Keeping a deepened euro area on the agenda - speech by Rolf Strauch

Rolf Strauch, ESM Chief Economist

“Keeping a deepened euro area on the agenda”

Annual Lecture in Economics 2019

Dear Chairman Clerides,

Dear Vice-President Tirkides,

Dear ladies and gentlemen,

I feel honoured to give the Annual Lecture in Economics here at the Bank of Cyprus. This special event is organised by the Cyprus Economic Society, whose mission is “to combine practical economic research with public debate and policy making”. And I hope I can contribute to this mission with my lecture today.

These are politically important times for the European Union as a new political and institutional cycle will start soon. During the next days and until Sunday, citizens all across Europe will vote for the new European Parliament.

This lecture is not meant to be an electoral speech. But needless to say, I have a personal position, and the ESM has an institutional position as well. We believe that a strong and functioning European Union will continue to protect and support its member states. As Commission President Juncker said in his last State of the Union speech: “United we stand taller!”

This lecture is a timely opportunity to recap what has happened over the last EU institutional cycle and to provide an outlook – both economically and politically.

The current economic situation: where do we stand today?

Let me start with the economic outlook for the euro area. We are clearly at a turning point of the cycle. After years of above-potential growth, a "normalisation phase" naturally follows. As economists we know that this is in line with the maturing global economic cycle.

Last year, the euro area grew by 1.9%. This year and beyond, growth will slow down to a more moderate pace. Recent forecasts point to a continued moderation with GDP growth at 1.2% in 2019, centring around potential-growth estimates for the euro area.

On the back of stronger fundamentals this year and a pick-up of global trade next year, euro area growth is expected to gradually recover in 2020 (1.5% on a yearly comparison).

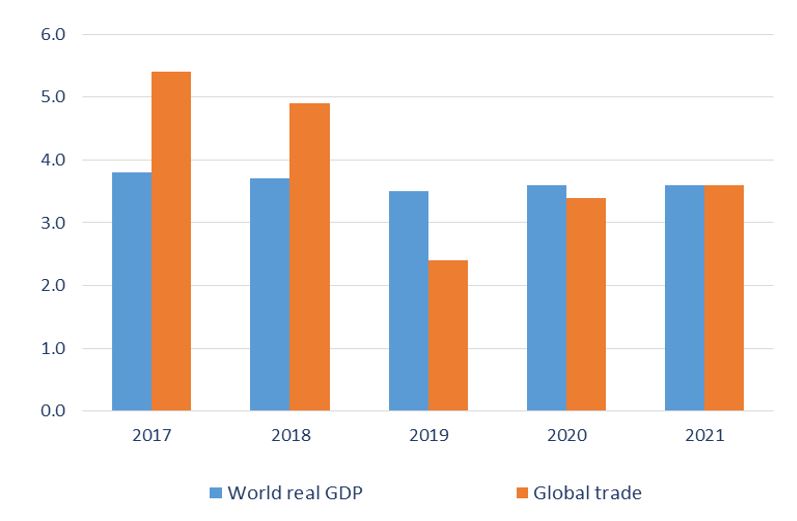

Two key factors explain the cooling down of growth in the euro area: the external environment and some one-off factors. First, international trade disputes have slowed down global trade (Figure 1). Second, within the euro area, some one-off factors – such as environmental permissions in the car industry and policy uncertainty in some member states – have led to a sharper than expected slowdown. These factors from 2018 are temporary, but carry over into 2019. At the same time, investment and total consumption remained overall fairly robust.

Figure 1. Global real GDP and trade evolution (2017-2021)

Source: ECB staff macroeconomic projections. Note: 2017 refers to final data of the September 2018 projections. For the period 2018-2021, projections from March 2019 have been used.

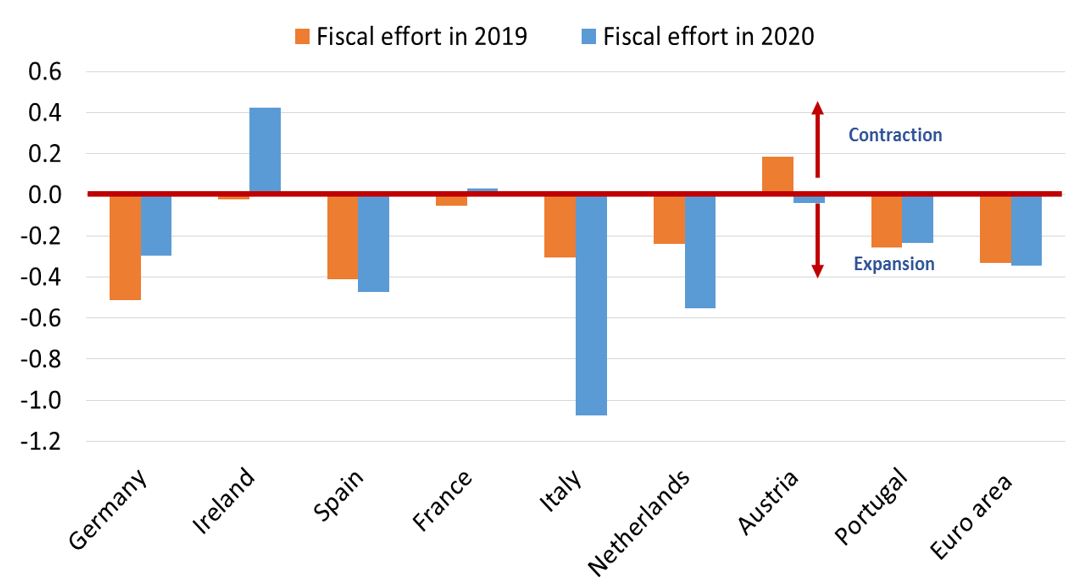

Improvements in domestic economic fundamentals are supporting the stability of the euro area. On the back of continued employment and wage growth, household disposable income is rising and domestic demand remains strong, despite a temporary dip in production. Moreover, some member states are expected to adopt expansionary fiscal policy (Figure 2). Their fiscal space available under the EU fiscal rules is being assess by the European Commission.

Figure 2. Fiscal effort in the euro area in 2019 and 2020

Source: AMECO. Note: Change in percentage points of the structural primary balance between 2019 and 2018 and between 2020 and 2019 in % of potential GDP. (-): expansionary stance, (+): restrictive stance.

In a nutshell, the moderation in euro area growth is not a reflection of economic weakness. It is a natural normalisation phase related to the maturing global economic cycle and external downside risks. Nonetheless, this slowdown in growth leads to questions – also among economists – whether the euro area is sufficiently strong or whether we are facing the next recession. In my view, we currently face a moderation in growth but not a recession.

Let me now highlight where the euro area has actually managed to redress the consequences of the seminal crisis of 2008 to 2012 and has gained strength.

Achievements in overcoming the crisis – towards a more robust euro area

When assessing the current economic situation, we have to be mindful that over the past decade, the euro area mastered two crises: first, we had to overcome the effects of the 2008 global financial crisis. Second, we had to deal with the effects of the sovereign crisis.

From an institutional and economic point of view, the euro area has overcome or reduced some of the imbalances that led to the past crisis and followed from it.

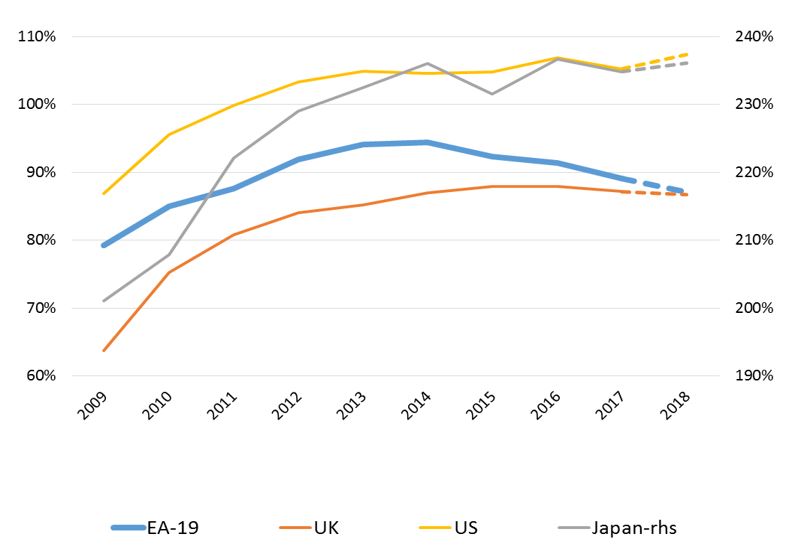

Since the sovereign crisis, the euro area has managed to stabilise and reduce its public debt – contrary to other advanced economies such as the US, Japan and the UK (see Figure 3). This is overall positive as it creates some fiscal space. But we know that the distribution of debt levels is uneven among member states, and countries with higher debt levels remain more vulnerable.

Figure 3. Public debt-to-GDP (%)

Source: AMECO. Note: 2018 refers to forecast data.

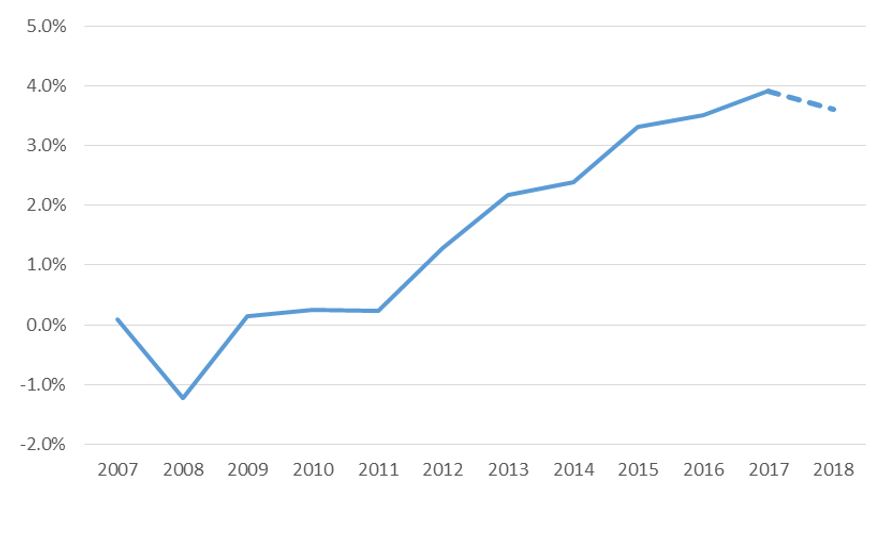

Moreover, external imbalances that fuelled the sovereign crisis at the euro area level have now turned positive (see Figure 4). Current account imbalances were reduced across the board, and countries are improving their foreign investment position. During the recent upswing, countries showed high growth rates without widening external deficits.

Figure 4. Euro area current account balance with the rest of world (% of GDP)

Source: AMECO, European Commission Spring 2019 Economic Forecast. Note: 2018 refers to forecast data.

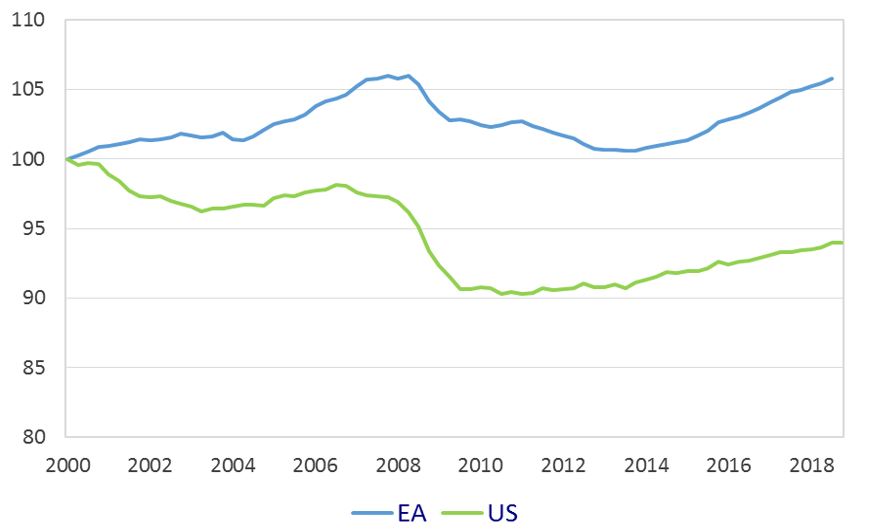

These improvements also extend to the domestic real economy, including the euro area labour market. At slightly below 8%, unemployment stands now at its lowest level since 2008. Employment growth was strong in 2017, with some signs of normalisation in the end of 2018 and beginning of 2019 (see Figure 5). Overall, there are more people on the job now than before the last crisis. Moreover, the labour market recovery after the last crisis is marked by improved participation rates.

Figure 5. Employment rate (index = 2000)

Source: Eurostat, US Bureau of Labor Statistics. Note: Cumulative change in percentage points. Age group: 15+ for euro area, 16+ for US. Latest observations: Q4 2018 for euro area, Q1 2019 for US.

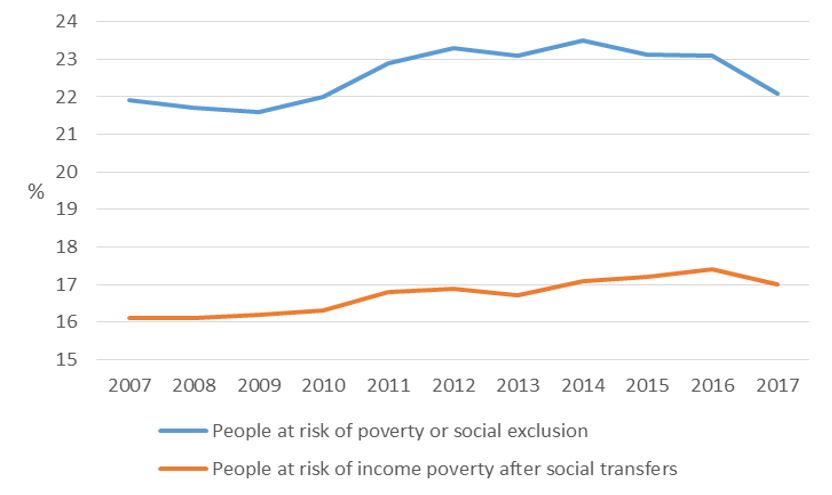

We see that poverty rates have started returning to pre-crisis levels (see Figure 6). Europe has stronger social policies and more equally distributed incomes than essentially any other region of the world.

Figure 6. Percentage of EU citizens at risk of poverty or social exclusion

Source: EU-SILC. Note: People at risk of poverty or social exclusion corresponds to the sum of persons who are: at risk of poverty after social transfers, severely materially deprived or living in households with very low work intensity. Persons are considered to be at risk of poverty after social transfers, if they have an equivalised disposable income below the risk-of-poverty threshold, which is set at 60% of the national median equivalised disposable income

And finally, looking at the financial sector, we see that banks are safer now than before the crisis – they are better capitalised and are also under more comprehensive regulation and supervision. In terms of risk-sharing, non-performing loans have been drastically reduced during the last years, though they are still too high in some countries.

Thus it is not by chance that support for the euro as our single currency has grown substantially again. Three in four euro area citizens support the single currency and the euro area as a whole. 75% of EU citizens think that the euro is a good thing for the EU, in Cyprus it is 65%. Overall, support for the single currency has never been higher.

To protect the single currency, Europe came up with a robust answer, which included five components:

First, in particular member states with ESM loans, such as Cyprus, have largely eliminated their macroeconomic imbalances. These countries have shown a strong willingness to reform and consolidated their budgets and improved their competitiveness compared with the euro area average. As a result, Ireland, Portugal, Spain and Cyprus are experiencing high growth rates and falling unemployment. And they can refinance themselves on the market again. That is why we call these countries “success stories”.

Second, the European Central Bank (ECB) successfully intervened with its unconventional monetary policy to stabilise the euro area.

Third, economic coordination and surveillance has been improved.

Fourth, the banking union was created: the Single Supervisory Mechanism (SSM), which oversees systemically important banks, and the Single Resolution Mechanism (SRM), which resolves banks.

Fifth, the two crisis resolution mechanisms were created. In 2010, the temporary European Financial Stability Facility (EFSF) was established and two years later, the permanent crisis resolution mechanism, the European Stability Mechanism (ESM).

The ESM was a key contributor in overcoming the crisis and in strengthening the recovery of countries that experienced difficulties. The euro area in its present form would look different without the ESM. Of course, the ESM could not have solved the crisis on its own.

Before the crisis, there was no "lender of last resort for sovereigns”" in the euro area. Because the ECB is the lender of last resort for euro area banks, not for countries. Thus, these two institutions closed a gap in the framework of the monetary union.

The ESM applies the principle of the International Monetary Fund (IMF): loans are combined with strict conditionality. This “cash against reforms principle” means loans will only be disbursed if the country implements the reforms agreed in its ESM programme. As many of you know, these reforms are often painful, both for the government and for the households. But they are necessary to restore competitiveness and regain investor confidence.

The ESM obtains the money for its loans by recurrently issuing bonds in the international market. It is one of the largest euro-denominated bond issuers. The programme countries will repay their loans in full with interest. ESM programmes do not use taxpayer money, contrary to what is often said.

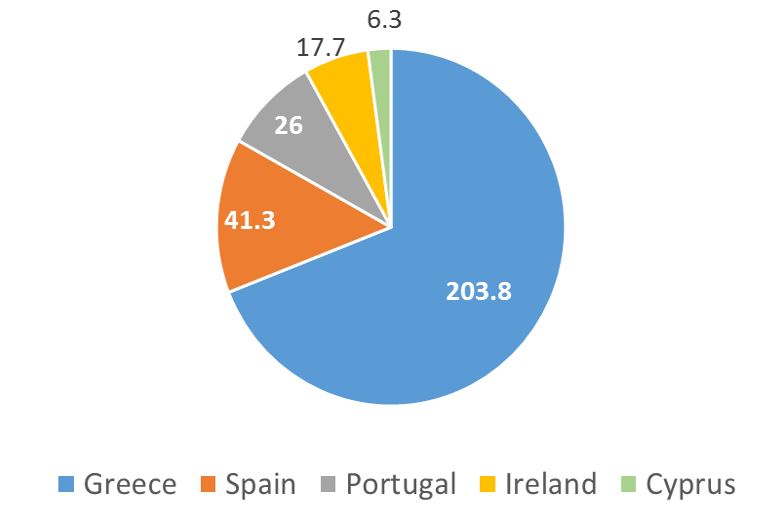

Since 2011, five countries have received financial support of €295 billion: Cyprus, Ireland, Greece, Portugal and Spain. The ESM still has an unused lending capacity of over €410 billion (see Figure 7).

Figure 7. Disbursements to former EFSF/ESM programme countries

Source: ESM. Note: Total loans disbursed by EFSF and ESM in billion euros.

In a nutshell, the achievement of overcoming the crises was significant. As a result, the euro area is in many respects institutionally more resilient than ten years ago.

Cyprus as former ESM programme country

At this point, I would like to touch upon how I see the Cypriot development in this context. Cyprus was the fourth country receiving support by the ESM. Although the loans amounted to almost half the size of the Cypriot economy, Cyprus mastered its challenges, and successfully exited the programme three years later.

Cyprus has since the start of the ESM-programme pushed through a long list of reforms, modernised its economy and its legal framework. It has restructured and recapitalised its banks, improved financial regulation and supervision. Its fiscal deficit has shrunk, and the public debt is now on a downward trend.

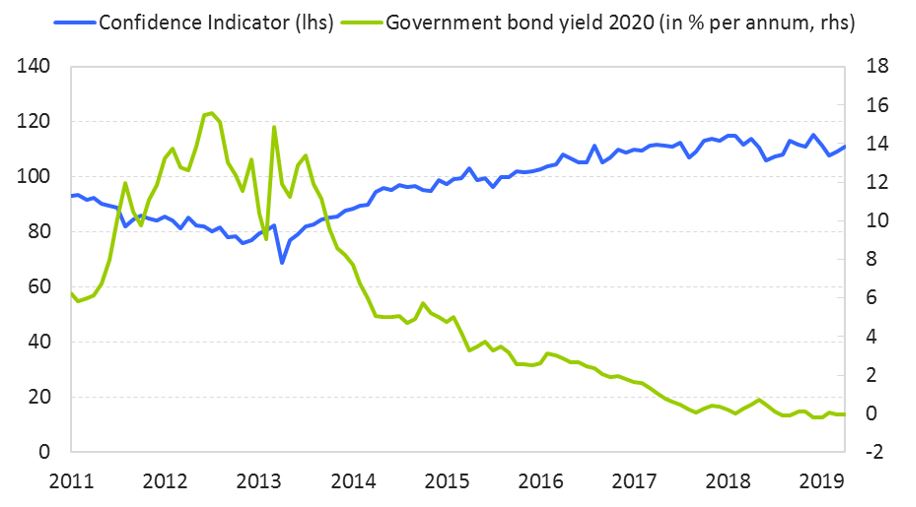

That is why Cyprus is today one of the success stories of the ESM. The country can once again finance itself on the market with steadily declining financing costs (see Figure 8). At the same time, unemployment is rapidly falling. With almost 4% real GDP growth in 2018, Cyprus continues to enjoy a remarkable post-crisis rebound.

As the external environment turns less favourable and the private sector continues to deleverage, growth is forecast at around 3.1% this year and around 2.7% in 2020. The growth momentum should ease further as elsewhere, mostly reflecting the less favourable external environment. The budget is expected to return to surplus and public debt is expected to decline from this year onwards.

Figure 8. 2020 bond yield and confidence indicator of Cyprus

Source: European Commission, Bloomberg. Note: 10-year yields are not available for the time span desired, bonds yield with a maturity in 2020 used.

Despite the fact that growth is currently slowing down, the current favourable economic conditions provide a window of opportunity to accelerate structural reforms. These reforms would boost potential growth and further reduce the remaining legacies of the past crisis, in particular non-performing loans and indebtedness.

There are a number of reform areas where Cyprus could do more. One key priority is the judicial reform, which is essential for the functioning of the economy. Another one is the long-overdue reform of the title deeds issuance and transfer system. It is also essential to improve the efficiency in the public sector, in particular the functioning of the public administration and of local governments. These reforms would help diversify investment to sectors other than construction and tourism, currently the key drivers of growth.

Short-term risks and longer-term challenges

Alongside the former programme countries, Europe also worked on many institutional shortcomings that led to the past crisis. Progress has been made that seemed unimaginable before the crisis. But more needs to be done to make the euro area fully robust. Let me briefly outline the main short-term and longer term risks and challenges from my perspective.

There are currently two major sources of external risks, which have both short-term and possibly longer-term effects.

First is the effect of the current trade disputes on the euro area as the world is experiencing a push of de-globalisation and neo-mercantilism. This is a new phenomenon in the post-war period and it is driven by the US-China trade war.

An escalation of protectionism would have significant consequences also for the EU: the US was the largest partner for EU exports last year and the second largest for EU imports. The consequences are difficult to predict but by no means positive. Responding to high uncertainty, economic sentiment in the euro area continues to disappoint. Restricting free trade also undermines the long-term prospects for growth along with investor confidence.

The second most immediate risk for Europe is Brexit. Although the extended deadline gives some breathing space and further time to prepare. Most of the financial stability risks are well contained following the actions of supervisory authorities as well as the ECB and the Bank of England.

Brexit is a challenging situation where losses are overall tilted towards the UK. But, a “no-deal” Brexit situation would also worsen the euro area outlook; it will specially hit those countries that are strongly connected to the British economy.

Then there are still other, longer-standing challenges ahead of us, limiting euro area potential growth in the future.

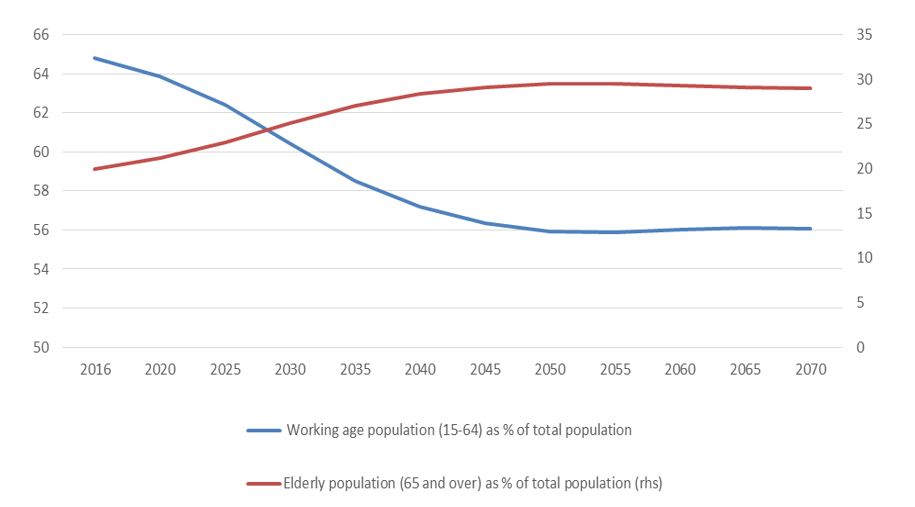

These long-term challenges refer, first, to unfavourable demographics that are gradually expected to use some of the fiscal space of the euro area. The elderly population is growing faster than the younger generations, which may create supply-side constraints for labour markets in the euro area (see Figure 9). Future immigration dynamics will affect the euro area labour markets. A coherent and forward-looking immigration policy may offset the adverse impact of an ageing population on potential output in the EU.

Figure 9. Working and elderly age as part of total population (%) in the euro area

Source: European Commission, Ageing report 2018.

Second, with constrained labour supply, productivity should be the main driver of potential growth. Unfortunately, the track record in this respect is fairly weak for many European countries. The need to scale up labour quality and allow for productivity gains through innovation becomes stronger if we want to maintain past growth rates.

Third, we should be aware of a structural change in financial market behaviour and its implications for longer-term convergence. Before the euro debt crisis, sovereign risk for euro area countries was not priced in. This has changed and we have witnessed episodes of high market volatility for countries with high debt levels. European sovereigns may now face different risk premia. This can entail a positive disciplining effect. At the same time, spreads often affect the funding costs of the private sector in the economy. Continued differences in financing costs would make the economic convergence among euro area countries more difficult to achieve. In the short run, higher servicing costs will for sure reduce the available fiscal space and the ability to put in place countercyclical policies for the euro area countries.

Policy response

I have described the past achievements and challenges to you. Let us now take a forward-looking stance. What can Europe do to address these challenges? This brings me to the third part of my lecture, in which I would like to describe the remaining steps in deepening the euro area to strengthen it and to make it more resilient.

Short- and longer-term policy agenda

To prepare the euro area better for the future, the December Euro Summit adopted a reform package to deepen the monetary union. This involves the completion of banking union, the further development of the ESM and fiscal issues. For the ESM this implies different elements (see Figure 10):

Figure 10. Overview of ESM reforms

Source: ESM.

First, the ESM will provide the backstop in bank resolutions carried out by the Single Resolution Board. It will be “fiscally neutral”, which means that there will be no additional burden on taxpayers. By 2024 at the latest, the backstop should be fully operational. Right now, we are working on the last details.

Second, the ESM will play a stronger role in future economic adjustment programmes. In collaboration with the European Commission, the ESM will design, negotiate and monitor future assistance programmes.

Third, the ESM’s toolbox was reviewed to make the use of precautionary credit lines more effective.

Fourth, there should be more transparent and effective means to ensure debt sustainability when entering into an ESM programme.

Looking at what has happened since the crisis, and bearing in mind the December decisions, one might wonder if this is sufficient to prepare the euro area for the future. The December decisions are another important step towards a more robust monetary union. The Summit also mandated the Eurogroup to work in two areas where the discussions are still controversial: a common European deposit insurance and a euro area budget.

The completion of banking union focuses primarily on the deposit insurance, which is the missing third pillar envisaged from the start. But this is not the only element missing. More steps need to be taken to create a level playing field for banks across the euro area and beyond. This includes a further reduction in national discrepancies, the harmonisation of insolvency laws and a removal of barriers to capital and liquidity use across banking groups. Euro countries also need to agree on a mutually acceptable balance between risk-reduction and risk-sharing. This means a further reduction in non-performing loans and a re-balancing of government bonds in bank balance sheets.

Lastly, the introduction of a euro area budget should support convergence and competitiveness among euro area countries. The Euro Summit mandated “the Eurogroup to work on the design, the modalities of implementation and timing of a budgetary instrument for convergence and competitiveness”. This is a positive step as it will encourage structural reforms and strengthen competitiveness in the euro countries. Convergence reduces the risk of macroeconomic and financial imbalances, while competitiveness strengthens the growth potential and the stability of the economies.

Need to progress on private and public risk-sharing and convergence

It is currently expected that elements of this agenda may be decided or endorsed already at the next Euro Summit in June 2019. Others, in particular the completion of banking union, are still controversial and may require further discussion. The implementation of all measures inevitably leads into the next institutional cycle.

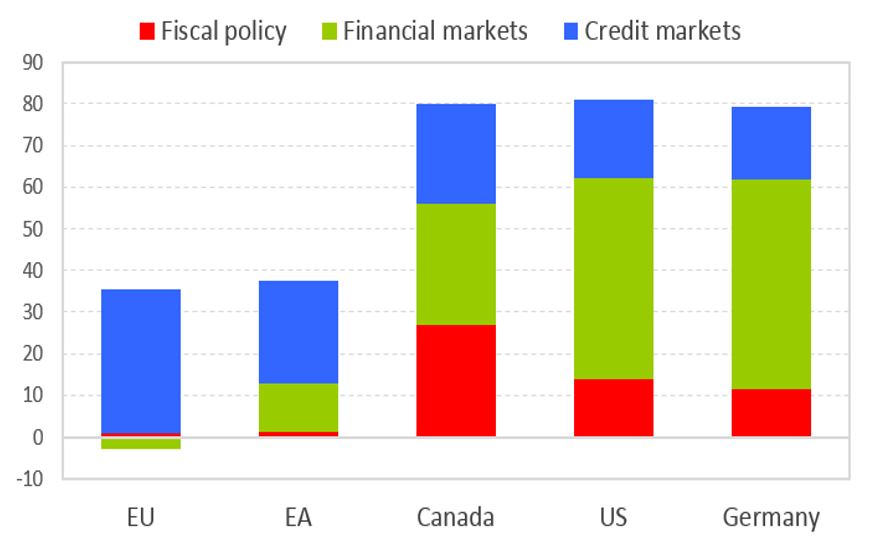

There are additional elements, not on the current agenda, which can further support the functioning of monetary union. The completion of the banking union and the use of new fiscal tools serve the same economic objective: to increase economic risk-sharing. Economic risk-sharing is underdeveloped in the euro area, when compared to the United States, but also compared to risk-sharing within France or Germany (see Figure 11).

Figure 11. Percentage of shocks smoothed by different channels

Source: IMF Staff Discussion Note (2013), “Towards a Fiscal Union for the Euro Area”.

On the private sector side, next to the completion of banking union, we need to think about improvements of European capital markets. The need to strengthen a European capital markets union even increases in light of Brexit. A number of initiatives have been taken to implement the capital markets union by the current European Commission. Some important issues are still pending for discussion, and other issues are not yet fully addressed. This includes more clarity on the need to regulate the shadow-banking sector to avoid liquidity risks, taxation and further harmonisation of insolvency law, and properly handling big-tech companies entering the market.

On the side of public risk-sharing, I am an advocate of the fiscal stabilisation instrument avoiding fiscal transfers. Such a fiscal policy tool could help avoid a situation when a large shock hitting part of the euro area triggers negative spill-overs onto the EU as a whole. It could be structured as a “rainy day fund” which exist in the US and is now also being established for example in Ireland at the national level. Alternatively, it could take the form of an ESM credit line. There are many proposals in the public debate.

However, it should also be considered that before any step is taken in this direction, there is a need to increase trust among member states and strengthen their ability to create fiscal space. The European fiscal framework has become very complex over the crisis years. An attempt needs to be made to simplify the fiscal rules to make them more efficient. Several proposals – among others by the IMF and the European Fiscal Board – point to a combination of a debt and an expenditure rule as a possible way forward.

Finally, I think we need to also keep the topic of a European safe asset on the agenda. Such an asset could help to create common financing conditions, lead to the diversification of bank exposures to sovereigns, and strengthen euro area capital markets. By creating a more liquid and deeper euro area market for securities, it would also strengthen the international role of the euro.

A number of proposals have been made how to structure a European safe asset without mutualisation of debt and permanent transfers among euro area member states. It is helpful to work on this topic. However, this is not an equivalent for Eurobonds, for which the euro area is neither politically nor structurally prepared in the foreseeable future.

Drawing a longer-term vision for deepening the euro area also implies a stronger international role of the euro. A globally stronger euro would improve the resilience of the international financial system. It would also provide market participants around the world with additional choice, and make the international economy less vulnerable to shocks linked to the strong reliance of many sectors on the US dollar.

Conclusion

This brings me to my concluding point. We will be better prepared to weather the next crisis if policy-makers in Europe stay focused on completing the agenda of reforms for strengthening EMU and the international role of the euro.

Since the crisis, the euro area has increased its robustness. But there are still steps that need to be taken in order to strengthen the euro area. Politically and institutionally we are in a middle of a crucial year. That is why I consider it important that the policy-makers keep a deepened euro area on the agenda following the European Parliament elections.

Thank you for your attention.

References:

Consilium (2018), Future cooperation between the European Commission and the European Stability Mechanism. Available at: https://www.consilium.europa.eu/media/37324/20181203-eg-1b-20181115-esm-ec-cooperation.pdf

European Commission (2019), Europe in May 2019, Preparing for a more united, stronger and more democratic Union in an increasingly uncertain world. Available at: https://ec.europa.eu/commission/sites/beta-political/files/euco_sibiu_communication_en.pdf

European Commission (2019), Spring 2019 Economic Forecast – Cyprus. Available at:

https://ec.europa.eu/info/sites/info/files/economy-finance/ecfin_forecast_spring_070519_cy_en.pdf

European Commission (2019), Spring 2019 Economic Forecast. Available at: https://ec.europa.eu/info/business-economy-euro/economic-performance-and-forecasts/economic-forecasts/spring-2019-economic-forecast-growth-continues-more-moderate-pace_de

European Commission (2019), Staff statement following the sixth post-programme surveillance (PPS) mission to Cyprus. Available at: https://ec.europa.eu/info/news/staff-statement-following-sixth-post-programme-surveillance-pps-mission-cyprus-2019-mar-22_en

European Commission (2019), Assessment of the 2018 country-specific recommendations implementation. Available at: https://ec.europa.eu/info/sites/info/files/file_import/2019-european-semester-country-report-cyprus_en.pdf

European Commission (2018), Standard Eurobarometer Autumn 2018, Press release. Available at: http://europa.eu/rapid/press-release_IP-18-6896_en.htm

European Commission (2018), State of the Union 2018: The Hour of European Sovereignty. Available at: https://ec.europa.eu/commission/news/state-union-2018-hour-european-sovereignty-2018-sep-12_en

European Fiscal Board (2018), 2018 annual report of the European Fiscal Board. Available at: https://ec.europa.eu/info/publications/2018-annual-report-european-fiscal-board_en

European Stability Mechanism (2019), Financial Assistance to Cyprus. Available at: https://www.esm.europa.eu/assistance/cyprus

Author

Contacts