The impact of the EU’s pandemic response on financial markets - speech by Jürgen Klaus

Jürgen Klaus, ESM Team Lead Derivatives and Market Intelligence

Presentation on “The impact of the EU’s pandemic response on financial markets”

Riga Graduate School of Law webinar

Online, 8 June 2021

(please check against delivery)

Ladies and Gentlemen,

let us take a look at the market impact of the EU’s measures to support the economy during the pandemic.

The package of EU and national crisis response measures are an expression of European solidarity. I would like to emphasise that it is this demonstration of solidarity which calmed markets. In fact, this solidarity is a key element for understanding the current financial market sentiment and - more broadly - for explaining the continued financial stability in the euro area during this crisis.

The European Central Bank supports the market for debt securities with various measures. They include regulatory easing for market participants and a large debt securities buying programme. We call it the Pandemic Emergency Purchase Programme, PEPP for short, which enables sovereigns to maintain access to financing on favourable terms (we will look at this in a moment).

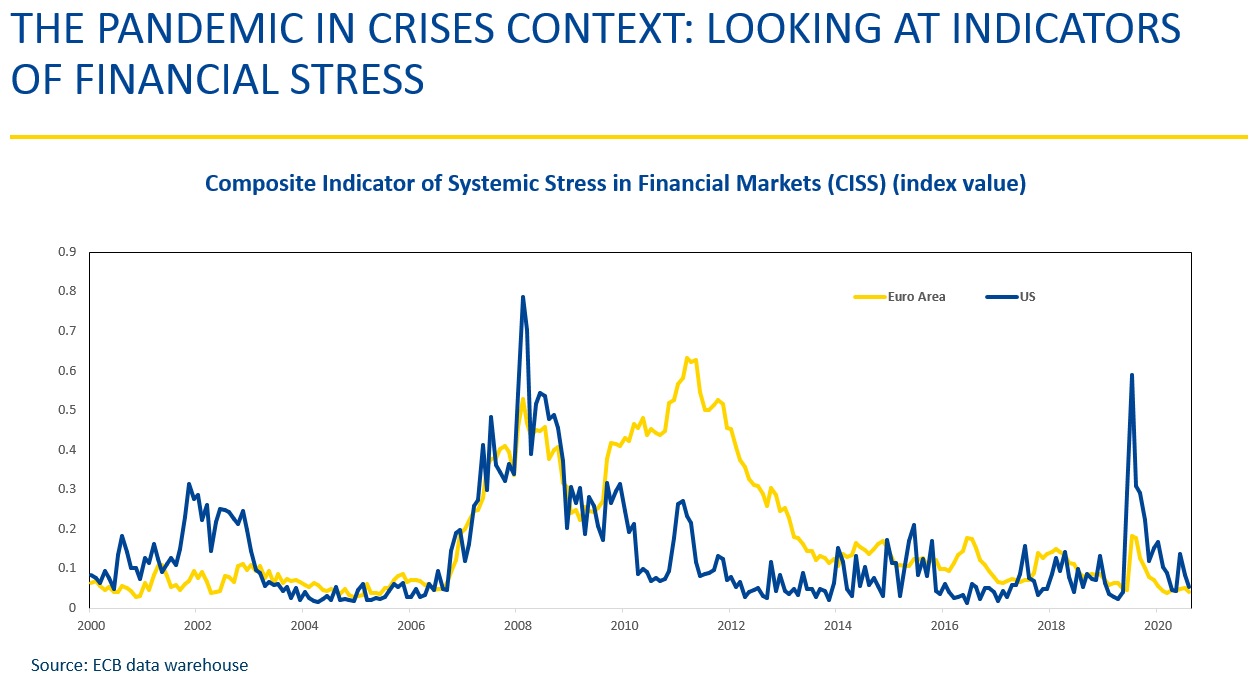

Financial markets can be erratic, over-active and - in extreme cases - cause severe damage to financial stability and the economy. In short, markets can be in stress and amplify stress. Financial market stress can be measured as we show in slide 1.

The Composite Indicator of Systemic Stress, CISS in short, is computed for the euro area in yellow and includes fifteen raw, mainly market-based financial stress measures that are split equally into five categories, namely the financial intermediaries sector, money markets, equity markets, bond markets and foreign exchange markets. The higher the stress, the higher the curve. For comparison, you see the US equivalent in blue.

I would like to point out two things: First, you of course see the massive outbreaks around the financial crisis in 2008 and a more prevailing stress level around the euro crisis. Second, compared to the recent past since 2000, we find that financial stress appeared to a lesser extent and was corrected, or relaxed, faster during the recent pandemic crisis.

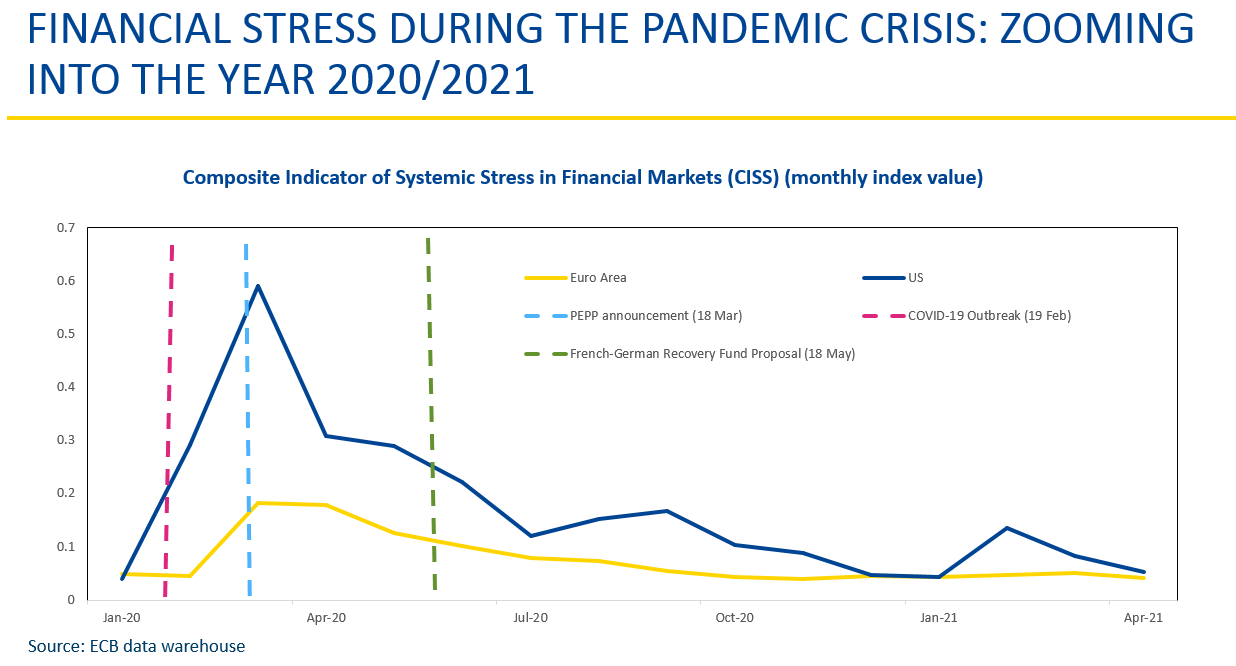

Zooming into the current crisis in chart 2, we find the market stress levels back at pre-pandemic levels after an initial spike n March 2020.

So from a broader angle - based on these stress indicators - markets are back to pre-pandemic levels. Market feedback indicates that this was thanks to the unprecedented degree of European solidarity. The swift implementation of the joint measures helped calm down the market. As you can see in slide 2, the recovery fund proposal is another important element contributing to market stability and stress reduction.

The ESM’s Pandemic Crisis Support (PCS) was made available in May 2020, just a few weeks after the pandemic outbreak and the ECB announcement on launching the PEPP. I would like to highlight the message this gave markets: together with the ECB’s commitment to keep market rates at favourable conditions, the ESM created a safety net for the euro area to ensure that additional financing can be made available at short notice.

I mentioned the ECB’s PEPP programme, and the next slide shows the refinancing levels of selected euro area members since January 2020.

At present, you see the 10-year rates around or partly even below the pre-pandemic levels which confirms that the ECB’s response continues to calm markets to this day.

Lastly, let me point to the discussions starting in April this year about whether and how these ECB measures could be - or have to be - reduced. From a market perspective, it is noteworthy that this discussion on halting the support measures did not result in additional market stress or higher financing costs.

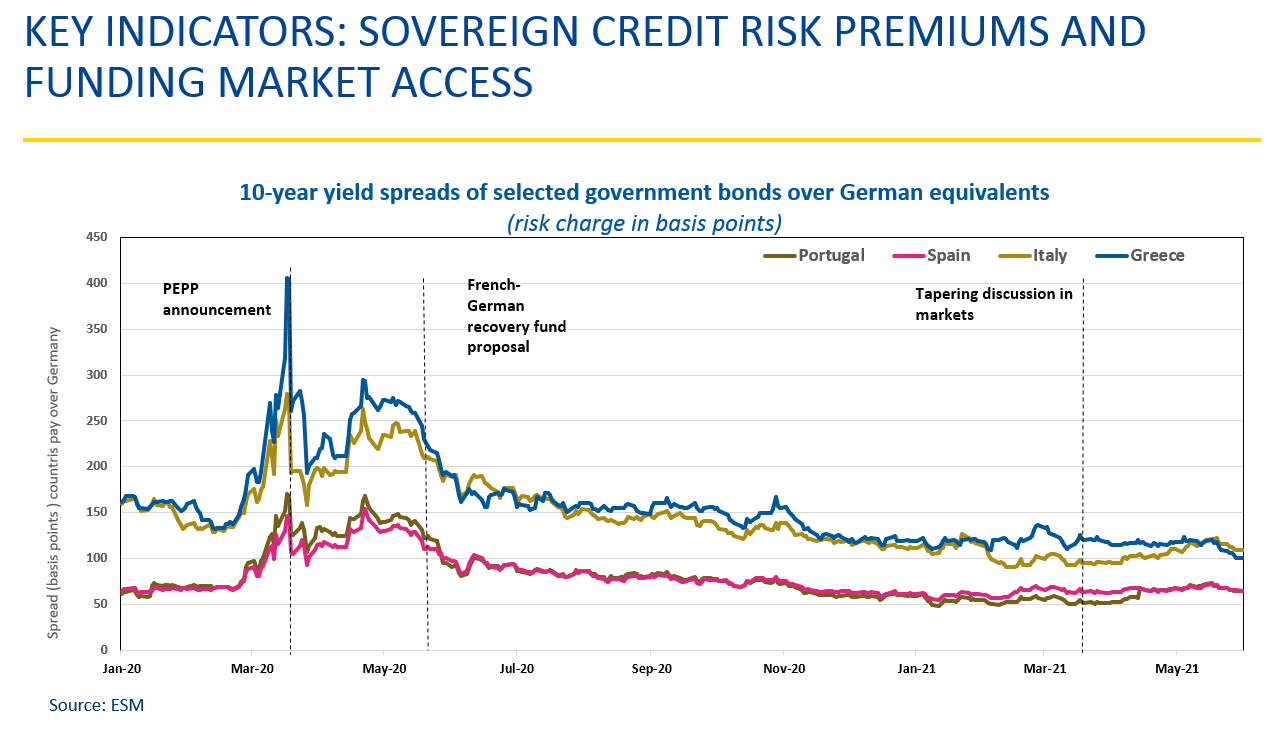

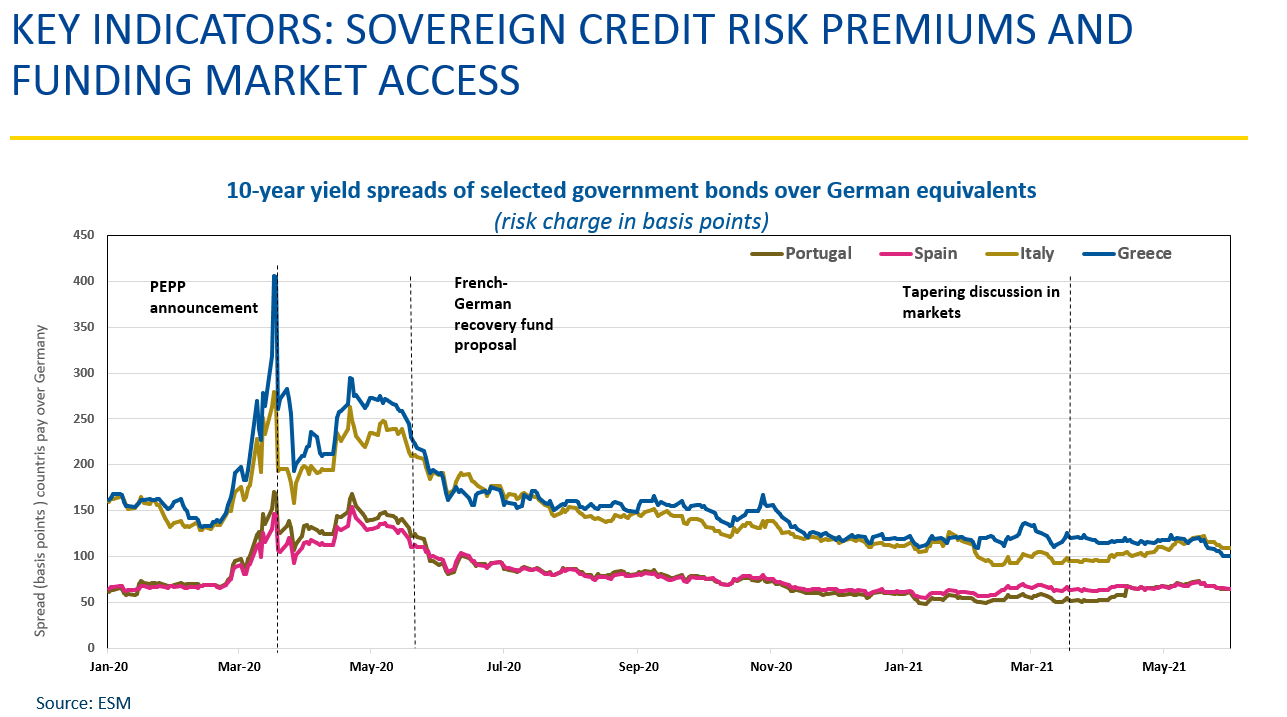

My next chart in slide 4 shows the premium countries have to pay in the market compared to highly rated issuers. It is common practice to use Germany as an AAA-rated euro area country for comparison.

What is different here to the previous chart is that we are not looking at an absolute level of financing costs (e.g. 2%), but at a relative measure which helps us to understand if markets see in increased risk for funding access in certain countries. The higher the premium, shown here as the rate difference in the colourful lines, the higher the risk.

So we see that the risk premium for Italy and Greece first increased significantly and then dropped after the PEPP announcement. They now stand at levels that are mostly lower than they were before the pandemic.

So what does all this mean?

-

First, market stress levels increased less and recovered faster in the pandemic than they did during previous crises.

-

Second, financing levels - in absolute and relative terms - recovered quickly. The decisive national and EU measures helped to maintain favourable financing conditions to mitigate the impact on the economy and on government finances.

-

Third, the support measures need to continue as long as the pandemic constrains the economy as we need to support the virtuous cycle to regain economic growth. The current, historically low interest rates mean that countries can sustainably carry more debt than they could in the past so the support measures can and should continue.

-

Lastly, we should remind ourselves that the current calm situation will not last forever. Market sentiment can be volatile and interest rates are expected to rise at some point. Despite the comfort of the current favourable financing conditions, countries need to look forward. They need to start mapping out a credible fiscal path to keep this market trust and to manage their debt levels in a sustainable way in the long-term.

Thank you.

Author

Contacts