Electronic trading – a boost to ESM bond market resilience

Electronic trading has led to faster trading environments, enhanced transparency, and improved liquidity. These benefits contribute to the effective operation and regulation of financial markets, supporting greater financial stability.

The European Stability Mechanism (ESM) and its predecessor, the European Financial Stability Facility (EFSF), fund themselves primarily through the sale of bonds, which are complemented by short-term bills and, more recently, commercial paper securities. After being issued to investors through primary transactions, these euro area government-backed fixed-income securities can be traded in secondary markets, often bilaterally between buyers and sellers via a network of dealers in the over-the-counter market.

Traditionally, this involves voice trading, where one or more dealers are contacted via phone or an online chatroom, a process that can be time-consuming and lack transparency. Advances in technology have encouraged electronic trading, where buyers and sellers transact through electronic platforms that offer access to multiple dealers, potentially speeding up trade execution time, reducing costs, improving transparency, and providing innovative standardised trading methods.

Electronic trading plays a crucial role in ESM and EFSF bond markets, accounting for a majority of the traded volumes and enhancing liquidity in the secondary markets by improving price discovery and making primary market transactions more efficient, especially in challenging market conditions. These advantages allow the ESM to issue bonds more effectively, benefitting its mission to support euro area financial stability.

The increase in electronic trading

Various electronic trading platforms offer automatic matching of buy and sell orders or operate as centralised exchanges. In asset classes like equities and commodities, most trading is now conducted on electronic exchanges or via high-frequency automated platforms. Over the past two decades, euro area government bond markets have also moved predominantly to electronic trading. As more innovative solutions are developed, less mainstream segments of the fixed income markets, such as the supranational, sub-sovereign, and agency (SSA) markets, are being impacted. Trading in ESM and EFSF bonds, part of the broader SSA market, is no exception and has undergone a significant move towards electronic trading in recent years.

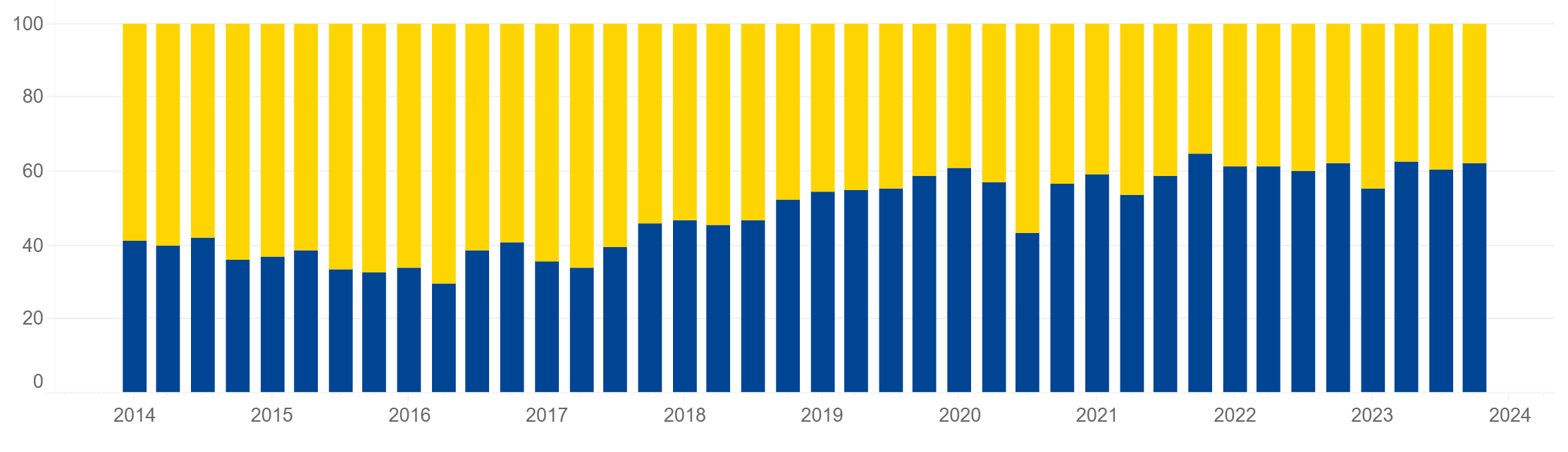

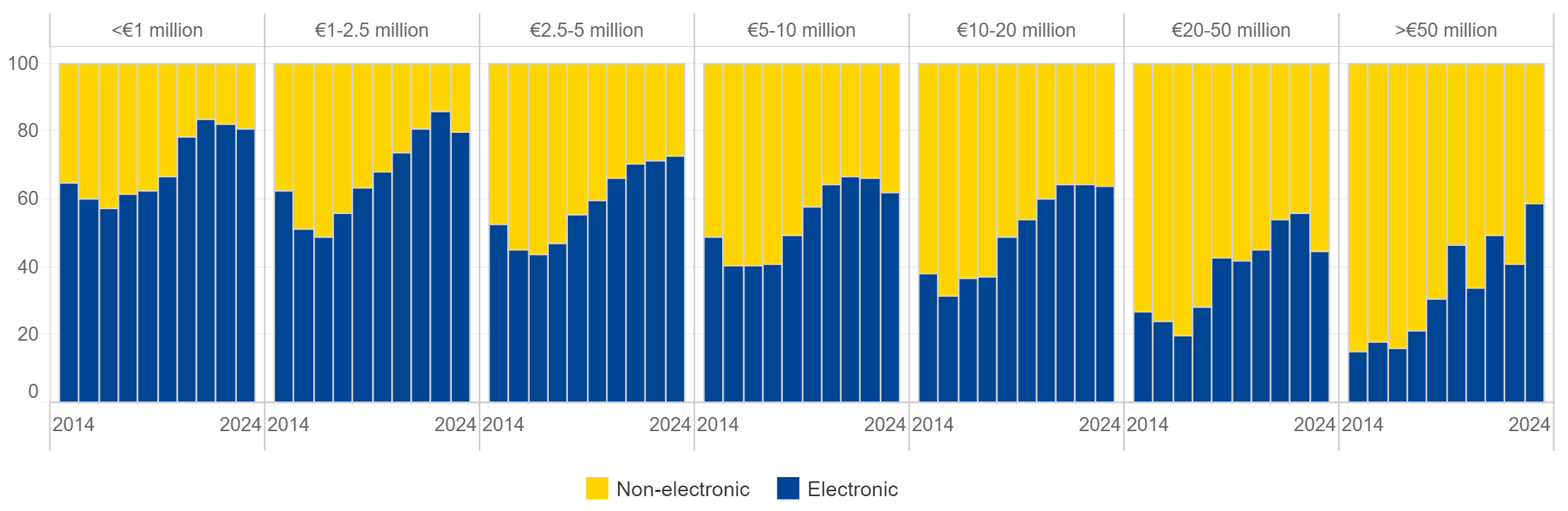

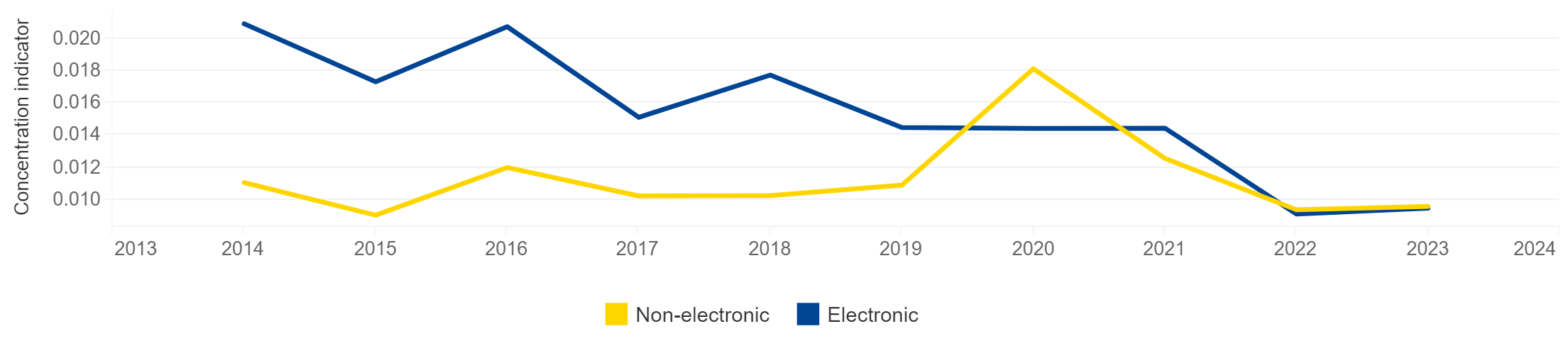

Figure 1: Electronic vs non-electronic trading activity in ESM and EFSF bonds

(% share of volumes traded in secondary markets in terms of bond face value)

Figure 1a: Quarterly share of traded volume

Figure 1b: Annual share of maturity weighted volume by trad size category

Source: ESM

Figure 1a shows the rise in electronic trading for ESM and EFSF bonds over the past decade based on ESM internal data, including over 300,000 secondary market bond trades of €1.2 trillion, as reported to the ESM by a market group of primary dealers. Over this period, the electronic trading share has increased to 60% from around 40% in terms of traded volume of exchanged securities and to 80% from around 55% in terms of number of executed trades. The electronic trading momentum briefly stalled after the initial Covid-19 lockdowns in the third quarter of 2020 but has quickly regained momentum since then. The electronification trend is confirmed across market segments of different investor types and regions, with some segments more advanced than others, e.g. private fund managers compared to central banks and other public institutions.

Figure 1b, however, shows that the overall share of electronic trades as well as initial levels decrease as the size of trades increase. Larger trades bear a larger market risk, often encouraging investors to trade them through less transparent voice trading channels. Still, the largest trade size category shows the most prominent shift and continuous adoption of electronic trading. This contrasts with trades below €2.5 million, where the use of digitalisation was high already a decade ago (around 60%) and appeared to plateau at 80% in 2022. It remains to be seen if the electronification of small bond trades will expand further. We may witness a continued coexistence of voice and electronic trading in this area, where voice trading still plays a part in more complex transactions that necessitate hedging or during periods of significant market volatility when electronic liquidity can deteriorate even for smaller volumes.

Electronic trading enhances liquidity

Well-functioning secondary markets that are active and liquid are important for investors to effectively manage their positions and for issuers to conduct efficient primary market transactions. While the ESM does not oblige its market group of primary dealers to quote on any specific trading platforms, there has been noticeable growth in activity on electronic platforms across different trade sizes, as well as improved market liquidity as measured by activity distributions across various market segments.

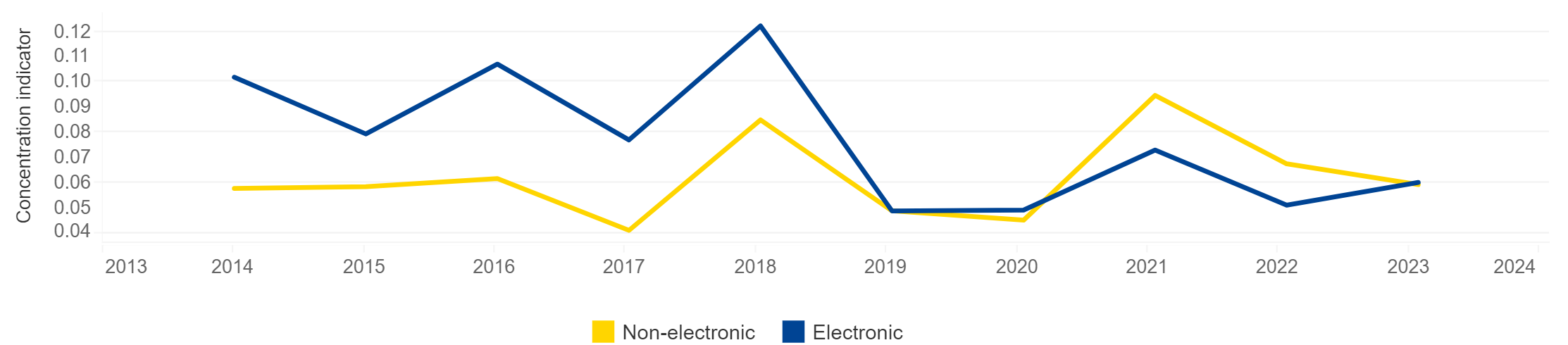

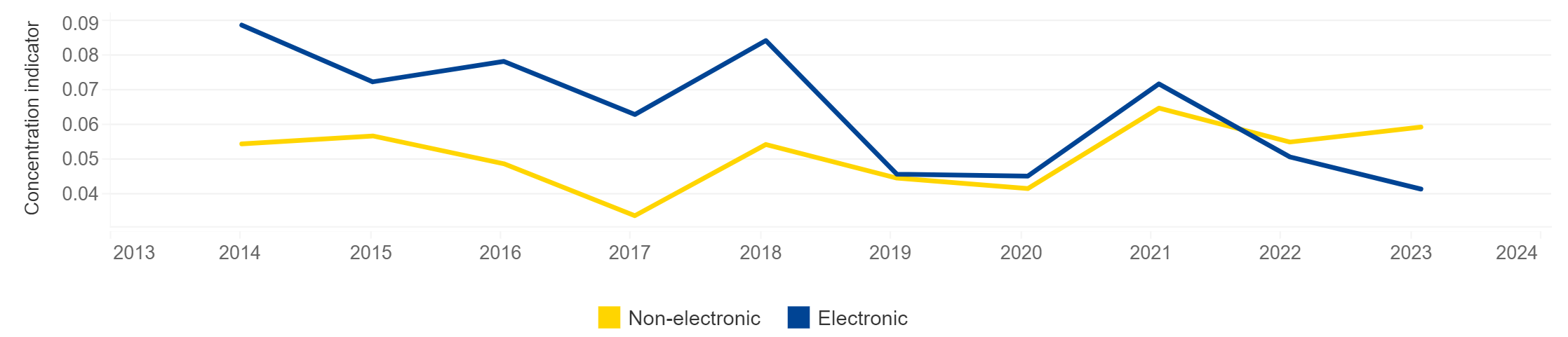

Figure 2: Distribution of ESM and EFSF bond trading activity across bonds and investors

(based on secondary market trades larger than €50 million; larger value indicates higher concentration)

Figure 2a: Distribution of traded volumes across bonds

Figure 2b: Distribution of number of trades across bonds

Figure 2c: Distribution of traded volumes across investors

Source: ESM

The scope of trading on electronic platforms has broadened over time, transitioning from a limited number of securities to encompassing a similar range of securities as in non-electronic trading, particularly within the segment of riskier trades exceeding €50 million. Figure 2 demonstrates this trend by showing the development of different levels of concentration throughout the past decade. It indicates that the execution of large trades on electronic platforms has improved, now offering comparable depth across different bonds as voice trading, and even surpassing voice trading in terms of number of trades.

This shift in trading practices suggests that investors now have access to markets of comparable depth on electronic and voice platforms, both in terms of bonds traded and in the participation of other investors. Balanced access to diverse trading methods is necessary as it equips buyers and sellers with broader ways to transact in volatile markets and demonstrates that activity is not merely shifting from voice to electronic platforms, but that both options offer access to similar levels of liquidity across securities and investors. Consequently, electronic trading can now serve as a strategic complement to voice trading, even for high-risk transactions.

Electronic trading remains active in volatile markets

We examined electronic trading behaviour during periods of increased market volatility, focusing on both isolated bond volatility (events as defined by at least 99th percentile of daily bond returns using Bloomberg as the market data source) and significant stress events such as the Covid-19 market crash, the interest rate hikes in 2022, and the banking crisis in 2023. Our findings indicate that the share of electronic trading volumes remained high overall also during these periods, declining by up to 10% on the day of the event but normalising in subsequent days. Without more detailed order book data, we conclude that market participants successfully engaged in transactions on electronic platforms, which continued to complement voice trading.

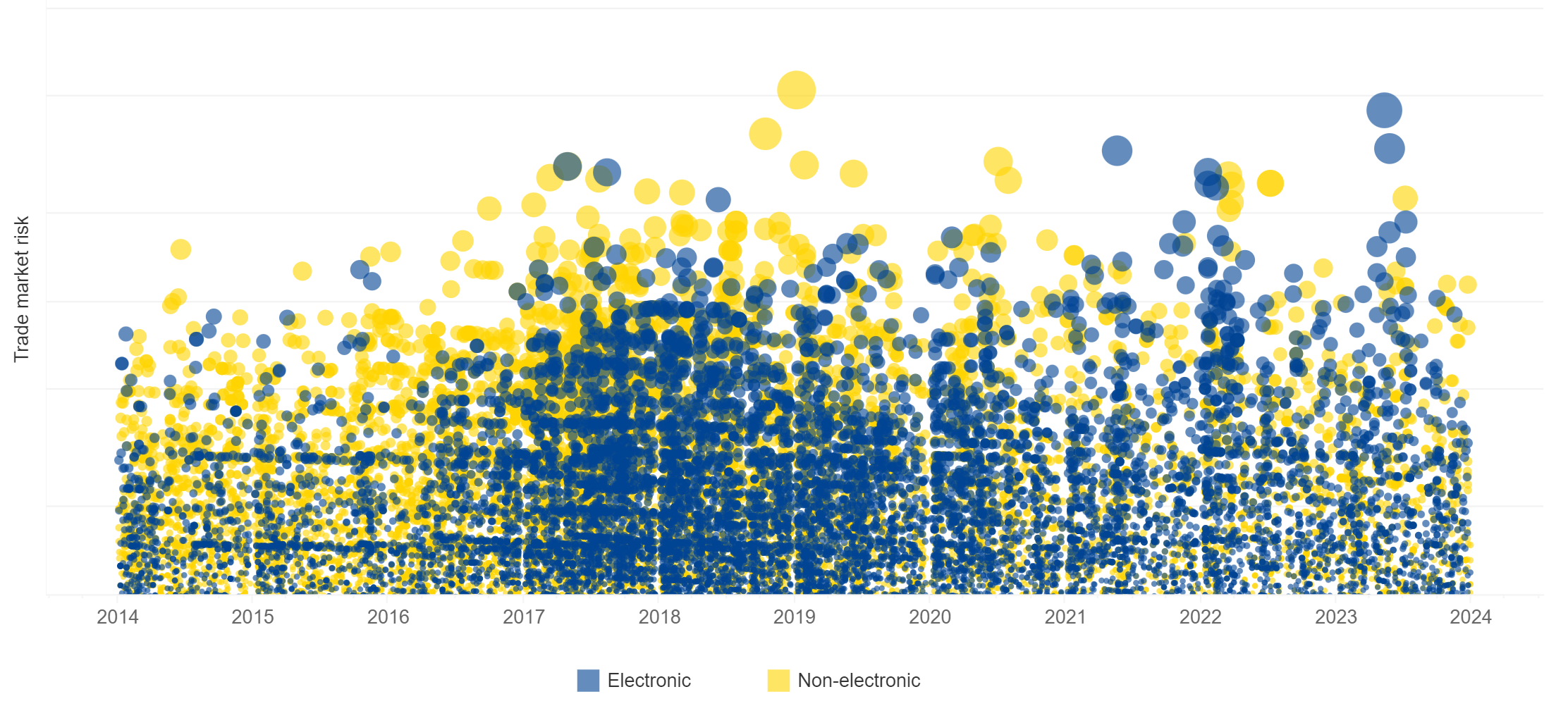

Innovative technologies are transforming how buyers and sellers interact, facilitating trade automation, and bringing bond markets into an era of algorithmic trading, particularly as artificial intelligence continues to advance. Whereas electronic trading already dominates some ESM and EFSF bond market segments, such as small transactions and private fund managers, it continues to grow in others, including public institutional investors and high-risk trades (with respect to market risk), as illustrated in Figure 3. It remains to be seen if electronic trading will entirely dominate bond markets or if a portion will remain managed through traditional voice trading.

Figure 3: Individual ESM and EFSF bond trades by market risk and type of execution in the secondary market

(vertical axis is shown in logarithmic scale, size of each circle is proportional to the trade’s market risk)

Source: ESM

A well-balanced secondary market that blends traditional voice trading with modern electronic platforms providing market participants comparable liquidity levels supports efficient market functioning, particularly during periods of high volatility. The continued high proportion of electronic trading that we have seen during the Covid-19 market shock and other recent increases in market volatility may explain why ESM and EFSF bond markets have remained active and resilient during these events, thereby contributing to the stability of the euro area financial system.

Acknowledgements

The authors would like to thank George Matlock and Ivan Semerdjiev for the valuable discussions and contributions to this blog post, Raquel Calero for the editorial review, and Peter Lindmark for the graphics.

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors