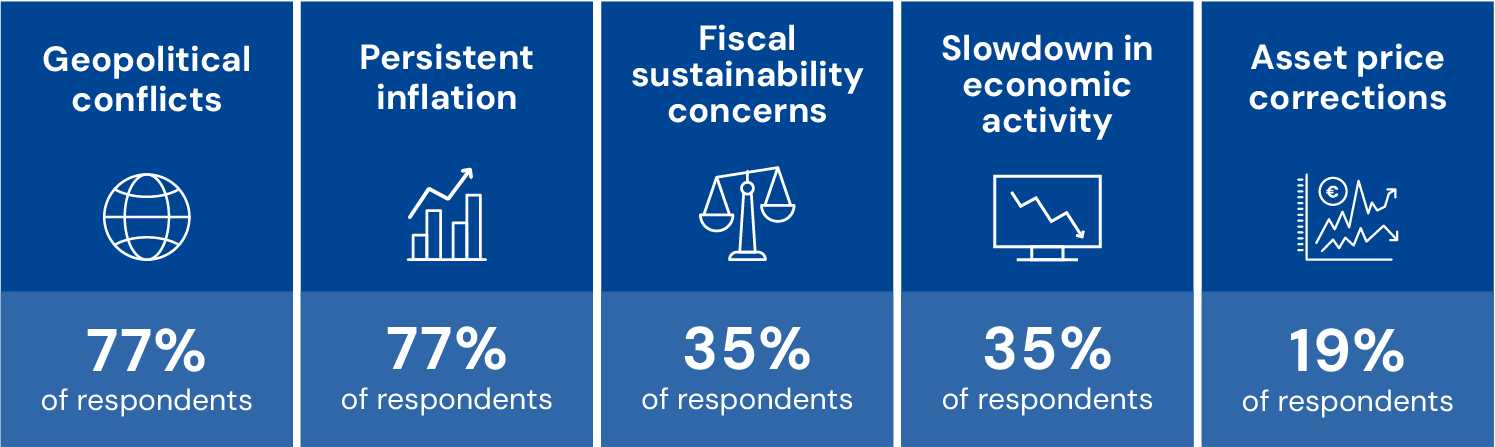

The euro area faces a volatile global environment, shaped by heightened geopolitical tensions and the ongoing global energy crisis.

- The economy enters this era with proven resilience, but it is not immune to external shocks: openness and energy dependencies leave it vulnerable and resilience is coming under strain.

- Under a baseline scenario (European Commission’s spring 2026 economic forecast), growth slows to 1.1% and inflation rises to 2.7% on average in 2026–2027, reflecting the impact of energy prices and a relatively swift normalisation of supply conditions.

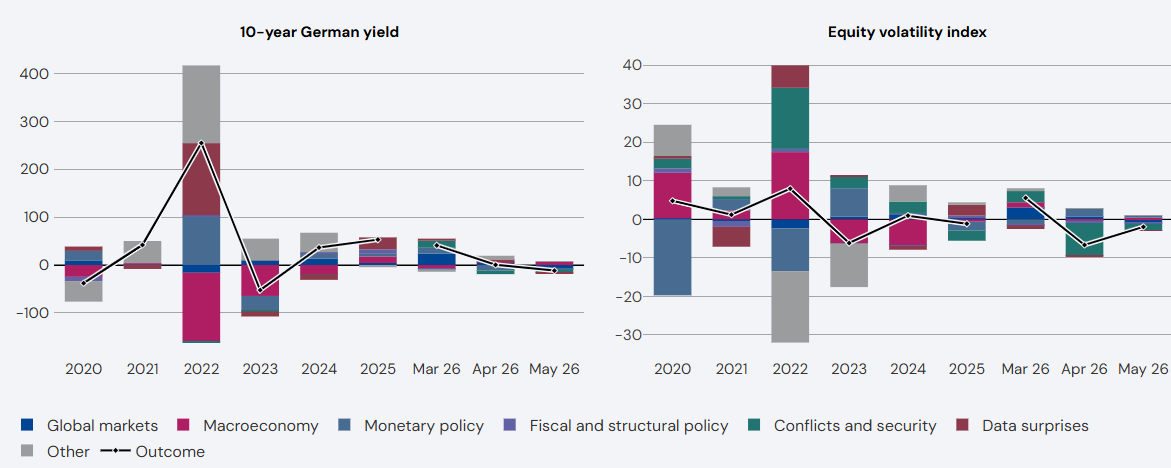

Two external risks dominate the outlook and could reinforce each other through real, confidence, and financial channels.

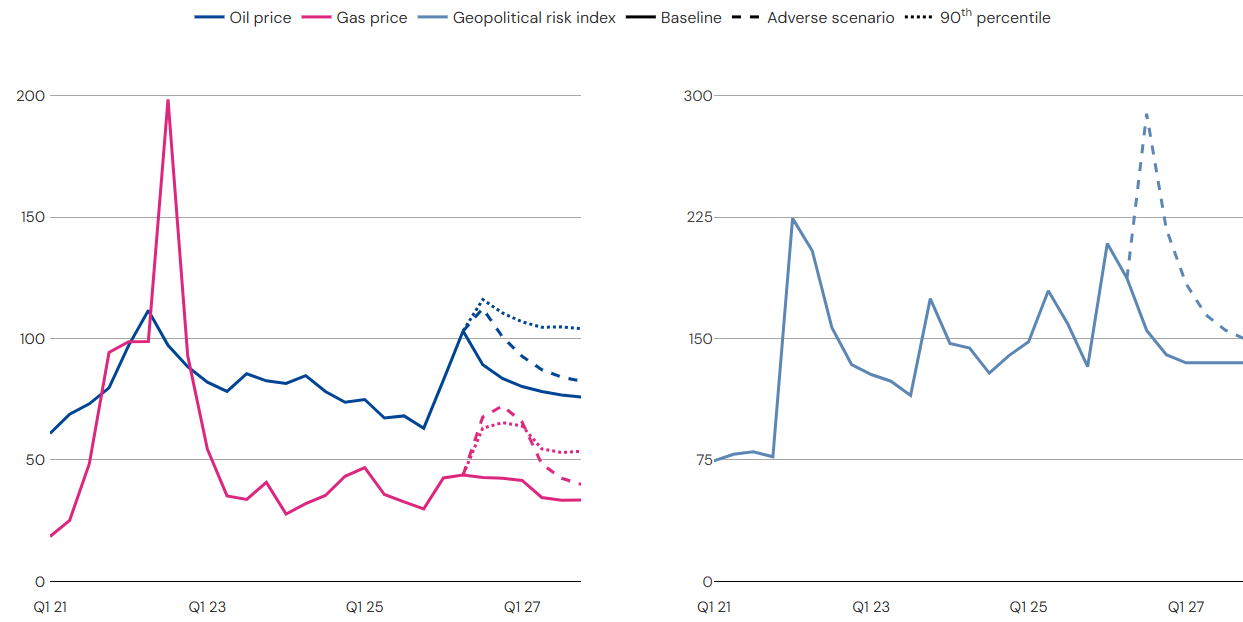

- Prolonged geopolitical tensions and re-escalation in the Middle East could intensify supply disruptions and energy price pressures, resulting in second-round effects and heightened uncertainty.

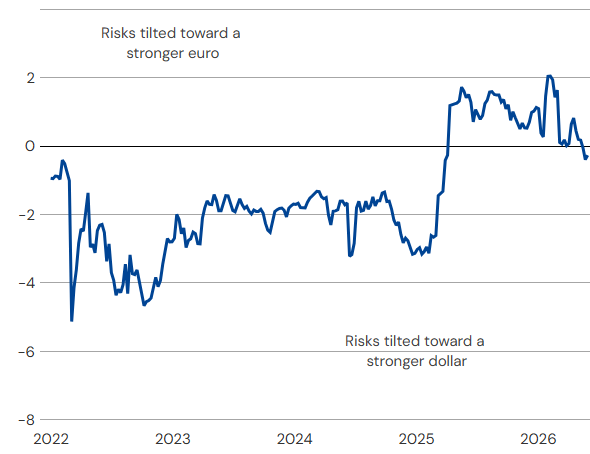

- An abrupt repricing of US assets amid high US policy uncertainty and stretched equity valuations would raise global risk aversion and tighten financing conditions.

Financial vulnerabilities can act as amplifiers through cross-border financial exposures and changing market structures.

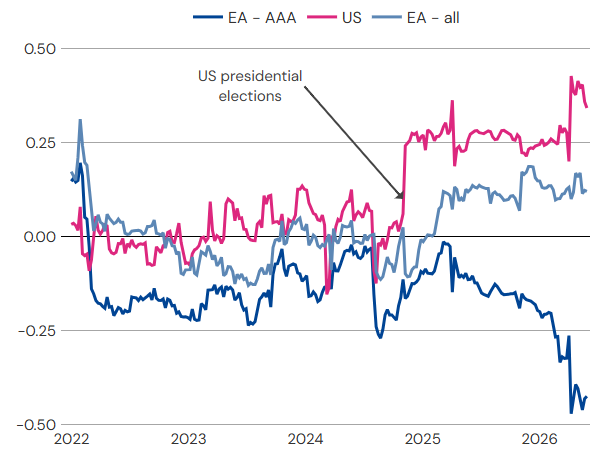

- The euro area financial sector’s large holdings of US assets and concerns about private credit markets could amplify market stress episodes.

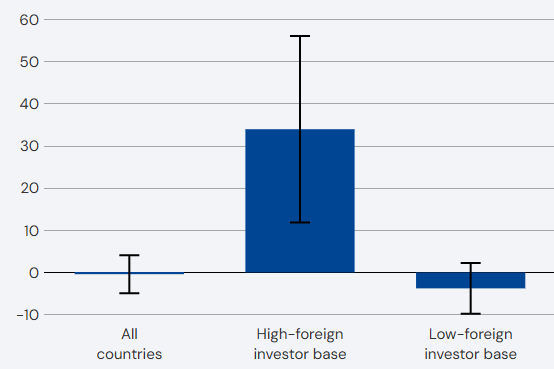

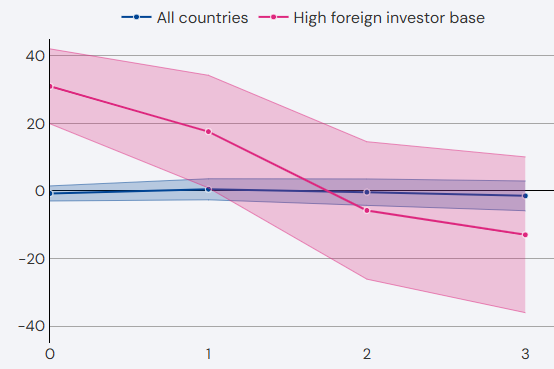

- Sovereign bond markets are vulnerable to abrupt sentiment shifts, partly due to the growing share of more price-sensitive investors, including hedge funds.

- By contrast, firms, households, and banks remain relatively resilient at this stage.

In an adverse scenario with prolonged geopolitical tensions and a sharp repricing of US assets, the euro area approaches recession while inflationary pressures intensify.

- Annual growth drops to 0.1% and inflation rises to 3.6% on average in 2026–2027.

- Over time, protracted high uncertainty and energy prices weigh on investment and competitiveness, leading to lasting output losses.

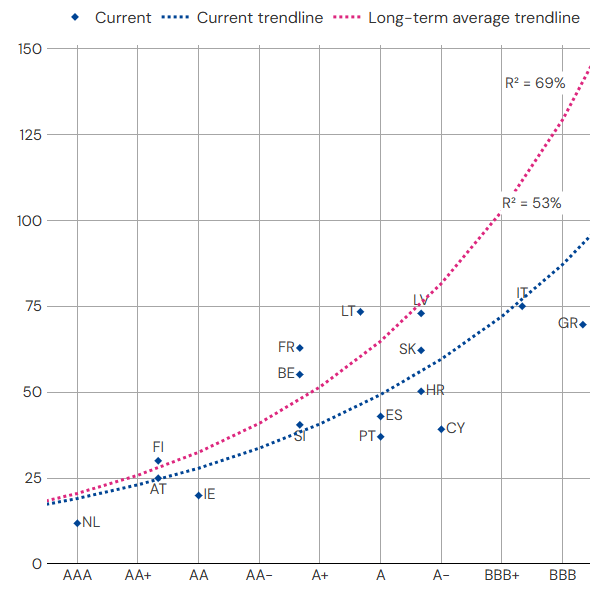

- Debt sustainability risks increase markedly, despite the immediate fiscal impact being relatively contained by the inflation surge.

Credibility is critical for maintaining fiscal resilience.

- Large fiscal adjustment needs will have to be managed under the new EU fiscal framework, leaving little room for policy missteps.

- Efficient fiscal support only when needed, credible medium-term plans backed by clear priorities to ensure implementation are key to maintaining market trust and safeguarding fiscal resilience.