Euronomics: Charting a new course - Europe's response to global disruptions

Global political uncertainty has become a persistent feature of the changing international order, which presents Europe with both a challenge and an opportunity to adjust its policy frameworks. A comprehensive reset could build upon three foundational principles:

- strengthening the single market and creating diversified external supply chains,

- leveraging defence investments for innovation and convergence in the medium term, and

- establishing a nimble and reliable European Union-level policy framework to tackle disruptions.

Today’s challenges pave the way for tomorrow’s opportunities

Global political uncertainty and a shift from multilateralism to transactional power dynamics are now pervasive features in international relations. Policy disruptions are reframing international relations into a competitive game, particularly in discussions about trade and defence. Higher tariffs and reduced defence protection add to the existing challenges of climate change and ageing populations, limiting fiscal space and further straining financial stability.

By understanding the nature and impact of each policy option, Europe can choose the most appropriate course of action to simultaneously address its vulnerabilities and chart a new path on multiple agendas.

Higher tariffs – more frictions in an increasingly fragmented global economy

Geoeconomic uncertainty is weakening the European growth outlook and higher United States (US) tariffs add downward pressure. The US represents nearly 21% of the European Union (EU) goods export market,[1] making the immediate impact of additional tariffs (if ultimately applied) contractionary.

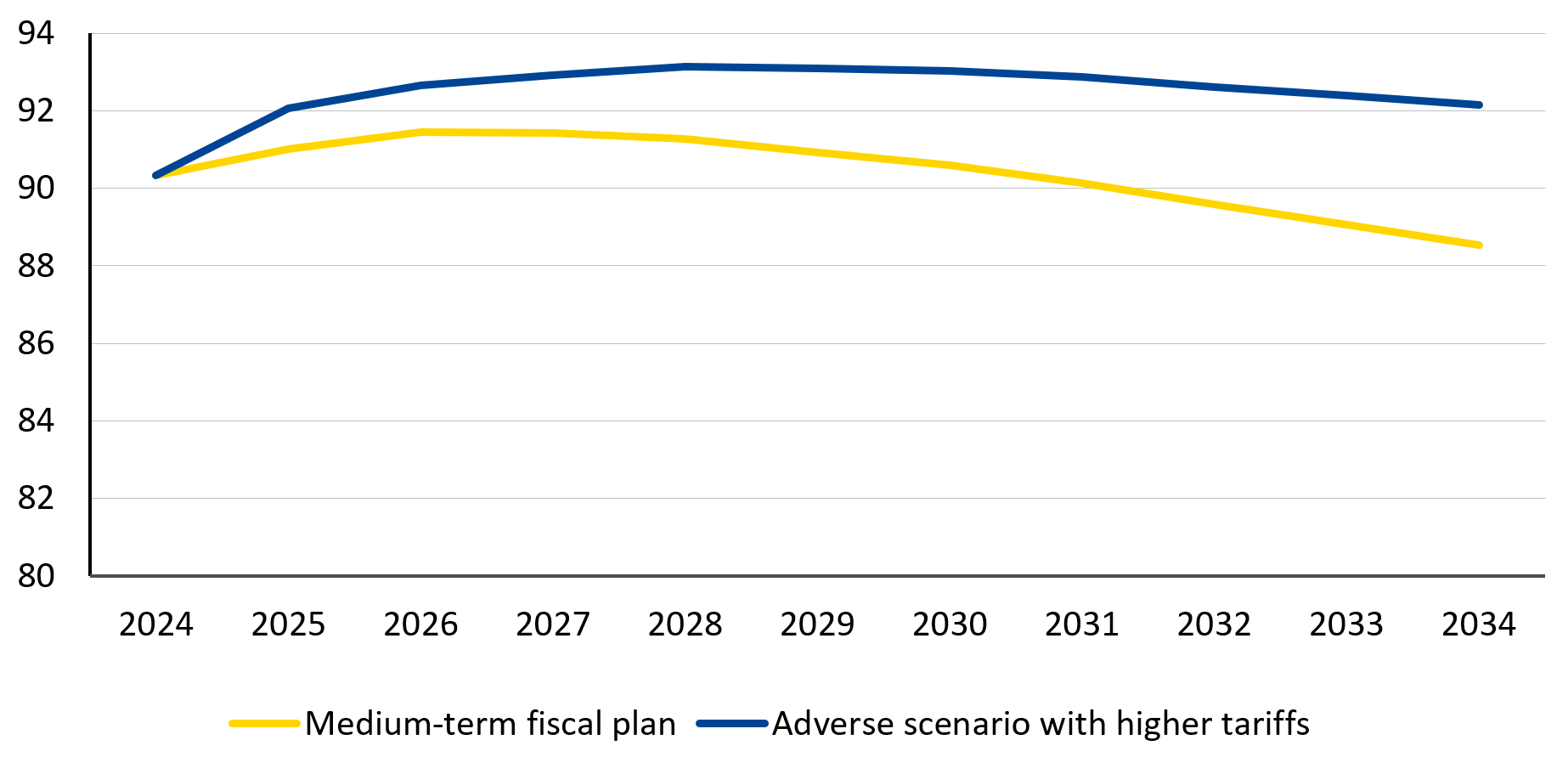

Lower growth will translate into lower revenue, reducing fiscal space. If the tariffs stand, fiscal deficits will increase, and compliance with fiscal rules (i.e. the stipulated net expenditure path) might not be enough to bring public debt down in the medium and long term (Figure 1).

Figure 1: Euro area projected debt following the rules and weathering the trade shock (in % of gross domestic product (GDP))[2]

Sources: European Commission, and ESM staff estimates

Geopolitical shifts: defence spending as the new policy priority

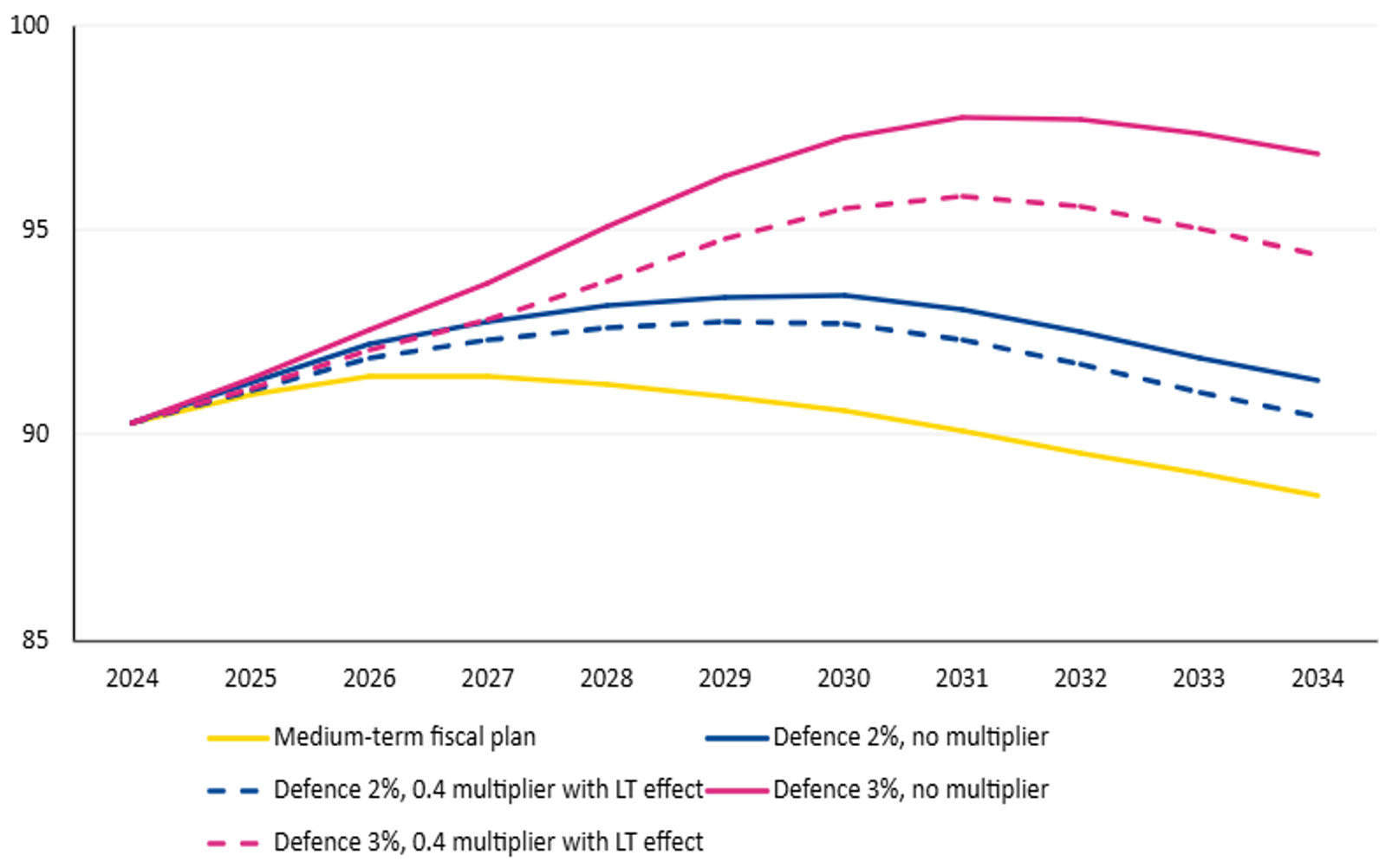

With increased volatility along the eastern flank and reduced US military protection, Europe’s security and strategic autonomy require substantial defence spending that will impact fiscal deficits, interest rates, and long-term financing strategies. In the view of many observers, the surge in defence spending needs is likely to exceed the original 2%-of-GDP target set for defence[3] and return to Cold War era levels of 3% of GDP or more.[4], [5]

The ultimate impact of defence spending on public debt will depend on the growth multiplier. Unlike traditional infrastructure spending, the growth multiplier of defence spending is uncertain and typically lower, unless accompanied by innovation that benefits both defence and civilian sectors.[6]

Figure 2: Euro area debt—catching up on defence (in % of GDP)[7]

Note: LT stands for long-term.

Sources: European Commission, and ESM staff computations

EU policy outlook in a fragmented and uncertain global environment

The current environment’s disruptions reduce the policy space available to fiscal authorities, complicating economic stabilisation efforts. Some European tariff retaliation efforts are in the works on a broad range of US exports which, though perhaps a desirable signal from a political point of view, will undoubtedly amplify economic costs.

Addressing these challenges requires a longer-term policy response, and I see three important dimensions to shape those around trade and defence.

I: Trade uncertainty: easing the transition to stimulate potential growth

Tariffs increase production costs, decrease external demand, and disrupt supply chains leading to a reallocation of capital and labour. European firms will need to adapt. The primary step is to advance the integration of the single market, and ensure a new economic structure shaped along the principles of variety and diversification.

The EU is externally vulnerable but also uniquely prepared to deal with a fragmented global economic order.[8] Differently from the US, the EU is composed of very different economies and a strong manufacturing core that “provides the scope and scale to support European-based supply chains.”[9] Beyond that, the diversification of supply chains can also be pursued externally. At the same time, long-term reallocations might enhance domestic linkages and productivity.

II: Defence policy as an opportunity to support innovation and convergence

A defence scale-up focused on domestic demand and investment that fosters innovation and maximises linkages with the civilian industry could stimulate growth. Europe could leverage on its strong industrial base, providing incentives to partially reorient operations towards defence. Public spending on defence could play a catalytic role by providing certainty to firms and supporting private investment, allowing for increased adoption of artificial intelligence in manufacturing, and ultimately increasing the growth multiplier. This would, in turn, help absorb defence spending in the budget planning and help mitigate risks to debt sustainability.

Given the urgency of the matter, relying on short-term debt financing seems unavoidable. But, should the increased defence spending become permanent, countries will need to reintegrate it into the medium-term plans and deal with potential trade-offs upfront.

III: Nimble policy framework to deal with disruptions

Structural changes beget policy frameworks that can adapt, guide market perceptions, and anchor expectations. The current experience suggests that medium-term plans in the EU’s fiscal framework should be robust against major structural shocks. This would allow markets to have a clear view on fiscal policy developments, reducing uncertainty.

A nimble policy response framework works best with a resilient financial system and flexible financing options. First and foremost, progress towards a savings and investments union increases investment efficiency and helps pool risk across a diverse economic landscape. Resilient public finances are best supported by precautionary financing arrangements from key European institutions. As seen during the Covid-19 pandemic crisis, the existence of such instruments, such as the ESM’s Pandemic Crisis Support credit line, could help stave off adverse market reactions, even if they are not used.

The challenges are here, but so are the opportunities. From carrying through old solutions to introducing new ideas, Europe has what it takes to adapt and grow more resilient.

Acknowledgements

The author would like to thank Giovanni Callegari and Ermal Hitaj for their insightful comments and contributions to this blog post, Aleksandra Kolndrekaj and Luca Zavalloni for valuable input, and Raquel Calero and Cedric Crelo for their editorial review.

Further reading

Banque de France (2025). “Trade War and Geoeconomic Fragmentation.” Available here.

European Investment Bank (2025) “Investment Report 2024-2025 – Innovation, Integration and Simplification in Europe.” Available here.

Grabbe, H., & Zettelmeyer, J. (2025). “Not yet Trump-proof: an evaluation of the European Commission’s emerging policy platform”. Bruegel. Available here.

Ilzetzki, Ethan (2025). “Guns and growth: The economic consequences of defense buildups.” Kiel Report, No. 2, Kiel Institute for the World Economy (IfW Kiel). Available here.

IMF (2023) “Europe in a Fragmented World”, Speech by G. Gopinath, available here.

Schularick, M. (2024). “Arming for Growth.” Kiel Focus, Kiel Institute for the World Economy (IfW Kiel).

Tordoir S., S. Valleee, O. Reiter and R. Stehrer (2025), “Europe’s Policy Options in the Face of Trump’s Global Reordering”, ECON committee In-Depth Analysis, Brussels, available here.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager