Developing European safe assets - article in Intereconomics

Chief Financial Officer, ESM

“Developing European Safe Assets”

Intereconomics, December 2023

Volume 58, 2023 · Number 6 · pp. 315–319 · JEL: H63, H61, G28

Safe assets rank as the most assured and reliable securities, commanding the highest credit ratings, and are a key component in a well-functioning capital market. Safe assets are critical for economies and their existence is especially welcomed in capital markets in times of market stress or uncertainty.

They are typically associated with three fundamental characteristics (Gorton 2017, Brunnermeier et al., 2016, 2017, Brunnermeier and Huang, 2018, Gorton and Ordonez, 2022): a high credit worthiness (asset “quality”), an ability to retain value in the event of adverse market price movements (“robustness”), and a strong liquidity profile (“liquidity”).

Thanks to these characteristics, market participants can use safe assets as a refuge in the event of market turmoil, as collateral in financial transactions, as a risk management instrument, or as a reference for pricing other financial securities.

The European safe assets base includes government bonds from the highest-rated euro area countries, as well as bonds issued by European supranational institutions that are backed by the European Union or euro area countries. German Bunds form naturally the first level of safe assets in the euro area. They are complemented by government bonds from euro area countries with ratings similar to those of Germany.

Bonds issued by European supranational issuers – the European Investment Bank, the European Union, the European Financial Stability Facility, and the European Stability Mechanism – are part of this European pool of safe assets. They were created to respond to the various challenges Europe experienced. They are part of what markets define as the European safe assets.

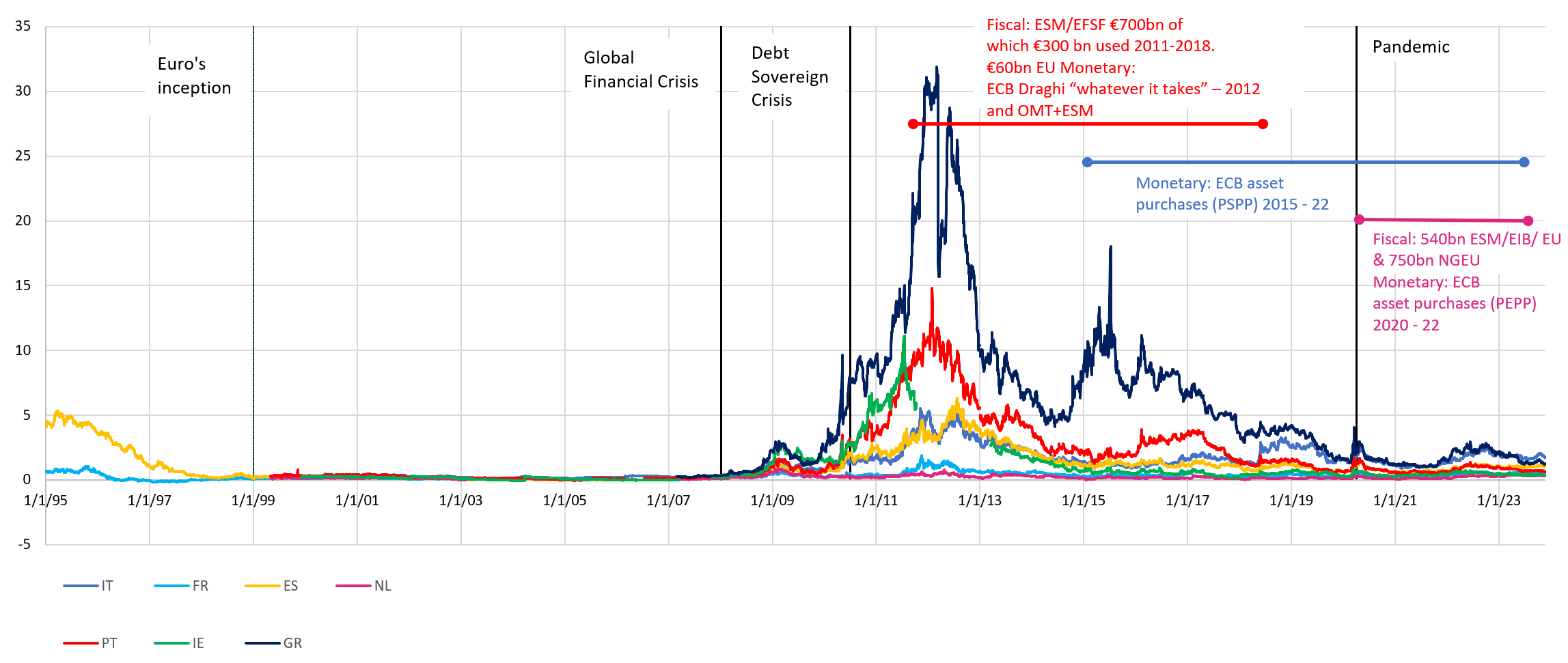

The creation of the European safe assets stems from the important role that a deep safe asset base contributes to financial stability in times of crisis, such as the Global Financial Crisis and the European Sovereign Debt crisis. We witnessed the positive market impact that the creation and usage of safe assets had (Figure 1). The creation of the European Financial Stability Facility in 2010 and European Stability Mechanism in 2012 and its programmes combined with the ECB response helped to reassure markets. This was manifest with reduced bond yield spreads relative to Germany in several euro area countries. The EFSF, the ESM, and the coordinated policy response with the European Union, European Central Bank and International Monetary Fund contributed to this success. During the Pandemic, the initial €540 billon policy response of the European Stability Mechanism (ESM), European Investment Bank and European Union, followed by the €800 billion Next Generation EU post-pandemic recovery vehicle further eased upward pressure on euro area countries' bond yield curves.

As figure 1 shows, the financial markets punished the absence of shock absorbers in Europe. But by 2015, when Greece needed more financial assistance, which the ESM provided, it is evident that even 10-year Greek government bond (GGB) spreads versus German Bunds were less than half of that experienced 5 years earlier. By 2020, when the pandemic became a common shock for Europe, GGB spreads widened even less. Over time, Europe’s financial architecture has reassured markets, and we see less volatility and narrower spreads. Europe was able to calm markets.

Figure 1: yield spread evolution of euro area Sovereigns against Germany

(percentage points)

Source: Bloomberg, ESM

History of European Safe assets

The European Investment Bank (EIB) created the first European safe asset. It was founded in 1958 by the Treaty of Rome and was granted permission to issue bonds. From 1961 – when its initial loan of 20 million guilders was floated on the capital market of the Netherlands – to 1972 (just before the first enlargement of the European Economic Community), the EIB issued 99 loans for an amount of almost 2 billion (Bussiere, et al, 2008). Initially, the EIB was backed by the six founding members: Luxembourg, Belgium, Netherlands, Italy, France and Germany. Today, the EIB has 27 shareholders – the 27 member states of the European Union.

The second European safe asset came from the European Union. The EU issued several community bonds on private markets since the 1970s, which were guaranteed by the member states and distributed to countries where required. (Meyer, et al 2020). The first European Community bond was issued in 1976 and used for Italy and Ireland.

The third European safe asset issuer was the European Financial Stability Facility, created in 2010 as a response to the Global Financial Crisis and European Sovereign Debt Crisis. The EFSF issued its first bond in 2011, for the Irish adjustment programme.

The fourth European safe asset issuer was the European Stability Mechanism. Founded in 2012, the ESM issued its first bond in 2013 for the Spanish bank recapitalisation programme.

Comparison of European safe assets

The four European supranational issuers have different institutional bases. The EFSF is a private company under Luxembourgish law owned by the 17 countries of the euro area upon its creation. It excludes Latvia, Lithuania, and Croatia, who joined the currency bloc later. The EFSF has very limited capital and its bonds are backed by explicit guarantees of the 17 countries. The six best credit-rated euro area countries (Luxembourg, Finland, Netherlands, Germany, France and Austria) over-guarantee up to 165% in order to ensure a safe asset status and high credit rating.

The European Stability Mechanism is an inter-governmental institution under international law. It has a paid-in capital of €80.5 billion and callable capital of €624 billion. It is owned by the 20 countries of the euro area.

The European Investment Bank is owned by the 27 European Union Member States. Its paid-in capital is €22 billion, and it has €227 billion of unpaid subscribed capital.

The European Union is backed by the 27 European Union Member States, it has no paid-in capital. The European Union borrowing is guaranteed by the European Union budget.

The four European Supranational issuers accounted for almost €1 trillion in euro-denominated bonds and notes as of 6 November 2023. The EU, with €431.3 billion was the largest, followed by the EFSF/ESM with €276.7 billion, and the EIB with €250.7 billion.

Table 1: Comparison of the four European supranational issuers

| European Financial Stability Facility | European Stability Mechanism | European Investment Bank | European Union | |

|---|---|---|---|---|

| Ratings | Aaa/AA/AA- | Aaa/AAA/AAA | Aaa/AAA/AAA | Aaa/AA+/AAA |

| Ownership | Private company under Luxembourgish law owned by the 17 euro area member states at the time of EFSF creation | Inter-governmental under international law owned by the 20 euro area member states | Owned by 27EU member states | Owned by 27EU member states |

| Guarantee | Explicit | Implicit | Implicit | Implicit |

| Subscribed capital paid-in | €745mn | €81bn | €22bn | Non applicable |

| Subscribed capital unpaid | Non applicable | €624bn | €227bn | Non applicable |

| Risk weighting | 0% | 0% | 0% | 0% |

| Liquidity coverage ratio | Level 1 | Level 1 | Level 1 | Level 1 |

| Purpose | Limited to rolling over maturing debt (outstanding loans €172.6bn: 76% GR, 14% PT, 10%IE) | Permanent institution, to enable countries of euro area to avoid/overcome financial crises | To support investment in infrastructure projects, and SME development, and to mitigate the effects of global warming | To support recovery from the COVID-19 crisis and investments into a sustainable economy |

| Eligible for the public sector purchase programme | Yes | Yes | Yes | Yes |

| 2023 funding (estimates) | €20bn (liquid benchmark bonds, up to 2056, private placements) | €8bn (liquid benchmark bonds EUR, USD, maturities 1 to 45y, private placements) | Up to €50bn (mainly EUR, USD, 3-5bn size, benchmarks 2-30y, green bonds) | €170bn borrowing authorisation for the year (liquid bonds from 3y, 30% green format) |

Sources: EU, EIB, ESM

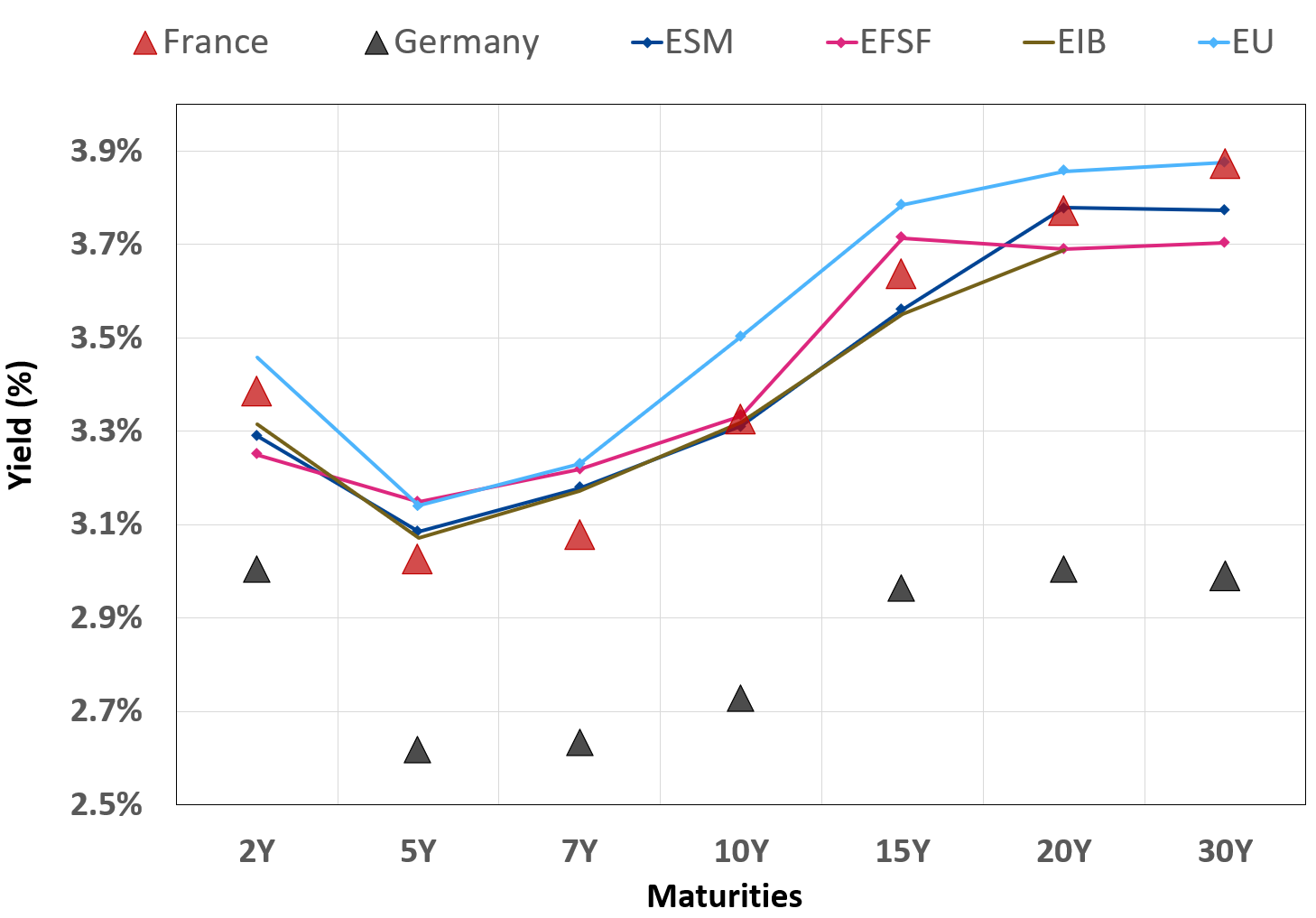

The four European safe asset issuers price close to the strongest European sovereigns. They include a market premium compared to Germany and are close to France.

The longest established issuer, the European Investment Bank, has the tightest market pricing. It is followed by the European Stability Mechanism – with a strong capital base – and the EFSF. The European Union trades the widest among the four issuers, since the introduction of the NGEU vehicle.

Figure 2: yield curve of the four European supranational issuers versus Germany and France

(As of 6 November 2023)

Sources: Bloomberg, ESM

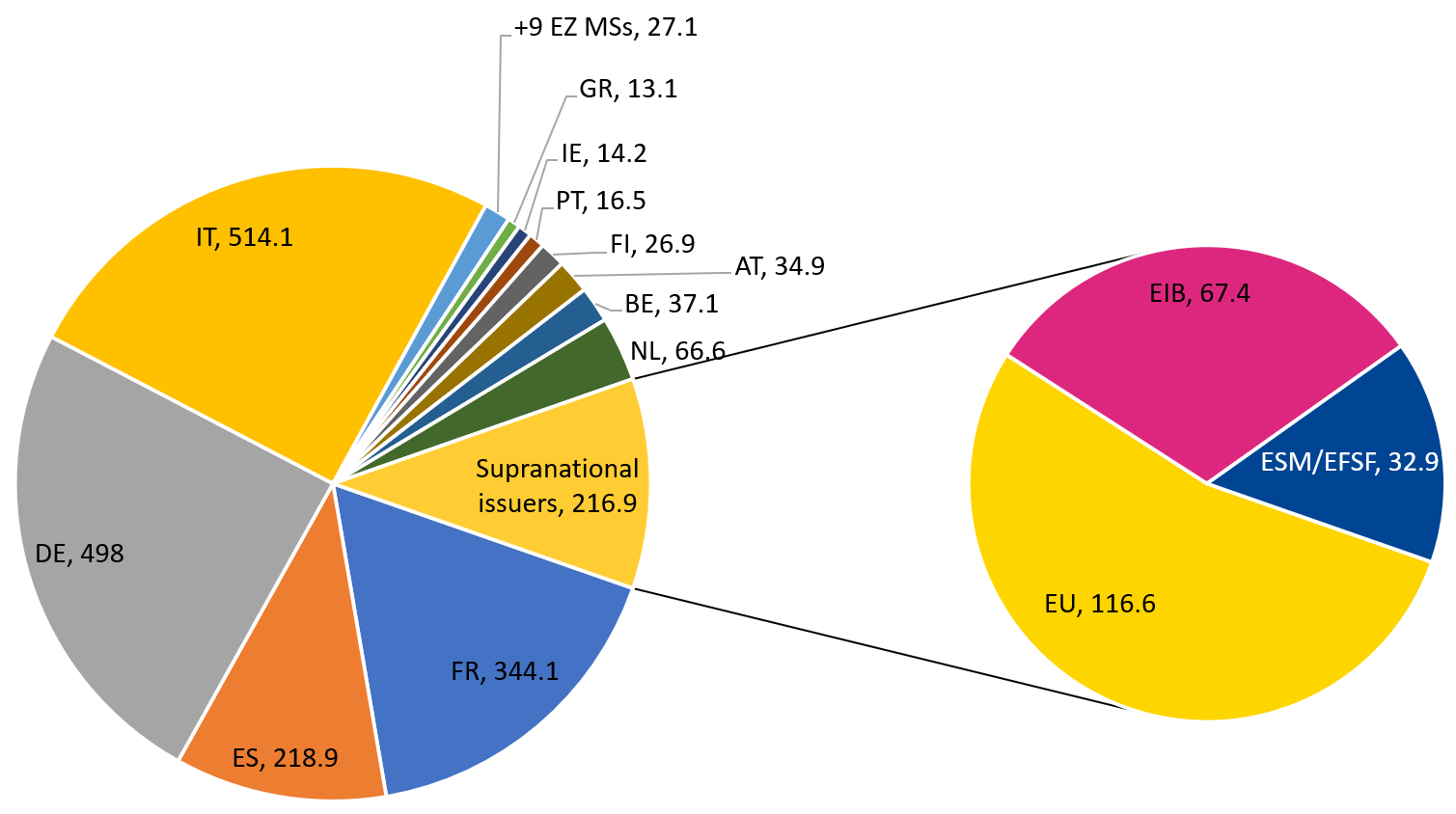

In terms of market liquidity, the government bonds issued by Italy, Germany, France, and Spain are the most liquid ones. The European safe assets are fifth in terms of liquidity. The chart displays daily average traded volumes for the main government and European safe assets.

Figure 3: daily average traded volumes for the four European supranational issuers versus euro area Sovereigns

Sources: AFME, Finbourn (Oct 2022)

It is worth noting the difference between highly-rated government bonds and the ones from the four European supranational issuers. The latter have an insurance component to break the link between sovereign and banking risks and allow a safe harbour for flight to safety (Brunnermeier et al. 2011 and 2017). This led to the proposal of the creation of European Safe Bonds (ESBies). Papadia and Temprano Arroy (2022) take it a step further and state that safe assets labelled in euro are critical for creating deep banking and capital markets unions. They also illustrate how far we have progressed already in European supranational bonds.

The size of European safe assets has been increasing over time, and this accelerated during the pandemic with the introduction of the NGEU vehicle. We have come some way in establishing European bonds as benchmarks and large investment assets with blended risk.

Markets’ appreciation

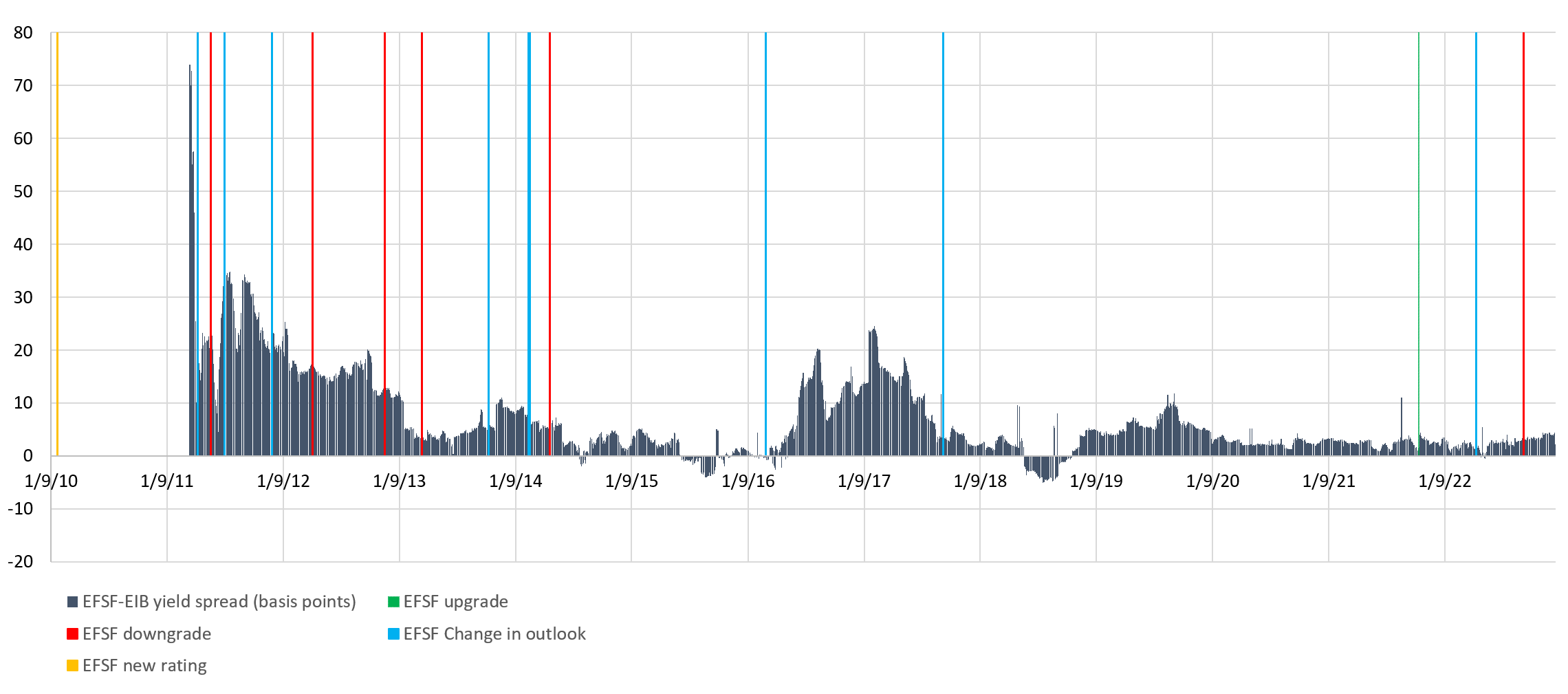

Developing a safe asset status takes time. When the EFSF was created, it traded 75 basis points above EIB in its early years. The EFSF follows closely the rating of France and has gone through similar upgrades and downgrades over the last decade. Over time, the market started recognising the EFSF as a European safe asset. Despite the upgrades and downgrades, the EFSF converged to the price of the EIB. Over the years, the spread came down to 25bp and now the price is similar with moments where the EFSF goes through the curve of the EIB.

This shows that the market – despite the volatility and different ratings, mandates and capital structures – sees these European issuers are safe assets.

Figure 4: EFSF yield spread versus EIB through rating agencies decisions on EFSF

Sources: Bloomberg, ESM

We have seen a counter-intuitive phenomenon in the European safe assets since the beginning of 2022. Despite the high ratings and good liquidity profiles of the European safe assets, their yield spreads relative to Germany widened significantly. However, this trend reversed somewhat in 2023.

These developments are the result of a number of factors, the effects of which need to be curbed to ensure that they do not lead to increased fragmentation and price distortion within the European safe assets base.

From a conjunctural perspective, the reduction of ECB bond holdings in the context of Quantitative Tightening has disadvantaged European supranational issuers more than sovereigns in terms of yield trends. Indeed, during the Quantitative Easing phase of ECB monetary policy, the ECB was able to purchase up to 50% of each outstanding bond line from supranational issuers, whereas this ceiling was limited to 33% in the case of sovereign bonds. The ECB Pandemic Emergency Purchase Programme (PEPP) came on top of these numbers. Quantitative tightening is now leading to a faster increase in free float for supranational bonds than for sovereigns, pushing their yields higher.

Additionally, the heavy bond supply from the European Union to finance the €100 billion SURE and €800 billion NGEU programmes has pushed yields of the four supranational issuers higher. Given its relative weight in the supranational market segment, the European Union has indeed become the main driving force for yield spreads of the European safe assets. The European Union has repeatedly secured a substantial order book with a high issuance premium. This has added to upward pressure on yields in the supranational market segment as a whole.

A number of structural factors also explain the yield trends that have been at work since the beginning of 2022 within the European safe assets pool.

Firstly, the ECB’s new anti-fragmentation tool, the Transmission Protection Instrument (TPI), which aims to mitigate speculative market fluctuations for sovereign bonds, does not cover supranational issuers.

Secondly, in the absence of specific hedging instruments, such as bond futures for German Bunds, bonds of supranational issuers are priced using the euro-denominated interest rate swap curve as a benchmark. Against a backdrop of rising interest rates over the past two years and heavy use of interest rate swaps by financial investors to hedge their bond positions, the spread of interest rate swaps against German Bunds has sometimes widened sharply, mechanically pushing up yields on the four European supranational issuers.

Thirdly, the non-inclusion of European supranational issuers in global sovereign bond indices has also limited the interest of some index funds in their bonds.

Finally, the four supranational issuers lack Security Lending Facilities similar to those used by sovereigns to manage the liquidity of their bonds.

Future considerations

Over and above these conjunctural and structural factors, which are holding back the consolidation of the European safe asset base, Europe needs a strong political commitment to ensure the continued success of the four European safe assets.

In particular, the concerns in the market regarding the European Union as a bond issuer are twofold.

Firstly, the market is wondering what will happen once the temporary NGEU mandate expires and new loans cease after 2026.

Secondly, questions relating to indirect and direct taxation, which would provide the European Union with its own financial resources, similar to the competence of sovereigns to collect taxes, remain unresolved.

In the longer term, there are political issues beyond the scope of this article that will need to be addressed.

But the prevalence of more safe assets supporting borderless investing across Europe from completion of Capital Markets Union and further internationalisation of the euro offer investors, businesses and citizens enormous advantages. These changes also place the European capital markets on a more level footing with their counterparts in other major economies such as the United States.

References

Brunnermeier, M.K., L. Garicano, P.R Lane, M. Pagano, R. Reis, T. Santos, S. Van Nieuwerburgh and D. Vayanos (2011) ‘ESBies: A Realistic Reform of Europe’s Financial Architecture’, VoxEU, 25 October, available at https://cepr.org/voxeu/columns/esbies-realistic-reform-europes-financial-architecture

Brunnermeier, M.K., S. Langfield, M. Pagano, R. Reis, S. van Nieuwerburgh and D. Vayanos (2017) ‘ESBies: Safety in Tranches’, Economic Policy 32(9): 175 -219

Brunnermeier, M.K., L. Huang (2018): A global safe asset for and from emerging market economies”. Working Paper 25373, National Bureau of Economic Research https://cepr.org/voxeu/columns/esbies-realistic-reform-europes-financial-architecture

Bussière, É., Dumoulin, M. and Willaert, E. (2008), The Bank of the European Union: TE EIB, 1985-2008, Imprimerie Centrale. ISBN: 978-2-87978-072-6 The EIB, 1958 -2008

Gorton, G. (2017), The History and Economics of Safe Assets, Annual Review of Economics, 9:547-86 The History and Economics of Safe Assets (annualreviews.org)

Gorton, G.B. and G. Ordonez (2022): The supply and demand for safe assets. Journal of Monetary Economics, 125, p. 132-147

Meyer, J., Trebsch, C. and Horn, S. (2020), Coronabonds: The forgotten history of European Community debt, CEPR Column, Coronabonds: The forgotten history of European Community debt | CEPR

Papadia, F and Temprano Arroyo, H. (2022), Don’t look only to Brussels to increase the supply of safe assets in the European Union, Bruegel Policy Brief, Don’t look only to Brussels to increase the supply of safe assets in the European Union (bruegel.org)

Author

Contacts