How banking union and capital markets union can help Europe finance the climate change challenge

Climate change and actions taken to mitigate its negative effects should be of great concern for European citizens, economies, and, ultimately, for financial stability. Experts agree that billions of euros are needed every year to reduce emissions and curb climate change risks. With the ESM mission to safeguard financial stability, we find it important to explore the financing of the green transition and what can be done to close any financing gap.

Commitments, legislation, and policies are just the beginning

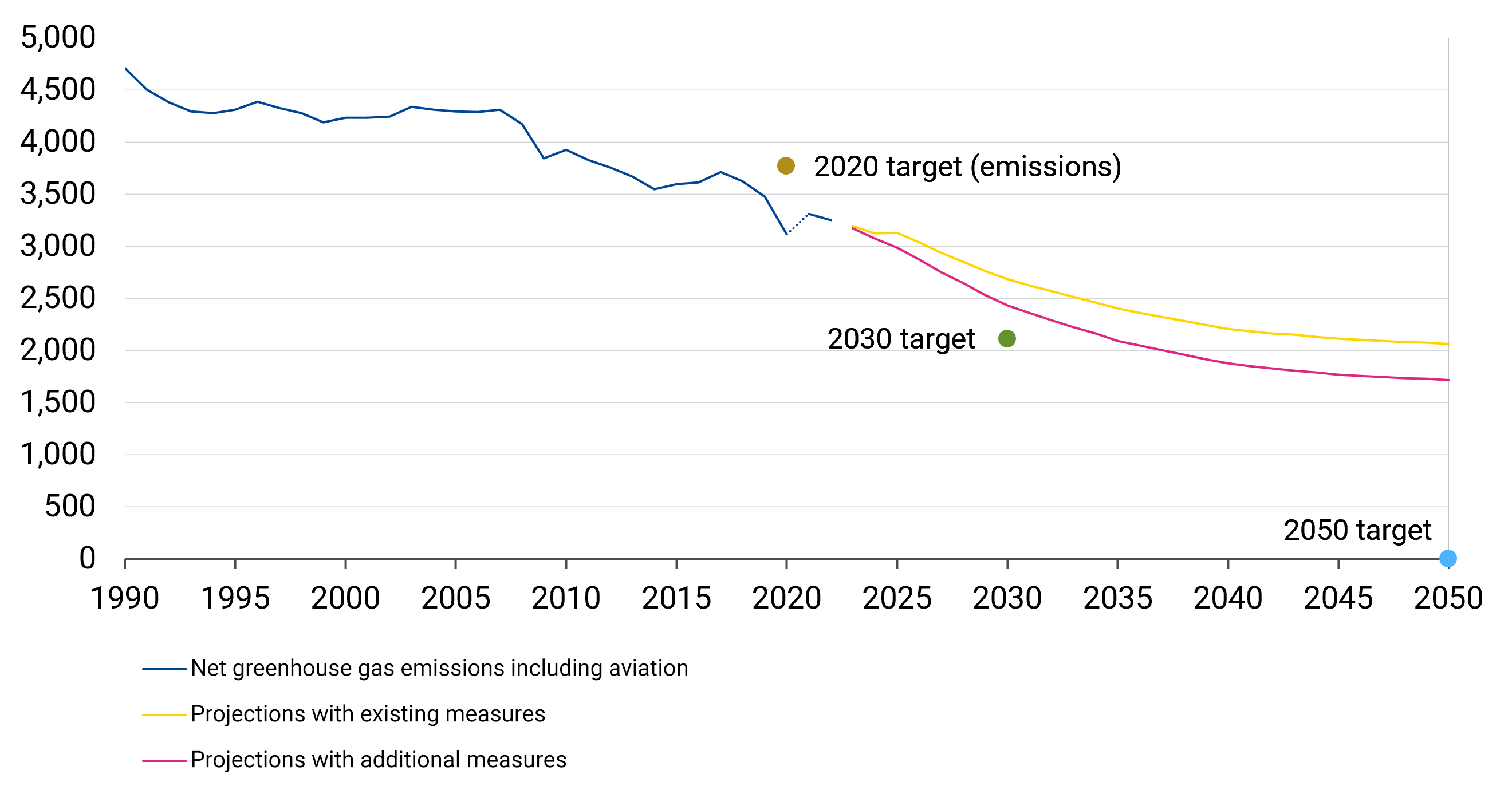

In response to climate change risks, the European Union (EU) Member States plan for climate neutrality by 2050, in line with a commitment to global climate action under the Paris Agreement. [1] To reach that goal, the EU turned the carbon neutrality plan into binding European law through legislation and policies. These actions, although only a first step, imply realistic and appropriate limits on carbon emissions in the EU (see Figure 1).

Figure 1: A decreasing trend for total EU net greenhouse gas emissions from 1990 onwards

(in million metric tonnes of CO2 equivalent)

Source: European Environment Agency

How much cash is needed to finance the green transition?

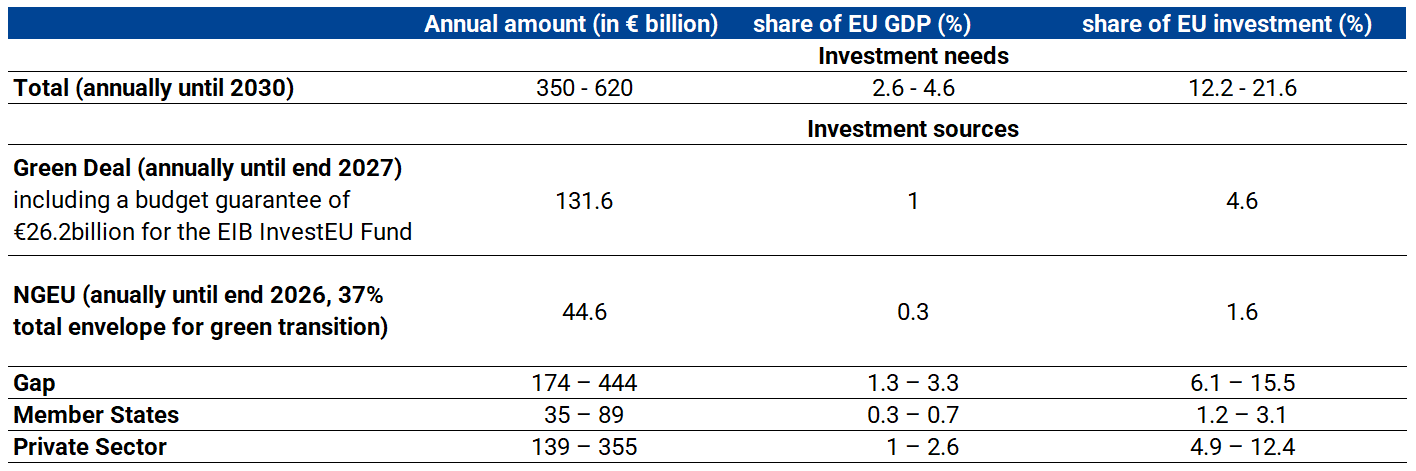

Achieving net zero carbon emissions requires large investments towards an ecologically sustainable economy. The European Commission estimates that Europe needs between €350 billion and €620 billion in additional investments per year until 2030 to achieve its goals (Figure 2). [2] This represents between 2.6% and 4.6% of annual EU gross domestic product (GDP), or between 12.2% and 21.6% as a share of investment in the EU. So, it’s time to step up our game.

With that in mind, the EU launched the European Green Deal initiative and Next Generation EU package to jump-start funding from the private sector. To incentivise additional private sector investment into greening the economy, the EU increased transparency, comparability, and standardisation of green financing, which also contributed to mitigating greenwashing at the European level. [3] Public funds were also provided by the European Investment Bank. Accounting for the EU’s financial contribution, the remaining investment gap is between €174 billion and €444 billion annually.

With limited fiscal space in some countries, the public sector cannot finance the remaining additional investment needed without the participation of the private sector. It has been estimated that the public-private split would be as follows: for each €1 that public entities commit, the private sector crowds in €4. [4] The EU Member States would account for 20% or €35 billion to €89 billion of additional investment, while the private sector would supply the remaining 80% or €139 billion to €355 billion.

Figure 2: Additional annual investment needs to meet climate targets by 2030

Note: We use Darvas and Wolf’s (2021) assumption of a public private ratio of 1:4 (80% private sector, 20% public sector).

Sources: European Commission, Impact assessment accompanying the document Stepping up Europe’s 2030 climate ambition; Investing in a climate-neutral future for the benefit of our people, 2020; Strategy for Financing the Transition to a Sustainable Economy, 2021; Strategic foresight report, 2023; The European Green Deal; The European Green Deal Investment Plan; For investEU, 30% of total envelope allocated to climate objectives; ESM calculations

Financing the gap: green gains from banking union and capital markets union

Given the large role for the private sector, enhancing financial integration in the EU would be beneficial, particularly in view of the cross-border character of climate change risks and financing needs. Completion of banking union and progress with capital markets union offer a greater choice of financing, enhance competitiveness, and improve cost efficiency which, in turn, could encourage more cross-border bank lending and financing.

Cost efficiency gains for debt and investment financing from banking union and capital markets union could bridge the lower bound of the private sector financing gap (€139 billion). For debt financing, such cost efficiencies could positively impact new loans and net corporate bonds issuance. For investment financing, similar cost efficiency gains could be beneficial for securitisation, private equity, investment funds, and deposits.

The benefits of enhanced financial integration are particularly important for small- and medium-sized enterprises, which represent 99% of all companies in the EU, or households looking to increase their green capital expenditure in a more cost-efficient way.

With an annual volume of new loans to corporates and households of around €3.5 trillion in the euro area, [5] an increase in cost efficiency through banking union could prompt savings. Similar cost efficiency gains in capital markets union for new corporate bond issuance of just under €580 billion annually [6] could also have a positive impact. These gains could help close the financing gap.

One path ahead could be to revive asset securitisation and continue the significant progress euro area banks made in freeing up lending capacity through risk transfers. A stronger capital markets union would also simplify the framework for cross-border capital investment, which could help redeploy capital and support the private sector in their transition towards a sustainable economy.

European private equity market activity represented €133 billion in 2023. [7] This market could benefit from efficiency gains in capital markets union through an integrated and stable legislative framework, an increase in size, and the fostering of more green innovation.

Given a €369 billion annual average for European investment funds’ activity [8] and trends over the last 10 years, cost efficiency gains from capital markets union could add additional capital for green investment. A more integrated capital market marginally increasing such funds would imply new capital allocated for sustainability-related purposes.

Within the euro area alone, there were approximately €12.7 trillion in savings deposits by the end of 2022. Providing incentives could generate investment inflows from depositors into a green capital market that could be attracted to a safe and sustainable investment option. Sustainability could possibly serve as a catalyst for a green capital markets union, which would bring a broader range of investors to projects looking for financing.

These financing instruments together cover the most obvious asset classes and could generate enough additional funds to allow Europe to finance the lower bound of the private sector investment gap (€139 billion).

Climate change and financing the green transition – a robust option

Climate neutrality in Europe is a clear goal, though a heavy task. Europe is committed to its ecological and financial sustainability goals and has taken steps to enable the green transition. Yet, a sizable investment gap remains. The EU Member States can provide some additional investment but would still rely on the private sector to supply the bulk of the remaining share. Completing banking union and progressing capital markets union could generate sufficient funds to fill the lower bound of the private sector investment gap.

Not only would such enhancements benefit financial stability, a topic close to the heart of the ESM, they could also free up additional necessary funds for the green transition in Europe.

Acknowledgements

The authors would like to thank Elisabetta Vangelista, Marco Onofri, Ioannis Vazouras and Olivier Pujal for their contributions to this blog post; Kalin Anev Janse, Rolf Strauch and Nicoletta Mascher for their valuable comments; and George Matlock, Peter Lindmark and Raquel Calero for their editorial review.

Further reading

Momentum builds for Europe’s capital markets union

Europe greening the world: the “Brussels effect” on sustainable finance

Assessing climate risks at the ESM

Five themes to watch for multilateral financial institutions

How capital market finance can boost European business

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors