Building resilience in times of inflation-induced inequality

Energy prices in the euro area have receded from their peaks of last year, yet prices of other goods and services continue to rise. Headline inflation is declining, but core inflation remains stubbornly high. Fiscal policy has an important role to play in aligning with monetary policy to bring inflation back down to target.

The recent inflation episode has hurt low-income households the most, since they typically spend a larger share of their income on energy. Support measures put in place in many countries have mitigated this effect but have not ironed it out. Furthermore, poorer households’ incomes have increased by less than those of richer households in many countries over the past three years.

This inequality creates vulnerabilities that can aggravate recessions, reinforcing the need to build resiliency through larger fiscal buffers. Fiscal consolidation – as agreed by euro area governments and recommended by European institutions – helps create resilience for the future and avoid procyclical tightening. Near-term consolidation efforts need to be mindful of the increased inequality and avoid overburdening already struggling households.

Low-income households experienced higher inflation rates

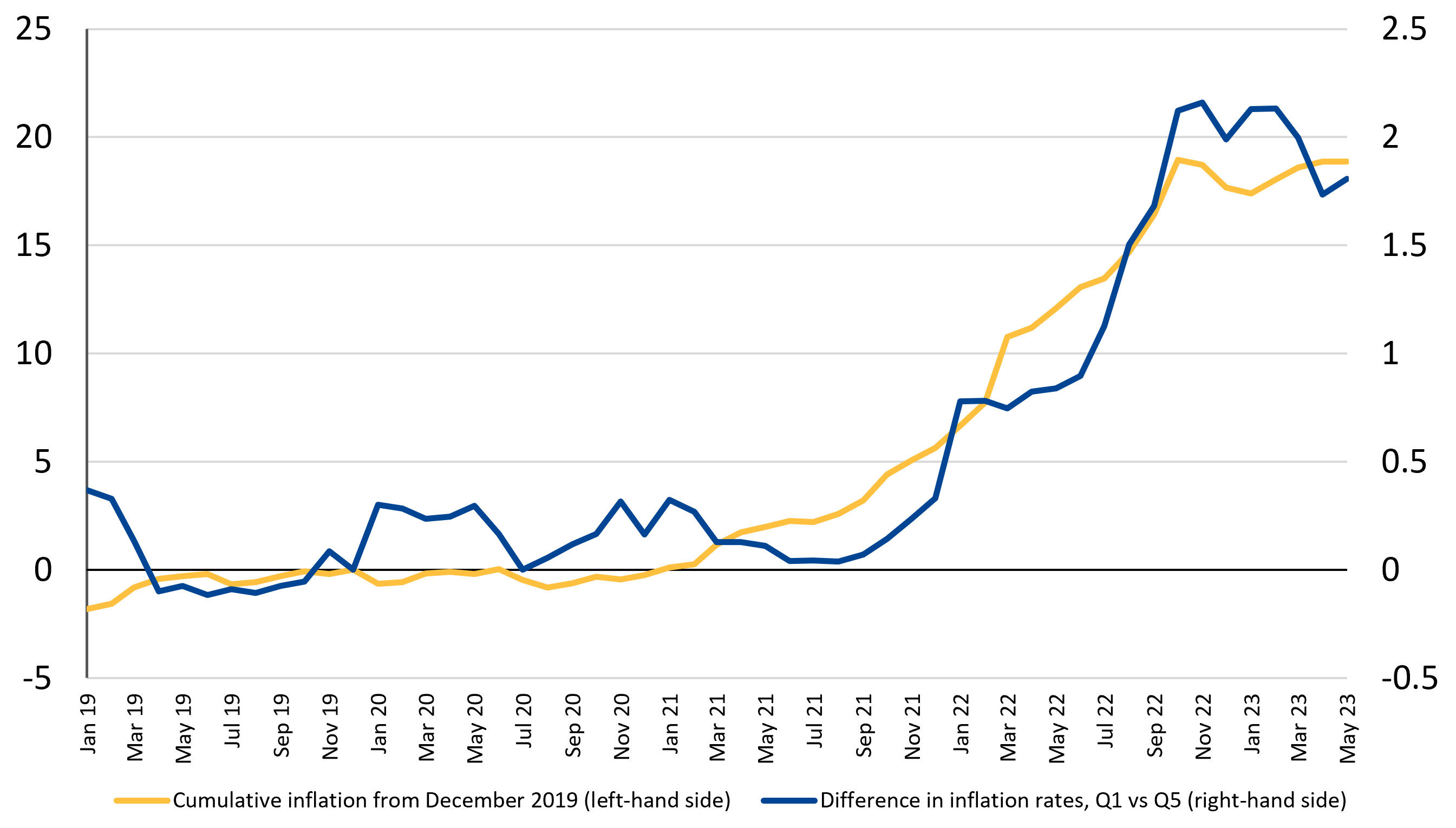

Recently, inflation rates soared to unprecedented highs in the euro area – hitting low-income households the hardest. Within three years, consumer prices rose by almost 20% (see Figure 1), with prices of necessities like utilities (including energy) and food rising the most.[1] As these goods account for a larger share of the typical expenses of low-income households, those households experienced even higher inflation rates. The difference of inflation rates experienced by the bottom and the top income quintile rose steadily alongside the headline inflation rate (see Figure 1) beginning at the end of 2021 before stabilising around two percentage points at the end of 2022 as inflation became more broad-based and less driven by energy prices.

Figure 1: The cost-of-living crisis hurt low-income households the most

(Price change in % relative to December 2019 and differential in percentage points)

Note: Q1=1st quintile, Q5=5th quintile of the income distribution.

Source: ESM based on Eurostat data.

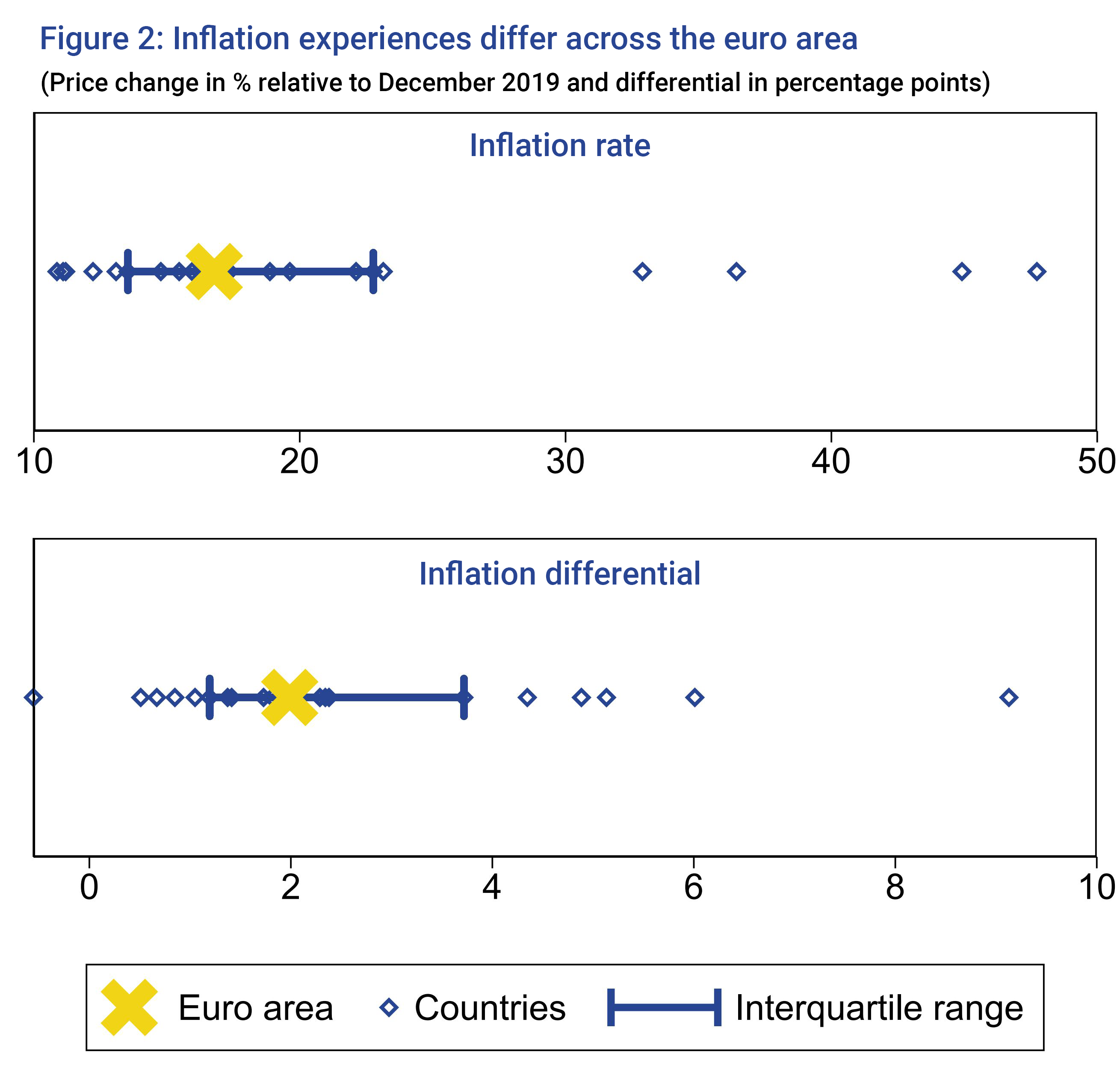

While all euro area countries were hit by the cost-of-living crisis, the magnitude differs, ranging from 11% to 48% (cumulatively from end-2019 to end-2022, see Figure 2, upper panel). Similarly, while the inflation differential of low-income and high-income households stood at 2% for the euro area, (see Figure 2, lower panel), it ranged from about zero to nine percentage points across countries.

Figure 2: Inflation experiences differ across the euro area

(Price change in % relative to December 2019 and differential in percentage points)

Note: Inflation differential is the difference in inflation rates of the 1st and the 5th quintiles of the income distribution.

Source: ESM based on Eurostat data.

Lower income growth amplified losses for the low-income households in many countries

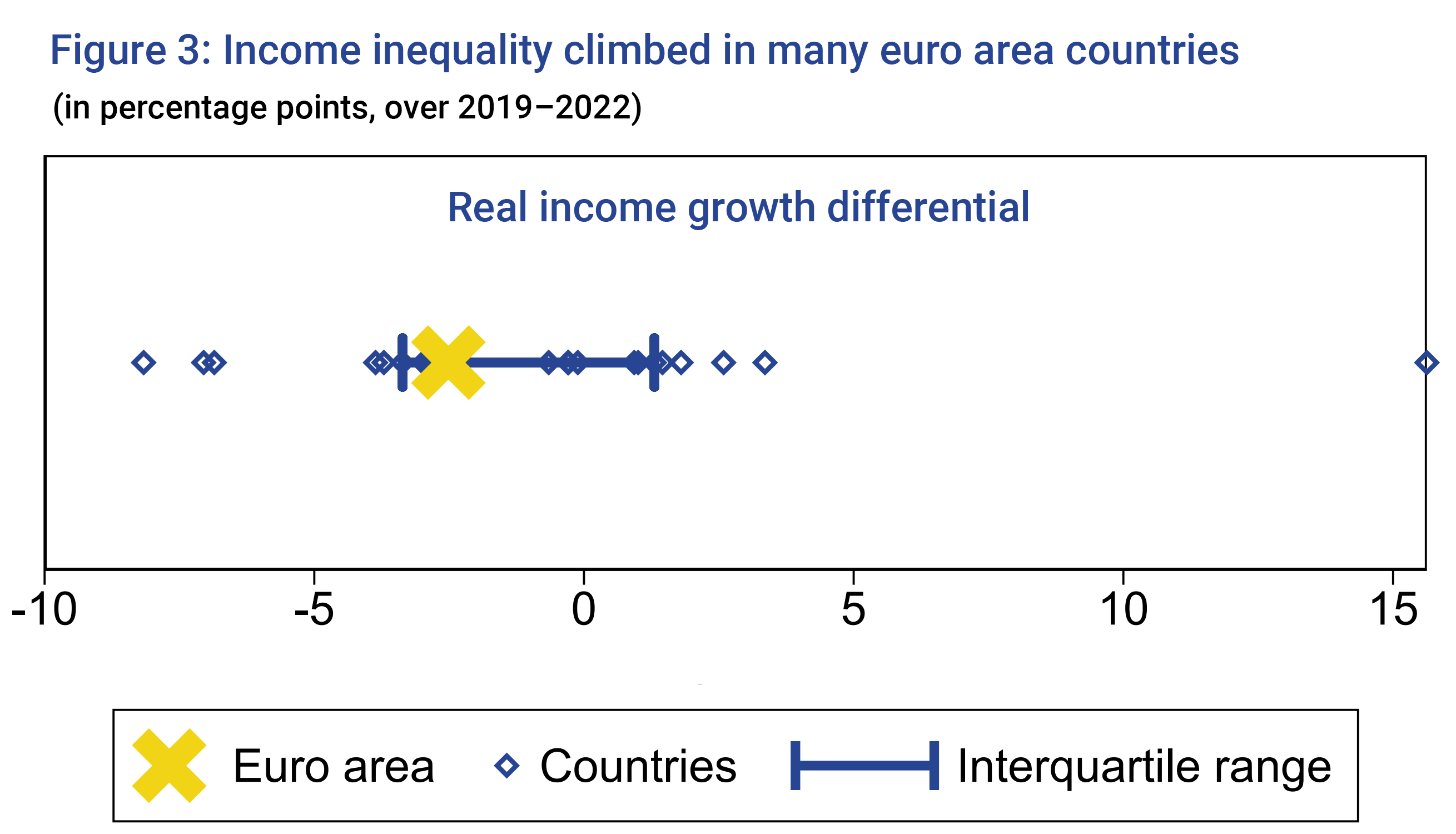

During the cost-of-living crisis price hikes outpaced incomes, triggering a roughly 6% loss of purchasing power for households in the euro area between 2019 and 2022. Low-income households suffered the largest losses because their incomes grew less while also facing higher inflation rates. Real income of poorer households fell by 2.5 percentage points more than that of richer households, amplifying inequalities in the euro area (see Figure 3).

Figure 3: Income inequality climbed in many euro area countries

(in percentage points, over 2019–2022)

Notes: The real income growth differential is the difference between real income growth of the 1st and the 5th quintiles of the income distribution. Real income growth is the change in the median income divided by the change in the price level.

Source: ESM based on Eurostat data.

Developments across euro-area countries differed, reflecting country-specific support mechanisms (see Figure 3). Low-income households experienced larger losses in most euro area countries, but their real incomes declined less than those of richer households in a few countries. This diversity reflects wide differences in economic structures, minimum wage increases (including inflation indexation), and different targeting and persistence of government support schemes.

Increased inequality and poverty risk increase euro area vulnerabilities

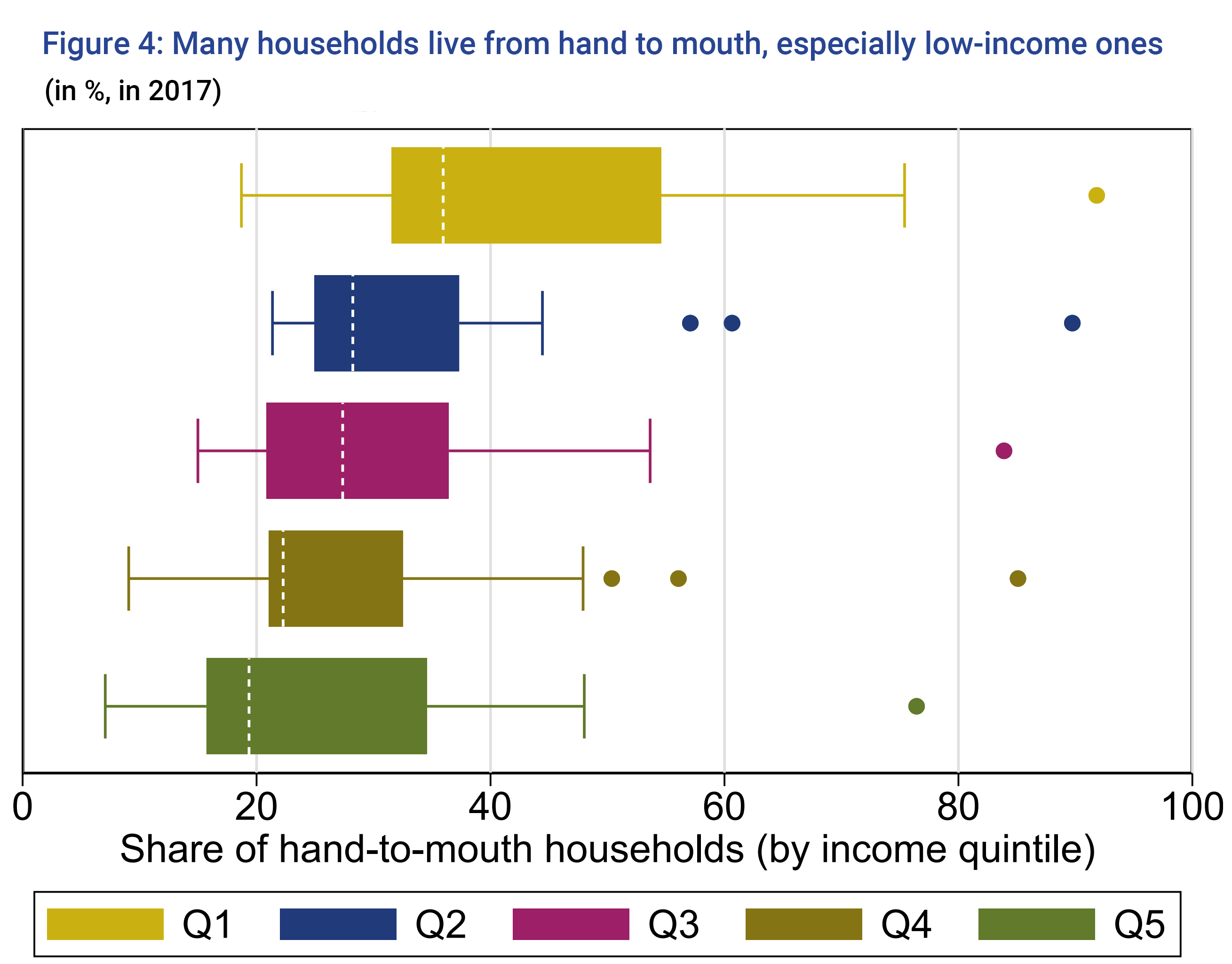

Euro area countries need to account for the capacity of households to withstand shocks. Many households live from paycheque to paycheque, either because they do not have savings and cannot borrow, or because their savings are invested in illiquid assets (such as housing) that they cannot draw on. The share of such households in most countries is understandably substantially higher in the lowest income bracket (see Figure 4). [2] These households will find it difficult to cope with the present shock as well as any further declines in income.

Figure 4: Many households live from hand to mouth, especially low-income ones

(in %, in 2017)

Note: Hand-to-mouth households are households who hold little or no liquid wealth (cash, checking, and savings accounts), irrespective of whether they own sizeable amounts of illiquid assets like housing (Kaplan et al., 2014).

Source: ESM calculation based on Eurostat’s Household Finance and Consumption Survey microdata.

The economy is more vulnerable if income inequality remains high. Unemployment and wage moderation, as typically observed during recessions, would hit low-income households hardest, pushing them to reduce consumption given their limited savings and borrowing capacity. Even households not immediately affected by a recession would cut back consumption to build savings for a rainy day. Taken together, a recession would be more severe because more households, particularly those living from paycheque to paycheque, cut back on consumption.

Implications of increased inequality on fiscal policies

The Eurogroup and European institutions agree that “a strategy of determined, gradual and realistic fiscal consolidation is warranted, to strengthen fiscal sustainability, to rebuild fiscal buffers, [and] to deliver higher sustainable growth”.[3] It is recommended to wind down energy support measures as soon as possible, so long as there are no further energy price shocks.

This strategy supports euro area resilience against future economic downturns and should create the space to invest in climate change and digitalisation measures that support future growth. Emerging from this crisis with higher inequality and an increased number of low-income households reinforces the need to build up resilience.

Those living paycheque to paycheque are unable to smoothen income over time, meaning a recession could become even more pronounced. Procyclical tightening of fiscal policy, as it has regularly happened in the past, would thus be more detrimental. In turn, supporting those in financial need in recessions would have an even bigger economic impact. At this stage, it is important to also remain mindful of the near-term effects of fiscal consolidation plans on low-income households.

Recent energy support measures were only partly targeted at low-income households. Withdrawing these costly measures that were ineffective to prevent rising inequality will help align monetary and fiscal policies and support a “smooth landing” of the European economy. Labour markets are very strong by historical standards, which tends to help low-income households. In addition, energy price inflation has turned negative, while wage developments are expected to recover some of the related real income losses. For those outside the labour market, support through social security systems will be more effective as the energy price shock dissipates. For governments to be able to support households during hard times, it is essential to consolidate budgets and build fiscal space while the opportunity is present. The present situation implies that the suggested consolidation strategy is viable with governments remaining mindful of the poor over the coming years.

Acknowledgements

The authors would like to thank Marialena Athanasopoulou, Robert Blotevogel, Giovanni Callegari, and Rolf Strauch for their valuable comments and contributions, and Raquel Calero for her editorial review.

Further reading

Adam, Klaus, and Junyi Zhu. "Price-level changes and the redistribution of nominal wealth across the Euro Area." Journal of the European Economic Association 14, no. 4 (2016): 871-906.

Araki, S., Cazes, S., Garnero, A. and Salvatori, A., 2023. Under pressure: Labour market and wage developments in OECD countries.

Aiyagari, S.R., 1994. Uninsured idiosyncratic risk and aggregate saving. The Quarterly Journal of Economics, 109(3), pp.659-684.

Bilbiie, Florin, Giorgio E. Primiceri, and Andrea Tambalotti. Inequality and Business Cycles. No. 2275. Faculty of Economics, University of Cambridge, 2022.

Alina Bobasu, Virginia di Nino and Chiara Osbat, March 2023, "The impact of the recent inflation surge across households", ECB blog post, see here

Cardoso, M., Ferreira, C., Leiva, J. M., Nuño, G., Ortiz, Á., Rodrigo, T., & Vazquez, S. (2022). The heterogeneous impact of inflation on households’ balance sheets. Red Nacional de Investigadores en Economıa Working Paper, 176

Cristina Checherita-Westphal and Ettore Dorrucci, February 2023, "Update on euro area fiscal policy responses to the energy crisis and high inflation", ECB blog post, see here

Claeys, Grégory, and Conor McCaffrey, Lennard Welslau, 28 November 2022, “Does inflation hit the poor hardest everywhere?”, Bruegel blog post see here

Del Canto, F. N., Grigsby, J. R., Qian, E., & Walsh, C. (2023). Are Inflationary Shocks Regressive? A Feasible Set Approach (No. w31124). National Bureau of Economic Research.

International Monetary Fund, European Regional Economic Outlook, April 2023, see here

Jaravel, Xavier. "Inflation inequality: Measurement, causes, and policy implications." Annual Review of Economics 13 (2021): 599-629.

Kaplan, Greg, Giovanni L. Violante, and Justin Weidner. The wealthy hand-to-mouth. No. w20073. National Bureau of Economic Research, 2014.

Kaplan, Greg, and Giovanni L. Violante. "A model of the consumption response to fiscal stimulus payments." Econometrica 82, no. 4 (2014): 1199-1239.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager