Reviving securitisation in Europe for CMU

More than a decade ago, the Global Financial Crisis pushed us to rethink securitisation. Banks landed in trouble, investors lost money, and a severe economic downturn ensued. Governments had to step in to help; securitisation stood accused of both masking and amplifying risks that caused the crisis.

Securitisation is the financial practice of pooling various types of debt, such as residential mortgages, car loans or credit card debt, and selling their related cash flows to third party investors as securities.

Due to expansion of poorer quality subprime mortgages and complex and opaque structures, especially in the US, securitisation received significant criticism. Yet over time, market participants have begun to better appreciate the benefits as well as counter the risks of securitised products. In the US, the biggest market for securitisation, this led to a revival with the market size now more than triple that of 12 years ago. In Europe, by contrast, the stigma persists and securitisations are a small fraction of what they were a decade ago.

In this blog, we explain how securitisation can be a key element in a successful European Capital Markets Union (CMU) and why, as we exit the pandemic, it could provide a springboard to economic prosperity.

When properly structured and monitored, securitisation is a powerful technique that can support the development of capital markets. In its latest action plan on CMU last November, the European Commission clearly identified the rise of securitisation as a key measure to build European capital markets. The authors of this blog presented it as one of the 5 “game changers for CMU” in a blog in 2020.

Securitisation shrank in the EU; in the US it expanded

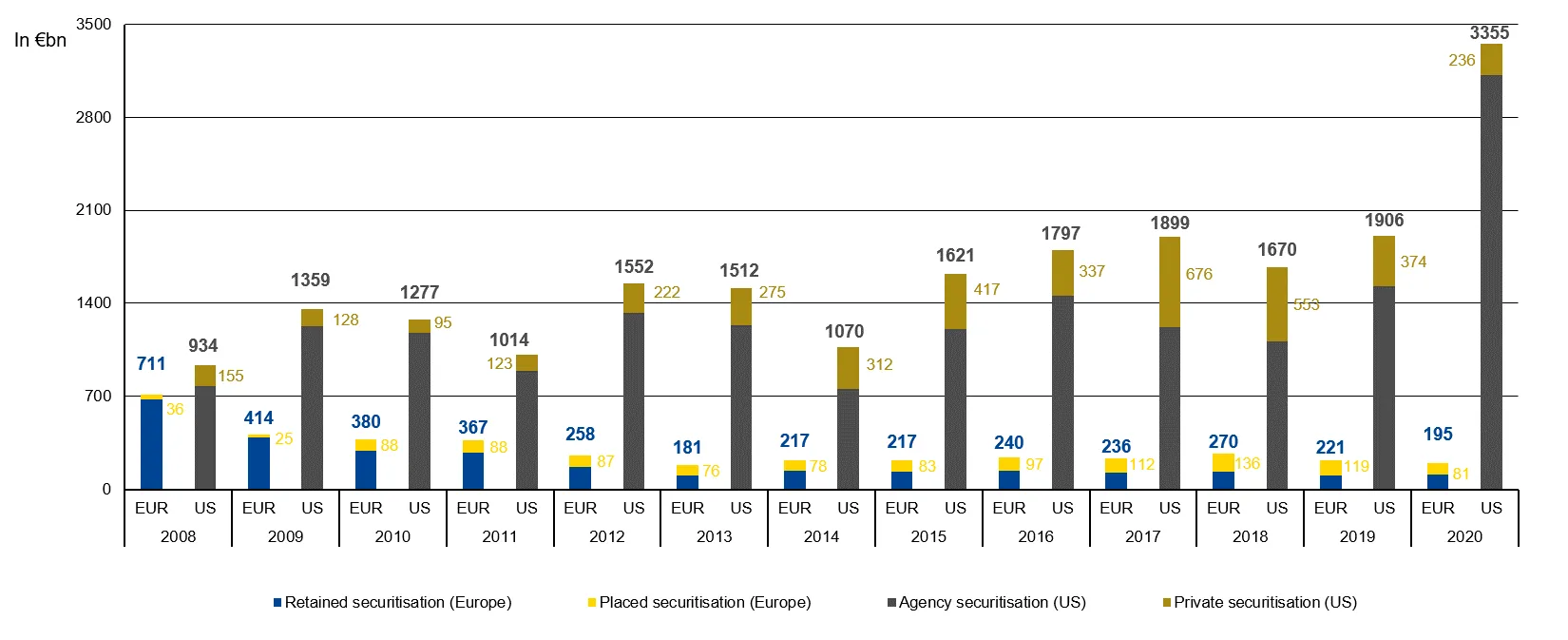

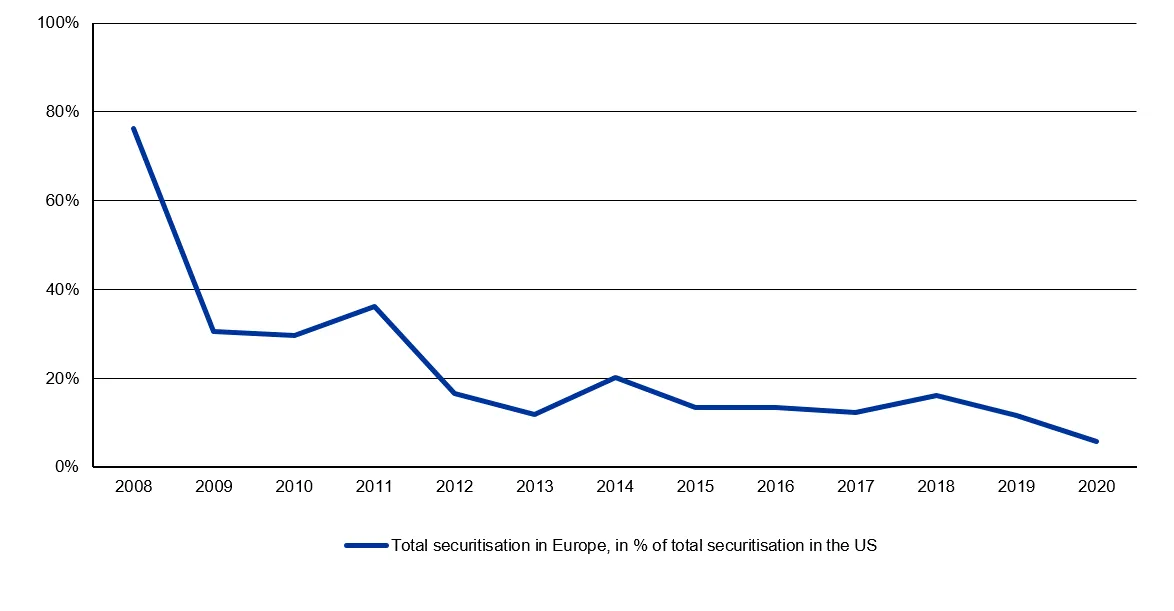

In 2008, the size of the European securitisation market, including the United Kingdom, was 75% that of the US. In 2020, it was just 6%. This is a quantum shift between both regions, despite similar private non-financial lending activities in both economies. When looking only at purely private transactions,[1] volumes were still three to six times higher in the US than in Europe, including the UK, over the last eight years.[2]

Figure 1: Securitisation volumes US vs Europe (including the UK)

Sources: AFME, ESM calculation

Figure 2: Europe’s securitisation volumes (including the UK) in percentage of US volumes

Sources: AFME, ESM calculation

The gap between both economies stems from the variety of legal frameworks applicable across EU Member States to securitisation operations. Transactions covering assets originated in different countries suffer from greater complexity and costs. In the wake of the crisis, the EU may also have adopted more demanding accounting and prudential rules than the US.

Well-regulated securitisation is a key tool for managing credit exposures and risks on banks’ balance sheets. It allows for the transfer of the risks associated with the initial assets to the market and provides banks with more capacity to extend lending to their customers. The risks and exposures of the initial assets are shared among multiple market participants, according to their risk appetite.

Securitisation can help manage banks’ balance sheet exposures, shed non-performing loans

Securitisation involves banks selling loans on their books to special purpose vehicles that fund the purchase of these assets via bond issuances with varying degrees of subordination. This frees up bank balance sheets for other activities by shifting these securitised assets to professional investors.

The subordination dictates the priority of payments stemming from the recovery of the underlying assets in case of default. This acts as a form of credit enhancement, as the lower tranches absorb losses first given they rank last in the payment hierarchy. Among other possibilities, additional credit enhancement can take the form of over-collateralisation, cash reserves, and guarantees from third parties like the European Investment Fund, as well as other forms of safety margins to protect from losses.

Well-designed securitisation provides an effective tool for banks to free up their balance sheets and release capital. Hence, it could be an effective tool to redeploy capital and support small and mid-sized companies (SMEs), spur recovery from the pandemic crisis, and aid the transition towards a sustainable and digital economy.

Moreover, the introduction of Basel 3 regulations in Europe will likely increase capital needs in the coming years and push banks to retain earnings for building up additional capital buffers, or deleverage by shrinking credit portfolios. A well-functioning securitisation market can help banks comply with new rules.

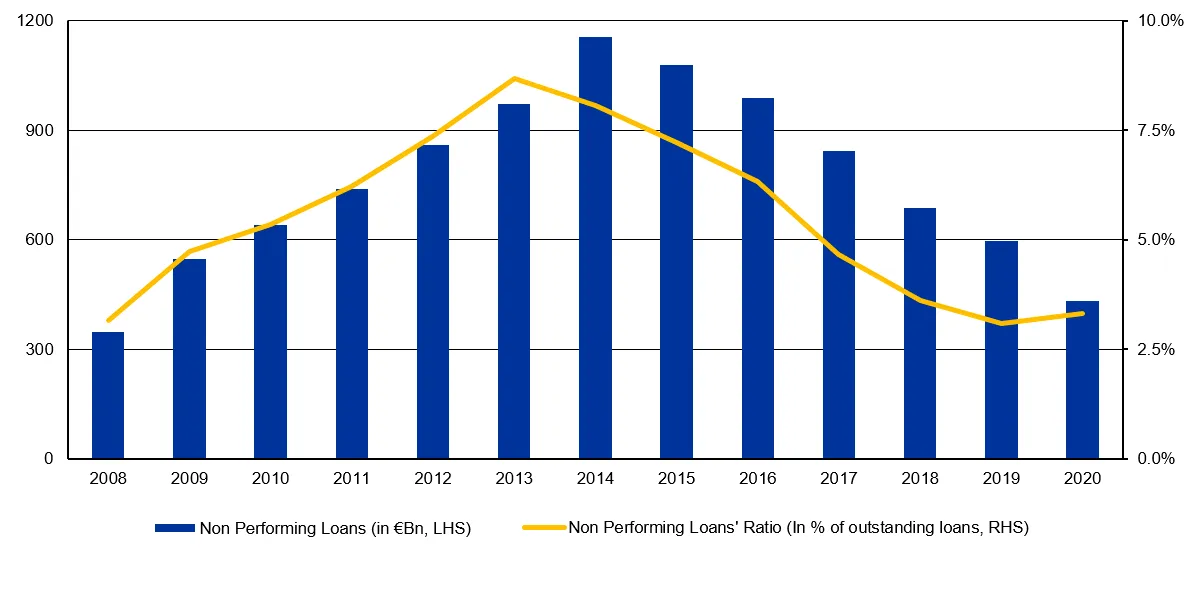

For this reason, securitisation helps to free up banks’ lending capacity. The Global Financial and European sovereign debt crises a decade ago showed the damage non-performing loans (NPLs) can do to banks. While this crisis was largely overcome in the past decade, NPLs are expected to increase when governments’ support provided during the pandemic crisis ends.

Banks heavily burdened by NPLs not only have less capacity to provide new lending but are also less attractive to investors. This further calls for solutions, such as securitisation, to ease the burden NPLs place on banks’ balance sheets.

Government-backed schemes launched in the past few years have especially helped kick-start new NPL securitisation transactions in countries heavily burdened by legacy issues. The benefits of NPL securitisations can have a broader impact. Moreover, the acceleration in the pace of risk reduction on bank balance sheets creates a more conducive environment for the political debate on the completion of banking union. Completing banking union will significantly support financial stability and euro area growth.

Figure 3: Non Performing Loans’ evolution in the EU

Source: ECB, Fitch Ratings, ESM calculation

However, the uncertainty around NPLs’ recoverability makes due diligence challenging and NPL-backed securities difficult to price. The varying insolvency and debt recovery frameworks across the EU as well as the lack of centralised and harmonised information on borrowers also impede the development of a pan-European secondary market for distressed assets.

Securitisation provides new investment opportunities

Securitisation can help reduce the over-reliance of European borrowers on bank financing and encourages access to capital markets. SMEs benefit the most from enhanced access to capital markets, especially start-ups that drive innovation but struggle to raise funds.

For investors, an additional supply of securitised assets would create more opportunities. Securitised assets allow investors to build up diversified portfolios exposed to market segments and to alternative borrowers from mainstream ones, such as SMEs, while providing a high degree of transparency and risk segmentation. Fixed income investors with longer-dated risk profiles also find it a real advantage to invest in securities backed by corporate credit or residential mortgage loans.

Investors may become more eager to participate in the digital and green transition with the creation of securitisation vehicles. In a prolonged low yield environment, growth of NPL-backed securities can also benefit from investors’ demand driven by a quest for higher returns.

Finally, securitisation is a valuable tool to increase risk sharing across the EU by facilitating cross-border investments. Fund managers, insurers or pension funds from one country could buy securities backed by assets originated in other European countries.

In summary, this has the opportunity to create a “win-win-win” situation: it allows banks to free up balance sheet monies for other activities, capital market investors to have more investment opportunities, and “final beneficiaries” (like SMEs) to access more sources of funding.

How to boost the European securitisation market?

First, refinements to the European policy and legal frameworks could boost the securitisation market as a whole. The implementation of the EU framework for Simple, Transparent and Standardised Securitisation (STS) and the EU Regulations defining capital requirements for banks and insurance companies have set high safety and disclosure standards for securitisation operations across the EU.

At the same time, EU policy-makers seem to agree that this regulatory framework may have created some hurdles to the development of the securitisation market in Europe. There could be an opportunity to provide more incentives for banks and investors to engage in securitisation. This may entail some refinements on capital charges attached to securitisation operations or some simplifications in the approval process of the transfer of risks, without reducing the necessary prudential safeguards.

Moreover, a European market for securitisation needs at least a minimum harmonisation of national insolvency laws, including collateral enforcement, to provide equal safeguards and predictability of outcomes to investors across the board.

Second, the EU needs to continue to facilitate the development of specific segments of the securitisation market, such as securities backed by NPLs or SME loans. A recent package voted by the European Parliament recognised the need for banks to reduce the burden of NPLs, including via synthetic securitisations, which could provide risk-weighted asset relief.

However, one needs to go further. Improving the quality and comparability of data on NPLs within the EU is a key action to help due diligence and the valuation of NPL transactions. Establishing a central data hub at EU level for NPL data, enforcing common reporting templates, would increase transparency at granular level and facilitate pricing. Harmonised and centralised data on SMEs would also make securitisation of SME loans easier.

Finally, the development of asset management vehicles on national and European levels as an outlet for NPL disposal could boost the case for a European securitisation market.

As Europe emerges from the pandemic and seeks economic growth, the moment to encourage careful securitisation is now.

Acknowledgements:

The authors would like to thank Olivier Pujal, Nicoletta Mascher, Loukas Kaskarelis, Joao Giao, and George Matlock for contributing to this blog post.

Further reading

Momentum builds for Europe’s capital markets union

European supervision fit for capital markets union

Europe greening the world: the “Brussels effect” on sustainable finance

Pandemic crisis as a catalyst for a common European safe asset

Footnotes

Excluding retained securitisation in Europe and securitisation backed by public agencies in the US.

AFME (2021) Securitisation Report Q4 2020, ESM calculation

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors