A stronger banking union for a stronger recovery

European banks are safer since the global financial crisis and the sovereign debt crisis. With the outbreak of the pandemic, a number of measures were put in place to make sure liquidity reaches the real economy. Nicoletta Mascher and Rolf Strauch argue that banks need a stronger and completed banking union in order to emerge stronger from this crisis.

The euro area banking sector is faced with the current pandemic while emerging from a long healing process after the global financial crisis and the sovereign debt crisis. This process has made European banks safer. With the outbreak of the virus, countries and EU institutions put a number of measures in place to ensure that banks can continue to provide loans and support the economy. Nevertheless, banks’ share prices plummeted right after the outbreak of the pandemic and have remained low. In fact, share prices reacted initially in pretty much the same way as in the past financial crisis (Figure 1) even though safer banks, after all, should be more likely to deliver adequate returns in the longer term. What do share prices tell us about the state of the banking sector and why are they so low? In this blog post, we explain why investors seem to have lost trust in European banks’ profitability despite banks being much safer than in the last crisis.

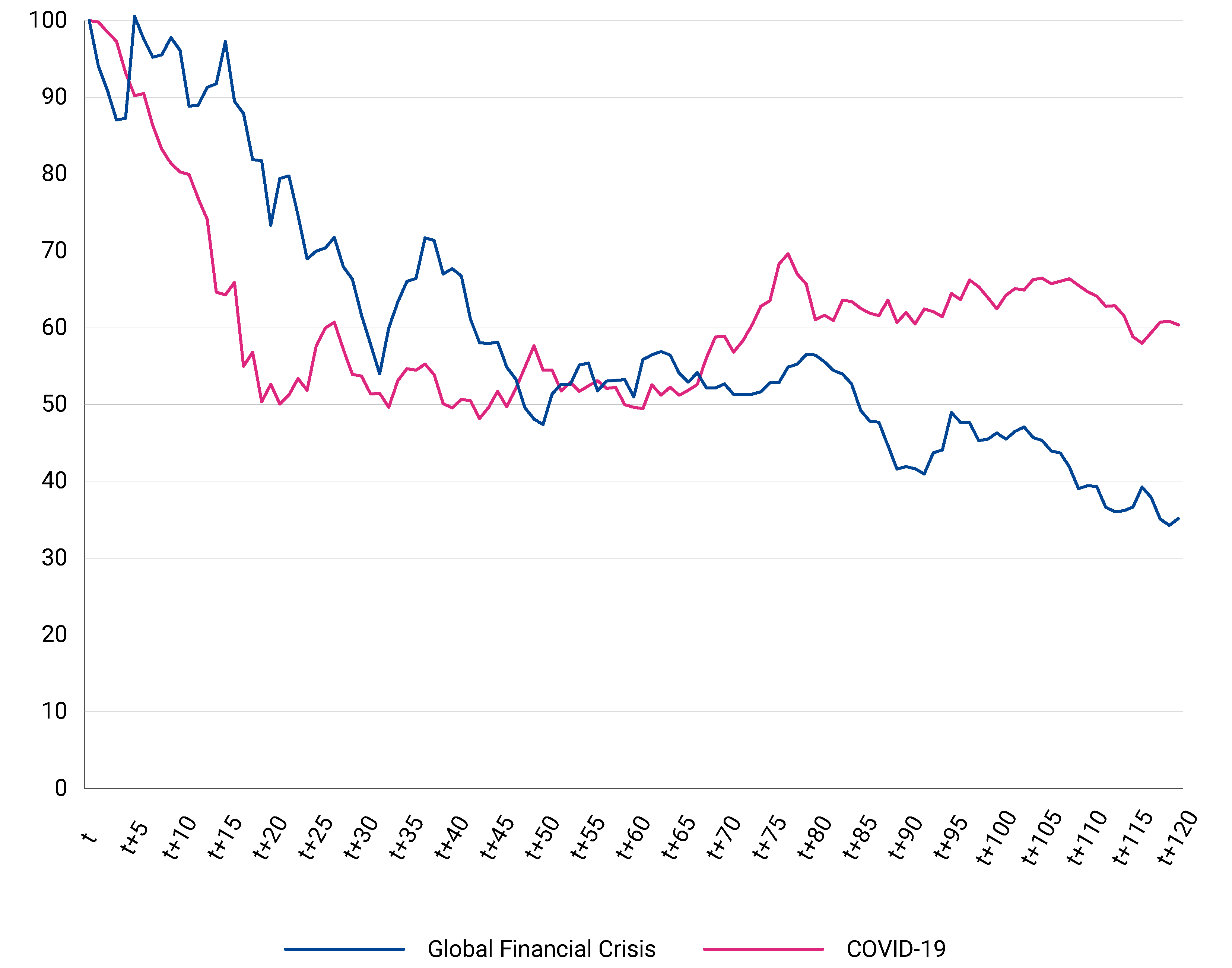

Figure 1: Share prices reacted initially during Covid-19 in a similar way as in the global financial crisis

Source: Bloomberg. The graph depicts the changes of the daily quotes of EURO STOXX Banks (SX7E index) since the Lehman bankruptcy and the Covid-19 outbreak. The index tracks stock price movements of the largest 22 listed banks in the euro area. “t” refers to the date before the collapse of Lehman Brothers, and to the date before Covid-19 broke out.

Taking into account that the low valuation of banks indicates remaining vulnerabilities and weaknesses, we argue that these deficiencies should be addressed. Further effort is needed both from the industry itself and from policymakers, as well as domestic and supranational institutions. This is crucial, as the banking system is a vital component in the recovery phase after the pandemic; fostering a sound and profitable banking industry is a strategic necessity to support growth and ensure long-term stability at the same time. The completion of banking union should be considered a strategic priority.

Banks were at the heart of the past crisis. The global financial crisis did not only start with the collapse of a large bank, it also exposed flaws in the banking industry. Financial market engineering, lacking transparency and exposing banks to unclear risks, financing housing bubbles with insufficient capital backing, unbalanced funding structures, weak risk measurements, inadequate controls and distorted governance incentives – all these factors were part of the problem. As banks made high returns, they found investors willing to provide financing. This was based on the assumption that banks would be bailed out by taxpayers.

The approach to bank rescue has drastically changed since and is paying off now. Banks had to acquire substantive amounts of additional capital and liquidity as well as to step up their risk governance, while regulation and supervision tightened on almost all business aspects. Moving supervision and resolution to the European level ensures a level playing field and addresses the cross-border effects of bank failures. Thanks to the new regulatory framework and the ramping up of capital and other loss absorbing instruments, investors have to contribute to bank resolution and restructuring, and costs will be shared to a lesser extent than in the past in the event of a bank failure.

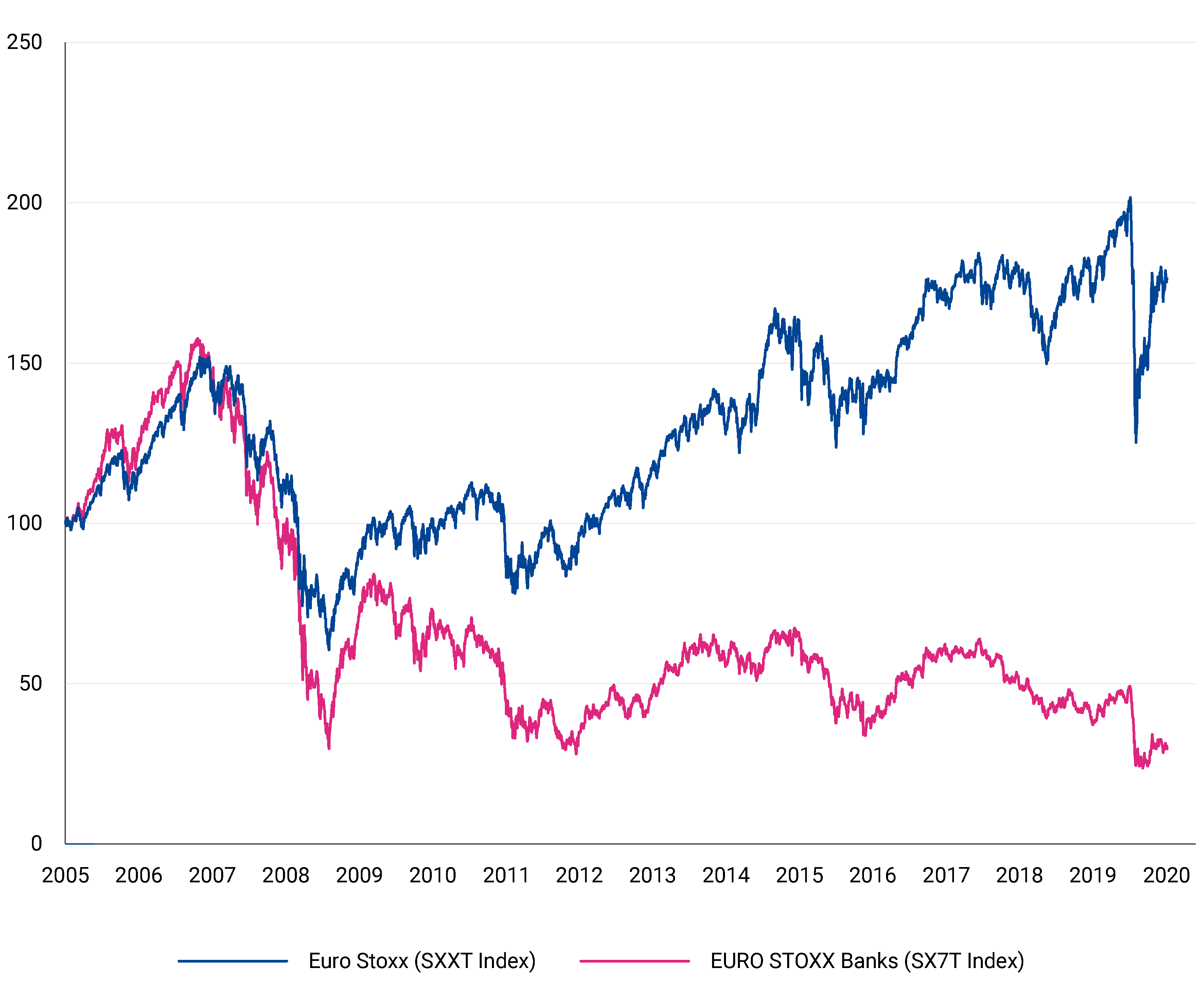

However, the overall performance of bank shares has been disappointing for long (Figure 2), which is a cause for concern. Clearly, improved safety is not rewarded through higher share prices if it comes with higher costs and dilutes net returns persistently. But higher safety would allow share prices to rise if banks were able to increase their profitability, net of risk, in the longer term.

Figure 2: Overall performance of banks’ shares has been disappointing for long – Index performance between August 2005 and August 2020

Source: Bloomberg. Note: The indices show net returns. The EURO STOXX Index (SXXT) is a euro area subset of the STOXX Europe 600 Index. With a variable number of components, the index represents large, mid and small capitalisation companies of 11 euro area countries. The SX7T is the net returns version of the SX7E index.

While in 2007, euro area banks earned 12% of their equity, their return on equity (RoE) – a measure that indicates financial performance – stood at 5.5% in 2019. This follows a steep and arduous recovery path from a record bottom at 1.3% in 2013, when profits were almost entirely wiped out by loan losses.

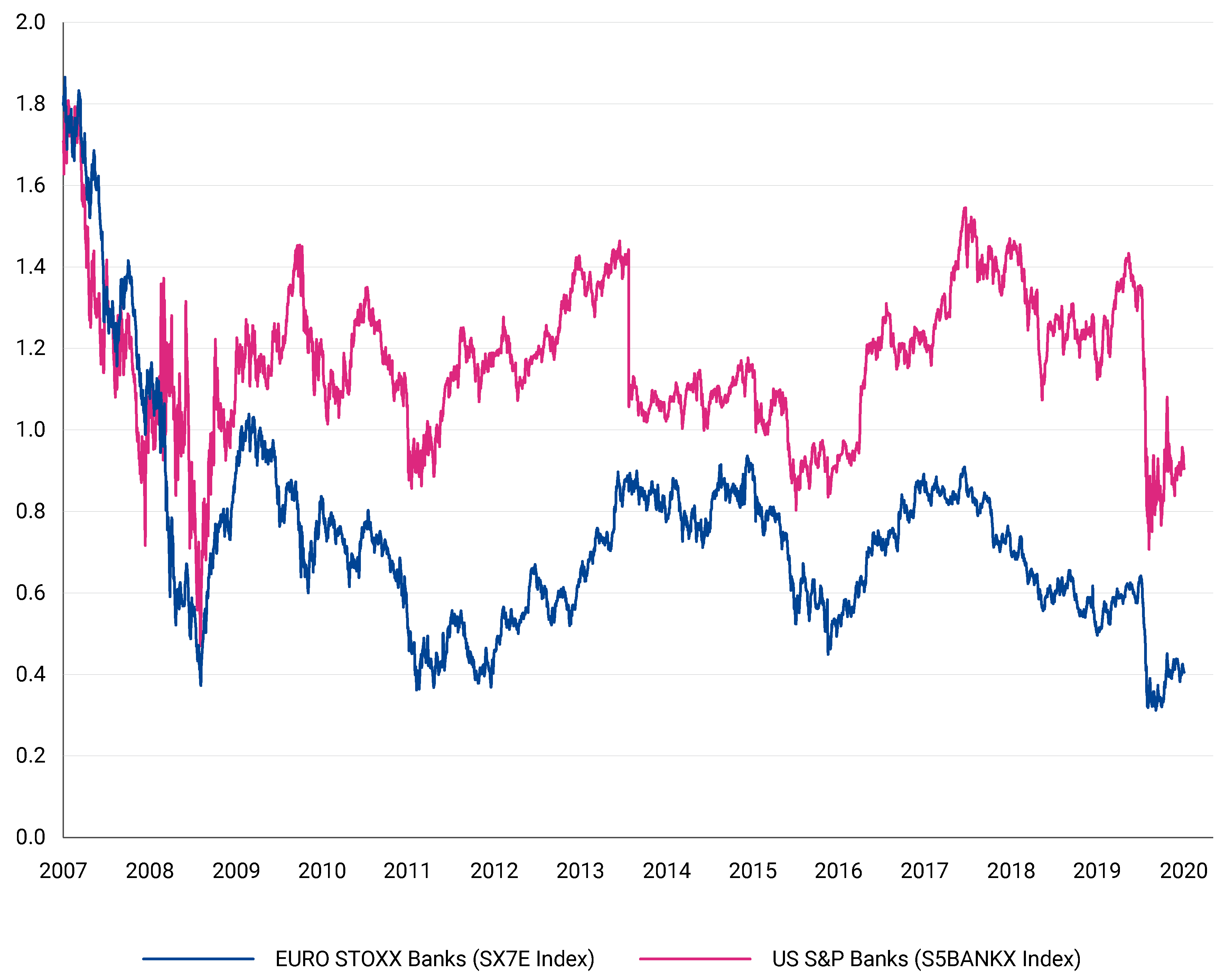

Looking at the price-to-book ratio, which compares the market value of a bank’s shares[1] to its book value[2], it is even more evident that euro area banks will continue to yield little value according to market expectations (Figure 3). In fact, the cost of equity - the return that investors require on average for taking an equity stake in banks – is between 8% and 10%. While the returns generated by euro area banks in the largest countries ranged between 0.5% and 9% end 2019 – only a minority of these banks exceeded the 8% lower bound. Banks that are not sufficiently profitable are not able to attract investors or generate enough capital by themselves to expand their business.

Figure 3: Euro area banks will continue to yield little value according to market expectations – Price to book ratio between August 2007 and August 2020

Source: Bloomberg. US S&P Banks refers to the Standard and Poor's 500 Banks Index (S5BANK), which tracks the performance of US banks stocks (according to the Global Industry Classification Standard, level 2 industry group).

With the outbreak of Covid-19, market expectation of banks’ returns have been further lowered due to:

- Greater margin compression amid a prolonged negative interest rate environment; uncertain loan growth prospects given the business standstill and expected secular changes in spending behaviour;

- Increase in loan losses as a consequence of the pandemic scarring effect, and uncertain trading revenues, hampered by increasing volatility despite massive central bank interventions;

- A largely incomplete transformation of banks’ business models, whereby fragilities affect the whole sector horizontally and many banks lag behind the technological innovation curve, while banking union has not yet delivered the expected results.

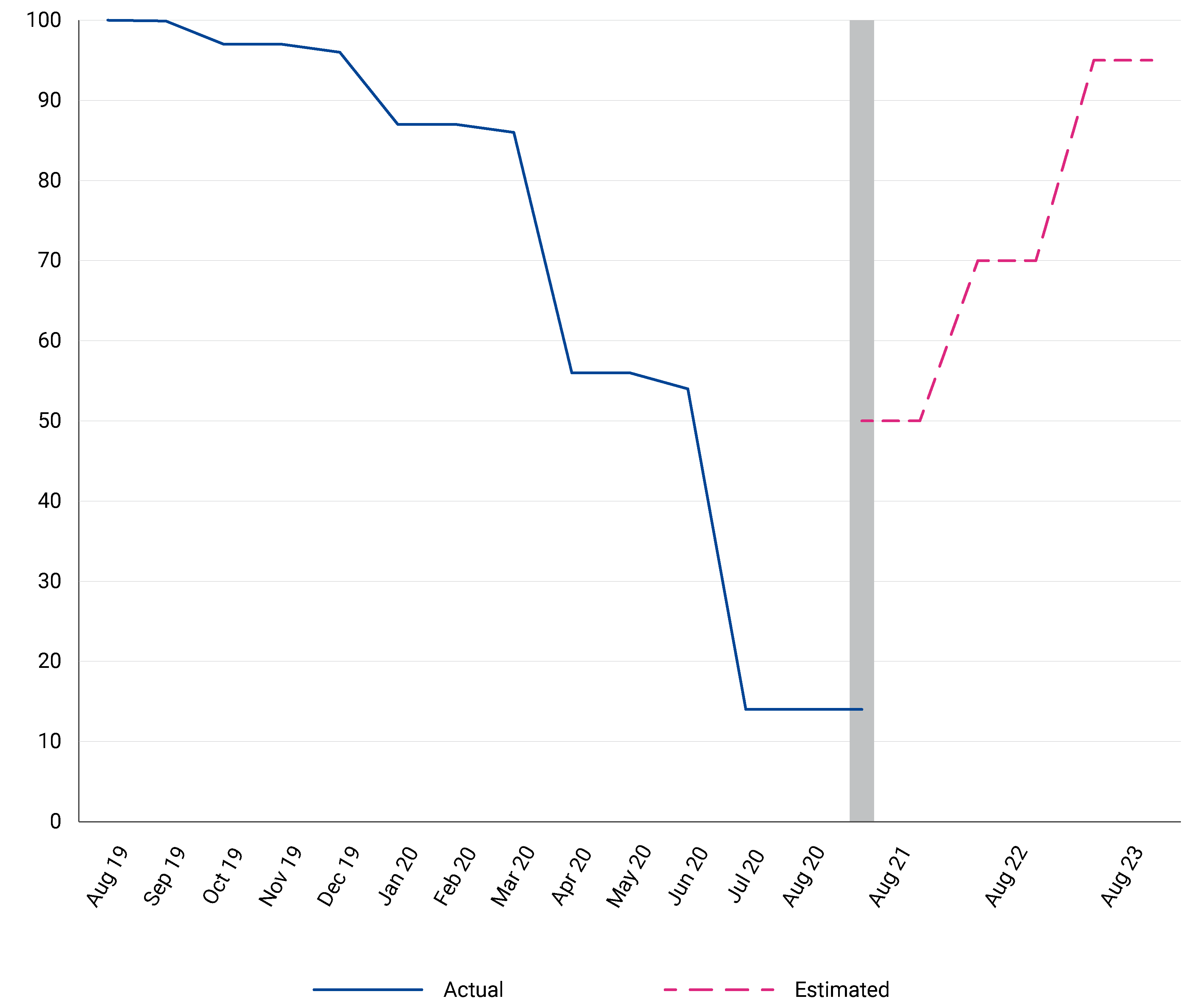

As a result, according to market analysts’ projections on 19 August 2020, earnings per share are currently around 15% of what they were a year ago. And next year, they are expected to improve to 50% relative to August 2019. It will take more than three years for the average earnings per share of listed euro area banks to approach the already depressed pre-crisis levels (Figure 4).

Figure 4: Actual and estimated earnings per share of listed banks will approach pre-crisis levels only in more than three years

Source: Bloomberg. Note: Actual and estimated earnings (cut-off date 19/08/2020) per share of banks in SX7E Index in 2020 and in the next three years compared with August 2019.

However, financial market observers do pay attention to the details. Before Covid-19 a small number of banks in Europe could attract better market valuations thanks to their strategic focus and operational choices and, hence, profitability. These banks have been able to innovate, transform and adapt their business to the profound changes in social behaviour and demands of the economic agents. Covid-19 has made this call even more urgent. To support and facilitate this transformation, even among traditional and larger commercial banks, market conditions and regulation need to evolve. At the same time, banks themselves need to continue their work on restructuring, digitalisation and innovation to spur efficiency and productivity.

The sudden halt caused by Covid-19 has the potential to derail banks’ transformation efforts and to weaken the entire sector in the longer run, hampering future economic growth. Banks have to address the emergency and focus on immediate customers’ needs of restructuring and renegotiating, while dealing with a deteriorating operational environment and emerging defaults. The challenge is maintaining momentum and progressing on multiple fronts. Profitability was and will be the key hurdle; further pressured by low interest rates and flat term premiums, banks will face multiple strategic dilemmas between an inevitably impaired organic growth, radical transformation and market exit.

Although the health of banks pales in importance compared to the humanitarian shock caused by Covid-19, thinking of initiatives geared towards the banking sector is essential to ensure funds continue to flow to households and firms, thus helping the recovery.

To pool and activate the necessary resources, countries can draw on the joint EU responses as well as on national development agencies, banks and investors. Industry-wide initiatives could help find the way to a new equilibrium where banks are safer and can produce sustainable profits. These factors are adequately reflected in market expectations.

However, without a concerted effort to support banking union, we risk that the crisis will act as a catalyst of the existing divergences, exacerbating vulnerabilities across different national banking sectors and fuelling disintegrating forces. We will miss the opportunity to support growth and stability at the same time.

A truly integrated market for banking services with fully harmonised rules, well-funded and encompassing regimes for orderly resolution - including a strong safety net for depositors and a backstop to the Single Resolution Fund - are necessary conditions for a sound and safe banking sector in the euro area. Even more so, to navigate the euro area out of this pandemic.

We will return to the topic of completing banking union in future blogs.

Footnotes

Further reading

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager