Europe greening the world: the “Brussels effect” on sustainable finance

Europe delivered two groundbreaking initiatives last week to counter the global climate change crisis: a European Union climate deal, committing the EU to more than halve greenhouse gas emissions by 2030 and reach zero net emissions by 2050; and the publication of a first-of-its-kind of regulation, the EU’s sustainable finance taxonomy, with the potential to become the gold standard for global investors in green finance.

Governments, enterprises, and investors are increasingly conscious of the sustainability risks our economies and societies face. While the Covid-19 pandemic poses a grave short-term risk, climate change presents the most severe long-term challenge.

One of this blog’s authors, Anu Bradford, coined the term “the Brussels effect”[1] in 2012 to explain how regulations drafted in Europe shape the global marketplace. In this blog, we explain why Europe’s actions to encourage Environmental, Social and Governance (ESG) investment practices could lead to a new global standard for sustainable finance, transforming global capital markets in the process.

Sustainability risks pave way for ESG growth

The World Economic Forum’s recent annual risk reports identified climate change and infectious diseases as top threats facing humanity.[2] Both risks present policy-makers and companies worldwide with enormous challenges, but also with opportunities to reset priorities.

The EU is transforming these risks into opportunities by embracing a sustainable recovery agenda. This includes deploying innovative funding instruments to help industries evolve towards sustainable practices and re-orienting investment towards resiliency projects.

There has been a steep rise in public, corporate, and investor awareness of ESG-related risks in the last half decade[3], which is also reshaping the capital markets landscape. ESG investments are one of the fastest-growing asset classes worldwide; they expanded exponentially during the pandemic and are expected to continue to do so during the forecast recovery phase.

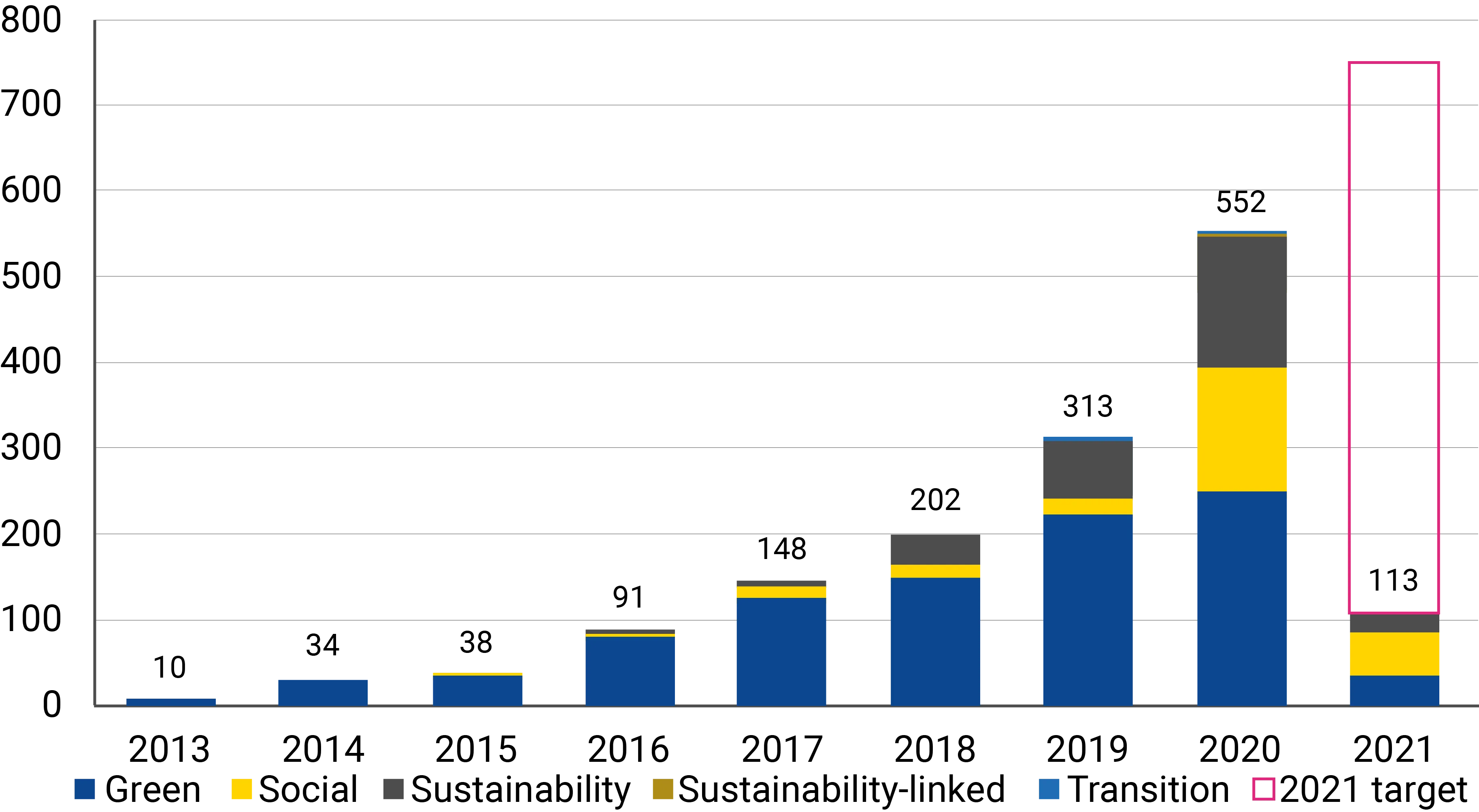

Figure 1: Global sustainable bond issuance volumes

Figure 2: Global sustainable bond issuance volumes (Breakdown)

FIG - Financial institutions groups

Corp - Corporates

SSA - Sovereign, Supra & Agency

APAC - Asia Pacific

EMEA - Europe, Middle East and Africa

LATAM - Latin America

NAM - North America

Note: As of 2 April 2021.

Sources: Dealogic, Citigroup

Europe championing sustainable investing

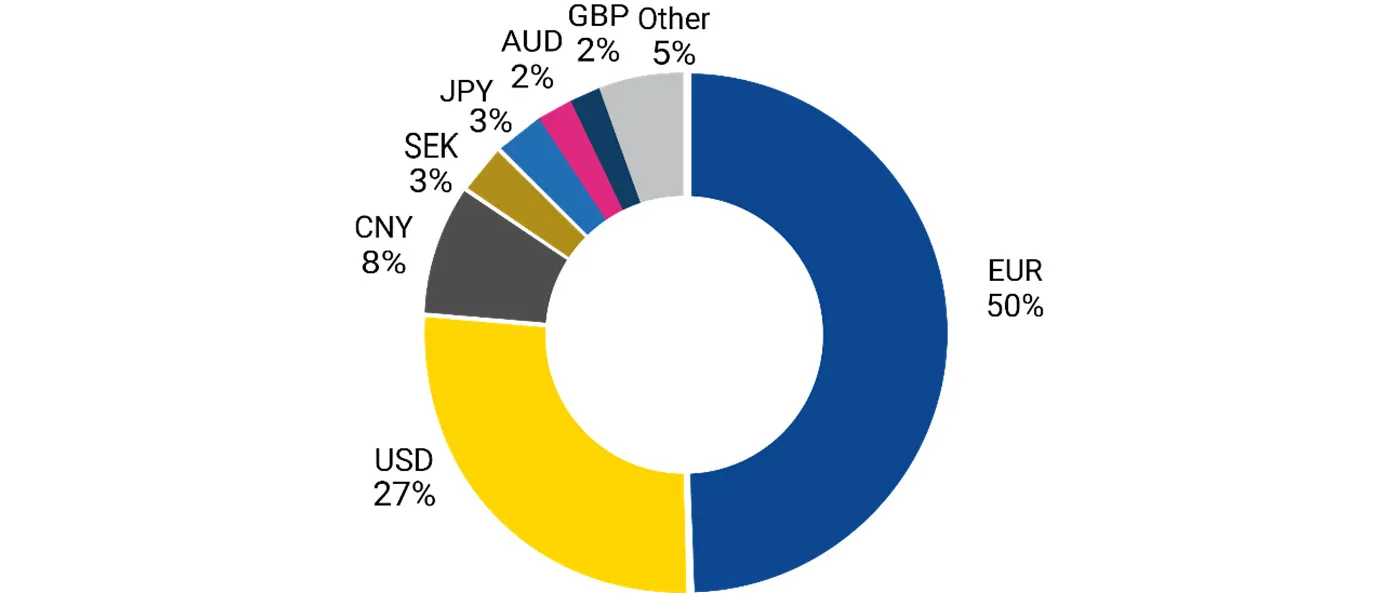

Europe is leading the world in ESG issuance and has become the global hub for ESG bonds. The euro stands as the global currency of choice for sustainable finance, with 50% of global sustainable capital markets denominated in euro compared to the US dollar’s 27%. The European Investment Bank (EIB) issued the first-ever green bond — the “Climate Awareness bond” in 2007. Since then, the social, green, and sustainability bond market has boomed, with worldwide issuance growing more than six-fold between 2015 and 2019 and 2020 recording the highest quarterly issuance record. For the first time in history, ESG bond issuance exceeded USD 1 trillion.

Figure 3: ESG by currency

Note: As of April 2021.

Sources: Dealogic, Citigroup

The Covid-19 pandemic is reinforcing the EU’s leadership in ESG investing. Wide-ranging rescue packages designed to fight the pandemic and lift economies out of this crisis underscore European efforts to add to existing green bond programmes in individual member states.

The ESM, the European Council, the European Commission, and the EIB are all contributing to this effort. The ESM designed a €240 billion pandemic response credit line to finance euro area countries’ healthcare costs. If called upon, this instrument would be financed by social bonds, representing a major ESG milestone for the ESM. In addition, the European Commission announced that 30% of the €750 billion EU recovery fund will finance itself with green bonds that are expected to be issued from mid-2021. Furthermore, 100% of the funding for the Commission’s €100 billion Support to Mitigate Unemployment Risks in an Emergency (SURE) programme will come in the form of social bonds. Finally, the EIB’s €200 billion loan guarantees help support businesses in the EU.

Yet more work on taxonomy is needed to harness the full potential of ESG capital. Standardised methodologies and terminology are needed to resolve market dissonance and minimise false or misleading claims about sustainable investing — a practice known as “greenwashing”.

Sustainable finance as the next frontier of the Brussels effect

The EU has acknowledged the need for common standards, and is actively seeking to bolster sustainable finance market through regulation.

The Commission has worked on key elements for the evolution and growth of sustainable capital markets that pave the way for clear and ambitious rules for ESG investing. Namely, the EU taxonomy of environmentally sustainable economic activities, an EU Green Bond Standard, and climate-related disclosure practices.

The EU taxonomy will apply to financial products offered in the EU as “environmentally sustainable”, ensuring financial market participants who wish to market bonds as environmentally sustainable in the European market — the largest ESG marketplace — comply with the taxonomy.

This new standard on sustainable investing is expected to influence investment practices also outside the EU — a phenomenon known as the “Brussels effect.” Most multinational corporations follow EU regulations, considering it the price for accessing its large and wealthy consumer markets. Yet, these companies often extend EU rules to their global operations to avoid the cost of complying with multiple regulatory regimes. This explains why so many large non-EU companies follow the EU’s General Data Protection Regulation or many EU environmental regulations across their global operations.

Global financial firms are expected to follow the EU’s taxonomy as a condition for entering the largest ESG market in the world. To qualify as an EU-approved ESG investment, each listed company in these firms’ equity or fixed income portfolios would have a percentage of investment aligned with the EU Taxonomy, and the final portfolio alignment would be the result of the weighted average of each position.

This trend of global firms constructing their ESG portfolios to align with EU taxonomy is likely to accelerate if investors shift policies to favour investments that meet Europe’s ESG standards. Rating agencies have introduced brand new ESG ratings. Failure to comply with such ESG standards will make capital-raising more expensive, because companies deemed to be non-compliant will end up in the “brown-” rather than the “green-list”. They will then need to pay a premium to access the market.

EU leadership is particularly important given the lack of adequate multilateral progress on fighting climate change and towards a carbon-neutral economy. For example, the Paris Agreement explicitly calls for making finance flows consistent with climate-resilient development. Little has been accomplished to meet that goal to date.

Yet last week was busy for climate change action on both sides of the Atlantic. A day after the two European initiatives, US President Joe Biden pledged to cut gas emission by 2030 too[5], and we welcome that development, but there is more needed.

The US Treasury has issued no green bonds, and the US dollar lags the euro as currency of choice to issue, or invest, in ESG finance. Under former President Donald Trump, the US sought to actively limit ESG investing. Now under Biden the US will still only be playing catch-up. Thus, in the global efforts to rebuild a sustainable, post-pandemic economy, the EU is leading the way.

Solving the pandemic and climate change crises needs a global effort, but Europe can serve as catalyst for such a global transformation.

Anu Bradford is Henry L. Moses Professor of Law and International Organization at Columbia Law School.

This blog post was published as an op-ed in Project Syndicate (link is external).

Acknowledgements

The authors would like to thank Herbert Barth, Carlos Martins, Niyat Habtemariam, Fernando Rodriguez, George Matlock from ESM, and Sanaa Mehra of Citigroup.

Footnotes

Anu Bradford (2020) The Brussels Effect: How the European Union Rules the World, Oxford University Press

World Economic Forum (2020) The Global Risks Report 2020; World Economic Forum (2021) The Global Risks Report 2021

Risk Management Magazine (2019) Banham, R. Getting Serious about ESG Risks

Citigroup (2021) Financing A Greener Planet – VOL II: Bridging the Gap between Green Investment & Investors February 2021

US White House (2021) FACT SHEET: President Biden Sets 2030 Greenhouse Gas Pollution Reduction Target 22 April 2021

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.