Rolf Strauch's speech at the SEV General Assembly

Rolf Strauch, ESM Chief Economist

SEV General Assembly, Athens

31 May 2017

Ladies and gentlemen,

It is a real pleasure for me to be addressing you, here at the General Assembly of the SEV, the Hellenic Federation of Enterprises. Let me first congratulate you with your 110th anniversary. Europe is also celebrating a number of decisive historic events this year - though your organisation has been around almost twice as long as the process of European unification.

The Treaty of Rome was signed 60 years ago, which created the common market, while the Maastricht Treaty – which was signed 25 years ago - was the basis for the economic and monetary union. The signing of these two documents were landmark moments in Europe’s history. They reflect political unity and form the basis of economic integration and the many benefits that it brings.

Today’s event offers an opportunity to reflect on European integration, on what it means for Greece and on the role of Greece in an integrated Europe. The SEV forcefully argues that Greece should turn the page and leave the crisis behind. It should move on towards economic normality outside a programme. I wholeheartedly agree. It will not be an easy process at all, but everybody wants to get Greece back on a healthy growth track, which would benefit every Greek citizen. Let me explain how the ESM helps in providing the most significant form of financial solidarity available in Europe.

The EU is an unprecedented example of international cooperation. It has also been extremely successful. Its members have not seen war for more than 70 years now, a period of peace longer than any other in its recent history. When the Berlin Wall fell, the EU offered countries emerging from communist rule an immediate and obvious alliance that has served them extremely well. The EU has established a firm basis of human rights and protecting its citizens. In 2012, the EU was awarded the Nobel Peace prize for helping to promote international cooperation and peace.

Beyond these impressive political achievements, the EU has sought and succeeded in being an open economy from the start. It is the largest trading block of the world. The four freedoms of movement – of goods, services, capital and labour – have been a source of growth and employment. Outside this block, individual countries would lose significance and lack bargaining power, particularly with the rise of new superpowers such as China and India. Europe represented 32% of the global economy in 1970, but that share now stands only at 23%. By 2050, it is projected to be just 9%. Even large countries like Germany or France will appear tiny on a global scale by then.

Launching a common currency was a natural step for a number of countries once the single market had existed for some time. As entrepreneurs you feel the benefits of a stable currency and lack of exchange rate risks every day. Across Europe, companies are saving foreign exchange costs of €20 to 25 billion per year. Cross-border trade between euro area countries also benefited. Price transparency improved, leading to greater competition, which, as we know from economic theory, results in larger productivity gains, and higher growth. Or to put it in plain English, it leads to better and cheaper products, and creates higher living standards for people.

At the same time, by no means has the euro area worked seamlessly. The crisis brought to light a number of design flaws in the institutional and policy framework underlying the single currency. When the Maastricht Treaty was signed, it had been deemed impossible that a country inside the monetary union could lose market access. But this is precisely what happened in Greece and other countries. To keep the euro together, Europe needed to rapidly set up a lender of last resort for sovereigns. As you know, this first led to the establishment of the European Financial Stability Facility, a temporary solution. The ESM was then set up in 2012.

There are other important lessons that Europe drew from the crisis. Firstly, countries did their homework, something you have witnessed closely here in Greece. They put their fiscal house in order, and adjusted macroeconomic policies. Budget gaps have now tightened to more sustainable levels across the euro zone, and are well below the US in the aggregate. Equally important, competitiveness has returned in programme countries, while current account deficits emerging in the run-up to the crisis have largely disappeared. Programme countries implemented more structural reforms to address their economic and financial weaknesses than any other country in the world, according to the OECD and the World Bank.

On top of these national efforts, there is stronger and broader policy coordination at the European level. In this respect, the new Macroeconomic Imbalances Procedure is an important new tool. Another significant institutional innovation needed to fight the crisis is Banking Union, which saw the establishment of the Single Supervisory Mechanism and the Single Resolution Mechanism. This constitutes an important transfer of regulatory powers to the supranational levels.

With these changes, the monetary union is on a more stable footing than before the crisis, and the euro area economy is more resilient. And it is performing well. The crisis has strengthened Europe, not weakened it. Many of you have lived through this crisis in this country, which was by far the hardest hit. So let me spend the remainder of my time on how to drive progress in Greece.

The current debate about Greece focuses on debt relief, and this is something that I think should change. This is for two reasons. Firstly, because Greece has received very substantial debt relief already in the past. It is still getting it in the present and may well continue to do so in the future. I will come to talk about this in a minute.

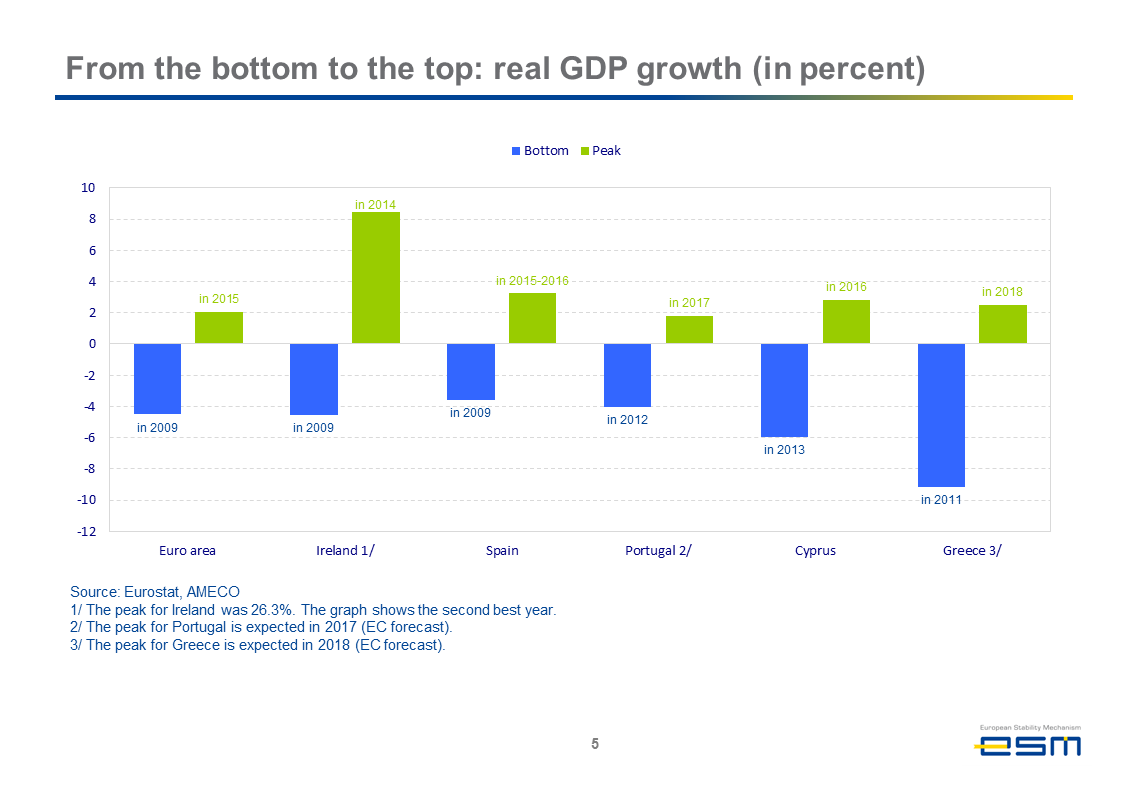

But more importantly, the benefits of economic reform to the Greek economy, and programme ownership are now a higher priority than debt relief. Former programme countries such as Spain and Ireland are at the top of the growth league in Europe. Portugal and Cyprus are also doing well. The common denominator in these success stories is policy reform. That’s what brought them from the bottom to the top. And this should also be the prospect for Greece. Let me illustrate that with a story about football.

You will remember the big surprise when Greece won the Euro 2004 football championship. One of the winning team’s members, Takis Fyssas, said the following: "We did not have a Zidane, or Simao, or Cristiano Ronaldo. We only had hard work, sacrifice, determination and that family spirit.” So it wasn’t magic or pure luck that led to the top, but hard work and team-spirit. What happened then is not impossible for Greece now. Several projections show that growth rates are expected to be above the euro area average next year, in line with other countries that received ESM assistance. I commend your government – after a difficult initial year – to have taken decisive steps contributing to this recovery.

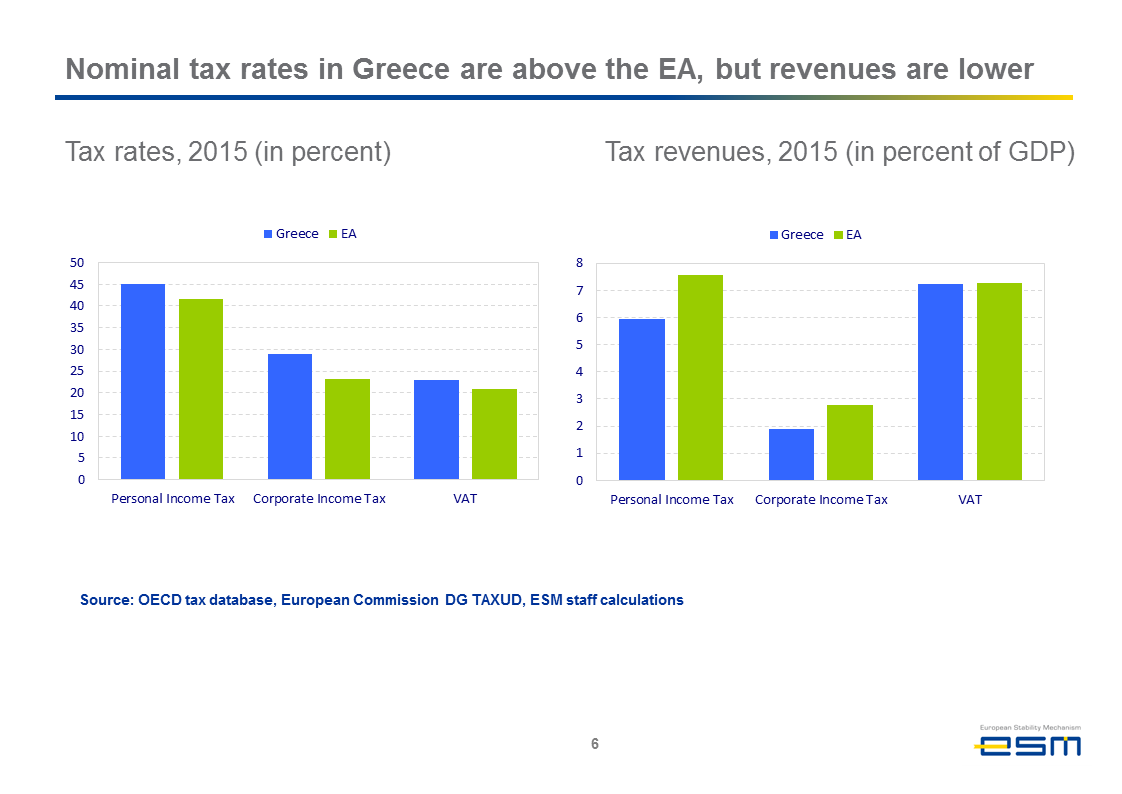

Let me talk a bit about the strategy that would allow the Greek team to win that match as well. Taxation is an important factor to strengthen competiveness and reinvigorate investment. Here there is room for improvement. Nominal tax rates in Greece are above the euro area average, but tax returns are not. This is because the tax collection effort shows still gaps and there are huge tax arrears in the private sector. So it is welcome that Greece is strengthening its tax administration, which will help lower the nominal rate and more evenly share the tax burden. This is an area where programme ownership is particularly important. Greece cannot make it to the top if the tax system punishes the honest tax payer. I am sure that from your everyday practice, you will agree.

Another issue are non-wage labour costs, which remain high by European standards. With the new tax and pension reforms that have been agreed, this should change further. At the same time, the compensatory benefit measures agreed and the roll-out of the general minimum income scheme should lead to a more equitable social benefit system.

Other costs for companies remain high because of remaining regulation and inefficiencies in the energy sector and high energy prices, because of contract enforcement costs and still too much red tape. The programme aims to lower these costs, reduce regulation and support privatisation through the creation of the privatisation fund, the Hellenic Corporation of Assets and Participations, or HCAP. Again, this is an area where I would welcome strong implementation to ensure a sustainable recovery in the country.

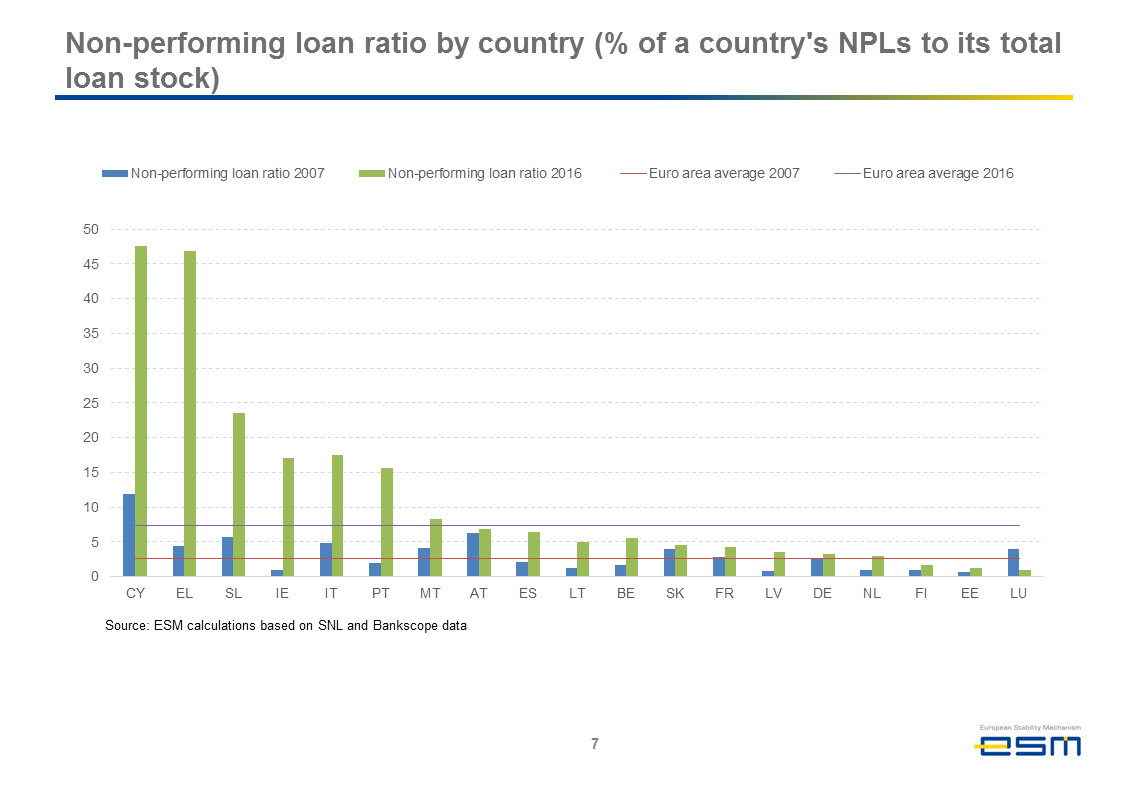

Finally let me say a few words on the Greek banking sector. Like I said before, the euro area banking sector is much safer as a whole because of the establishment of Banking Union. Differences in financing costs across the euro area have diminished as a result, and the Greek banking sector is also improving after last year’s recapitalisations. However, it remains fragile. Lending activity remains subdued and needs to improve. Financing conditions are normalising, but there is still a high reliance on the ECB’s Emergency Liquidity Assistance (ELA) which is expensive. A third important priority is to address non-performing loans. This will allow banks to start providing credit again so that businesses can get the cash they need to invest in future growth.

The measures agreed between the Greek government and the European institutions and the IMF recently during the second programme review address all these areas. Strong programme ownership along these priorities is what Greece can do to put the country on a stronger footing.

From our side we will continue to look at the debt burden, because sustainable financing conditions are needed for Greece to regain investor confidence. But hopefully I can give you a different perspective on the issue than what you normally read in the papers.

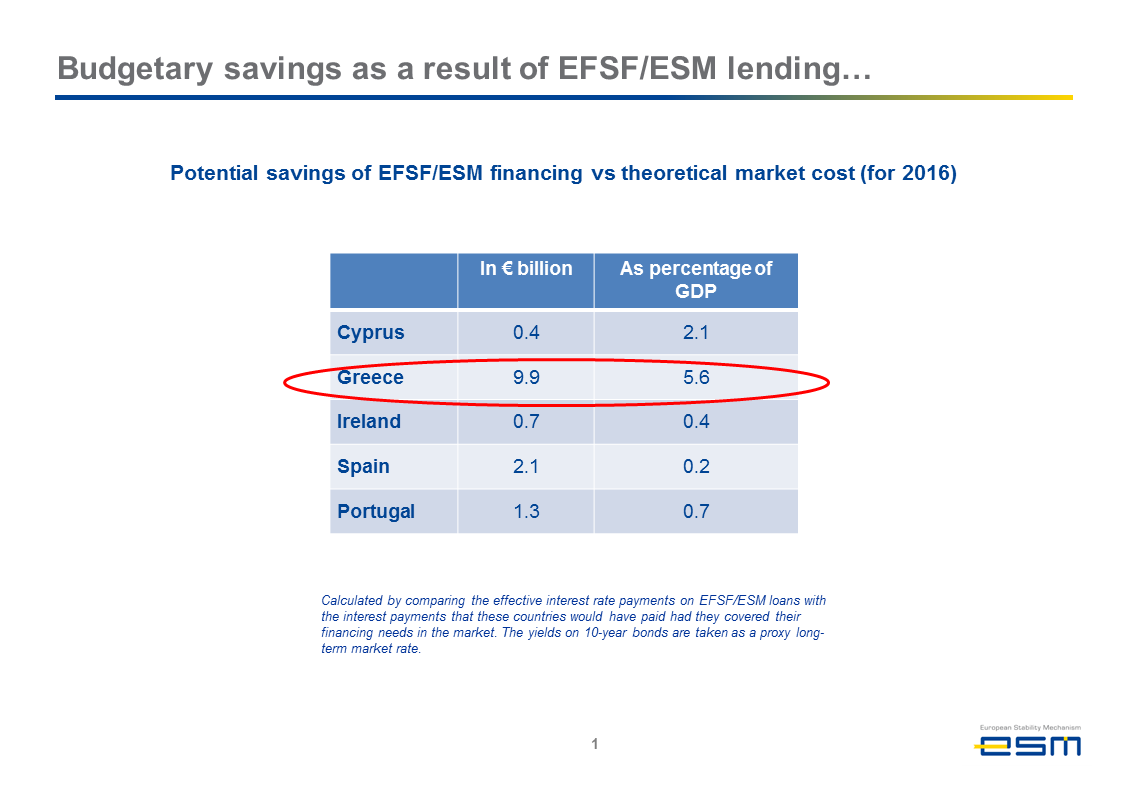

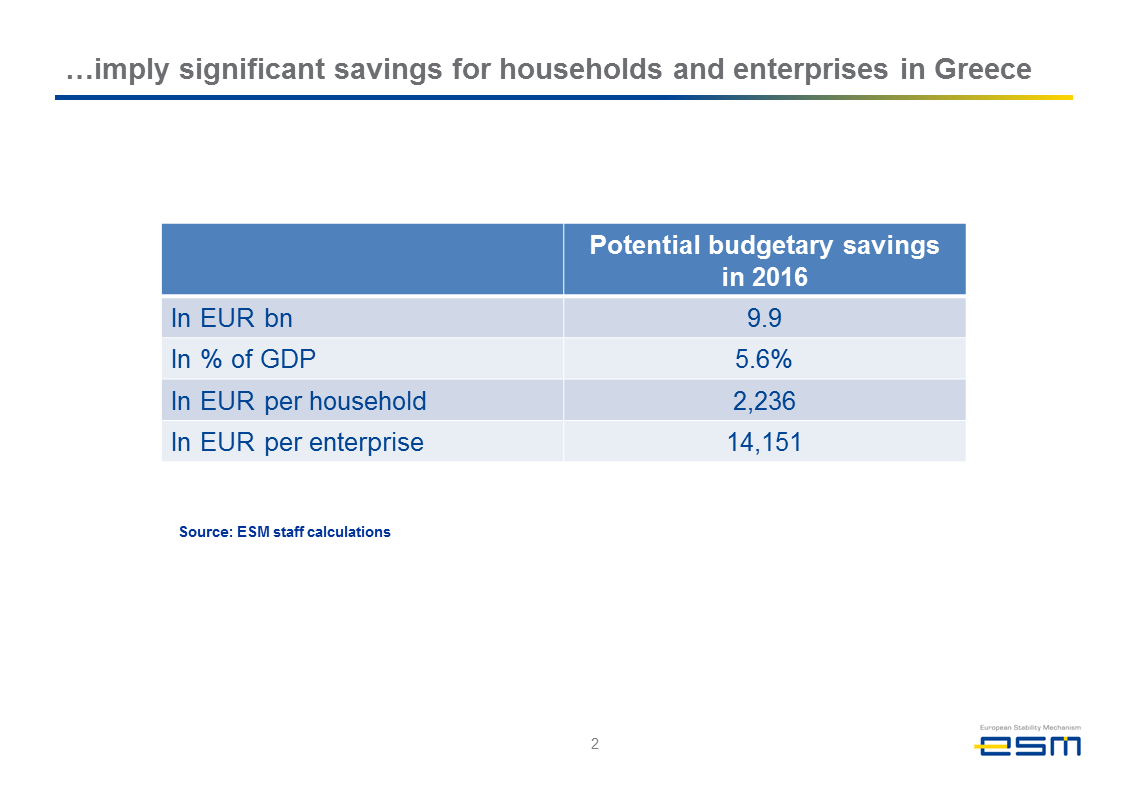

Greece was the beneficiary of the world’s biggest-ever debt-restructuring deal in 2012. At that time, private sector creditors took a 53% haircut on virtually all of their debt holdings, which amounted to €107 billion. This was a very difficult decision at the time, but eventually helped Greece. This was matched by measures reducing the net present value (NPV) of public sector debt by 40 percent of the Greek economy. Greece also hugely benefits from the favourable lending conditions of the ESM and EFSF. This is saving the Greek budget €10 billion each year, or close to 6 percent of its GDP, compared to a rate it would have paid in markets. This amounts to more than €2,200 per household and €14,100 per company. These savings are based on the ESM’s strong credit rating, backed by the capital of its shareholders, the countries of the euro area. We pass these favourable financing conditions on to Greece, and these savings therefore are a strong sign of European solidarity.

On top of these significant efforts, the Eurogroup last year pledged a further easing of lending conditions if needed, and if certain conditions are met. There are three sets of measures: those that will be implemented in the short-term, in the medium-term and possibly also in the long term. Staff at the ESM is implementing the first set of measures right now, and they are estimated to reduce Greece’s gross financing needs by 5 percentage points and the debt stock by around 20 percentage points by 2060.

The set of medium-term measures has also been agreed. They will become available if it turns out that Greece’s debt is still not sustainable at the end of the current programme in August 2018 and the programme is fully implemented. Finally, the long-term measures are there as a safeguard to ensure debt sustainability at a later stage if medium-term measures eventually turn out not to be sufficient and Greece follows the European fiscal framework. In summary, Europe has made abundantly clear that it will stand by Greece: today, tomorrow, and in the future. Europe and Greece are long-term partners, there can be no doubt about that.

As to the current state of the negotiations, let me say only the following. As you know, Greece needs the next ESM disbursement to cover the debt payments in July without creating new shortages in other areas. There can be no disbursement without Greece’s compliance with the Prior Actions list, which includes some of the points I just addressed. The ESM stands ready to prepare the disbursement once all the conditions are met, including the involvement of national parliaments and final decisions by our governing bodies. It is not too late to unlock the disbursement in June. But Greece needs to act swiftly.

Ladies and gentlemen, I thank you for your attention. Europe has grown closer together – economically and politically over the past decades. And despite the crisis, it remains a simple truth: the euro is good for Europe and its citizens. Europe has worked very hard in the past seven years to assist Greece in getting its house in order. Part of these efforts was substantial and ongoing debt relief. Greece in turn has come a long way since the onset of the crisis: because of this help, but primarily because of its policy reforms since 2010.

For Greece to make it to the top it is of the utmost importance that authorities really commit to continue their journey towards a modern economy and a sustainable recovery. It is only then that the Greek economy can realise its full potential - driven by businesses like yours and to the benefit of all its citizens.

Photo: SEV

Author

Contacts