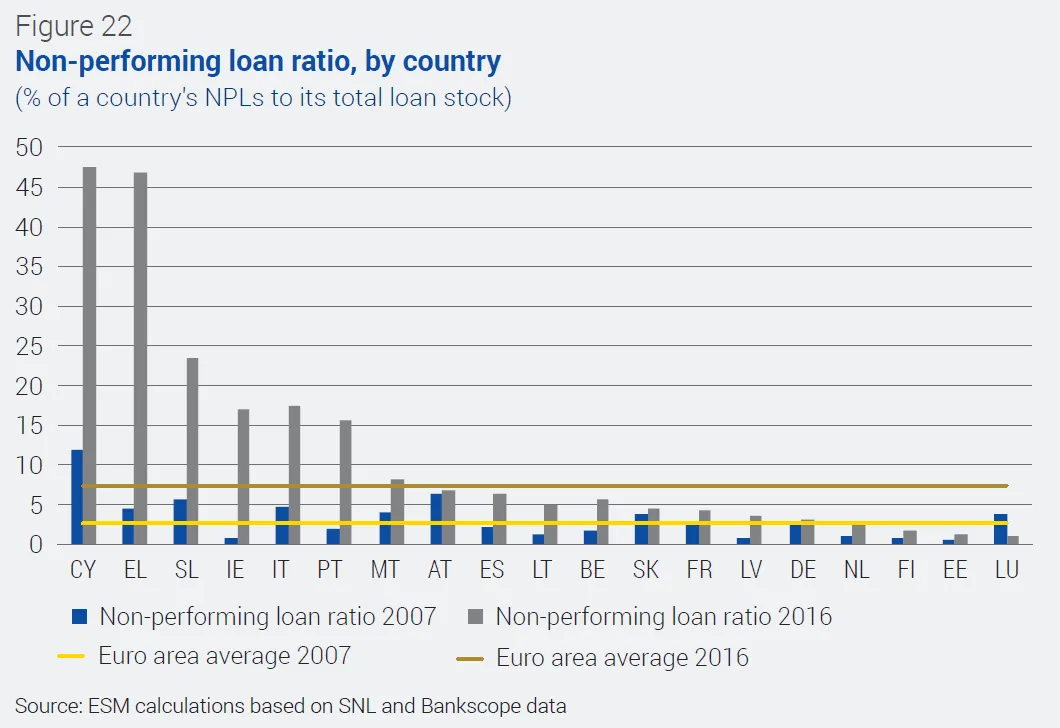

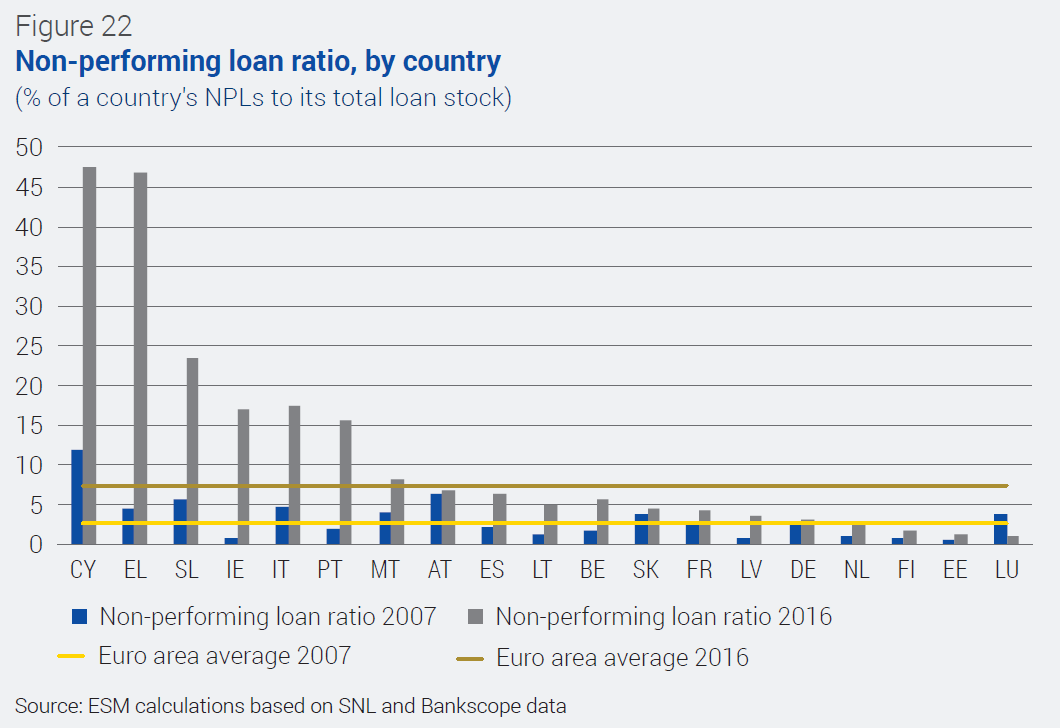

NPLs in the euro area remain a barrier to full recovery and a potential source of instability to the financial system. They represent a problematic issue overall as they tie up bank capital, put pressure on banks’ profitability and funding costs, and burden corporates and households with at least some unserviceable debt. As of the end of 2016, euro area banks still held approximately €849 billion of gross NPLs, representing 7.4% of total gross loans, up from 2.6% before the crisis (Figure 22).20 Although NPLs have declined since 2013 (-11.2%), they remain unevenly spread and uncomfortably high in current programme country Greece and post-programme countries, as well as in Slovenia and Italy.

In recent years, EU and national policy makers designed a series of regulatory and legal policies to accelerate NPL resolution. They encouraged countries and banks to use multi-pronged and complementary approaches. The measures varied. They included enhancing prudential supervision by introducing best practices for lending and provisioning, reforming debt enforcement regimes and insolvency frameworks, developing distressed debt markets by promoting the servicing and sale of NPLs, and introducing flexible and efficient securitisation laws. Certain banks also faced weak corporate governance and a lack of focus on NPL management, and needed to employ various approaches to tackle this particular problem. Solutions included launching internal bank initiatives via joint ventures with other banks and NPL management specialist companies. Establishing such specialised external asset management companies (AMCs), for example, proved particularly effective for countries where NPLs were clustered in a specific sector. Additionally, European institutions incentivised banks to set up internal NPL management units devoted to NPL restructuring and to reducing the formation of early arrears.

All programme countries have attempted to deploy a combination of these solutions but with varying results. Although these measures usually take effect mainly in the medium- and long-term, in Ireland and Spain the stock of NPLs held by the banks has already decreased by 55% and 29%, respectively, from their peak.21 An early implementation of these measures coupled with a strong economic recovery facilitated NPL restructuring and their reduction through the disposal of NPLs to companies specialised in distressed assets in the secondary market. As the bulk of NPLs in these two countries was mainly concentrated in one sector, real estate, it facilitated the standardisation of strategies and solutions, which sped up the workout process.

In Cyprus, NPLs have only recently started showing a feeble declining trend as banks’ NPL management units and legislative reforms only took effect in 2015. Additionally, NPLs were more granular and spread across all sectors of the economy, making their workout more complex. In Portugal, early crisis management under the Economic and Financial Assistance Programme (2011–2014) focused on fiscal and structural reforms instead of on NPL management, delaying the banking sector’s recovery. The fragilities of the banking sector were not properly identified during the programme and, as a result, the necessary reforms targeting NPLs were not carried out during that period. Thus NPLs are still a reason for concern. In Greece, the prolonged recession and political uncertainty made the cleaning of balance sheets more difficult. Greece has seen an increase of its NPL ratio to 46.9% by end of 2016 from 7.4% at the end of 2009. While banks experienced a significant rise in new NPLs in 2016, the rate of increase has, however, slowed materially compared to previous years. This can be attributed to the design and implementation of a comprehensive NPL strategy agreed under the Economic and Financial Assistance Programme. Greece in particular is still suffering more than other countries from weak enforcement and insolvency frameworks. However, NPLs are expected to peak in 2017 as legislative reforms take effect, in line with targets set by the Single Supervisory Mechanism.

Ireland and Spain benefited from introducing external AMCs, which helped to alleviate banks’ balance sheets. More specifically, in Ireland and Spain NPLs were predominately concentrated in one sector, real estate. The AMCs could therefore benefit from economies of scale and experienced NPL workout specialists; they improved the liquidity of usually illiquid assets like NPLs by creating a secondary market. Additionally, transferring NPLs to a separate entity forced banks to segment their problem assets, create specialised NPL management units, and emphasise NPL management. These two countries could best benefit from this solution, because both had market access and investment grade credit ratings when their respective AMCs were established, enabling them to guarantee their AMCs, ensure sustainable funding rates, and attract private investors.

Greek, Cypriot, and to a certain extent Portuguese banks faced a more complex situation and have, therefore, opted for a different solution. High levels of NPLs were spread across all sectors and were coupled with poor collateralisation and/or under-provisioning, thereby disincentivising the transfer of troubled assets to an external AMC. Greek, Cypriot, and Portuguese banks opted, therefore, for on-balance sheet solutions. They continue to work on enhancing their internal NPL workout capacities and improving the overall enforcement and insolvency environment.

Given the complexity of the problem, countries with a large stock of NPLs should pursue a number of mutually reinforcing approaches to resolve their NPLs. Based on recent programme country experiences, country-specific solutions with private sector participation can help NPL resolution. An early implementation of measures helps accelerate the solution. Irrespective of the strategy selected, an enhancement of banks’ internal workout capacity is essential to dealing with the remaining legacy issues and mitigating a potential resurgence of the problem in the near future. Legislation to establish a secondary market for NPLs and further improvements to local enforcement and insolvency regimes and frameworks are critical and complementary tools to allow for the efficient resolution of distressed debts. There is currently a broad-based discussion in the European Union on useful initiatives to further strengthen and support the conditions for NPL resolution.

20 The figures and ratios refer to the sample of 117 euro area systemic commercial banks under the supervision of the Single Supervisory Mechanism, which account for about 75% of the euro area banking sector’s total assets. The €849 billion of the euro area NPL stock refers to the same sample and source.

21 December 2013.