Financial stability and risks to growth in the euro area: where do we stand?

Over the coming years, the current tightening of financial conditions could diminish the financial vulnerabilities coming from high asset prices that built up during the period of low interest rates. But there are short-term risks, as recently seen when some banks outside the euro area fell upon troubled times, triggering financial market turmoil that also impacted the euro area.

In this blog, we use a so-called “growth-at-risk” analysis to study the evolution of financial conditions and vulnerabilities in the euro area and compare the severity of risks across three different points in time. We found that while short-term risks to the economy remain high, the ongoing correction of asset prices should reduce vulnerabilities in the medium term. With its more robust institutional architecture of today, the euro area is better equipped to cope with short-term risks than in the past. Still, further progress in improving the resilience of its financial sector is needed.

Financial conditions in the euro area, favourable before the war in Ukraine…

Favourable financial conditions, including sufficient access to loans for businesses and households, are crucial for the growth and maintenance of a healthy economy. However, cheap credit may lead to higher debt levels and drive up asset prices, creating vulnerabilities and potentially leading to rapid but unsustainable growth. The global financial crisis of mid-2007 to early-2009 is such an example. Vulnerabilities materialised, pushing many countries into deep and protracted recessions. Back then, policymakers had only begun to heed financial conditions when assessing risks. For such risk assessments, indices of financial conditions are a simple tool used to summarise the information contained in various financial variables.

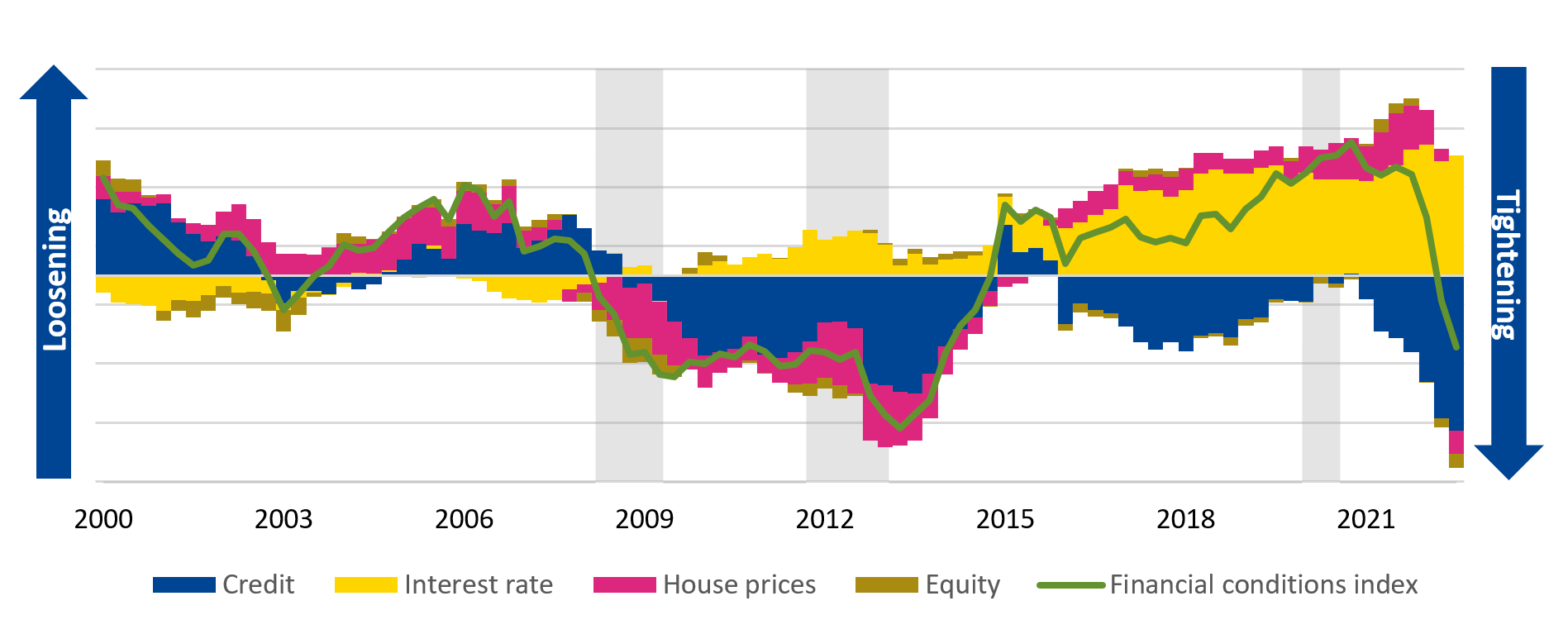

Our simple financial conditions index – which includes credit, an interest rate, housing prices, and equity prices, all adjusted for inflation[1] – suggests that euro area financial conditions before the war in Ukraine were at least as loose as before the global financial crisis (Figure 1), but the driving forces were very different. Following the European debt crisis and subsequent recession, the economy recovered but inflation and interest rates remained low. The large-scale asset purchases by the European Central Bank pushed down borrowing costs further. The policy response to the pandemic (for example, public loan guarantees) accentuated this trend: debt levels increased, and asset prices – particularly for real estate – rallied.

Figure 1: Euro area financial conditions 2000 – 2022

Notes: This figure shows a financial conditions index for the euro area. The index is the first principal component of real equity returns (year-on-year), real credit growth (year-on-year), real (short-term) interest rate, and real house price growth (year-on-year), extracted over the period 1971:Q1–2022:Q3. For periods where the aggregate euro area components are not available, these were constructed as gross domestic product (GDP)-weighted averages of the four largest countries (France, Germany, Italy, and Spain). For the euro area interest rate since 2004:Q3, we include the so-called shadow rate as computed in Wu and Xia (2017, 2020). The signs of the variables’ contributions are such that an increase indicates a loosening of financial conditions. Shaded grey areas indicate recessions.

Source: ESM calculations based on Bank for International Settlements, Organisation for Economic Co-operation and Development, and Wu and Xia (2017, 2020)

…are tightening rapidly

More recently, this trend reached a turning point, accelerated by the war in Ukraine. Inflation has risen sharply, prompting the European Central Bank to tighten monetary conditions at the fastest pace seen since the introduction of the euro. Equity prices and credit in real terms fell, while house price growth has started to ebb.

Thus, the reasons for tighter financial conditions are different from those of the global financial crisis. The euro area faced several external shocks that acted as side effect impacts on asset markets, while the bursting of the credit and housing bubble during the global financial crisis was largely rooted in the European financial sector.

Short-term risks to growth are high, but medium-term risks lower as imbalances are fading

Factors such as the energy crisis, falling real incomes, supply-side bottlenecks, and weak external demand have dampened macroeconomic forecasts. Although the euro area has shown some economic resilience, policymakers remain concerned about the current tightening of financial conditions. Of course, the economy must respond to rising interest rates for inflationary pressures to subside.

Tighter financial conditions strain growth and signal additional near-term downside risk as credit flows to the economy dry up and asset prices moderate or even fall, negatively affecting investors and the financial sector. While in the medium term, tightening financial conditions and corrections of asset prices reduce risks as previous vulnerabilities diminish, the recent troubles of several banks highlight that these adjustments can give rise to more extreme events in the short run.[2] These can cause financial instability and a potentially sizeable deterioration of economic growth.

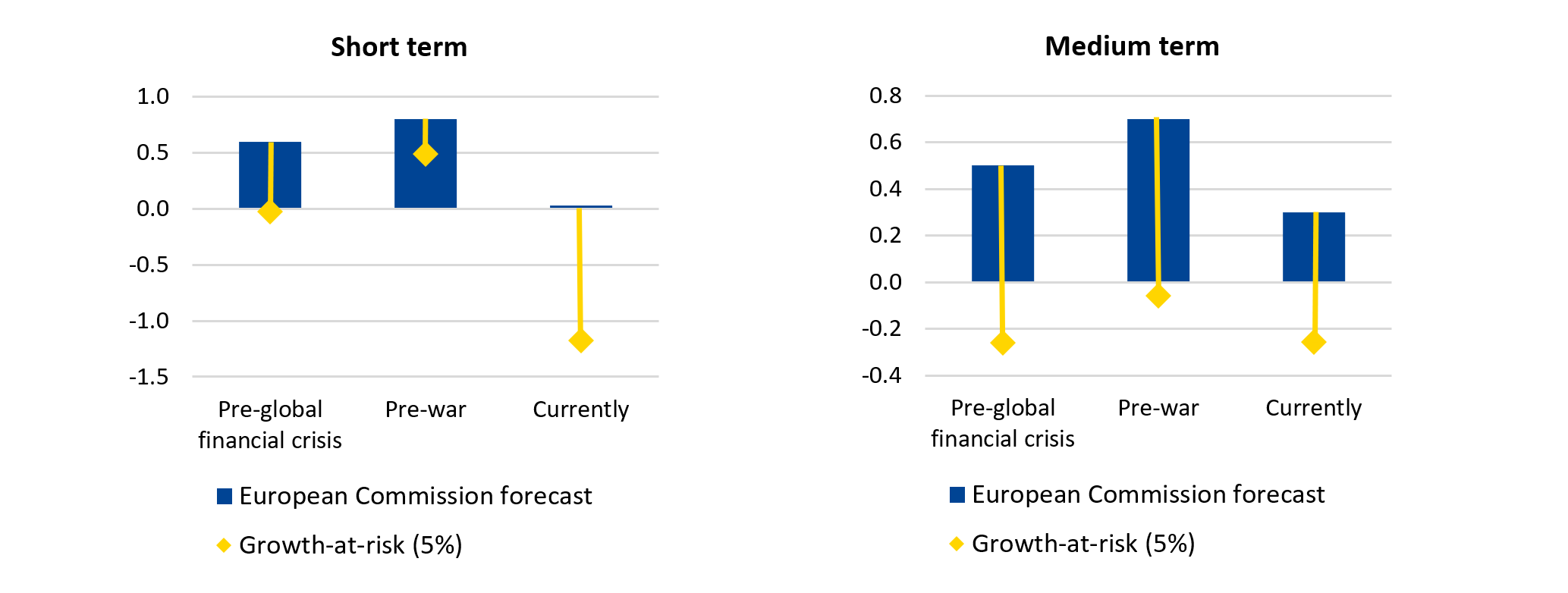

As part of our analysis, we link financial developments to risks for the economy using the recently popularised “growth-at-risk” methodology.[3] This approach allows us to assess the impact of changing financial conditions on the severity of a worst-case GDP-growth scenario.[4] We examine risks to the economy at three different points in time: before the global financial crisis (2006:Q3); prior to the war in Ukraine (2021:Q3); and the latest period for which our financial conditions index is available (2022:Q3).

We find that the current tightening of financial conditions signals sizeable downside risk for the economy in the next quarter (Figure 2, left) and that the economic slowdown[5] could be deeper than expected. Such short-term risks are likely to persist in the coming months, as European economies adjust to the changing global monetary-policy cycle. These risks to growth are larger compared to both the pre-global financial crisis and pre-war times – while we have already seen some financial disruption, in those pre-crisis times such turmoil had yet to unfold.

Figure 2: Euro area GDP growth forecasts and risks

(real average quarter-on-quarter growth rates, in %)

Notes: This figure shows real GDP growth forecasts (1/8-quarter ahead) based on European Commission forecasts with “Pre-global financial crisis” data coming from the Autumn 2006 edition, the “Pre-war” data coming from the Autumn 2021 edition, and the “Currently” data coming from the 2023 Winter edition. The forecasts start with the last quarter of the respective year (Q1 in case of 2023). The growth-at-risk estimates for 1/8-quarter-ahead (average) quarterly growth are based on data until Q3 of the respective years and built using quantile regressions (Adrian et al., 2019) including a constant, current growth, and the financial conditions index shown in Figure 1. The growth-at-risk estimates are centred around the European Commission forecasts. The estimation sample is 1971:Q1–2019:Q4 and euro area GDP growth prior to 1995:Q2 is taken from the European Central Bank’s area-wide model.

Source: ESM calculations based on European Central Bank, European Commission, Euro Area Business Cycle Network, Bank for International Settlements, Organisation for Economic Co-operation and Development, and Wu and Xia (2017,2020)

The picture is quite different when looking at a two-year horizon (Figure 2, right). Today, the economic outlook for the next two years is more pessimistic compared to the pre-global financial crisis and pre-war periods. This is partly because the impact of tighter financial conditions is embedded in the forecasts.[6] Despite the different drivers of financial conditions in these two periods, medium-term risks to growth expectations were comparable. By contrast, current medium-term risks – relative to official forecasts – are lower. In other words, the unwinding of financial asset prices we have experienced should leave us less vulnerable in the coming years.

The euro area boasts improved economic and financial resilience, but further progress needed now

Using the “growth-at-risk” approach, our analysis does not explicitly account for the resilience built into the financial sector. Since the global financial crisis, much progress has been made in fortifying the euro area economy and its financial sector.

The banking sector is able to better face today’s challenges due to improved regulation that required the build up of buffers. Moreover, the institutional architecture of the euro area has been strengthened, with the euro area’s rescue fund, the ESM, being one cornerstone of this.

Recent events remind us that additional work remains to be done to further reduce financial sector vulnerabilities and limit spillovers to the economy. Most importantly, work is needed on the completion of banking union and on progressing in the regulation and supervision of the non-banking financial sector. In the future, these institutional features could help member states better cope with a combination of multifaceted shocks.

Acknowledgements

The authors would like to thank Anabela Reis, Raquel Calero and Niels Hansen for valuable comments and contributions to this blog post.

Further reading

Boyarchenko, N., Crump, R., Elias, L., and Lopez Gaffney, I., “What Is “Outlook-at-Risk?”, Federal Reserve Bank of New York Liberty Street Economics, February 2023.

International Monetary Fund, “Financial Conditions and Growth at Risk”, Global Financial Stability Report (Chapter 3), October 2017.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager