How a wholesale digital euro can strengthen Europe’s capital markets

From Bitcoin to Ethereum, cryptocurrencies compete for media headlines – but have delivered mixed fortunes to their bearers.

It is why we are sceptical about unregulated cryptocurrencies. While disruption can be a force for good, it is important to remember safety first in all that we do. That is why we believe public interest can best be served with some form of a regulated market. Hence, we support central banks in their progress towards a digital currency that can boost financial stability, the goal of the ESM.

Let’s remind ourselves why central banks were created. Financial panic in 1907 led J.P. Morgan and other financiers to call on the US Congress to engender trust in the system, prompting lawmakers to pass the Federal Reserve Act in 1913 and thus create a US central bank.

Today, central banks around the world are assessing how we can progress with the technology that powers cryptocurrencies while harnessing the potential of digital currencies. The ESM recognises the potential of such new-age currencies. The provision of a digital currency through a central bank rather than private cryptocurrencies can help boost efficiency, transparency, trust, and financial stability.

In this blog, we will discuss how a digital currency used by financial intermediaries could benefit capital markets.

This exciting prospect also prompted the ESM to issue a discussion paper Wholesale central bank digital currency – the safe way to debt capital markets and to co-host a seminar with the International Capital Market Association in April,[1] where speakers highlighted, among numerous topics, the fact that more than 90 central banks around the world are already studying central bank digital currencies.[2]

There are two kinds of digital currency being examined by central banks and debated by others. A retail currency that allows the public to transfer funds cashless and a wholesale currency for use within the capital markets. The wholesale currency would be for use by financial institutions with the potential for use by other actors, such as debt issuers, be they public institutions or corporates.

When properly designed, a wholesale central bank digital currency carries five benefits:

- Expedited execution

- Increased transparency

- Reinforced financial stability

- Actual scalability

- Cost savings for all parties

Importance of central bank money in wholesale financial markets

Wholesale securities transactions involve large sums of money, and participants in these transactions, such as commercial banks, need a safe and reliable settlement instrument to ensure that payment is made in a timely and secure manner.

At the top of the banking hierarchy is a central bank, acting as regulator and ultimate provider of liquidity to financial markets. Central bank money refers to the money supply that is created and backed by the central bank of a country. Or, in the case of the euro area, the money supply for a group of countries using a single currency, as is the case for the European Central Bank (ECB). This includes physical cash (banknotes and coins) and reserves held by commercial banks at the central bank. These are all direct claims on the central bank.

Commercial bank money, however, refers to the deposits created by commercial banks from which they issue loans or make other investments. When a bank lends money it creates a deposit for the borrower, which is recorded as a liability on the bank's balance sheet. It is a claim on the commercial bank itself and is subject to credit risk.

The absence of credit risk in central bank money makes it the safest settlement instrument for wholesale transactions.

Defining a digital euro for retail and wholesale use

The ECB began investigating a digital euro project in July 2021, following a consultation phase triggered by a report on a digital euro.[3]

Although retail use was the primary focus of this report, “Wholesale application of a distributed infrastructure” was already discussed in this landmark document.

But what exactly would be the retail and wholesale applications of a digital euro? They are, after all, not the same thing.

A digital euro for wholesale purposes would be an electronic version of the currency accessible only to financial institutions and market participants rather than the general public. The ECB has argued that digital wholesale payments in central bank money are already available in the euro area, namely via TARGET 2 and T2S, the ECB real-time gross settlement system.[4]

We should therefore make the important distinction that by wholesale digital euro, we mean a form of central bank money that is available on distributed ledger technology, a technology that is distributed among different operators whom all possess a copy of a common register. This form of money can then be used in programmes running on a decentralised infrastructure, namely smart contracts. This would be a wholesale digital euro allowing programmable payments, thus unlocking automation capabilities.

It is worth noting that securities could be represented on a distributed ledger technology and powered by smart contracts, also in the case of an intermediate model where payments would be triggered by the smart contracts but performed in traditional systems such as the ECB’s Real Time Gross Settlement System.

Reinforcing the international role of the euro and financial stability

Europe is not the only region looking at digital currencies. That is why a digital euro will be essential to strengthening the international role of the euro and to cementing the common currency’s competitiveness. To be an attractive and fully-convertible currency, the digital euro should be legal tender as is currently the case for cash. A growing number of jurisdictions are progressing on their own digital currency projects, including recent announcements by the United Kingdom and the United States.

A digital euro would also offer a safer alternative to so-called stablecoins, currently unregulated and potentially threatening financial stability, should the use of decentralised finance further expand. Different types of stablecoins exist, but recent events confirmed that none are as robust as a settlement instrument should be.

The need for a wholesale digital euro

Until recently, efforts towards the digital euro project have been focused on a potential digital euro for retail use. The Eurosystem announced on 28 April 2023 that it would explore potential solutions for central bank money settlement of wholesale financial transactions recorded on distributed ledger technology platforms.[5] As argued by many actors of the financial markets industry, wholesale aspects of a digital euro enabling programmability are essential to be included long term.[6]

In our recent discussion paper, we argue that such a wholesale digital euro could provide added value to the end-to-end debt issuance process.

Many experiments in various jurisdictions demonstrate how bringing on-chain the cash leg of wholesale transactions on digital bonds confers efficiency to post-trade. Examples include the World Bank’s first global blockchain bond in 2018, targeting “faster, more efficient and more secure transactions”.[7] Or the Bank for International Settlements’ Innovation Hub’s projects Helvetia, Jura, or Mariana. Similarly, the European Investment Bank’s bond issuances powered by public or private blockchain, ultimately aimed at “reducing costs, improving efficiency and allowing for real-time data synchronisation across participants”.[8]

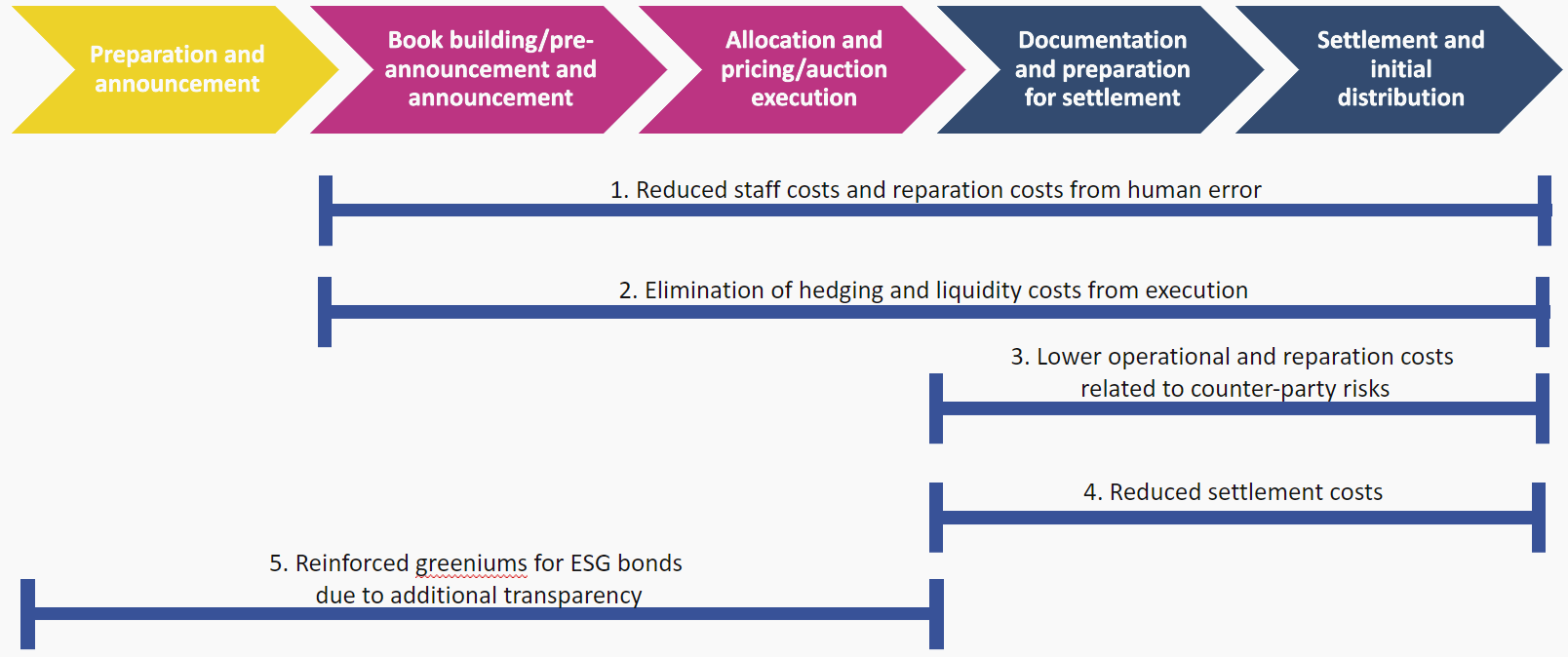

However, little has been explored on the added value of distributed ledger technology for pre-trade. Our discussion paper considers how distributed ledger technology and a wholesale digital euro could add efficiency to pre-trade steps of the debt issuance process (Figure 1).

Figure 1: Cost savings of on-ledger wholesale central bank digital currency in the case of sovereign bond issuance

Source: Authors’ compilation / ESM Discussion paper Wholesale central bank digital currency – the safe way to debt capital market efficiency

The path towards issuing a wholesale digital euro is not an easy one, but potential efficiency gains and reduction of existing risks are persuasive motivators. However, new risks may arise worthy of careful consideration, such as cybersecurity and privacy. Just as is the case for a potential retail digital euro, there is a need for a thorough analysis and experimentation of the technical design of a wholesale digital euro.

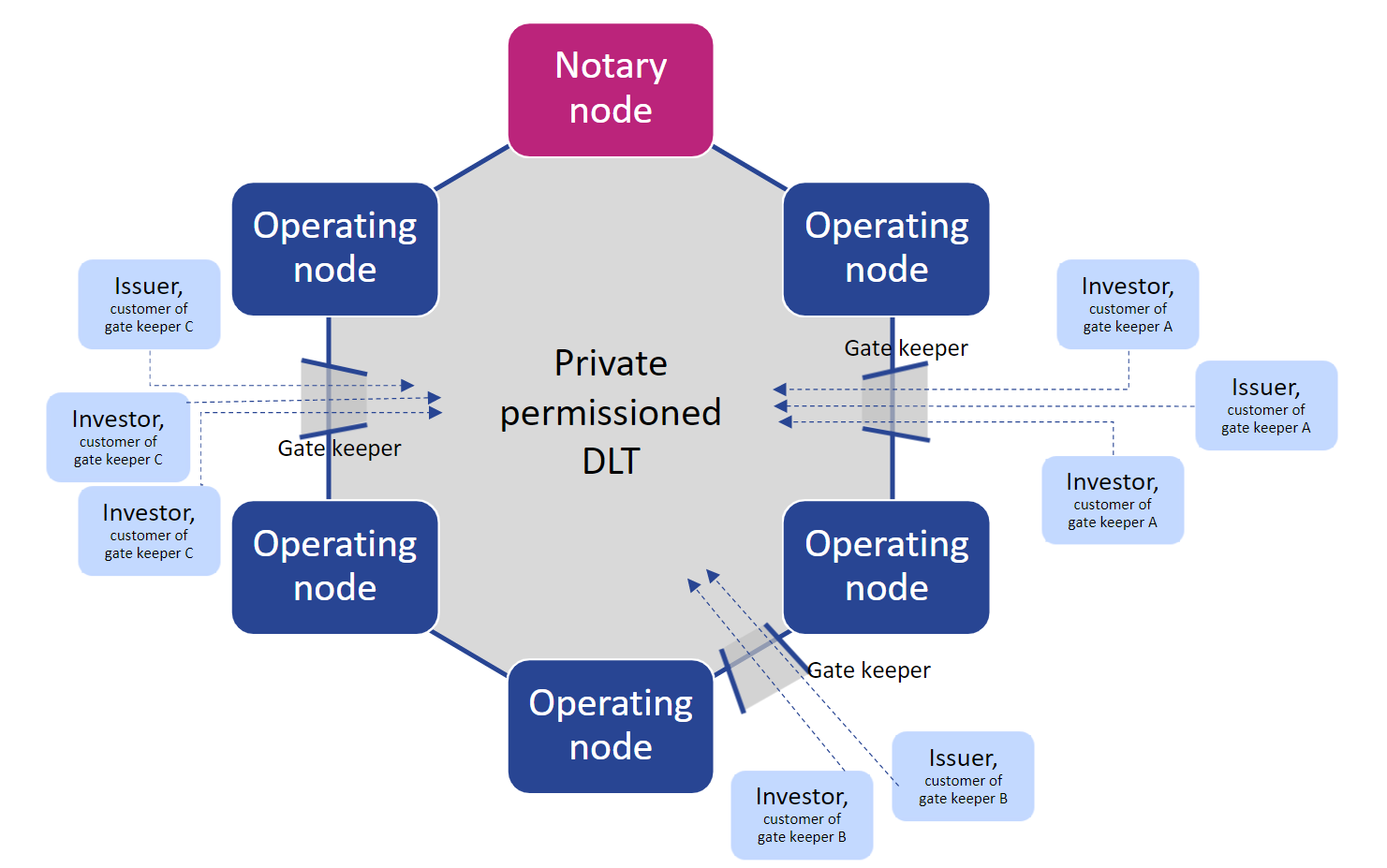

Our discussion paper outlines a proposed technical setup based on a private permissioned blockchain operated by the ECB and regulated actors. This setup, coupled with an on-chain wholesale digital euro, would present a balanced solution that simultaneously harnesses the benefits of this new infrastructure while limiting the risks (Figure 2).

Figure 2: Private permissioned distributed ledger technology operated by regulated actors

Source: Authors’ compilation / ESM Discussion paper Wholesale central bank digital currency – the safe way to debt capital market efficiency

Further testing around on-chain, end-to-end debt issuance automation would allow market participants to confirm the gains we foresee in this paper – an exciting concept!

The future begins today

To upgrade capital markets for the 21st century, we must develop a strong digital central bank currency. A successfully introduced digital currency will strengthen its role as a leading reserve currency in the world. The challenge is on for Europe to step up its game.

Acknowledgements

The authors would like to thank Rolf Strauch, Herbert Barth, Edmund Moshammer, Stefano Finesi, Nicoletta Mascher, Wim Van Aken, George Matlock, and Raquel Calero for their valuable comments and contributions to this blog post.

Further reading

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors