Ageing and demand for safe assets in the euro area

ESM Briefs is a concise presentation of research by ESM staff members, helping readers better understand and navigate current economic policy debates. More about ESM Briefs

Abstract

Will ageing societies in Europe lead to a new savings glut? To address this potential consequence of demographic change, we assess the relationship between population ageing and safe assets in the euro area, using data from the Eurosystem's Household Finance and Consumption Survey (HFCS). Our findings indicate that ageing is unlikely to lead to a structural shift in the demand for safe assets. The share of safe assets in household portfolios remains relatively stable across most of the age distribution, with only a slight increase among the oldest households. Projections based on demographic forecasts for 2050 point to a marginal change in aggregate demand for safe assets. Our results challenge the narrative that ageing will structurally increase the amount of savings and highlight the need for a nuanced understanding of demographic impact on financial markets and the broader economy.

Acknowledgements: The authors would like to thank Rolf Strauch and Clara Martinez-Toledano for advice and guidance, Nika Khinashvili for research assistance, and Karol Siskind for editorial support.

Ageing as a driver of savings and equilibrium real interest rates

European populations are ageing rapidly. Today, the median age in the euro area is around 45 years. Based on current projections, it will rise to 48 years by 2050. Although an increase of three years may not sound like much, it is in fact indicative of a tectonic shift in our economic system: consider that the ratio of workers to retirees is 3 to 1 in the euro area today, but this ratio will decline to 2 to 1 over the same period. These demographic changes will have profound economic implications.

Ageing is often mentioned as a critical determinant of real interest rates that will prevail over the long run (BIS, 2024 and Schnabel, 2024). Ageing is thought to affect the balance between savings and investment. The first issue of ESM Briefs explored one side of this relationship, analysing how ageing can influence the overall demand for investment, illuminating in particular the link between innovation and investment.

In this issue of ESM Briefs, we will take a closer look at the other side the balance: savings. Goodhart and Pradhan (2020), for example, argue that a large elderly cohort will soon enter retirement and start running down wealth—effectively dissaving (particularly in China and Europe). In contrast, Cesa-Bianchi et al. (2023) emphasise that people tend to live longer, leading to longer spells of retirement. To protect their living standard over a longer period without labour income, people will tend to save more.

An important insight from the work on household portfolio choice is to distinguish between savings in risky and safe assets (see Gomes, 2020). The optimal allocation between these two asset types changes with age: as households age, their investment horizon shortens, and the relative weight of labour income declines, while expenditures in old age loom larger. Ageing will determine the demand for safe assets and, by implication, also the natural interest rate if this process leads to a structural change in the portfolio share allocated to safe assets.

We therefore centre our analysis on the share of safe assets in a household’s total assets. Safe assets include deposits, bonds, life insurance and voluntary pensions (see Arrondel et al., 2016; and Fagereng et al., 2020). Before proceeding, recall that safe assets made up about one-fourth of the total stock of household savings in 2021 (we use the terms ‘stock of savings’, ‘total assets’, and ‘total wealth’ interchangeably).

Our overarching question is whether—all else equal—the ageing of society will lead to a structural increase in the relative demand for safe assets. To provide an answer, we proceed in three steps, taking smaller sub-questions at a time:

- Are the asset portfolios of older households structurally different compared to younger households (do they hold higher shares of safe assets)?

- How large is the marginal impact of age on households’ share of safe assets when considering other household characteristics that may be systematically related to age (such as education, marital status, income, house ownership status)?

- Using population projections for the year 2050 – and relying on the results of points 1 and 2 - how will ageing affect the share of safe assets for each household?

- What do these age-related changes in household safe asset shares imply for macroeconomic aggregate demand for safe assets?

Household surveys contain detailed information but need careful treatment

Our analysis is based on the stock of savings by household in the euro area using the Eurosystem's Household Finance and Consumption Survey (HFCS). The HFCS provides detailed information about households' assets and liabilities for all euro area countries. It is designed to be representative of the overall population. We use the most recent instalment of the HFCS collected in 2021 (HFCS wave 4).

Household surveys are popular tools to glean insights into the distribution of income and wealth, but they contain important gaps in the tail of distributions. Most notably, despite its careful design, the HFCS tends to underreport assets held by the richest households (Waltl and Chakraborty, 2022). We close these gaps by rescaling wealth components (such as deposits) in the HFCS to match the totals from the quarterly sector accounts (QSA), compiled in line with the standards of the European System of Accounts (ESA 2010). Our approach tracks closely the numbers from the ECB’s Distributional Wealth Accounts. [1]

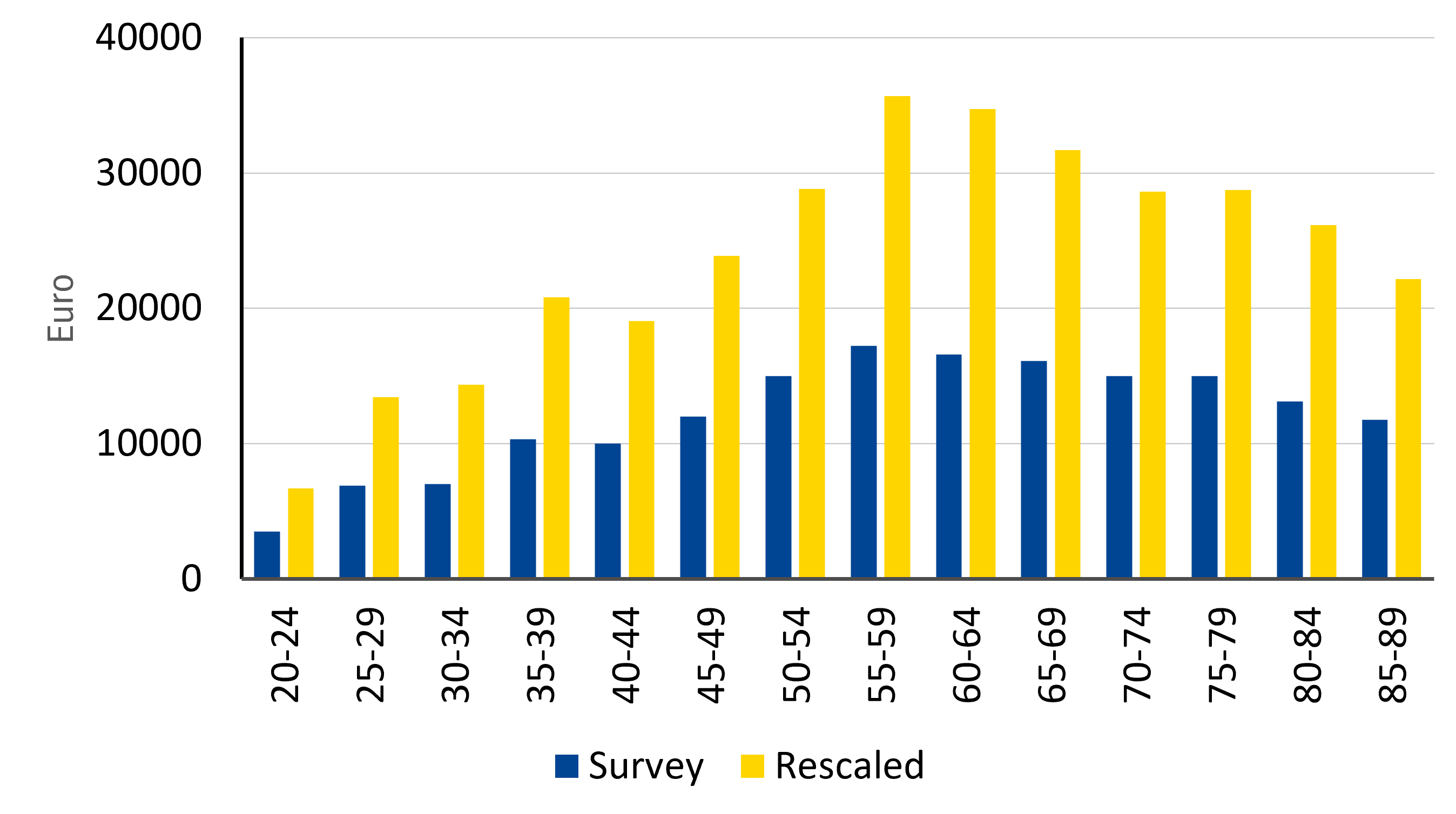

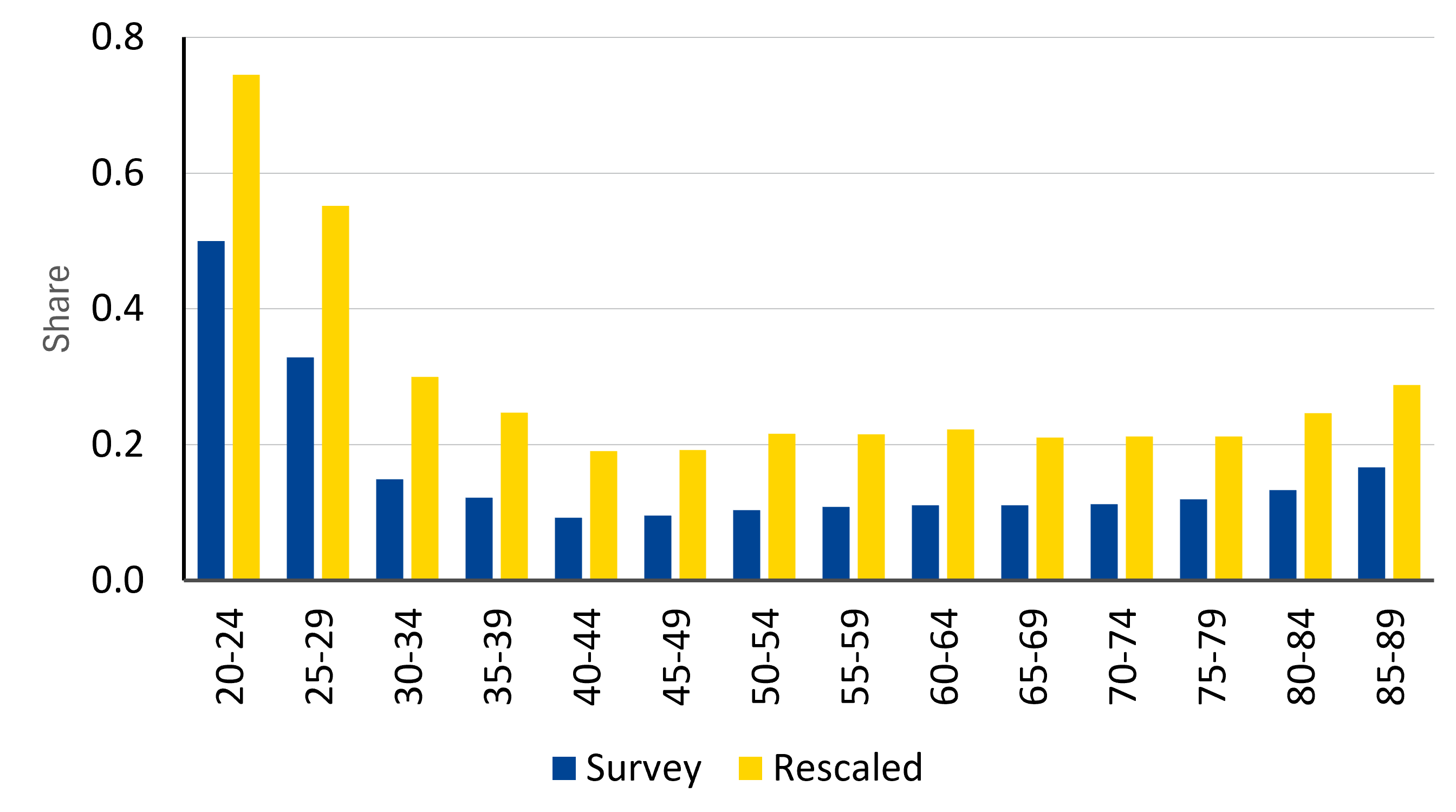

Figures 1 and 2 show the median value of safe assets by age bracket and the associated share of safe assets in households’ overall asset portfolios. Comparing the raw data in the HFCS with our rescaled data reveals two stylised facts: (i) rescaling significantly increases safe assets for all age brackets, indicating a significant gap in coverage of safe assets in the HFCS; and (ii) the share of safe assets is highest for the young, which mostly reflects a low denominator—young people do not have significant assets. From age 35 onwards, however, the share of safe assets is relatively stable until old age.

One immediate upshot of this stylised fact is that as households move into older age brackets, they seem unlikely to disproportionately increase their savings held in the form of safe assets, at least when we compare safe assets to households’ overall asset portfolio. Although this idea is consistent with some existing studies that also find a muted role of age in explaining the composition of households’ asset portfolios (Christelis et al., 2013 for an international perspective and Mian et al. 2021 for the US), it bears further examination to account for third factors like education and income.

Figure 1: Value of median safe assets by age bracket across the euro area

Note: The chart shows the median safe asset holdings per age bracket for all euro area households in the HFCS. The blue bars show the median of the HFCS raw data, and the yellow bars show the median of the data rescaled to match national account aggregates from the Quarterly Sector Accounts.

Figure 2: Safe asset share (in total assets) by age bracket in the euro area

Note: The chart shows the median safe assets share (safe assets/total assets) for each age bracket, using all euro area households in the HFCS. The blue bars use HFCS raw data, and the yellow bars use our rescaled data.

Age does affect household holdings of safe assets, but they are relatively uniform until old age

To investigate the impact of age on the composition of household saving portfolios, we use multivariate regressions. We estimate a fractional logit model to explain the safe asset share, using a standard set of household characteristics as control variables (age, income, total wealth, gender and so on).[2] In addition, as we pool all households in the dataset, we account for cross-country heterogeneity by including country-fixed effects in our regressions.

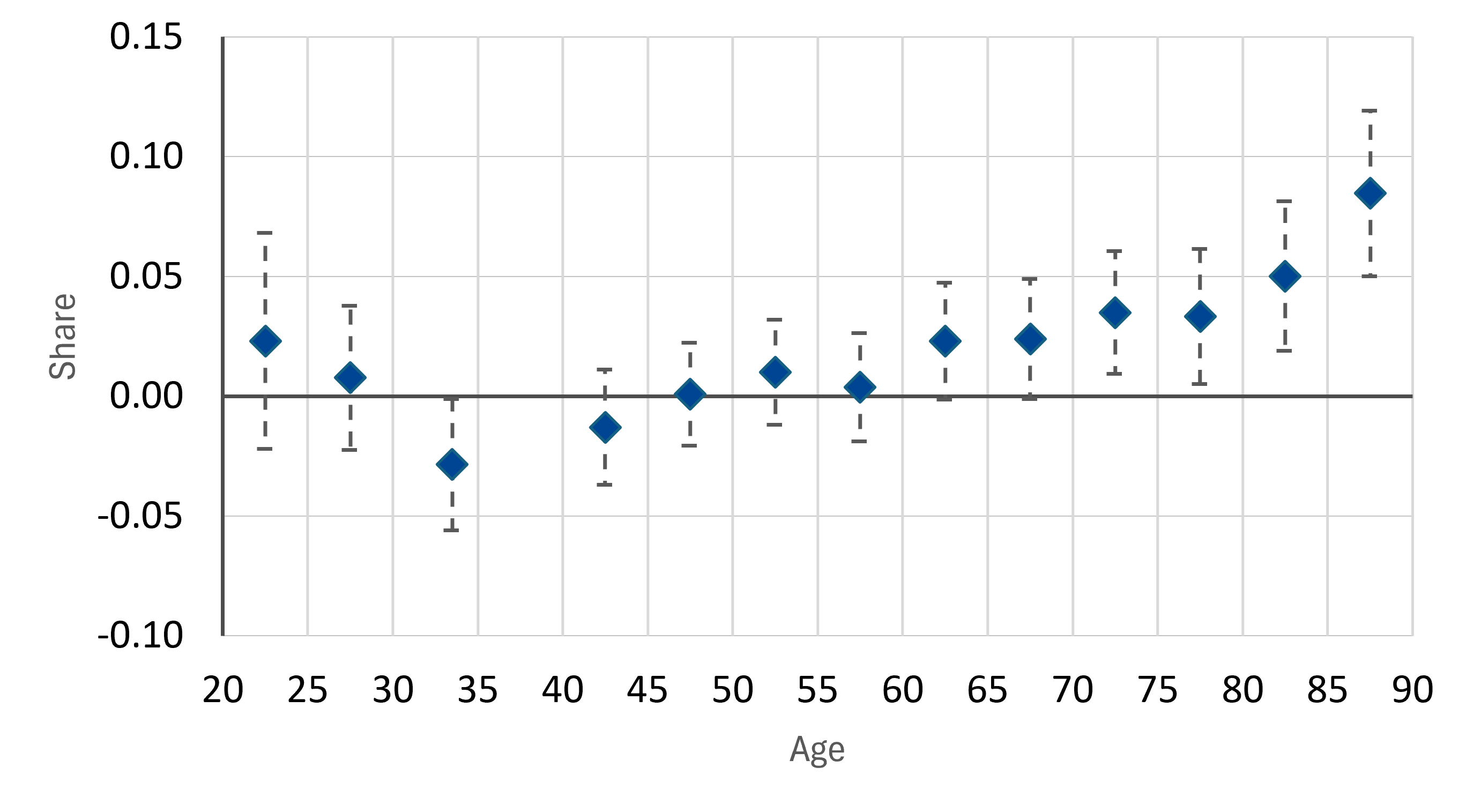

Figure 3: Average marginal effect of age brackets on the safe asset share

Note: The chart shows the average marginal effect of each age bracket on the share of safe assets in households’ asset portfolios. The marginal effect is from the fractional logit model of households’ safe asset shares. The base category is 35-39-year-olds. The markers show point estimates and the dotted lines show the 95% confidence interval.

Figure 3 displays the average marginal effect of age on the safe asset share across the age distribution. We measure age as a series of dummy variables that are equal to 1 if the head of the household is in the relevant age bracket. The coefficients are expressed as the differential to the safe asset share of 20-24-year-olds, which are the base category.

The average effect on the safe asset share clusters around zero and is generally statistically insignificant. Interestingly, and consistent with our visual inspection of the age-safe asset distribution above, the marginal impact of age does not change much between the age of 30 and 69. Only people from the age of 70 appear to start investing a greater share of their savings in safe assets compared to middle-aged households, although the size of the effect is relatively small: households in the 80-84 age bracket are predicted to have safe assets share that are on average 0.05 percentage points larger. This effect would lift the safe asset shares of households in the 80-84 age bracket to approximately 30%, remembering that the median share of the 35-39-year-olds is approximately 25%; see Figure 2).

Ageing would have only small aggregate effects on the aggregate household savings

We now turn our gaze into the future to project safe asset holdings for the euro area with an ageing population. To this end, we use population projections for the year 2050 for every euro area country. We use Eurostat’s EUROPOP2023 projections, which are the standard source for European demographic projections. Recall that the median person of the euro area will be older by three years, but the total number of people will be about the same as today (in part due to immigration). We therefore focus on the changes in the relative weights of each age bracket, abstracting from changes in the number of households.

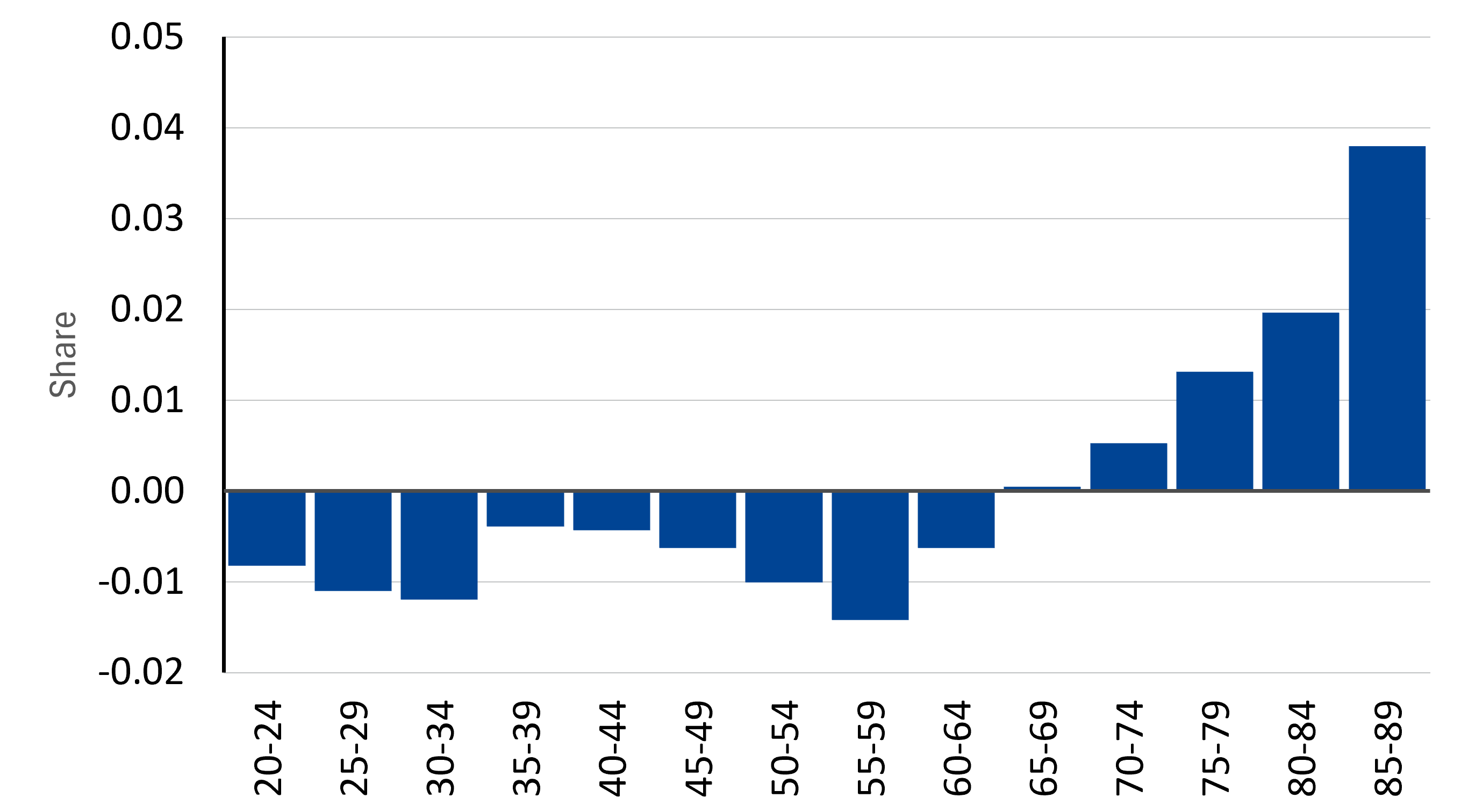

Figure 4 shows the change in the relative weight of each age bracket, noting that the change across all age buckets sums to zero. All age brackets up to 64 will be relatively smaller in 2050, offset by corresponding increases in the relative size of the 65+ age brackets.

To project safe asset holdings in the year 2050, we first assign a new age to each household. We rank all households in each country by their original age. Using the age bracket weights from 2050, we calculate the number of households in each bracket consistent with the population projections. We keep a fraction of households in their original bracket until they reach the size limit of the bracket, bumping up the remaining households into the next bracket. We repeat this exercise until we reach the final age bracket of 85-89 years. This method keeps the ranking of the household sample intact but respects the structure of the overall population in 2050.

Given this new distribution of age across households, we can proceed to predicting a new share of safe assets, using the results of our fractional logit model. Note, however, that the share of safe assets is not sufficient to predict nominal safe assets in the aggregate. To get there, we need one more input: the evolution of total assets. We make the most straightforward assumption possible: we assume that the wealth-to-income ratio for each country remains stable until 2050. Total income of each country in the year 2050 is easy to calculate, using long-run potential growth estimates from the European Commission’s Ageing Report and the ECB’s medium-run inflation target of 2%. Total assets at country-level are then proportional to the country’s wealth-to-income ratio. At the level of the households, total assets grow at the same rate as total assets for the entire country.

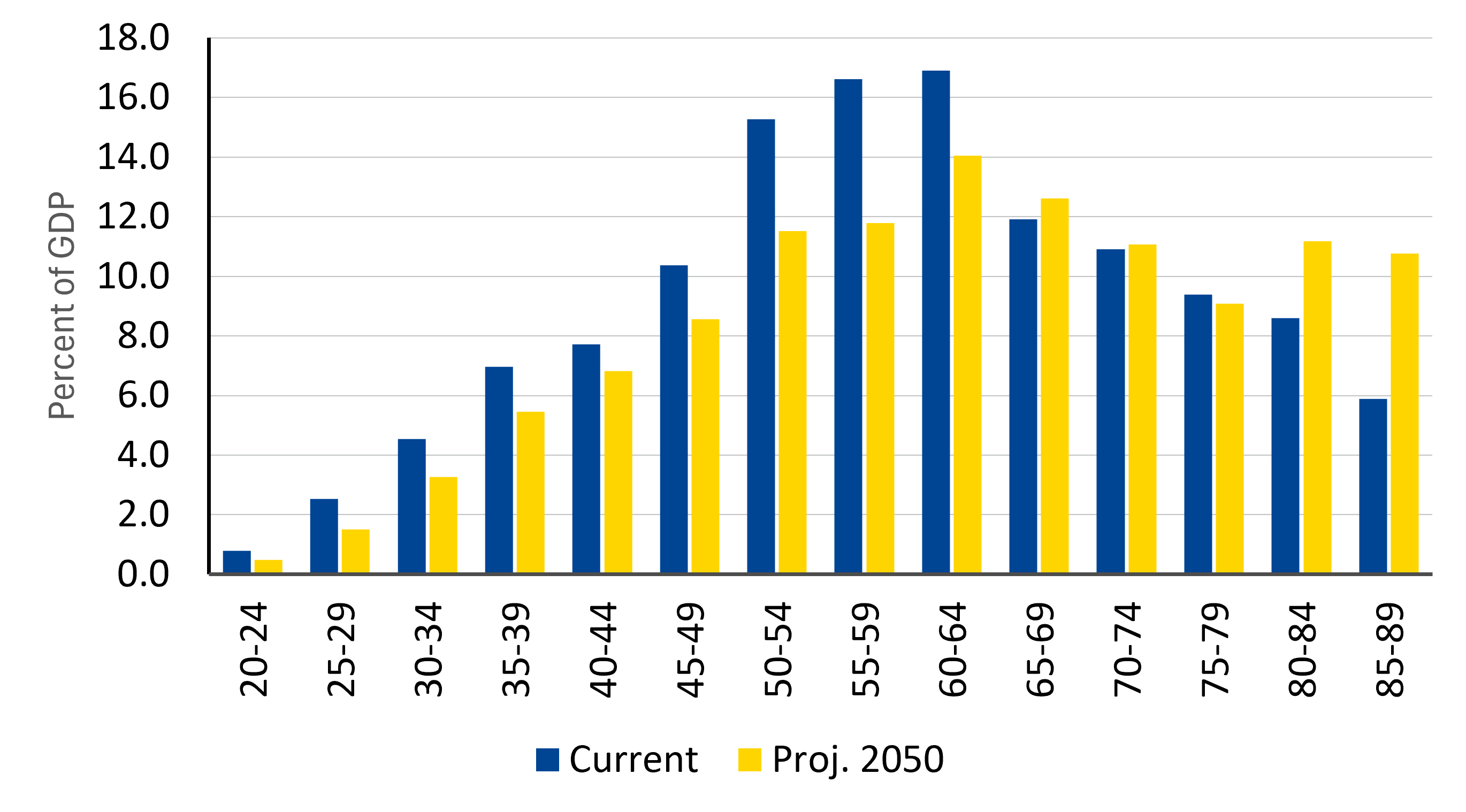

Equipped with simulated safe asset shares and total assets, we are finally able to generate a household-specific prediction of nominal safe assets. Figure 5 shows the result of this projection, expressing aggregate safe asset holdings in each age bracket as a share of GDP. It is obvious that total safe asset holdings by the young and middle-aged will decline, as there will be fewer households in this age bracket. But this decline is offset by larger safe asset holdings by older households, again mostly because of their larger number. In aggregate, the declines and increases almost perfectly cancel each other out: aggregate safe asset holdings are €16 trillion, about 126% of euro area GDP in 2021. In 2050, assuming a constant wealth-to-income ratio, safe assets will increase to €41 trillion. Despite the large increase in nominal amounts, safe assets as a percentage of GDP decline to about 118% of euro area GDP, driven by the relative decline of the 50–60-year-olds, who have the largest holdings of safe assets.

Figure 4: Change in relative share of each age bracket between now and 2050

Note: The chart shows the difference in weights of each age bracket between the projected 2050 age distribution and the 2021 age distribution as captured by the HCFS. A negative (positive) value implies that a given age bracket will be relatively smaller (bigger) in 2050 compared to 2021.

Figure 5: Total nominal safe asset holdings for each age bracket now and in 2050

Note: The chart shows the nominal aggregate safe assets for each age bracket, in percent of GDP. The blue bar shows predicted aggregate safe assets using our fractional logit model under the current age distribution. The yellow bars use the 2050 age distribution to predict safe asset shares for every household. This exercise assumes that total assets (wealth) as a share of total income (GDP) remain constant between now and 2050.

Conclusion: ageing on its own is unlikely to lead to a structural increase in the demand for safe assets in the euro area

Our analysis of detailed household balance sheet data in the euro area suggests that population ageing is unlikely to cause a large-scale shift in the demand for safe assets. This result assumes that household preferences remain as they are today and that total assets in the economy evolve in line with nominal income growth. Fewer young and middle-aged households imply less demand in aggregate from this part of the age distribution, offset by more demand from older households (who will be more numerous).

These findings have important implications for thinking about how to mount effective responses to the other megatrends affecting Europe in the 21st century, particularly climate change and geoeconomic fragmentation. The stability in safe asset demand across age groups suggests that concerns about a wave of dissaving and asset price meltdowns due to population ageing is not imminent, at least in the European context. At the same time, it also seems a stretch to assume that a permanent increase in public financing needs (due to structurally larger fiscal deficits) would be largely offset by higher savings from an ageing population (see Carvalho et al. 2016, for example).

Our findings also inform the debate about the future path of neutral real interest rates. Rather than a secular downward pressure driven by an ageing-related “savings glut”, the level of neutral rates may mostly depend on other structural forces, such as technological change and investment needs.

Our exercise focuses specifically on the direct effect of ageing on safe asset demand, all else equal. Ageing could affect the macroeconomy in a myriad of other ways, which we do not consider in this analysis: ageing can affect productivity and growth, as well as inequality, preferences, labour markets, capital flows, and bank credit. These changes could in turn feed back into changes in saving and asset demand through general (indirect) equilibrium effects, which we do not consider in our analysis.

Further research into other channels through which ageing affects the economy will be crucial for a comprehensive understanding of the economic implications of demographic change in the euro area. Additionally, more work is needed to understand why the breakdown of asset portfolios between safe and risky assets appears to differ as households grow older in Europe and other countries (for example, US households seem to systematically increase their safe asset share from the age of 50; see Vlieghe, 2021).

Further reading

Arrondel, Luc, Laura Bartiloro, Pirmin Fessler, Peter Lindner, Thomas Y. Mathä, Cristiana Rampazzi, Frédérique Savignac, Tobias Schmidt, Martin Schürz, and Philip Vermeulen. 2016. “How Do Households Allocate Their Assets? Stylized Facts from the Eurosystem Household Finance and Consumption Survey.” International Journal of Central Banking 12, no. 2 (2016): 129-220.

BIS (2024), “Quo vadis, r*? The natural rate of interest after the pandemic”, Quarterly Review, March.

Blatnik, Nina, Alina Bobasu, Georgi Krustev and Mika Tujula. 2024. “Introducing the Distributional Wealth Accounts for euro area households.” ECB Economic Bulletin, Issue 5/2024.

Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio. 2016. “Demographics and Real Interest Rates: Inspecting the Mechanism.” European Economic Review 88: 208-226.

Cesa-Bianchi, Ambrogio., Harrison, Richard, and Rana Sajedi. 2023. “Global R*”, Staff Working Paper, No 990, Bank of England, July.

Christelis, Dimitris, Dimitris Georgarakos, and Michael Haliassos. 2013. “Differences in Portfolios across Countries: Economic Environment versus Household Characteristics.” Review of Economics and Statistics 95, no. 1: 220-236.

Fagereng, Andreas, Luigi Guiso, Davide Malacrino, and Luigi Pistaferri. “Heterogeneity and Persistence in Returns to Wealth.” Econometrica 88, no. 1 (2020): 115-170.

Goodhart, Charles and Manoj Pradhan. 2020. “The Great Demographic Reversal,” Economic Affairs, Wiley Blackwell, Vol. 40, No 3, pp. 436-445.

Gomes, Francisco. 2020. “Portfolio Choice Over the Life Cycle: A Survey”. Annual Review of Financial Economics, Vol. 12, No. 1: 277-304.

Mian, Atif R., Ludwig Straub, and Amir Sufi, 2021. “What Explains the Decline in r*? Rising Income Inequality Versus Demographic Shifts,” Jackson Hole Conference Proceedings, 2021, (2021-104).

Vlieghe, Gertjan, 2021, “Running out of room: revisiting the 3D perspective on low interest rates”, Speech at the London School of Economics, London, 26 July 2021.

[1] The ECB makes conceptually similar but technically more demanding adjustments to the HFCS in its recently published Distributional Wealth Accounts dataset; Blatnik et al., 2024.

[2] ‘Safe asset share’ is equal to the sum of deposits, bonds and voluntary pensions and life insurance, divided by total assets.

Authors

Manager ESM Briefs