Ireland

Situation as of June 2025 (2024 ESM Annual Report)

Highlights

Programme overview

PROGRAMME TIMELINE FOR IRELAND

2007

Property bubble bursts

Irish government provides blanket guarantee for domestic banks

EFSF disburses first loan tranche

Ireland returns to bond market with 5-year issue

Ireland achieves highest GDP growth in EU

2008

2009

2010

2011

2012

2013

2014

ESM programme outcomes

Economic adjustment and reforms

Ireland’s economic growth in the years 2002-2007 was largely driven by a property bubble, financed through aggressive lending by Irish banks. When the property market crashed in 2007, the decline in prices and the collapse in construction activity resulted in severe losses for the Irish banking system. The government of Ireland responded by injecting public funds into banks to restore their solvency (over €60 billion). This led to a significant increase in Ireland’s public debt, while the sharp decline in economic activity caused GDP to fall and unemployment to rise. Rising yields on its sovereign bonds threatened Ireland’s ability to finance its government debt. Ireland requested financial assistance from institutional lenders and three European countries in November 2010.

The financial assistance package was tied to an economic adjustment programme, which included:

- A financial sector strategy comprising fundamental downsizing and reorganisation of the banking sector (including recapitalisation and deleveraging);

- A strategy to restore fiscal sustainability (reducing government expenditure, tax system reform, generation of additional revenues);

- A structural reform package to strengthen economic growth, focusing on competitiveness and job creation.

Thanks to the implementation of the reforms and measures, Ireland regained market access and achieved a remarkable economic recovery. Ireland’s GDP growth was among the highest of all EU countries in 2014-2019. The country also significantly reduced its fiscal deficit and debt-to-GDP level, a trend that continued until the pandemic crisis affected the European and global economy in 2020.

After the programme

Following the completion of Ireland’s programme in 2013, post-programme surveillance (PPS) has been carried out by the European Commission in liaison with the European Central Bank. The procedure involves regular review missions in the programme country to assess its economic, fiscal and financial situation. The ESM participates in PPS missions to fulfil the requirements of its Early Warning System, i.e. to assess a country’s capacity to repay its outstanding loans.

Ireland completed the early repayment of its IMF loans in December 2017 and made full early repayments of bilateral loans from Sweden (€0.6 billion) and Denmark (€0.4 billion) in December 2017. In addition, Ireland completed the repayment of its loan to the UK (€3.8 billion in total) in March 2021.

ESM country team coordinator for Ireland: Nicoletta Mascher

Details of EFSF financial assistance for Ireland

| Disbursement date | Amount disbursed | Cumulative disbursed amount | Initial final maturity | Revised final maturity |

|---|---|---|---|---|

| 01/02/2011 | €1.9 billion | €1.9 billion | 18/07/2016 | 01/08/2032 |

| 01/02/2011 | €1.7 billion | €3.6 billion | 18/07/2016 | 01/02/2033 |

| 10/11/2011 | €0.9 billion | €4.5 billion | 04/02/2022 | 01/08/2030 |

| 10/11/2011 | €2.1 billion | €6.6 billion | 04/02/2022 | 25/07/2031 |

| 15/12/2011 | €1.0 billion | €7.6 billion | 23/08/2019 | 01/08/2030 |

| 12/01/2012 | €1.2 billion | €8.8 billion | 04/02/2015 | 01/08/2029 |

| 19/01/2012 | €0.5 billion | €9.3 billion | 19/07/2041 | 01/07/2034 |

| 03/04/2012 | €2.7 billion | €12.0 billion | 03/04/2037 | 01/08/2031 |

| 02/05/2013 | €0.8 billion | €12.8 billion | 02/05/2029 | 01/08/2029 |

| 18/06/2013 | €1.6 billion | €14.4 billion | n.a | 15/11/2042 |

| 27/09/2013 | €1 billion | €15.4 billion | n.a | 27/09/2034 |

| 04/12/2013 | €2.3 billion | €17.7 billion | n.a | 04/12/2033 |

Weighted average maturity: 20.8 years

Explainer

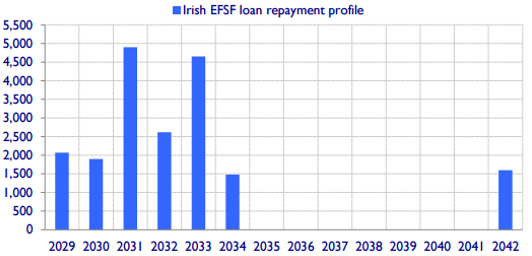

Ireland will repay the principal of the loan tranches starting from 2029, and the repayment is scheduled to end in 2042.

Ireland has achieved a remarkable economic recovery since the conclusion of its financial assistance programme in December 2013. Ireland’s GDP growth was the highest among all EU countries in 2014 (8.5%), 2015 (26.3%) and 2016 (5.2%). In addition, Ireland’s unemployment rate of 7.9% in 2016 was well below the euro area average (10%).

Ireland returned to the bond market in July 2012, when it issued a 5-year bond at 5.9%. Just one year earlier, the yield on 5-year Irish bonds was above 13%, which shows how quickly Ireland managed to put its economy back on track and regain the confidence of investors. The country had been forced out of international bond markets in September 2010.

The majority of the EFSF programme amount was used for budget financing needs and a smaller portion was assigned for the recapitalisation of banks.

- A financial sector strategy comprising fundamental downsizing and reorganisation of the banking sector (including recapitalisation and deleveraging);

- A strategy to restore fiscal sustainability (reducing expenditure, tax system reform, generation of additional revenue);

- A structural reform package to underpin growth, focusing on competitiveness and job creation.

The programme for Ireland was financed as follows:

- €67.5 billion in external support including

- €17.7 billion from EFSF (this was the EFSF’s first financial assistance programme);

- €22.5 billion from EFSM (European Financial Stabilisation Mechanism – an EU facility funded through bonds issued by the European Commission);

- €22.5 billion from IMF;

- €4.8 billion in bilateral loans from the UK (€3.8 billion), Sweden (€0.6 billion) and Denmark (€0.4 billion);

- €17.5 billion domestic contribution (from the Irish Treasury and the National Pension Fund Reserve)

The Irish economy suffered as a consequence of a boom-bust cycle in the housing market. House prices increased four-fold from 1997 to 2007, when the bubble burst. As the property boom was financed through aggressive lending by Irish banks, the decline in property prices and the collapse in construction activity resulted in severe losses in the Irish banking system. The government of Ireland responded by injecting public funds into banks to restore their solvency (over €60 billion). This led to a huge increase in Ireland’s public debt, while the sharp decline in economic activity caused GDP to fall and unemployment to rise. The Irish government was not able to resolve the situation on its own, and therefore requested financial assistance from the euro area countries, the EU and the IMF.