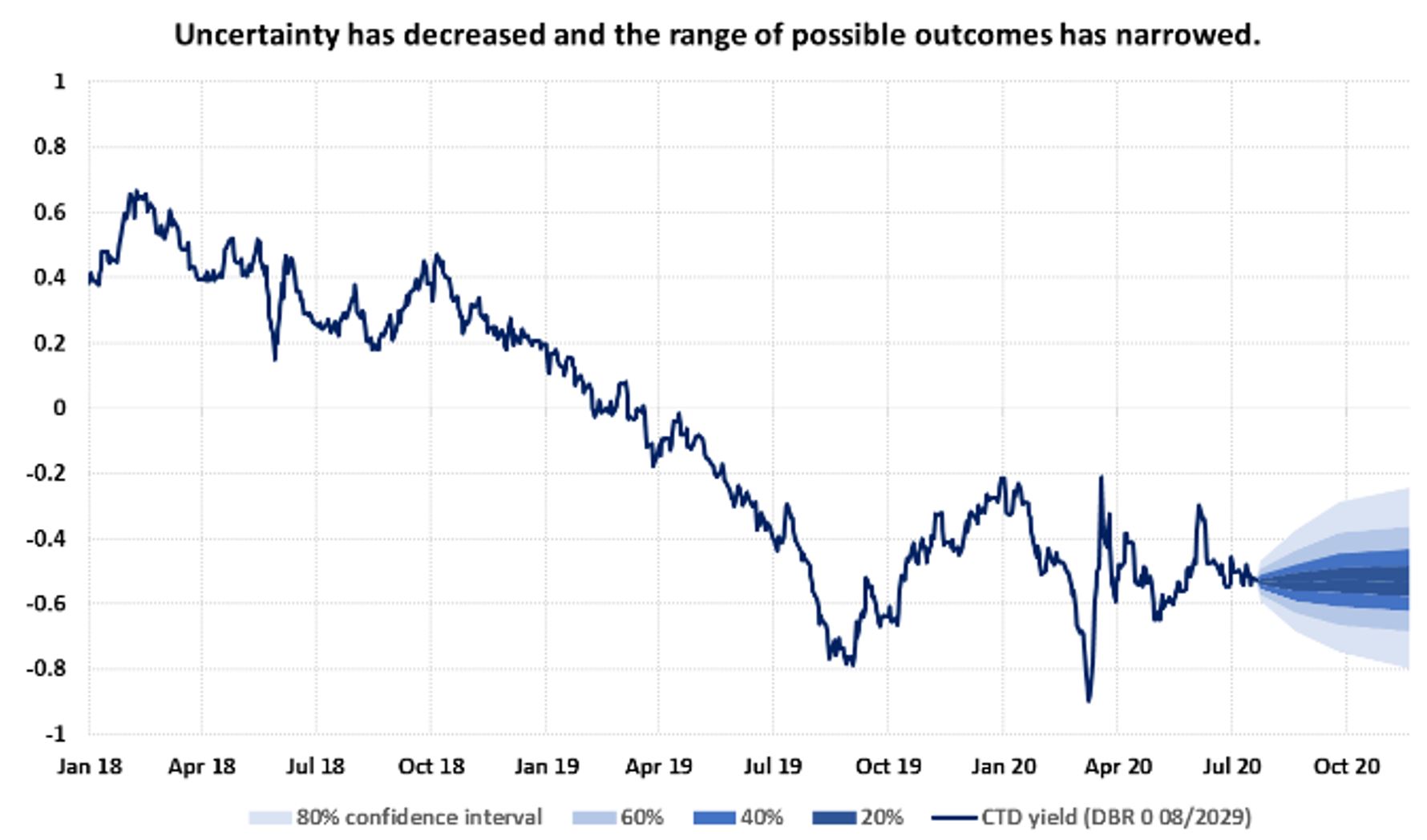

Implied uncertainty receded as quickly as it jumped. In less than three months, it reversed most of its upward move. It is back to its low, pre-pandemic levels. On 20 July the range of future outcomes, as priced by the option market (Figure 2), narrowed markedly, suggesting relative calm expectations despite uncertainty about the speed and shape of the ensuing economic recovery. For options maturing on 21 August 2020, about one month ahead, the range of possible moves in Bund yields narrowed to -10 and +9 basis points, with 60% probability. The distribution became almost symmetrical, pricing roughly equal chances of rising and falling Bund yields.

Figure 2: Historical cheapest-to-deliver bond yield of Bund futures and their option-implied quantiles as of 20 July 2020.

Source: Bloomberg, authors’ calculations.

The speed of the market reaction highlights, in many ways, the progress made by the euro area since the previous crisis to react quickly and decisively to bring back market confidence.

New European government bond volatility indices

Figures above help us visualise probabilities associated with future outcomes at different option maturities. We proposed new volatility indices for European government bond futures in our recent ESM Working Paper, in order to condense option-implied uncertainty into a single forward-looking measure. Volatility indices, built upon the VIX methodology, have become popular measures of short-term market uncertainty across a range of underlying asset classes such as equities, foreign exchange, or commodities. VIX methodology reigns as the most popular measure of market-implied volatility, but it is specific to US equities and derived from options on S&P 500 index. We expanded the family of volatility indices to track implied volatility of European government bonds.

Active exchange-traded option markets exist for German, French, and Italian government bond futures. We utilised these options to construct new volatility indices, which reflect market pricing of subsequently realised volatility, over the next 30 days. For example, Bund volatility index, a “Bund VIX equivalent”, tracks the implied volatility of Bund futures over the next 30 days using out-of-the-money options. To help interpretation, we expressed these indices in basis points annualised, corresponding to the underlying security of the bond future.

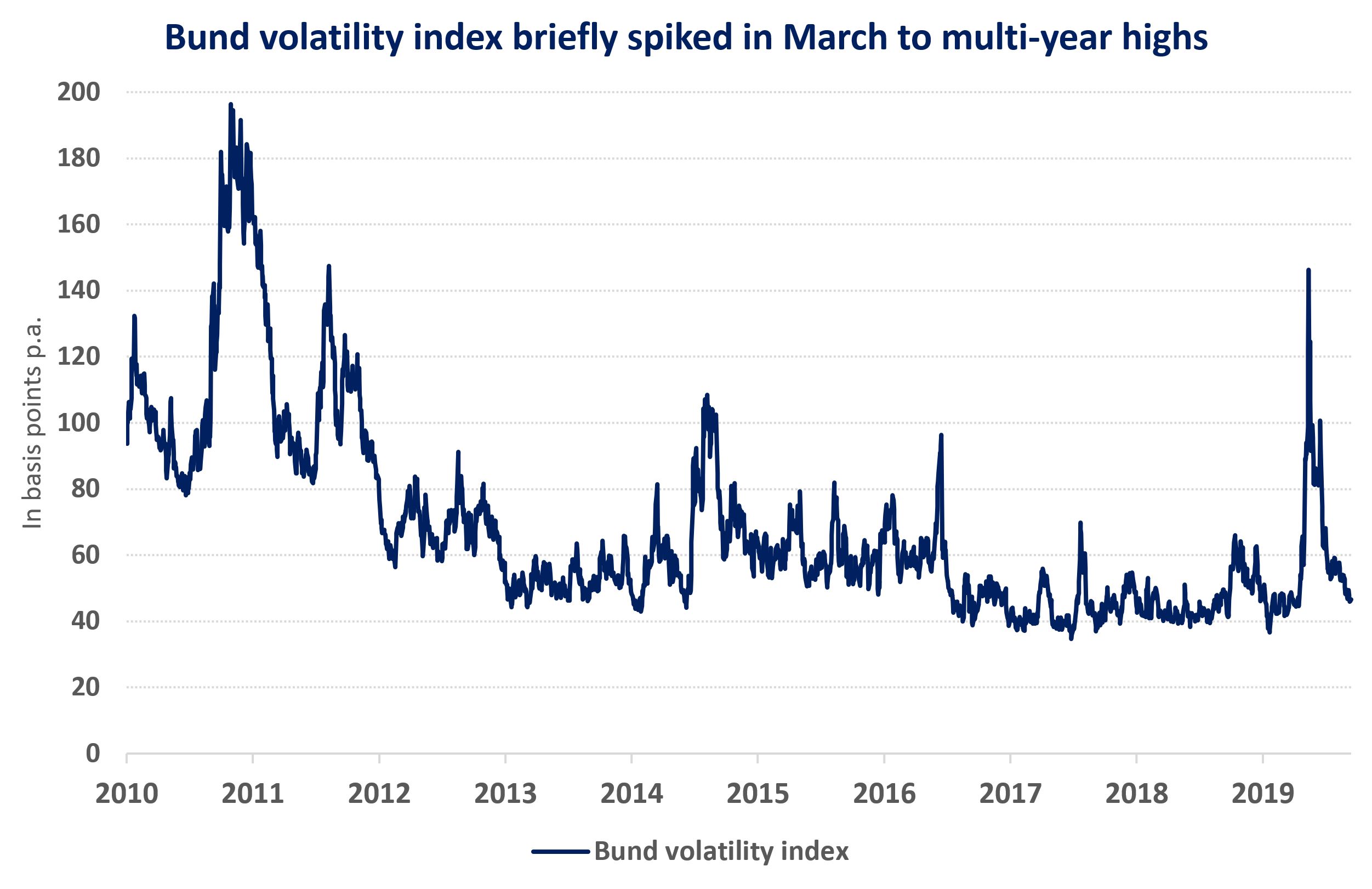

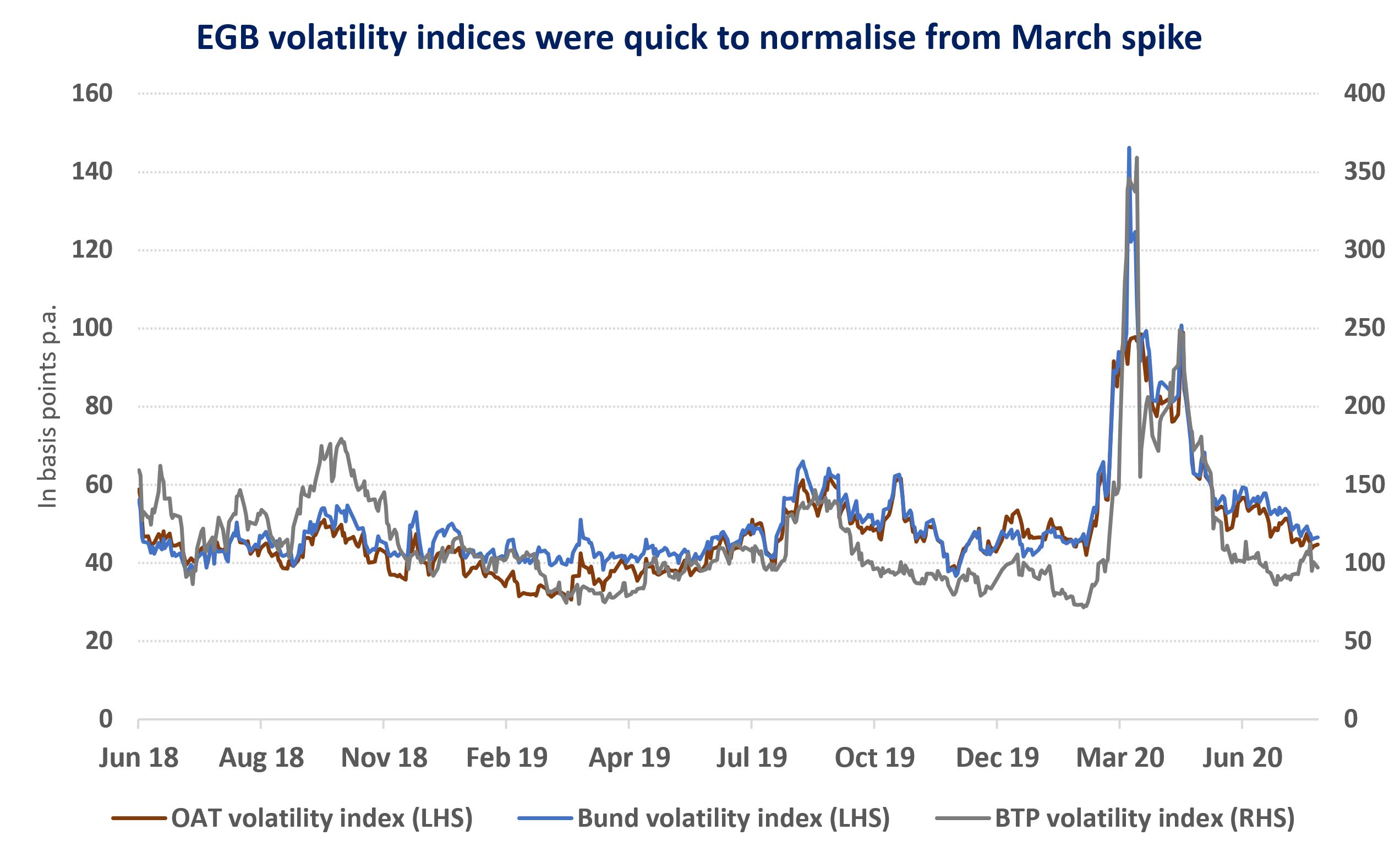

Bund volatility index briefly spiked in March to the highest level seen since the European debt crisis a decade ago, as Figure 3 shows. But this time, thanks to prompt and substantial liquidity support from the ECB as well as fiscal responses on national and European level, volatility was quick to recede and normalise. Volatility index for Italy jumped by similar magnitude, while in the case of France, volatility was more contained (Figure 4). Currently, option markets are not pricing any excessive Bund yield swings in either direction. The same behaviour is observed for France and Italy. Volatility indices have been trending downwards and reached pre-pandemic lows. Realised volatility has declined together with implied volatility and European government bond yields have recently fluctuated in tight ranges.

Figure 3: Bund volatility index jumped to multi-year highs, and quickly normalised.

Source: Bloomberg, authors’ calculations.

Figure 4: Implied volatility indices for OAT, BTP, and Bund futures are back at pre-pandemic lows

Source: Bloomberg, authors’ calculations.

Prospects for economic recovery and the path for growth and inflation remain uncertain, although they received a major boost with the EU summit’s agreed terms of a new Recovery Fund this week.[3] The high uncertainty around the economic outlook is evident in the broad range of growth projections, and their frequent revisions. Investors will continue to assess carefully how governments respond. Despite high uncertainty around the economic outlook, option markets anticipate the European bond market will remain stable in the near future, and yields are expected to stay in a narrow range. The ECB’s substantial balance sheet expansion and commitment to keep rates low as long as necessary, together with European policy response, effectively compressed volatility and prevented market fragmentation.

Streamlining the implied uncertainty into a single measure, new volatility indices from option prices on German, French, and Italian government bond futures provide insights into investor sentiment and forward-looking market uncertainty in the underlying European sovereign bond market.

Acknowledgement

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author