Rolf Strauch at press conference on launch of EASW

Remarks by Rolf Strauch, ESM Chief Economist

Press conference on the launch of the ESM’s Euro Area Stability Watch

Brussels, 6 July 2026

Welcome to the launch of the first Euro Area Stability Watch. You may ask, ‘Why yet another report by a European institution?’ The report does what the name says: it keeps a watchful eye on the financial stability of the euro area. And it asks what happens if things go wrong, rather than what will happen. We think that is an important question for us as a crisis resolution mechanism because we want to anticipate shocks and be prepared for future crises.

And that is close to our mandate. The work that we present in the report complements the work of our colleagues in the European Commission and the European Central Bank. It puts specific focus on the vulnerabilities and risks of the euro area and spells out the fiscal implications that those carry. We think it is a particularly important question to address and a particularly important aspect to focus on in this global environment marked by increased uncertainty.

The report has two chapters.

The first provides our assessment of the risks to the baseline economic outlook as presented by the European Commission in its Spring Forecast.

The second chapter does a deep dive into defence as one of the key topics that currently shapes financial stability and sovereign risks.

We plan to publish the report annually around this time of year.

Let us now turn to the report that will be released at 11 o'clock today. The main message of the first chapter is that resilience is coming under strain. In the current environment, we see a confluence of challenges for the euro area. We have security threats, frictions in global trade, disruptions to energy supply, and financial market volatility. All of that puts strain on growth and public finances.

So, will the euro area, in view of those rising risks and diminishing fiscal buffers, be resilient? The report gives a clear answer. It says that rising risks and higher demand for public support will put financial stability and debt sustainability under pressure. That implies that policymakers will have to make clear choices because they will have to embark on fiscal adjustments in order to safeguard the credibility of the European fiscal framework. Having that credibility is very important because otherwise financial markets will determine the fiscal space that governments have available. We have learned in past crises that this is an uncertain and inherently unstable place to be.

So let me dig deeper into Chapter 1, which has two parts. The first part presents the risks and vulnerabilities and the second part talks about the fiscal implications.

When we look at the euro area, fortunately we see important strengths that underpin resilience. That is record-high employment, a well-capitalised banking sector, and solid backstops. These will continue to underpin resilience. But at the same time, next to those three strengths, we see three vulnerabilities.

First, we have the diminishing and eroding of fiscal space. And defence spending is a strong part of this. In a few minutes, I will explain how defence spending can be done so that over time it partly pays for itself.

The second vulnerability is that the region remains exposed to energy supply disruptions. And here, of course, the main risk is geo-economic uncertainty and geo-economic tensions. Those lead to higher energy prices, uncertainty, they undermine competitiveness and investment, and therefore in the long run, also growth in productivity.

The third factor is the close linkage of financial assets and liabilities with the United States, and this financial linkage implies that European investors are exposed to possible losses, and those may occur both with a view to equities and US Treasuries. We know that US equity prices are still stretched. They're built on expected earnings for artificial intelligence-related investment. At the same time, we see that sovereign bond markets now have a higher share of investors that are highly price-sensitive, and at the same time, many of them are located abroad. That means that in the future, markets may become more volatile.

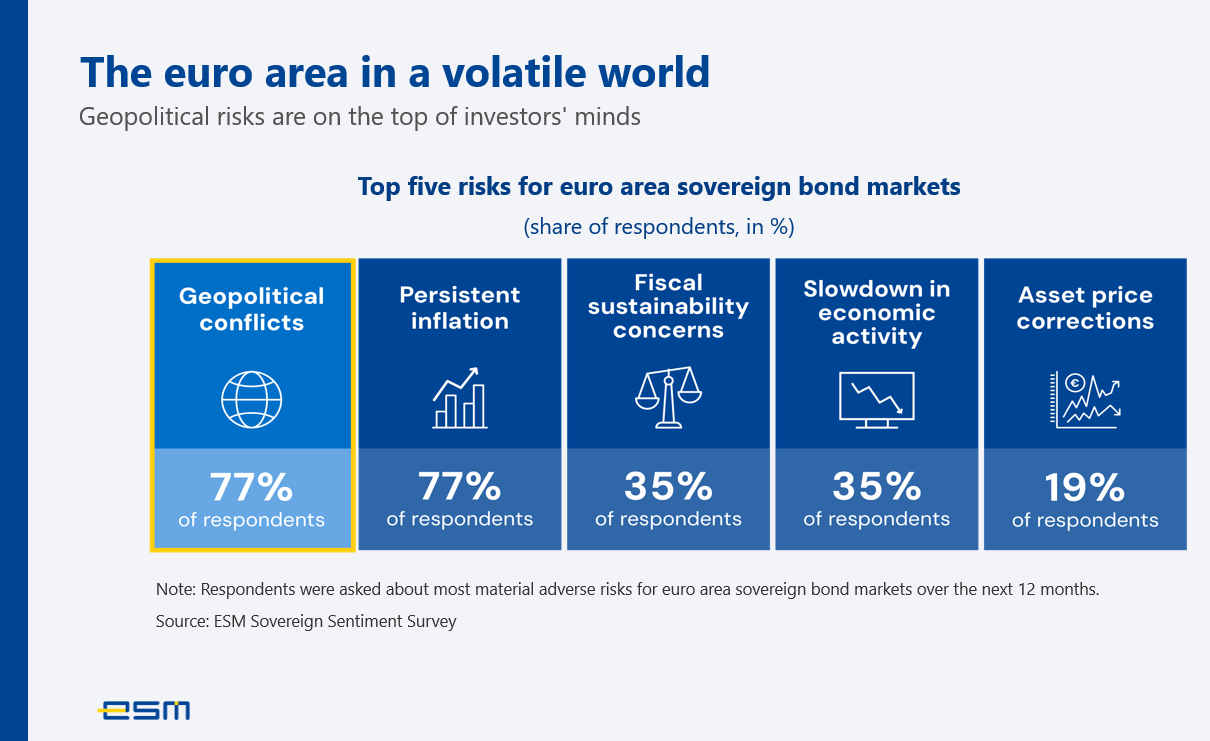

The escalation of geopolitical tensions is actually high in the minds of investors as a future risk for the euro area. And we have conducted a survey for this report where we asked investors how they look at the world.

And you see it in this chart what the outcome is. And you see in the chart that more than three-quarters of investors think that geopolitical tensions is one of the major risks that we are facing. The ESM, as an issuer and investor, is daily in the market, and we have an ample network of investors that we collaborate with, and we use that network in order to bring this element of market intelligence to the report.

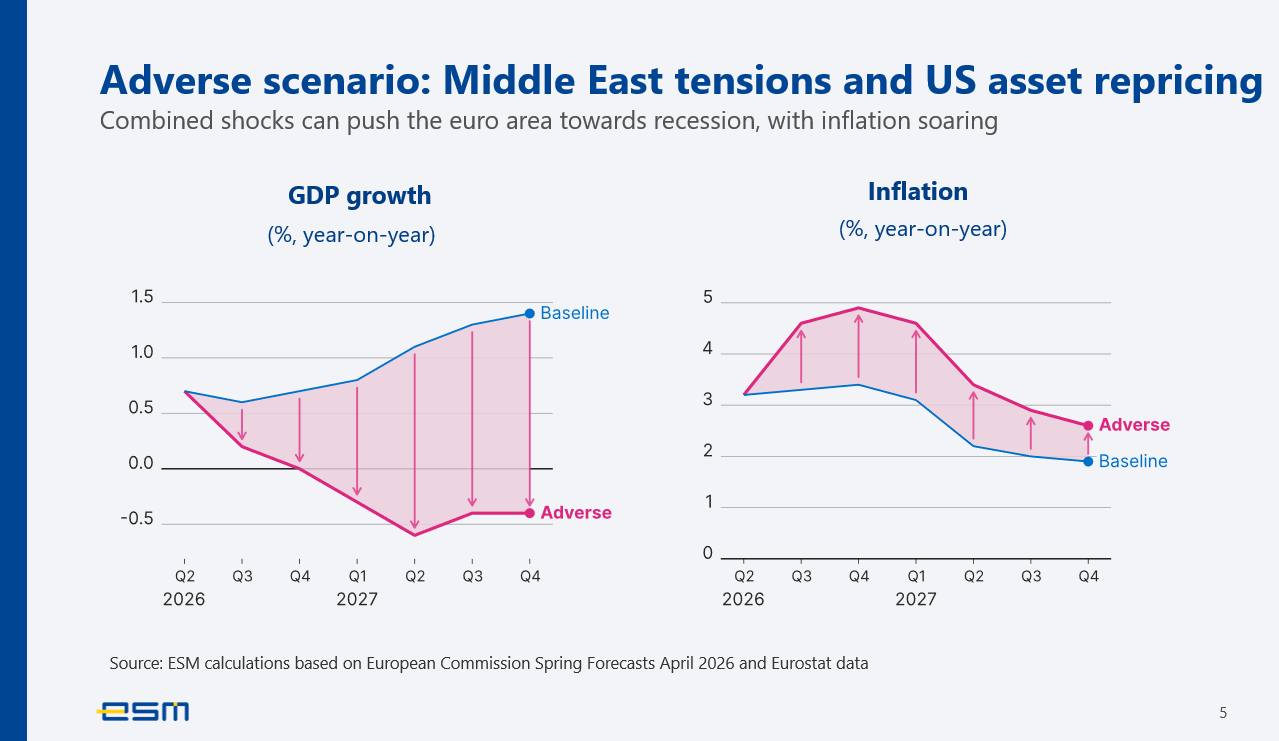

To better understand these risks, we present a scenario where we specify how shocks will affect the market, economy, and fiscal conditions, and how they would worsen when they occur.

We assume more specifically that two shocks occur simultaneously.

One is prolonged tensions and possible re-escalation in the Middle East that would lead to higher energy prices and extended uncertainty. We are obviously well aware of current developments and that probabilities for this to happen change. It's still an important risk to consider and to think about the implications of the shock.

The second shock that we look at is a strong loss of value in US assets. That would imply a tightening of financial conditions, and at the same time it would transpose losses to European investors. Each shock by itself would already be challenging. The two shocks combined in our view imply that the euro area would be pushed towards a recession and that inflation may be up to 5%.

From our perspective, there are long-term repercussions. The euro area would lose about 2% of GDP compared to past trends. That is about the magnitude of Finland's GDP. We also find in our analysis that big shocks have a disproportionately large effect on the economy, more than smaller tensions. The reason is that it mainly works through investment, and continued weak investment implies that there are scars in the economy, and those effects become more protracted. That is also why we think that European growth initiatives, and here specifically the Savings and Investments Union, are very important.

Another insight from the analysis is that the current situation differs from the sovereign debt crisis, the situation that we had in 2010. At that stage, it was mainly the fiscal position that was a determinant of the vulnerability and repercussions. Nowadays, the vulnerability emerges mainly from energy dependence and trade openness. So, there is a difference. It also implies that small open economies are more vulnerable than others.

What does all of that imply for fiscal policy? I will now dig a little bit more into the second part of the first chapter. And let me start this off by pointing to the main message of this chapter, and for that, use Willy Brandt and paraphrase him when he said, “Credibility is not everything. But without it, everything is nothing.” And what it means is that the fiscal framework gives flexibility and time, but only as long as markets trust that you will actually use this wisely.

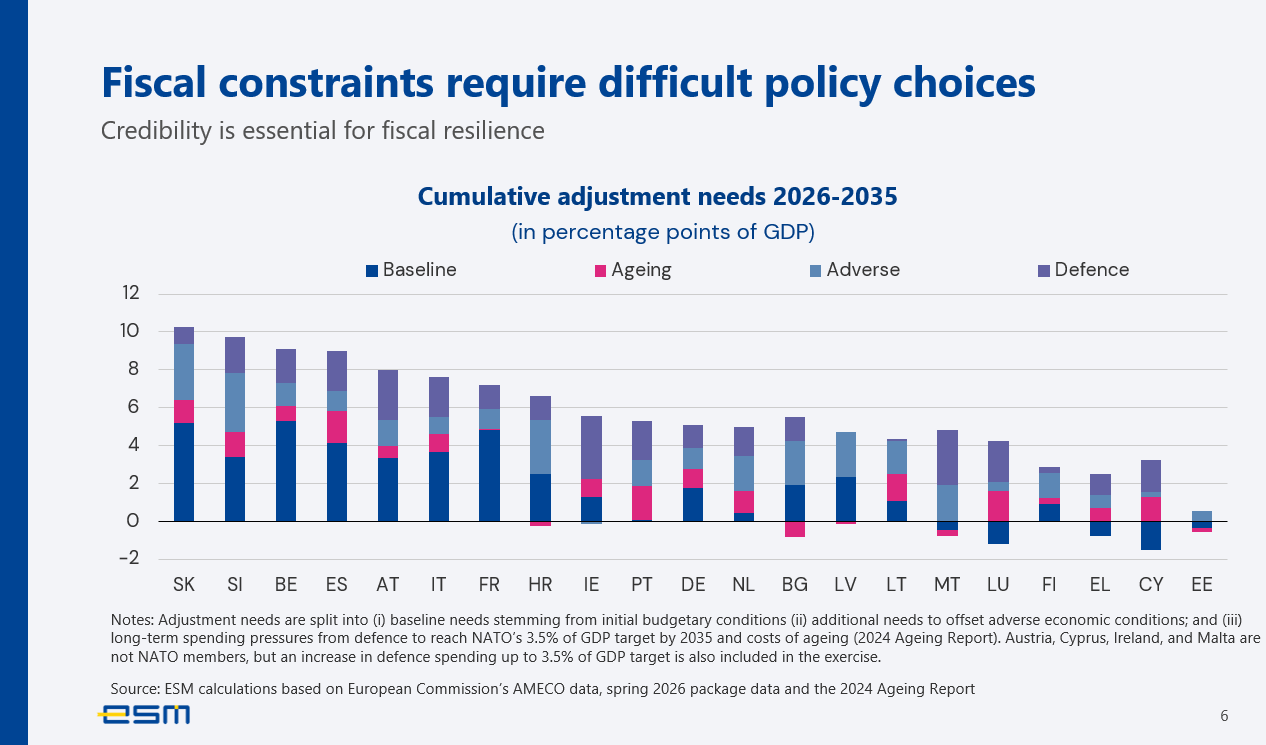

When we look at the repercussions of the two shocks that are outlined and the economic implications, there's also obviously a big impact on fiscal policies. And in our exercise, we find that public debt - when those shocks occur - would be 20 percentage points higher than under the baseline. And the debt trajectory for most euro area countries would be upward sloping. Obviously, addressing this implies large adjustment in a number of euro area countries, and you can see this in this chart here.

It shows what countries will have to do in the future in order to safeguard debt sustainability. You see that the amounts are very large, up to 10 percentage points of GDP. When you look at the chart, you see essentially that there are different drivers. And on the right-hand side, an important element of big fiscal adjustments that are needed is the current fiscal situation. Moreover, you see in the bars that are related to the adverse scenario and the impact that it has, that it is bigger for those countries, as I said before, that are small and vulnerable. And this has to be kept in mind.

These adjustments effectively for half of the countries exceed what has been done in the past, and that is an indication of the challenge that they face. And that is essentially what we mean when we say that sustainability is put under strain.

When you're in such a situation, it strengthens the case to look at the quality of public finance. And here we associate ourselves also with the call that crisis measures actually have to be targeted, timely, temporary, and tailored. This is more efficient, more cost-efficient than having broad-based measures deployed to the economy, such as general reductions in tax rates. Looking at the situation, it's essentially rebuilding buffers, spending efficiently, and advancing structural reforms that are the factors that drive growth and resilience. And this will require tough choices, looking forward. As a euro area safety net, we can prevent liquidity strains from turning into solvency fears. And we do this through credible insurance instruments and here above all, our ESM precautionary arrangements.

Now let me turn to the second chapter of the report that is more topical.

The euro area security situation has experienced a landslide change in the current environment. And what it means is that Europe has to spend more on defence and that is what governments have decided to do. That spending is necessary, but it matters a lot how you spend your money.

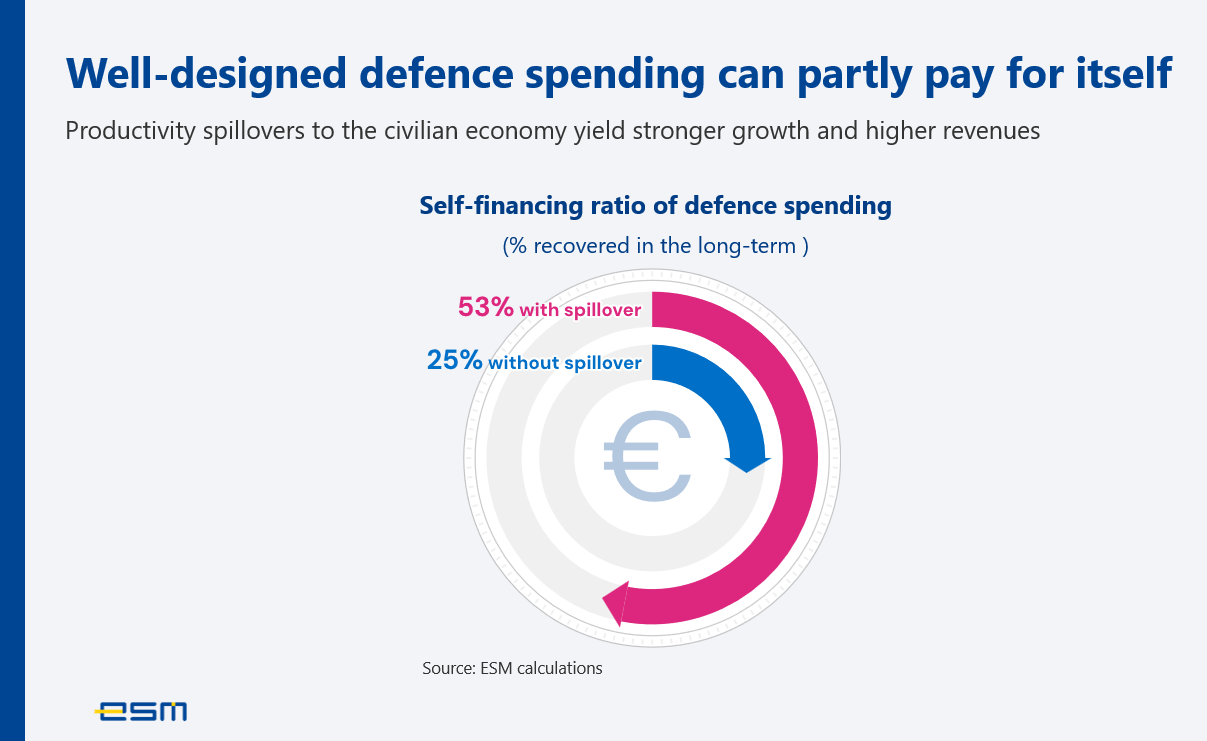

And one of the key results of the report is that when you spend your money wisely, in a well-designed way, and you take account of the European dimension, a big part of the spending actually can finance itself. And more specifically, you see the result of our analysis, which shows that with productivity spillovers, 53 cents of each additional euro spent can in the long run be recovered through higher growth and taxation. And that compares to 25 cents when you don't have those spillover effects. So it doubles the effect that you can have.

What does it mean that spending is well designed and has a European dimension? We have essentially four factors that determine the fiscal payback.

The first factor is how money is spent matters as much as how much is spent. Defence spending generates productivity spillovers, leading to stronger economic impact if you actually provide that money and spend it on technology and innovation, if it allows civilian companies to actually improve their production, and if you focus on research and development. In turn, if your money goes mainly to personnel, maintenance, and buying supplies from abroad, the growth impact is much less.

The second element is how defence spending is financed matters a lot. And here we see if you can reprioritise spending within a given budget envelope, then actually this is more growth-friendly than increasing taxation, and particularly more growth-friendly than increasing taxation on labour.

The third element is whether defence spending has a European dimension. And with that European dimension, we have in mind procurement. Procurement should be broadly sourced within Europe. When you do so, this will allow European countries to actually deploy their comparative advantage, build a comparative advantage, and then strengthen the single market. That should help overall efficiency.

Finally, the second element of European dimension is that you should respect the guardrails of a credible fiscal framework. As we have argued before, when you have credibility, it lowers costs. So, having defence spending integrated into well-designed national programmes, and observing what the European fiscal framework says, helps lower their costs.

Response to question on two different figures concerning inflation provided in the report

Rolf Strauch: Here I show again the chart that you also have in the report. Indeed, if you look at it, on the left-hand side, you see first that in the adverse scenario, GDP would go into recessionary area. And on the right-hand side, that indeed, according to our estimates, inflation could go up to 5%. Obviously, this scenario is under what we call the “no policy change assumption”. So we do not factor in ECB monetary policy, nor corresponding fiscal policy changes. That is important to note, which we think is prudent to do. But obviously, if there was a monetary policy reaction, then you would have higher interest rates, and that would also feed into the economy.

Pilar Castrillo, Head of Economic and Market Analysis: Just, to complement, the 3.6% that you mentioned is the annual average. Here you see that it peaks at 5% and the annual average that is in the report is 3.6%.

Response to question on whether exceptions to the Stability and Growth Pact rules, granted by the Commission, based on defence and green energy, project the credibility needed for a fiscal framework

Rolf Strauch: We think that the European fiscal framework is very important. It was also necessary to address the security concerns and allow for the national escape clauses to kick in because we need security and we need to have the necessary spending. The Commission later decided then to broaden somewhat the expansion that can be done under those national escape clauses, but also applying them to environmentally friendly and energy-saving measures. This is a decision of the European Commission that does not broaden the overall envelope that was created, but we are also very conscious that one must be mindful in what you do to the framework, because in financial markets this can be read as a weakening of the overall framework. For us, the key point is that even if you do this now, you need to have a forward-looking perspective, and we need to build on the framework forward-looking. That is why we are also spelling out now the challenges that will emerge and how eventually you have adjust. So even if you look, if you use the space forward-looking, you need to adjust your budgets in order to include those spending items.

Response to question on whether different types of triggers led to the euro sovereign debt crisis and the more recent crises

Rolf Strauch: If you look at that chart that I showed on the fiscal implications of the adverse scenario, you see indeed that those are bigger in small countries, which is not surprising because their economies are more affected. Obviously, there is the point that - and that also what makes the report relevant - is that at some stage, forward-looking, not now, but at some stage, obviously there can be a point when this is combined with broader concerns about the debt situation of a country, and then obviously that will at that stage also become by itself a driver, potentially, of financial instability. So, the origin of the crisis or the origin of the vulnerability that we see now is a different one.

Response to question on how the ESM is trying to address the stigma associated with its financial assistance, so that its credit lines could be used without fear

Rolf Strauch: First, let me say that this report is part of our work as a crisis resolution mechanism, because part of our mandate is also to think about the prevention of crises. And that is what this report is about. It's meant to strengthen overall resilience and crisis preparedness.

Now, on our role and the ESM being used, we have obviously thought about the issue and the question of potential stigma. We have discussed this also with Member States in our review of the toolbox that we have discussed. And we are thinking about possible solutions that can, for example, also entail the possibility that Member States as a group may sign up to a precautionary arrangement if a common threat emerges. So, it's part of our thinking to overcome that issue and part of the practical approach that you would have to take in a crisis.

Response to question on whether the risk exposure is higher on the left side of the chart “Fiscal constraints require difficult policy choices”

Rolf Strauch: When you look at the impact of the adverse scenario (the light blue bars), and you see that those can be big for countries, or are big in our estimate, for countries like Slovakia, Slovenia, but also if you move to the right-hand side, Bulgaria, Latvia. In the report we have also a very nice chart that shows the exposure to energy or the energy dependency of countries, and there is actually a correlation - so with the right-hand side of that chart. Higher energy exposure means higher vulnerability.

There is a difference between the left-hand side and the right-hand side on this chart. As I said before, this is what we call here the baseline. The baseline means the adjustment needs that emerge from your current situation and the forward-looking path of interest rates and growth - the interest rate growth differential. So if you have a high deficit or high debt this stage, and your interest rate growth differential is such that you don't grow more than your interest rates, that means that the dark blue bar is actually bigger. And that is the difference between the countries on the left-hand side and the right-hand side, by and large. That is why some countries that are small, but at the same time have less of a current fiscal issue are from that perspective less of a concern or will face smaller adjustment needs.

Response to question on whether 2028 could be seen as a cliff year because some European programmes will come to an end, and what the ESM would recommend to Member States in regard to fiscal adjustments

Rolf Strauch: In 2028, the Next Generation EU programme will end. And the other point is that the national escape clauses will expire in 2028. Those put a challenge on governments, and it comes back also to the question of the adjustment that you asked. It is not our role and not the task in this report here to devise concrete adjustment plans for countries. That is actually done in the country-specific recommendations by the European Commission.

As a general remark, the report is essentially a call to early think about these later fiscal positions. You now need to think essentially how the world will look when you get to 2028. And here we learn from the past that it is very important to keep up investment. And when the European money will be absorbed, it will be important also for governments not to scale down investment. It means that some space for that would have to be created. The other general element that we see is one needs to be mindful of spending efficiencies, and spending reviews are an important point here.

The third element – and this is a general topic for Europe - is that it's important to also focus on those areas where one can complement, or where the private sector can actually complement and take over tasks that have been done and spending that has been assumed by the public sector so far. And here I come back to this element of the Savings and Investments Union (SIU) that we mentioned before, because SIU meant to absorb and produce financing for the growth of the economy. And here, also the capitalisation of pension systems is a major pillar that needs to be developed, and that can actually help to save some money from the public purse. So, these are a few general elements that could drive that adjustment path.

Response to question on the situation of the Greek economy, as presented in the report, and what the ESM’s advice for Greece would be.

As you know, we are following the Greek economy very closely, and we have also pointed out to the gains that Greece has made and the progress that Greece has made ever since it left the ESM support programme. Greece is marked by relatively high growth and also you have high public surpluses, and that's obviously a fairly strong starting position in order to face shocks. At the same time, debt levels are high and you need to continue work on your productivity in order to sustain those high growth levels. So the overall point that we see is that for Greece, it's good to continue its fiscal prudence and to further embark on reforms to transform the economy and keep high growth levels.

Contacts