Outside the box: A new ESM for a new crisis

The Covid-19 pandemic is a crisis measured in the tragic human cost of fatalities as well as an expected sharp global economic recession in 2020. Investors are understandably keen to know how the ESM, as a crisis resolution body, can help Europe overcome the pandemic.

At a Global Investor Call attended by hundreds of investors across the three major financial time zones last week, we received many questions about how specifically we will raise funds if a euro area country applies for help to finance mounting healthcare-related costs.

When I wrote my last blog on 28 April, Funding health and stability, the European Stability Mechanism (ESM) had just been confirmed as part of Europe’s response to fight the crisis caused by the coronavirus outbreak.

On 15 May, our Board of Governors made our new Pandemic Crisis Support credit line operational.

The lines are open and attractive

Now any ESM Member can apply for funds to support domestic financing of direct and indirect healthcare, cure and prevention related costs due to the Covid-19 crisis.

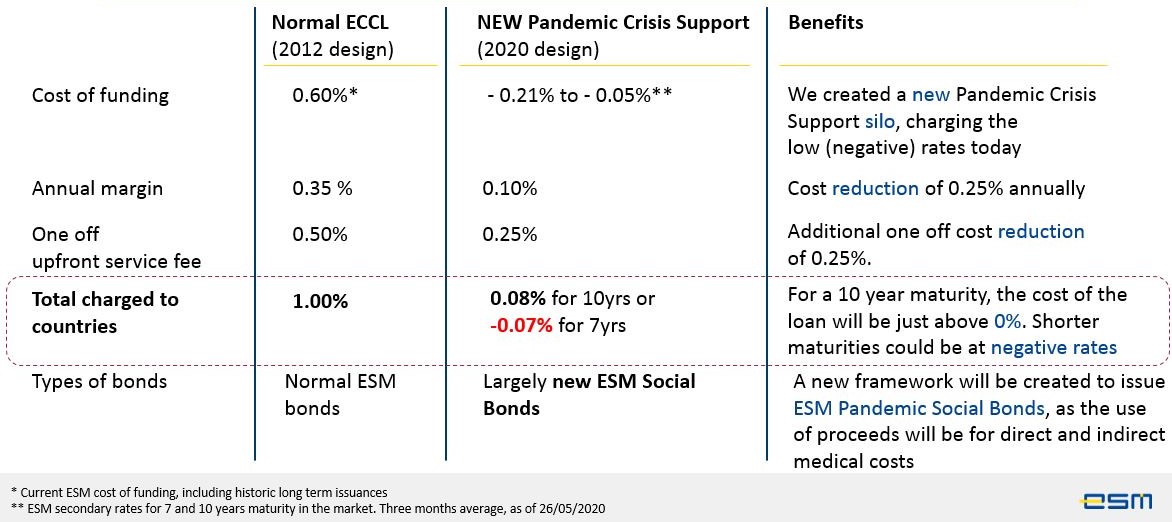

At policy level, our 19 member states agreed on this new Pandemic Crisis Support in just two months, showing how Europe comes together in times of crisis. Views differed at the start and that is a normal process in healthy democracies. But views converged rapidly and an agreement was found. At ESM level, we created – in record time - a new method to segregate internally the financing of the new credit lines from loans of the previous crisis. This is an internal Asset and Liability mechanism. For investors, nothing changes. Investors buy ESM bonds across the curve as we continue with our diversified funding strategy.

For Pandemic Crisis Support countries, it makes a big difference. They will not need to bear the costs of funding for past issuances. They will be able to benefit from ultra-low and even negative interest rates today. We will pass through our AAA/Aa1 cost of funding; for 7-year bonds we pay around-0.21% in the market and for 10-year bonds -0.05%.[1]

Then, our Members agreed to slash the Annual Margin and Upfront Service Fees. The standard Enhanced Conditions Credit Line (ECCL) created in 2012 has never been used but provided the structure for our new credit line. Had it been used, the annual margin would have been 0.35%. For Pandemic Crisis Support, this was reduced to 0.1%. The upfront - one off - service fee, which was 0.5% for ECCL, was reduced to 0.25%. The ESM will charge the bare minimum for these loans; the fees are there merely to cover our operational and administrative costs. Light conditionality and low fees of the new instrument reflect the symmetric nature of the Covid-19 crisis. The new instrument shows true solidarity.

Figure 1: The new ESM Pandemic Crisis Support has many benefits

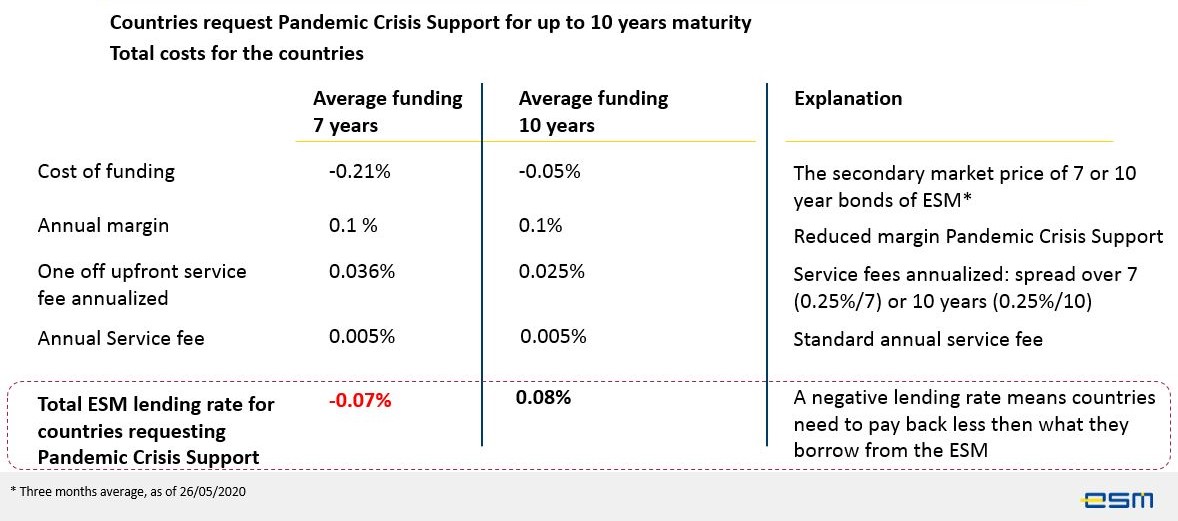

So – let’s do the numbers. If the countries request a 10-year loan and we finance the pandemic crisis support on average with 10 year funding, the full costs ESM would charge will be around zero. If the request is for a 7 years loan then the total cost of funding including fees will actually be negative and around -0.15%. With negative rates, countries will pay negative rates – in other wordsreceive money back. This is what makes the Pandemic Crisis support tool very attractive. Presently, some euro area countries pay positive interest rates when they borrow for 7 or 10 years.

Figure 2: What will countries be charged?

For how many countries is the Pandemic Crisis Support attractive?

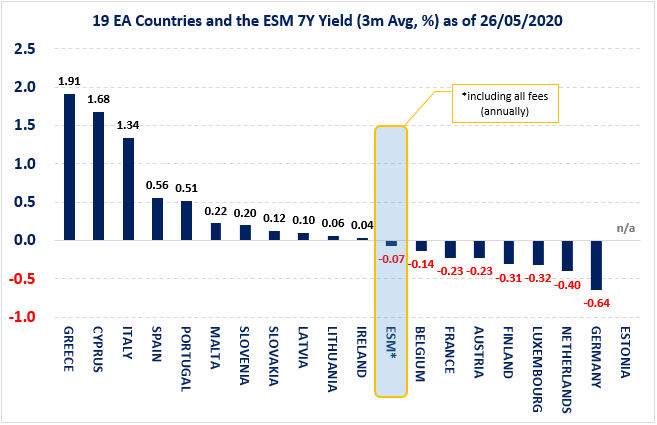

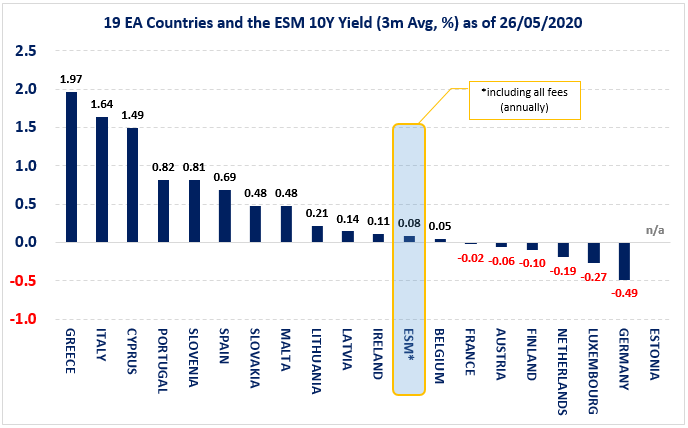

Looking at the all-in costs of the ESM, we would be attractive for 11 Member States.[2] For those countries, financing direct and indirect health care costs would be cheaper via the ESM than in the market. There are also other benefits; by applying for the pandemic credit line they create a safety buffer for financing and relieve part of the pressure on their domestic bond yields. In other words, several billion euros in some cases would not need to be financed in the market but could be financed via the ESM. This reduces the – already planned – large supply of national debt, which has a positive effect on the prices of the domestic bonds.

Figure 3: 19 euro area countries and the ESM 7Y Yield (3m Avg, %) as of 26/05/2020

Source: ESM, Bloomberg

Figure 4: 19 euro area countries and the ESM 10Y Yield (3m Avg, %) as of 26/05/2020

Source: ESM, Bloomberg

Members can apply anytime until the end of December 2022. Disbursements are made at 15% of the total amount a month ensuring a smooth funding process necessary to raise the funds. That means the total funds can be provided in around 7 months.

If loans are drawn, they will have a maximum average maturity of 10 years. But there is no pressure on Member States to draw the cash. For applicants, it could be simply the assurance that should they ever need the funds, they can be made available quickly.

What does this mean for citizens?

Let’s assume that “Country Europea” is among 11 countries who at present could obtain funds via the ESM more cheaply than if they raised them from capital markets.

“Country Europea's” 10-year bond yield is 72 basis points (0.72%) above 10-year ESM bonds - that is the average of all those euro area countries identified as presently having higher funding costs than the ESM. All things being equal, over 10 years of the loan, “Country Europea” could save €720 million for every €10 billion borrowed via the ESM.

In real life, under current market conditions, for some countries the cost savings could be up to €6 billion for 10 years. This is a real cash saving for taxpayers. They will simply need to pay less taxes to cover interest payments to global capital markets. This is European solidarity for citizens.

Ultimately, the decision to apply and then to draw is solely for our Member States to make. We stand ready to help in times of crisis.

The ESM and social bonds

In the Covid-19 crisis, the ESM has shown its ability to adapt to the crisis within its mandate and serve its 19 member states. Given that this is primarily a health crisis with severe socio-economic consequences, the dynamics are different than in the past. As such, we had to adapt and tailor our approach to effectively meet this new and unprecedented challenge. We have lowered our margins, reduced our fees and found ways to even lower further our cost of funding.

We will do even more. The ESM Pandemic Crisis Support is set up to finance direct and indirect healthcare, cure and prevention related costs due to the Covid-19 crisis. We are now also working towards designing the ESM bonds needed to raise funds for our support as Social Bonds, compliant with the Social Bond Principles established by International Capital Market Association (ICMA).

We are working on a Social Bond Framework to describe the compliance of the issuances with these Social Bond Principles. To reinforce our solid governance and transparency, we will have this verified by an independent second party opinion. With this approach, the ESM strives to make use of Social Bonds as an innovative debt instrument, in order to allow investors focusing on environmental, social and governance (ESG) issues to allocate their funds to the ESM Members hit by the pandemic crisis. Yet, our Social Bonds do not only seek to widen the ESM investor base but also underline the social dimension of our support.

Since last year, the ESM has also been member of the ICMA Green Bond Principles and Social Bond Principles Advisory Council. We aim to actively contribute and bring such best practices to the market.

The Pandemic 2020 corona crisis has changed the way we work, the way we interact and the way we live. These changes have reinforced the social nature of the ESM, soon visible in the social bond framework.

Further reading

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author