Why the Covid-19 credit line still makes sense

It is two months since the ESM became part of Europe’s response to the devastating Covid-19 pandemic crisis. Europe agreed that the ESM should provide a credit line worth up to €240 billion to help euro area member states cover healthcare costs related to Covid-19.

In that time, there has been much speculation around which countries would apply, as we identified that 11 of the 19 euros area countries could fund more cheaply via the ESM than by borrowing directly from capital markets.

We made those findings public with an extensive ESM blog published on 3 June, which explained how the new Pandemic Crisis Support credit line works and illustrated how much member states could save by opting for this facility.

Some member states could save up to €6 billion over 10 years, the blog explained at the time. In other words, real cash savings for their taxpayers.

The blog post raised legitimate public interest around how we arrived at those numbers and how loans under Pandemic Crisis Support could attract negative interest rates when our published interest rate is 0.76% on average for loans funded by our Diversified Funding Strategy.

As the ESM’s Chief Financial Officer and the Head of Funding and Investor Relations, we feel it is important to explain the mechanics of how we arrive at these figures - and how market movements can impact them.

First, we need to look at how the Diversified Funding Strategy used for the funding of outstanding loans works.

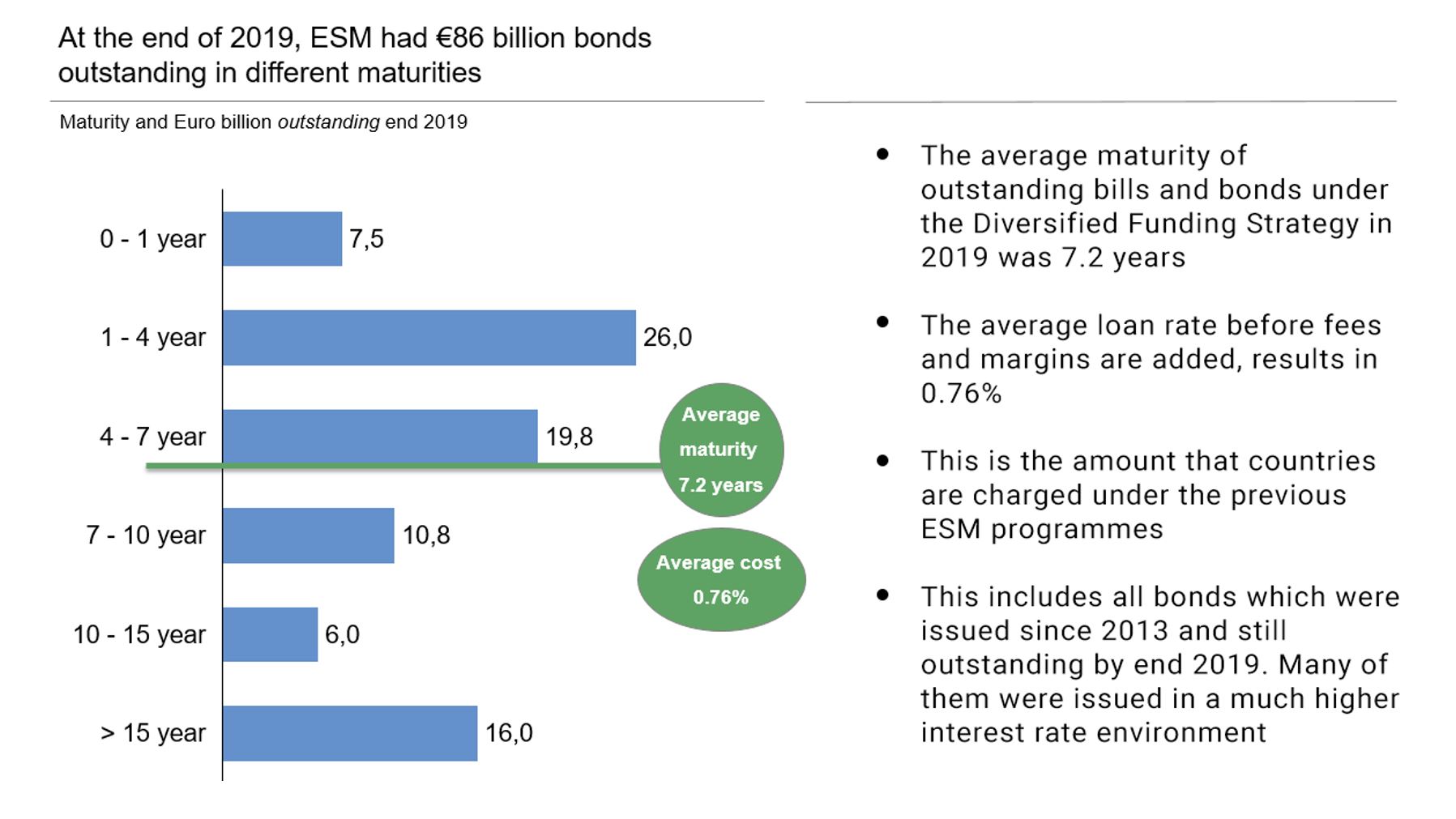

In Table 1 we show how much remains outstanding in bills and bonds and their various maturity dates from those past events. The table shows that the ESM had €86 billion outstanding debt under the Diversified Funding Strategy by the end of 2019, ranging from 3-month bills to 40-year bonds. The table also shows that if you add up all the bills and bonds outstanding, the average maturity comes out at 7.2 years and results in an average lending rate for loans funded under the diversified funding strategy of 0.76%.

It is worth noting this includes all bonds which were issued since 2013 and were still outstanding by end of 2019. Many of them were issued in a much higher interest rate environment as the one we currently see.

Although all the countries have now successfully exited their ESM programmes and become reform champions, the long-term loans are still outstanding and need to be funded. For this reason, the ESM’s current funding activities relate to rolling over maturing bonds that provided the long-term loan money to countries we helped during the sovereign debt crisis a decade ago.

Figure 1. The average maturity of outstanding bills and bonds under the Diversified Funding Strategy end 2019 was 7.2 years

Source: ESM

So how can ESM provide a credit line at negative rates?

In our blog of 3 June, we explained that the ESM would separate the costs for Pandemic Crisis Support from the costs of current outstanding debt.

A silo was set up. This involves the ESM segregating its funding for Covid-19 from the rest of its regular funding operations. As a result, countries will not be charged according to legacy issuance. So the funding costs will be lower because they reflect current interest rates in markets.

In that blog, both 7- and 10-year comparisons were made. Here’s why.

As the Pandemic Crisis Support loans can have an average maturity of up to 10 years, the ESM funding average maturity can be a maximum 10 years.

To finance the credit line, the ESM will issue in a similar way across maturities as it has done so far. The maximum maturity for a single bond is determined by the maximum maturity of a specific loan under the Pandemic Crisis Support.

We also showed an illustration of 7 years because our current funding average maturity is 7.2 years, to be precise.

Financial markets fluctuate, investor demands shift and we always strive to get the best price for our beneficiaries. We showed estimates based on current market rates for the 7- and 10-year maturities compared to bonds issued by ESM shareholders to illustrate the benefits of the Pandemic Crisis Support. For a precise comparison of funding costs, we would need to construct funding strategies for the ESM and the ESM shareholder which are similar and comparable regarding the liquidity risk and interest rate risk they bear. In addition assumptions of future funding conditions for the roll-over of the debt would be needed.

What changed over two months?

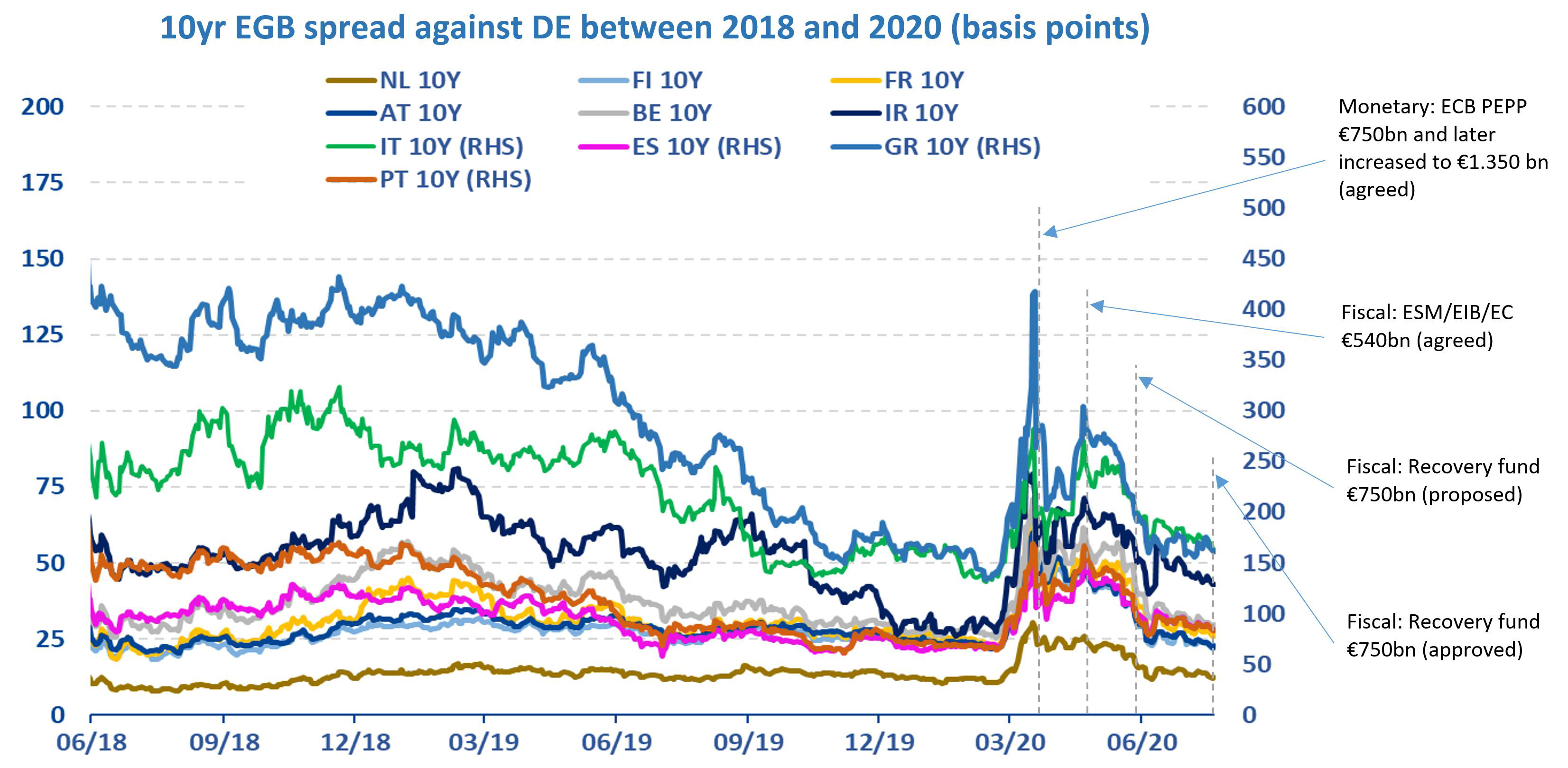

Figure 2: European Government Bond markets calmed down, supported by the European Central Bank and European policy decisions

Source: Bloomberg, ESM

Markets moved since Pandemic Crisis Support was introduced. After tightening in the last two weeks of May following the activation of Pandemic Crisis Support, yield spreads among European government bonds stabilised through June before narrowing further since early July. This was due to the positive market reaction to the European Central Bank’s monetary PEPP bond-buying operations (€750 billion and increased to €1,350 billion) and the European fiscal policy response: a package of measures from the European Commission, European Investment Bank and ESM worth a combined €540 billion as well as the European Recovery and Resilience Fund of €750 billion agreed at the EU summit last week.[1]

A blog from colleagues in ESM Investment and Treasury further illustrated the restoration of calm in markets following Europe’s response to the pandemic crisis.

What’s good for Europe is that the array of policy initiatives calmed markets and made it easier and cheaper for European sovereigns to finance themselves in the market.

So how can the ESM provide a credit line at negative rates?

News that Europe has agreed on the Next Generation EU recovery package, including the Recovery and Resilience Fund, should be widely and deeply welcomed. The initiative is there to help rebuild Europe after the devastation wrought by Covid-19. The market reaction has been positive too, with a further contraction of yields on euro area government bonds as well as reduced spreads versus yields of ESM paper.

What needs to be factored in, however, is that grants and loans from the Recovery and Resilience Fund will only start to flow from 2021.

The ESM’s Pandemic Crisis Support complements that longer-term funding with shorter-term funding that targets the healthcare costs of Covid-19. It can even also serve as bridge finance until the Recovery Fund is available.

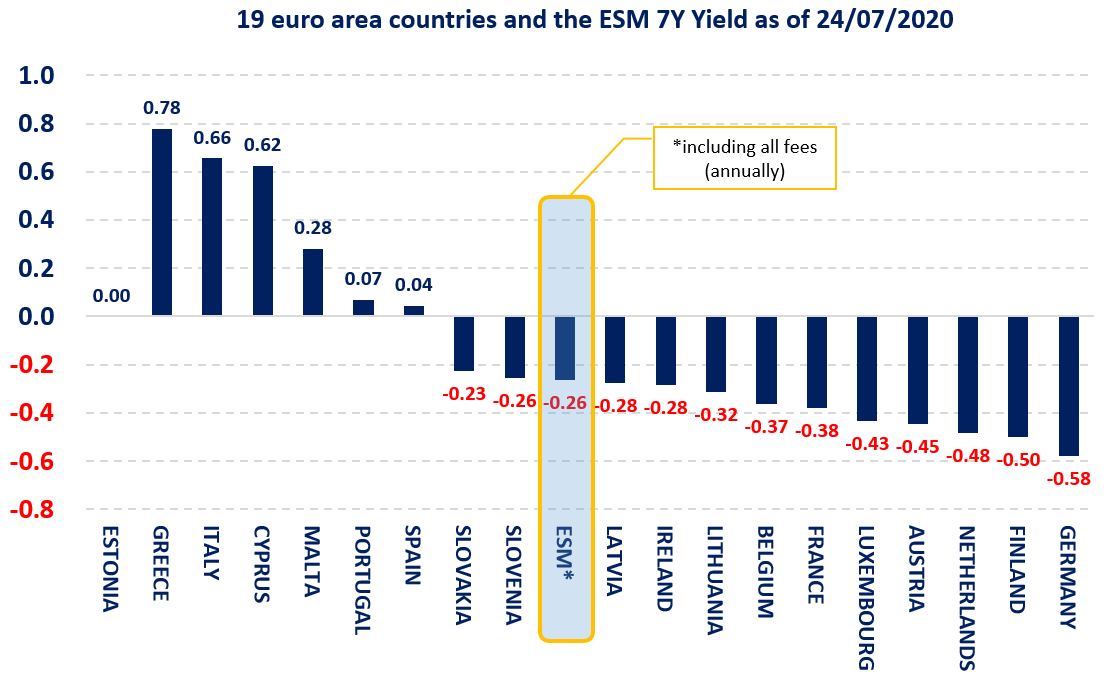

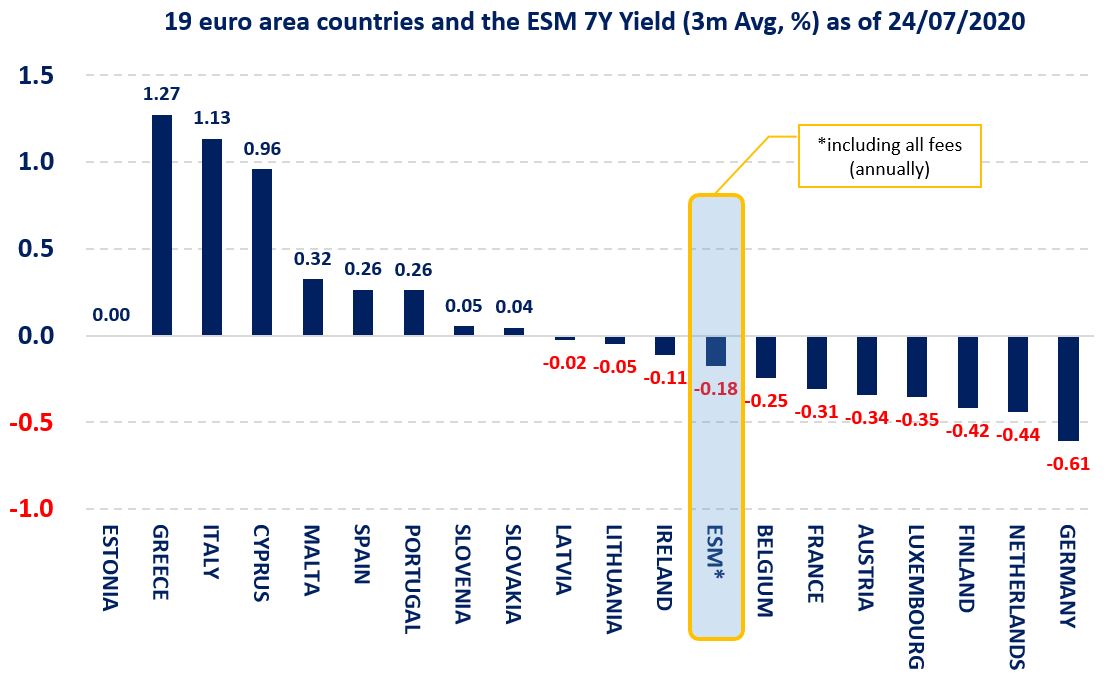

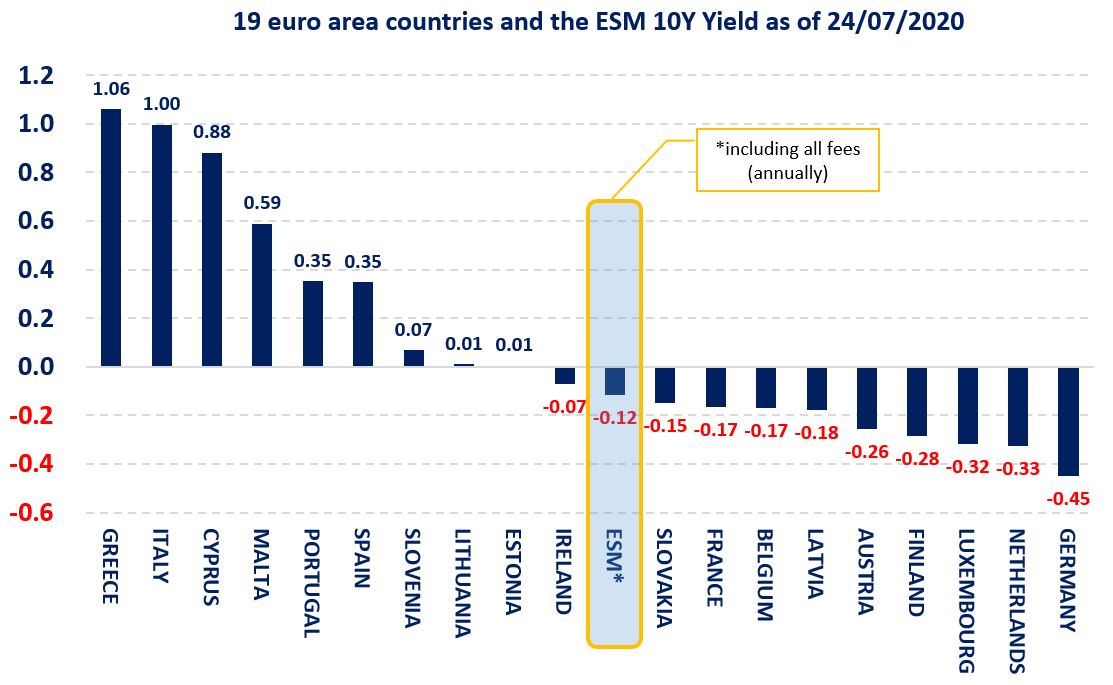

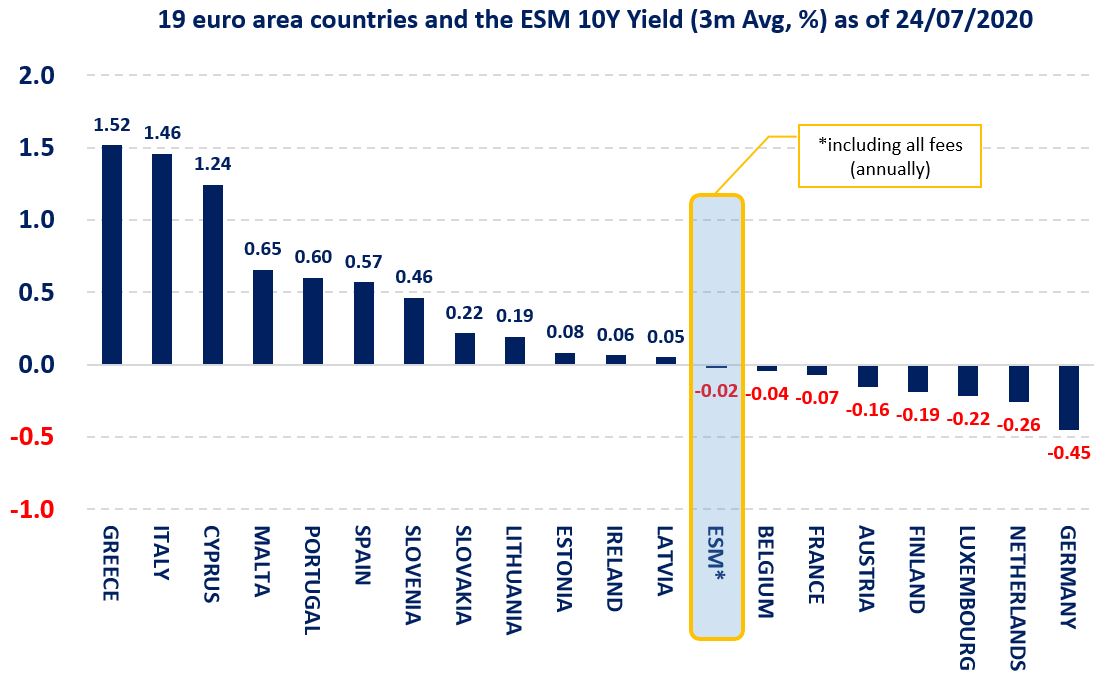

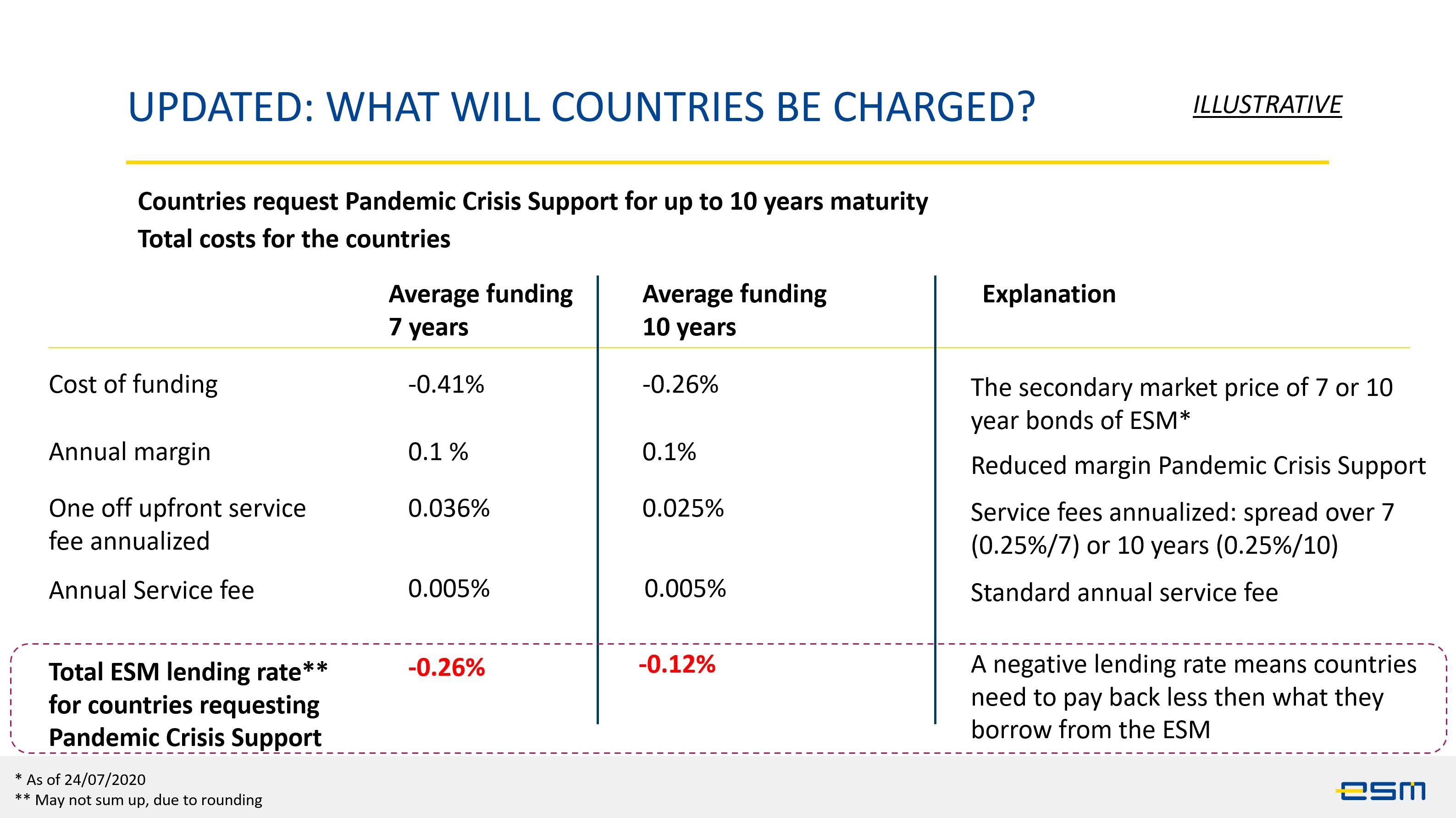

While the cost savings of Pandemic Crisis Support are less than they were two months ago, due to the contracted spreads, the ESM is still attractive for a large number of European sovereigns. In fact, several countries would fund more cheaply via the ESM. With bond yields falling across Europe, ESM yields have also fallen. Whereas in June we could illustrate that for 10 years a borrower would pay zero interest, it is now a negative rate. For illustrative purposes, for an average funding maturity of 7 years, the yield would amount to -0.26% and for 10 years, it would be -0.12%. You can see these updated comparisons in Table 1 below.

Figure 3. Updated Numbers: ESM Pandemic Crisis Support financially attractive for a large number of euro area member states

Source: ESM

Table 1: ESM lending rates fall

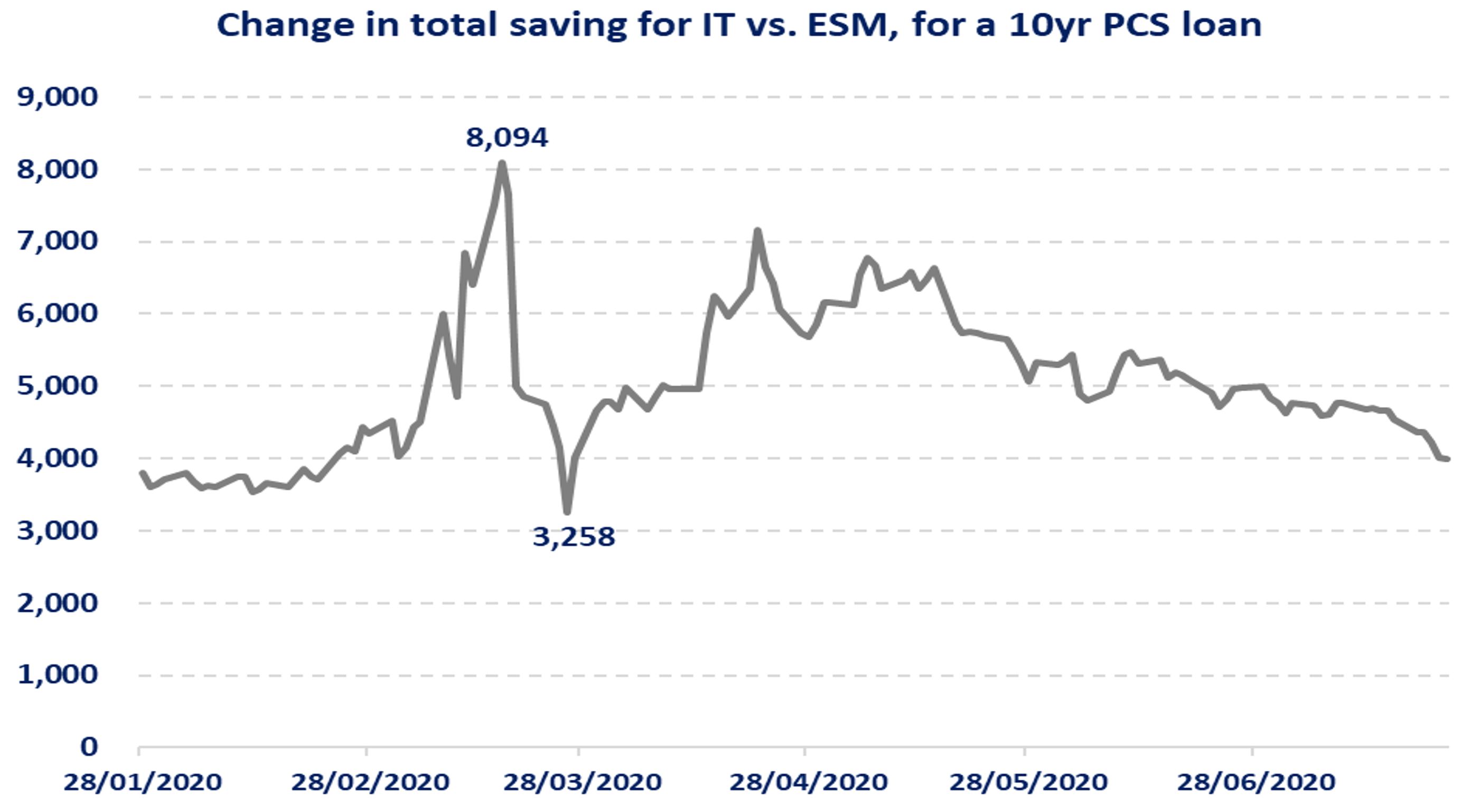

We received a lot of questions from people in Italy. If you look at the cost savings for Italy’s taxpayers, the chart below demonstrates they are still present and fluctuate based on market moves.

Figure 4. Change in total saving for Italy vs. ESM, for a 10yr Pandemic Crisis Support loan (euro, millions)

Source: Bloomberg, ESM

Any other reasons why the ESM can fund cheaply?

The ESM credit rating is top notch at AAA Outlook Stable from Fitch Ratings and Aa1 Outlook Stable from Moody’s. At present, and even after spreads contracted, the ESM can fund cheaper than a large number of euro area member states.

The ESM successfully places issuance via its Diversified Funding Strategy. This provides flexibility to tap the capital markets while at the same time committing to a pre-agreed maturity structure of loans.

This flexibility ensures that at any time of issuance, the ESM is able to secure funds at their cheapest levels possible. For the recipient of the Pandemic Crisis Support this means that they could benefit from the lower rates of shorter funding without having the liquidity risk for the roll-over of maturing funding instruments.

We received very positive feedback from investors on our Social Bond Framework in line with the latest version of the ICMA Social Bond Principles. This will enable us to issue also social bonds to fund the Pandemic Crisis Support, which finally may enable us to reduce funding costs further.

The conditionality of the Pandemic Crisis Support is limited to the use of proceeds. The money has to be used to fund direct and indirect costs of healthcare related to the pandemic. This is similar to what sovereigns and other issuers commit to when they issue green or social bonds - they give a promise to the lender about how they will use the money. There is no additional conditionality.

This means there is also no reason to see a stigma in requesting the Pandemic Crisis Support. It is a responsible decision to save taxpayers’ money. We have conducted investor calls with hundreds of our bond buyers around the world and these investors have confirmed there is no market stigma to use the ESM loans. Rather, they see the benefits.

The exact amounts saved will depend on when those applicants come to draw funds, as that is when the ESM will actively seek to fund Pandemic Crisis Support in capital markets and how funding conditions will develop in the future.

In addition to the cost savings to taxpayers, it is worth noting that the funds for the loans are not taxpayers’ money. They come from investors.

Pandemic Crisis Support, made operational on 15 May, remains available to all euro area member states to apply for until end 2022. Countries must weigh up if and when to apply for the credit line.

Most importantly, Europe and the ESM are here to help in times of crisis.

Acknowledgement

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.