Why Europe needs strong market making

Financial markets have a few things in common with grocery shopping: buyers want readily available products sold at the lowest possible price, and sellers want to find buyers. While in supermarkets it is the retailers that ensure the liquidity and price efficiency of goods, in finance it is banks and financial intermediaries, the market makers, that do so.

Since the 2008 global financial crisis, market makers, have undergone major regulatory changes that improved the measurement and control of risks. But these changes have also put pressure on banks to rethink their business model, particularly in capital-intensive activities such as market making, and some banks have become less engaged.

The development of trading algorithms and the rise of digital technologies have created new opportunities for market makers, but they have also forced banks to invest large sums of money to upgrade their processes and recruit staff. Only banks with critical size can afford such investments. European market makers have faced tough competition from their American peers, who benefitted from a strong consolidation move in the banking industry and relied on their deep domestic capital market.

In its latest action plan[1] on capital markets union (CMU), the European Commission identified the need to strengthen the role of European market makers, in particular banks. What is more, in times of crisis US banks might retrench to domestic activities,[2] which could put Europe at risk of service limitations.

We discussed the role of market making in rebooting CMU in a blog in 2020, and identified five key attributes for CMU success. One was the role of central supervision in capital markets. In a subsequent blog, we elaborated on the concept of reviving securitisation. In this post we now address an extension of that topic, market making.

Why strong market making is key for capital markets

Market makers are intermediaries who engage their own account to provide immediacy of trade execution to clients and buy or sell securities, such as bonds or equities, at prices they fix. Market making is therefore integral to an efficient allocation of resources through capital markets, even during periods of heightened financial stress, because:

- Market making plays a crucial role for issuers. Issuers need liquid secondary markets as a pricing reference. Bonds with a liquid secondary market also offer lower funding costs for issuers.

- Investors look for liquid markets that offer not only price efficiency but also rapid access to rebalance portfolios at low transaction costs.

- Market making is essential in risk management as well as price discovery. Investors do not consider one market segment, like equities or bonds, in isolation. They need to adapt their investment mix across asset classes as their needs change while minimising risk.

- Well-functioning and liquid euro area sovereign bond markets are important for central bank monetary policy transmission.

Global market making dominated by US banks

Building liquid financial markets requires ensuring sufficient resources are devoted to market making. Mainly large banks with sizeable balance sheets and a strong capital base can maintain a global network of sales and trading and provide efficient market making services.

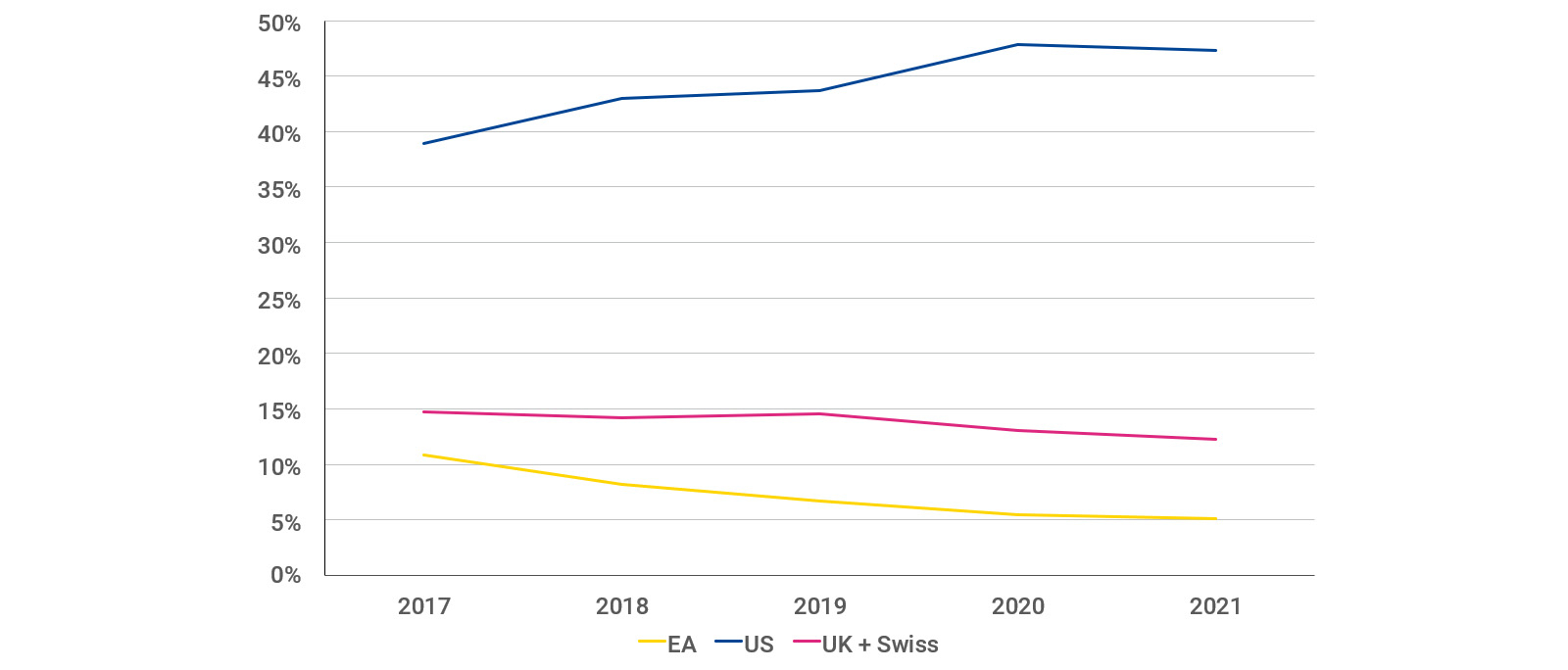

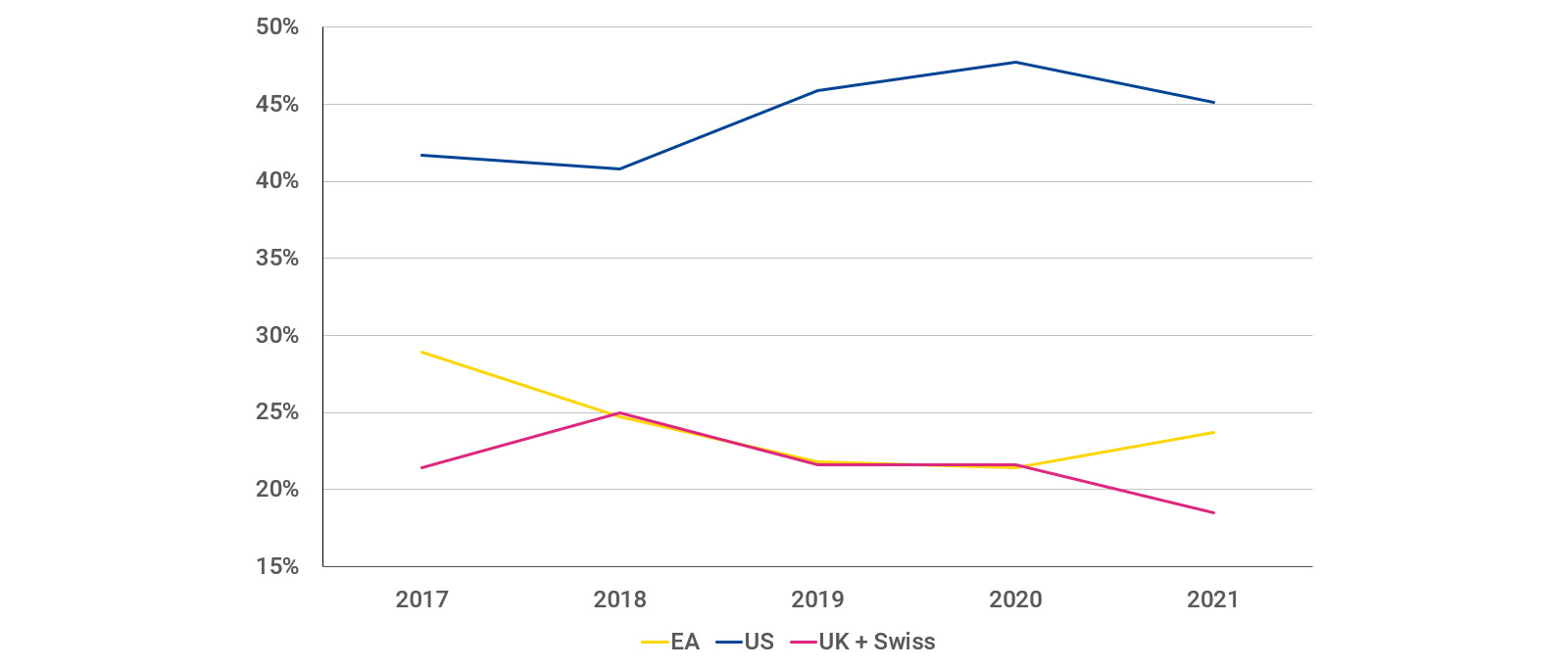

US banks’ domination of global capital markets has increased over the past five years. Over that period, we have seen US banks increase their global presence in equity capital markets to nearly 50% from just shy of 40%. The role of European banks halved to just 5%. Even in Europe’s domestic equities market, US banks command 45%, while Europe’s own banks lost market space and are below 25%.

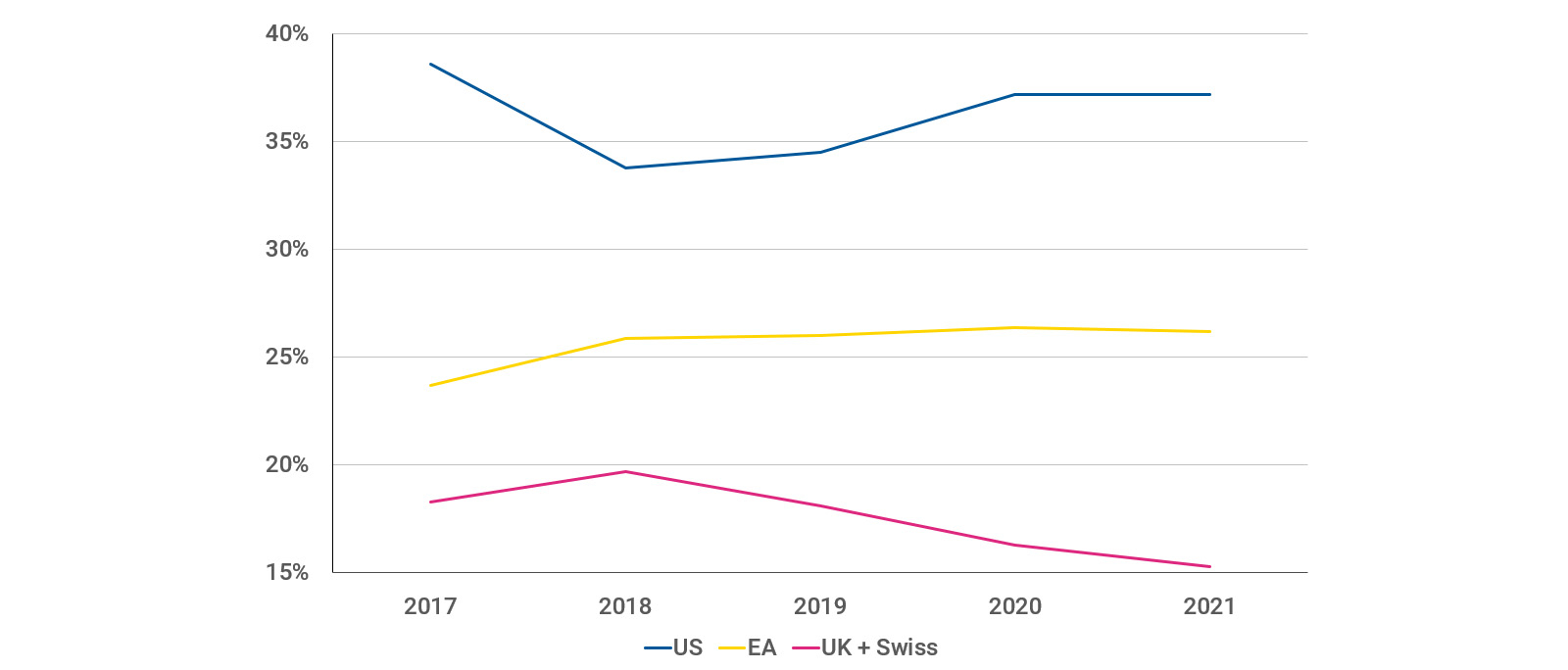

By contrast, in domestic debt capital markets European banks dominate at 43%, followed by US banks at 25%. This exception in European debt capital markets is the result of a specific market structure. We see that Europe has loyal bond investors, and this is often reflected in investor allocations.

Figure 1: Banks' market shares, split by their domiciles, in global equity capital market revenues

(in %)

Source: Refinitiv league tables

Figure 2: Banks' market shares, split by their domiciles, in European equity capital market revenues

(in %)

Notes: The market shares for equity capital markets are shown as a proxy, since there is no aggregate information solely on market making activity. Proceeds includes fees and other revenue sources. Euro area stands for the 19 countries of the euro area.

Source: Refinitiv league tables

Figure 3: Banks' market shares, split by their domiciles, in global debt capital market revenues

(in %)

Source: Refinitiv league tables

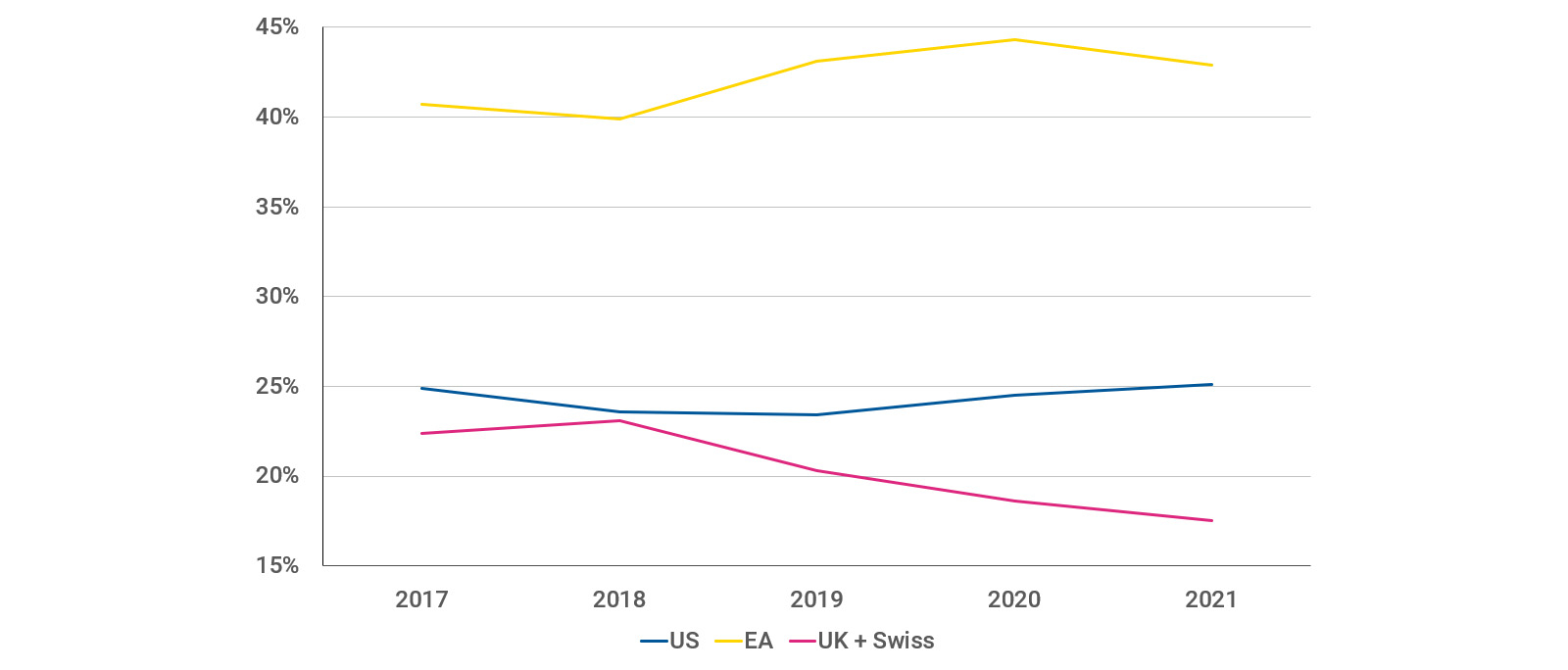

Figure 4: Banks' market shares, split by their domiciles, in European debt capital market revenues

(in %)

Notes: The market shares for debt capital markets are shown as a proxy, since there is no aggregate information solely on market making activity. Proceeds include fees and other revenue sources. Euro area stands for the 19 countries of the euro area.

Source: Refinitiv league tables

Yet in the European debt capital market we note a trend towards more concentration. In a sample of 16 European government issuers, the number of primary dealers who act as market makers is now at its lowest since 2006 and within this smaller pool the proportion of non-EU banks is at an all-time high.[3]

In times of crisis and heightened uncertainty – when the service of primary dealers ensuring smooth market flows is most urgent – some non-EU banks may reduce their activity, thereby putting liquidity in peril.

Why market making shrinks

The equity and debt markets are global and accessing them requires large banks with a worldwide coverage. American banks benefit from advantages in that regard. That is why major market players, corporates and large sovereign issuers, mainly opt for global US banks for their primary and therefore secondary market support. The dwindling number and market share of European market makers can to a large extent be attributed to the inability of European banks to thrive in the midst of continued fragmentation of Europe’s capital markets and an incomplete banking union.

Moreover, European banks had to adapt to a rapid succession of new regulations, particularly in terms of capital requirements, that increased costs and have weighed on their capacity to maintain high-quality services to investors in market making. For most European banks, the need to comply earlier with even a few of the newest Basel III requirements, at the request of regulators, was enough to increase the chasm of competitive edge.

Consequently, European banks have tended to withdraw from some market segments and reduced their worldwide coverage of clients to focus on their most profitable activities. When clients with a global footprint must choose among participants that provide capital market services, they might pick those with better pricing and execution capacity, such as US banks.

Additionally, we see the European scarcity in capital market innovation. European banks face more obstacles to develop on a large scale new technology-based trading solutions. The European Patent Office’s league table is dominated by US banks that filed more than 5,000 patents versus one European bank that registered 50.

How to strengthen Europe’s market makers

To revitalise market making in the 27-member European Union, we need to do three things:

- Complete capital markets union

- Assess the impact of Basel III standards

- Complete banking union

A robust CMU notably hinges on enhancing the capacity of European market makers to support secondary markets. CMU aims to bolster capital markets to reduce over-reliance of the European economy on bank financing and make capital raising easier, particularly for small and medium-sized enterprises and households. But this requires effective market makers. Reducing the dependency of EU capital markets on non-EU market makers would also bolster European financial strategic sovereignty and stability.

EU regulations should not inhibit European market making. That is why we welcome the European Commission’s recent package of legislative proposals to finalise the implementation of Basel III standards in Europe, which go in the right direction. The completion of banking union would also help European banks develop cross-border activities and encourage increased activity in the capital markets of Europe beyond their home country. Increasing critical size would enable European market makers to become more profitable and to encourage innovation, and in turn to improve the quality of service to customers.

Recent measures taken in the context of the European action plan to reboot the CMU initiative will have positive spill-over effects on market making activities as well. We welcome, for instance, the recent proposal to implement a consolidated tape by asset class for all EU countries. By expanding data transparency and providing a full picture of transactions across all trading venues, liquidity providers would be able to overcome the challenges of high costs and operational burdens that the current fragmented market ecosystem contains.

Improving the competitiveness and the attractiveness of EU financial markets is crucial. This is even more important now that Brexit has converted the UK into a formidable competitor at the EU’s doorstep, and one that does not hide its intention to make its regulation more attractive.

Acknowledgements

The authors of this blog would like to thank Olivier Pujal, José Cunha, Raquel Calero, Peter Lindmark, George Matlock and Mariia Penina for valuable comments and contributions to this blog post.

Further reading

Momentum builds for Europe’s capital markets union

Bringing Europe's securities together - speech by Kalin Anev Janse

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors