How non-euro countries have embraced the issuance of euro-denominated bonds

The issuance of euro-denominated bonds has become increasingly popular among countries outside the euro area. This trend has contributed to the growth of the market for bonds denominated in euro, offering investors alternatives to euro area government bonds. While issuers outside the euro area do not benefit from the protection of the European Stability Mechanism (ESM) in cases of distress, as members of the euro area (EA) do, and their bonds have gained traction due to favourable terms and the diverse benefits they offer to issuers. This blog post explores the factors driving this trend, the historical context, and the advantages of issuing bonds in euros.

Outstanding bonds issued by sovereigns globally amounted to above €75 trillion at the end of 2024, with almost 37% denominated in USD and 14% in euro. Issuance in euro has shown remarkable progress since the launch of the common currency in 1999. Among the €10.5 trillion sovereign bonds denominated in euro, those issued by countries in the euro area account for the dominant share. The remaining share corresponds to an outstanding value of €400 billion and is spread globally among 50 issuing countries that chose to issue in euro rather than their national currency, the US dollar or other currencies.

Evolution of euro-denominated bond issuance

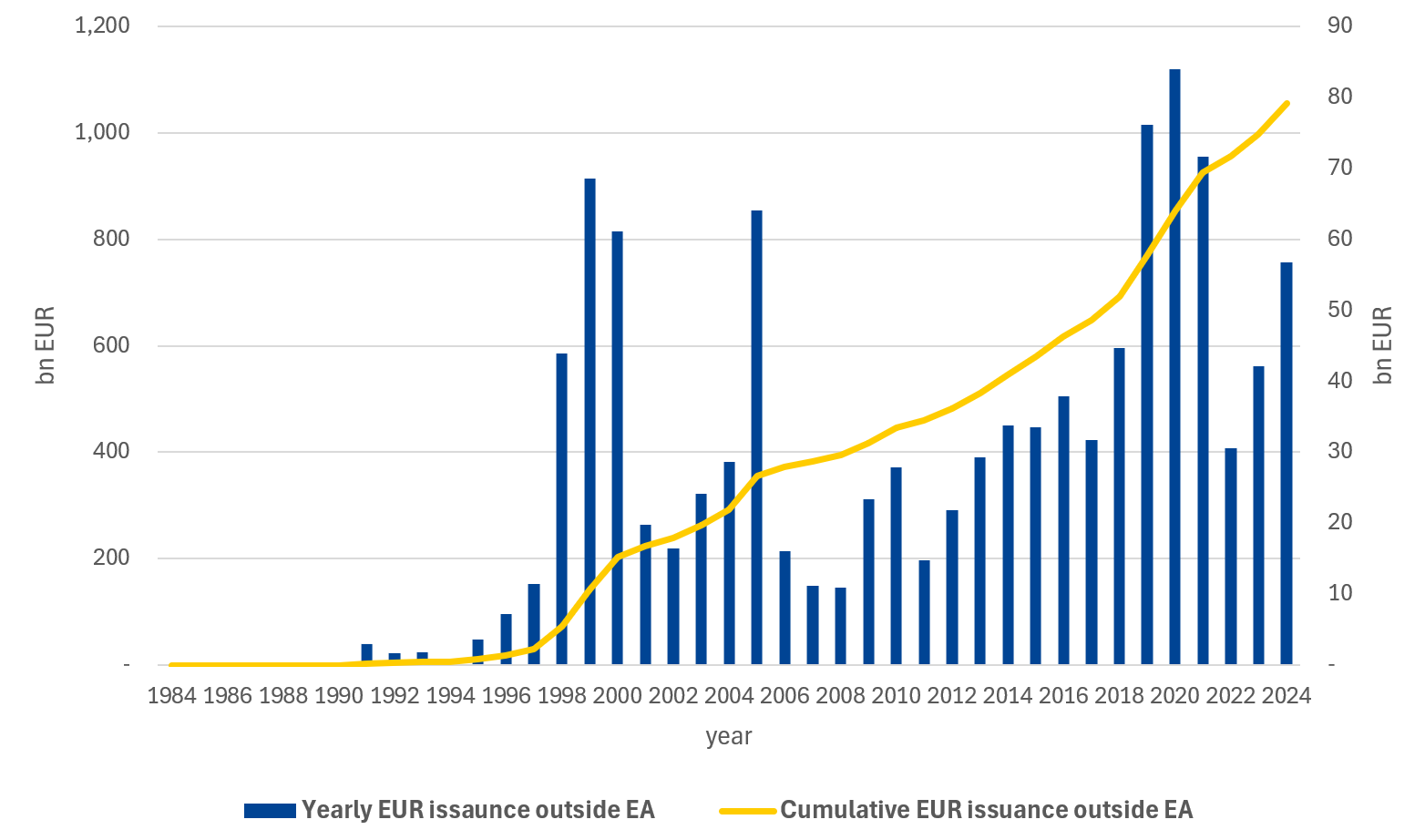

Cumulative euro issuance outside the euro area exceeded €1 trillion in 2024. Figure 1 below illustrates the fluctuations of yearly issuance outside the euro area, alongside cumulative issuance progress. Several factors contributed to these trends, as outlined below.

Figure 1: Yearly EUR issuance outside euro area

Source: ESM calculations based on Bloomberg Finance L.P.

It is noteworthy that even before the launch of the euro, some countries outside the planned euro area were issuing bonds in ECU (the currency account which was eventually replaced by the euro), albeit in relatively low amounts. By comparison, founding members of the euro area issued a cumulative €3.2 trillion worth of bonds in ECU before the EA's formation in 1999.[1]

Among euro area countries, Greece had a significant contribution to euro issuance outside the EA between 1998 and 2000. Greece’s inclusion in the euro area in 2001 caused a sharp decline in such issuance, as Greek bonds were subsequently classified as internal to the EA. This pattern repeated for other countries that joined the euro area after 1999.

The period leading up to the European Union's (EU’s) major enlargement in 2004 saw notable issuers from new EU Member States contributing significantly to euro-denominated bond markets. While Bulgaria and Romania joined the EU later in 2007, Romania gradually emerged as a dominant player among non-euro countries issuing debt in euros, particularly as it positioned itself as a candidate for future euro area membership.

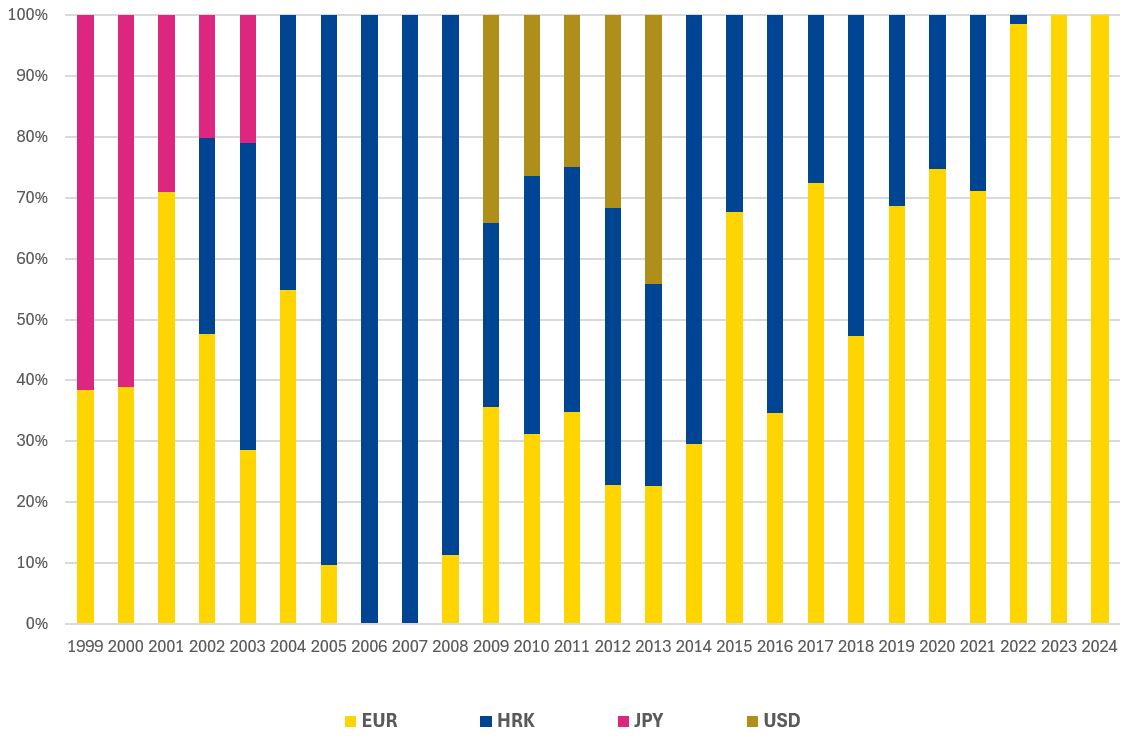

Croatia’s adoption of the euro on 1 January 2023 marked another milestone in this expansion. After joining the EU in July 2013 and fulfilling all convergence criteria, Croatia became the 20th member of the euro area. Figure 2 illustrates Croatia’s gradual shift toward full reliance on euro-denominated issuance following its entry into the euro area.

Figure 2: The currency composition of Croatia's yearly issuance on its way to euro adoption (2023)

Source: ESM calculations based on Bloomberg Finance L.P.

Issuance in euro is not restricted to European countries. For example, Argentina had a significant contribution to euro issuance outside the EA in 1999-2000 and most notably in 2005, when 60% of the issuance was related to the restructuring of its debt. Although Argentina has not accessed the euro market since 2020, it remains the second-largest issuer of outstanding euro-denominated debt outside the EA.

Financial conditions have also played a key role in shaping issuance trends. Between 2012 and 2022, very low or even negative interest rates in the euro area reduced borrowing costs for issuers. Concurrently, European Central Bank (ECB) asset purchase programmes limited the availability of European government bonds, prompting investors to seek alternatives such as non-euro area issuances denominated in euros. The peak of such issuance during 2020–2021 coincided with heightened government spending due to Covid-19-related healthcare and economic support programmes, alongside ECB’s Pandemic Emergency Purchase Programme (PEPP), which absorbed significant bond supply from within the euro area.

The decline in the issuance of bonds denominated in euro outside the EA observed in 2022 reflected reduced fiscal support measures, and to some extent the increased availability of European government bonds at higher yields following ECB policy normalisation. However, by 2024, demand for euro-denominated issuance outside the euro area rebounded due to relatively lower costs compared to USD or local currencies and potentially lower hedging costs for euro exposure versus USD.

With the increasing number of countries that want to join the euro area (Bulgaria expected next) and/or diversify their issuance, the popularity of the euro may increase. The presence of new issuers (e.g. Uzbekistan, which entered the euro-denominated bond market in 2024), as well as previously less frequent issuers such as Saudi Arabia and Philippines in the euro market was notable in 2025.

The benefits of issuance in euro

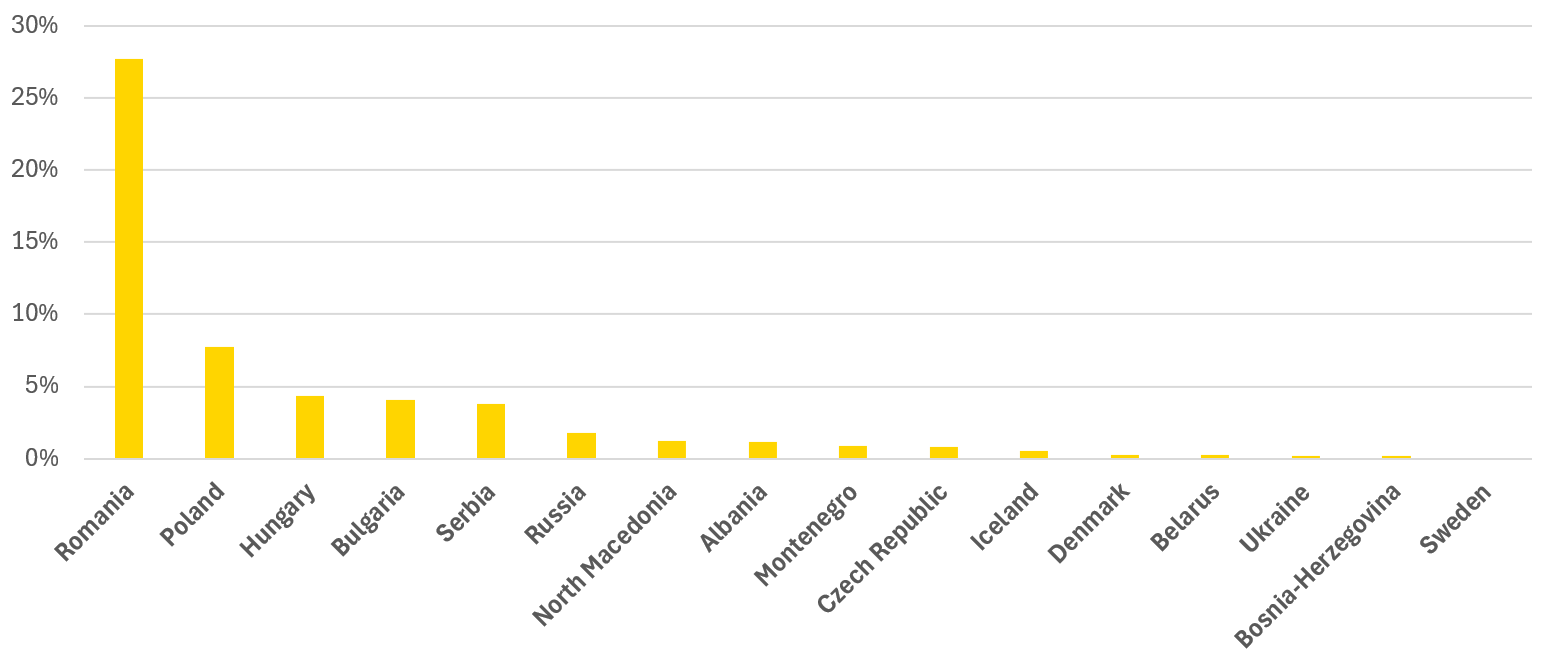

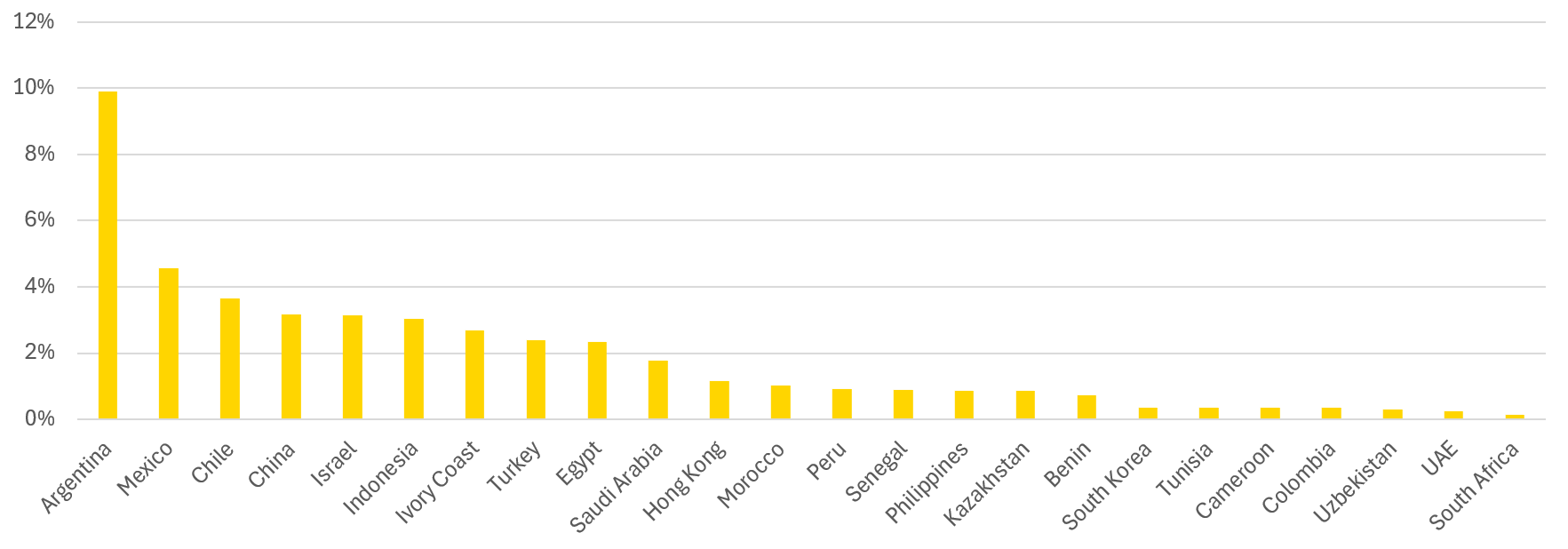

The outstanding amount of euro-denominated bonds issued outside the euro area is approximately €400 billion. Geographically, most euro-denominated bond issuers outside the EA are based in Europe, accounting for around 56% of the outstanding debt (Figure 3), while the remaining 44% are from outside Europe. Of this 44%, the Americas represent 19%, the Middle East and Africa 18%, and Asia 7% (country split in Figure 4).

Sovereigns are motivated to fund part of their debt in euro when they have important economic linkages with the EA or EU and/or a significant share of their international trade is denominated in euro. The higher a country’s economic ties to the EA, the more logical it becomes to issue in euro. However, there are additional rationales behind this decision.

Figure 3: 56% of the outstanding euro-denominated debt outside euro area (€400 bn) is with non-euro European countries

Source: ESM calculations based on Bloomberg Finance L.P.

Figure 4: 44% of the euro-denominated outstanding debt outside the euro area (€400 bn ) is issued by non-European countries

Source: ESM calculations based on Bloomberg Finance L.P.

One of the major benefits of euro issuance has been the cost of funding. This is often measured as the yield differential between United States (US) and euro area yields e.g. the yield of a 10-year US Treasury bond minus the yield of a 10-year German government bond. Many issuers see the interest rate differential as a good measure of costs and hence prefer to pay lower euro coupons.

However, the cost of funding extends beyond the interest rate differential, since the main risk arising from funding in a foreign currency comes from foreign exchange (FX) side. This is because the volatility of FX has a higher impact on the value of the debt relative to the volatility of interest rates. Yet the cost of hedging the FX exposure becomes irrelevant when issuers decide not to hedge for various reasons: i) in the case of short term funding, FX risk can be deemed bearable for a short period of time; ii) when funding in euro is below target or strategic weight envisaged by the debt management strategy; or iii) simply when the hedging costs are too high.

Other equally important benefits of issuing in euro extend beyond funding costs. One such benefit is diversification, where issuers can gain the following advantages:

- Access to a wider investor base: Euro-denominated bonds attract investors from the euro area who may face restrictions on investing in securities denominated in other currencies. The ESM established a US dollar programme in 2017 for the same reasons.

- Increased appeal to environmental, social and governance (ESG) investors: Europe has taken a leading role in ESG investing, supported by robust regulatory frameworks. Issuers tapping into this market can benefit from increased demand for green or sustainable bonds. For example, Saudi Arabia issued its inaugural green bond denominated in euro in February 2025 alongside a conventional bond.

- Access to a broader maturity range: The euro market offers access to a broader range of maturities compared to other markets, with tenors such as 10-year, 7-year, and 5-year bonds being particularly popular among non-euro area issuers.

In addition, issuance in euro can avoid crowding out their domestic markets when local investors cannot absorb all the supply. This strategy supports diversified funding mixes and can even create scarcity for an issuer’s bonds denominated in other currencies.

Finally, sovereigns may also issue euro-denominated benchmark bonds to pave the way for corporates seeking access to international markets.

Conclusion

Since its launch in 1999, the euro has established itself as a viable alternative to the US dollar, gaining traction as a funding currency both within and outside the euro area. While the majority of euro-denominated issuance occurs within the euro area, issuers outside it have increasingly recognised the benefits, including lower funding costs, diversification opportunities, and alignment with ESG priorities. This trend underscores the growing international role of the euro in global financial markets.

For the ESM, this development is particularly relevant. By issuing euro-denominated bonds, the ESM supports its mandate to ensure financial stability in the euro area while reinforcing trust in euro-denominated markets. The internationalisation of euro issuance further strengthens the euro’s position as a global reserve currency, enhancing resilience and stability in times of economic uncertainty.

Acknowledgements

The author would like to thank Kalin Anev Janse, Sarah Fouqueray-Carrick and Stephane Vincent for the valuable discussions and contributions to this blog post, Karol Siskind for the editorial review, and Edmund Moshammer and Peter Lindmark for the graphics.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager