How much of last year’s unexpected revenue boon is explained by inflation?

No one likes too much inflation. It causes instability by changing prices, and what you buy costs more than it used to. Central banks strive to curb inflation to avoid harmful effects on households and businesses.

Inflation also has an impact on public coffers, mainly because it affects taxes on consumption, income, and wealth. Last year’s record high inflation led to the fastest growth in tax revenue in the history of the euro area.

In this blog, we examine the implications of the “inflation tax” and how useful it was in lowering pressures on fiscal deficits.

Why it matters

Inflation boosts public revenue. How to spend it may become a delicate issue, especially when it is unexpected and driven by an energy crisis and a geopolitical conflict, as is currently the case by Russia’s war against Ukraine. There is more money in the public purse (almost) immediately, as collected revenues turn out to be higher than had been forecast. But governments have to assess how the improvement in the budget balance is best used in view of the macroeconomic environment. The additional revenues can be more lasting and saved, or they can be short-lived, depending on economic developments and policy choices.

Where does the extra revenue come from?

To disentangle the interplay between inflation and tax revenues, we use a simple framework to identify the sources of unexpectedly higher tax revenues emerging in 2022 and beyond. This angle is instrumental but insufficiently researched with regard to the impact of inflation on debt sustainability, which is at the core of the ESM’s mandate. Our analysis is complementary to the one conducted by the European Central Bank, and the European Commission in its assessment of Budgetary Plans.[1]

We look at the three largest taxes: taxes on consumption, on income, and contributions to social security, using the latest available government finance statistics for the first nine months of 2022. Altogether, these three categories yielded annualised revenues of around 40% of Gross Domestic Product (GDP) across our sample of countries.[2] This is about €220 billion or 2.6% of GDP higher than forecasted by the European Commission a year earlier.[3]

How does inflation influence tax revenue performance?

We attribute the positive surprise in tax collection to three factors: inflation, real growth, and an unexplained residual.[4] The first two factors, inflation, and real growth, determine the growth of nominal incomes, the main driver for tax collections.

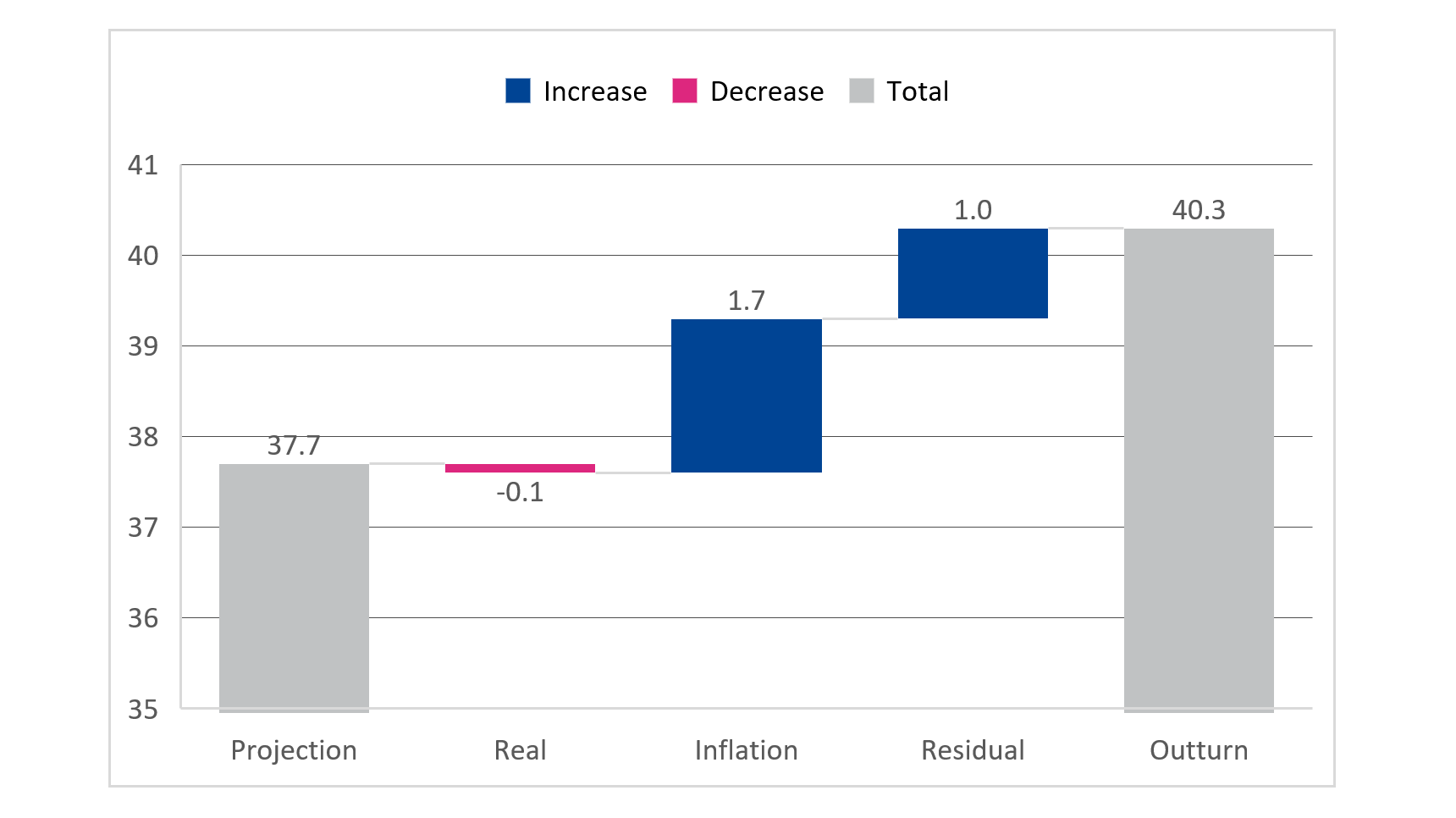

Our analysis suggests that changes in nominal income explained slightly more than 60% of the positive revenue surprise in the first nine months of 2022 (see Figure 1):

- The “macro surprise” – the combined effect of inflation and real growth – accounts for most of the total revenue surprise (1.6% of GDP, out of a total of 2.6% of GDP). Given the substantial increase in inflation during these quarters, the “macro surprise” is entirely related to inflation.

- The “unexplained residual” that captures all other factors that influence tax collections (such as fiscal drag, compliance, enforcement, and one-offs) is smaller (1.0% of GDP), but still economically significant:

- The so-called “fiscal drag” may have played a role, with the extra revenue generated from individuals and firms moving into higher tax brackets, as inflation pushes up their nominal incomes and profits.

- But also, pandemic-related tax deferrals and exemptions, which led to unusual patterns of declines and subsequent increases (i.e., growth base effects) in 2022.

- Other possible explanations include unexpected changes in the composition of expenditures and one-off windfall taxes on businesses.

- Finally, improvements in tax collection, which can emerge from higher digitalisation of economic activity, and a shrinking size of the informal economy can also yield tax revenue over and above the increase in nominal incomes.

- Empirically, the “unexplained residual” is positively related to the share of indirect taxes across countries. This points to the special role of energy spending. It is hard to change our energy consumption habits suddenly and significantly, even as the price (and tax) goes up suddenly – and this can lead to unexpectedly strong gains in tax revenue. The volatility of energy prices makes this additional driver of revenues rather uncertain and short-lived. The ability of firms and households to save energy should reduce the impact over time.

Figure 1: Euro Area Aggregate Outturns: decomposition of tax revenue developments in Q1-Q3 2022

(% of GDP)

Eurostat, AMECO, own calculations.

Note: To identify these components, we proceed in three steps: We construct a passive “macro-only” forecast. As input, we use actually observed growth rates of macroeconomic tax bases (personal consumption expenditure, gross operating surplus, and compensation of employees) in the first nine months of this year and the “implicit” tax/base elasticities drawn from the European Commission 2022 Spring Forecast. This “macro-only” forecast tells us how high tax revenue would have been if the Commissions Spring Forecast had perfectly predicted actual macroeconomic developments in the first half of the year. We then decompose the surprise in tax revenue identified by the “macro-only” forecast into “growth-only” and “inflation-only” components. Finally, the difference between the “macro-only” forecast and actual outturn is the unexplained residual. This residual captures all the factors influencing tax collections, in addition to the macroeconomic environment.

For the whole of 2022, we relied on projections produced as part of the 2023 Draft Budgetary Plans.[5] These continue to show an increase in revenue (1.4% of GDP), but smaller than the increase in the first nine months of the year.[6]

We found that 1 percentage point of the upward revision in tax projections was due to changes in the macroeconomic outlook, but only 0.4% related to the “unexplained residual”.

Looking ahead

For 2023, the revenue gains linked to nominal incomes (i.e., inflation and real growth) are still expected to continue. After all, nominal GDP – which is a critical driver of tax collections – is permanently higher. However, the baseline tax projections do not indicate an economically important role for revenue gains caused by other “unexplained residual” factors. The Draft Budgetary Plans for 2023 published by euro area member states appear more cautious as their projections are consistent with a more mechanistic forecast based on standard tax elasticities and announced measures. Revenue projections appear more reliable and easier to achieve in an uncertain environment when they include a smaller contribution of the unexplained part of the revenue increase.

The bottom line

Inflation can help those countries that want to reduce debt, not only by lowering debt-to-GDP ratios, but also by mobilising additional tax revenue, as last year’s evidence shows — we confirm the economic significance of this channel in this blog. How lasting this effect will be depends on the persistence of the increase in the price level. Further work is necessary to assess the importance of additional factors that could influence future tax revenue, such as the impact on revenue composition, tax structures and consumption habits.

It is yet to be seen to what extent the revenue boon translates into unexpectedly higher budgetary balances, which ultimately matter for debt sustainability. Governments face the difficult task of choosing between the desire to save the unexpected revenues and rebuild fiscal buffers after the pandemic, and the need to protect households and firms from hardships, such as the unprecedented surge in energy and food prices last year.

Acknowledgements

The blog post has benefitted from analytical input by Edmund Moshammer. Authors would like to thank Rolf Strauch, Giovanni Callegari, Robert Blotevogel, Anabela Reis, Raquel Calero, and George Matlock for their valuable contributions to this blog.

Further reading

European Commission (2021), Autumn Forecast.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager