Annual reports

ESM

In a world of increasingly integrated capital markets, the global financial crisis and subsequent European financial instability underscored the necessity of setting up credible financial backstops for crisis prevention and resolution. Countries that are under severe financial strain may be shut out of capital markets and need to seek immediate financing assistance, while others with sound domestic policies and fundamentals may also suffer from excessive capital outflows spurred by heightened financial market risk aversion or spillover from other countries. To tackle this problem, the Group of Twenty (G20) industrialised and emerging market economies have promoted an initiative to strengthen a multi-layered Global Financial Safety Net (GFSN), with Regional Financing Arrangements (RFAs) as an important component.

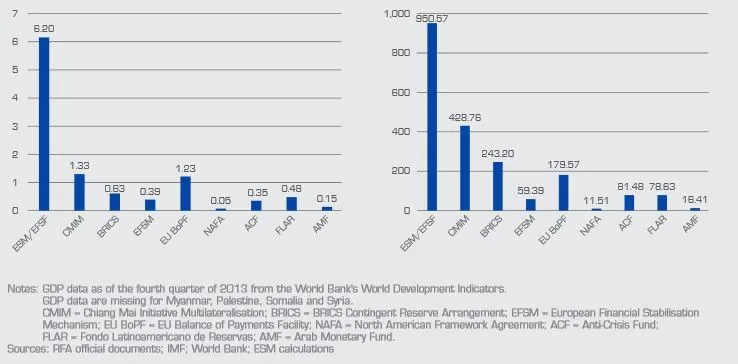

The European experience in dealing with recent crises highlights the importance of mobilising regional financial resources to complement IMF lending. The total resources available at existing RFAs, $1.2 trillion in 2013, almost reached the IMF’s $1.4 trillion that same year. The EFSF and ESM stand out with their combined lending capacity totalling €700 billion – the biggest among RFAs – covering 6.2% of Members’ total gross domestic product and 950% of Members’ aggregate IMF quota shares.

There are eight other major RFAs in the world. Some of them, such as the Arab Monetary Fund or Fondo Latinoamericano de Reservas, were created in the immediate aftermath of past crisis episodes. A few other RFAs have been created or further institutionalised in recent years.

In Europe, several crisis resolution mechanisms with different country coverage and lending capacity precede the creation of the EFSF and ESM. The EU created a balance of payment assistance facility, raising its lending capacity to reach a maximum of €50 billion in 2009. It could provide financial assistance to nine non-euro area countries. An equivalent mechanism was reproduced for the EU in May 2010 under the name of the European Financial Stabilisation Mechanism with a lending capacity of €60 billion to help resolve the euro area crisis. It was activated for Ireland and Portugal for €48.5 billion.

Asia took a significant step towards stronger regional coordination in crisis prevention in 2010.

On 24 March 2010, the existing bilateral swap line agreements – Chiang Mai Initiative – were merged into a single contract called Chiang Mai Initiative Multilateralisation (CMIM). It covers 10 ASEAN countries plus China, Japan, and Korea. CMIM’s total size has been increased twice in the recent financial crisis, to $240 billion in 2012 from $78 billion in 2008. A surveillance unit for the CMIM was also created in 2011 to monitor and analyse regional economies.

Armenia, Belarus, Kazakhstan, the Kyrgyz Republic, Russia, and Tajikistan founded an Anti-Crisis Fund of the Eurasian Economic Community in July 2009. Uniquely financed by members’ capital contributions, this fund has a total lending capacity of $8.5 billion; Tajikistan and Belarus have both benefited from this regional facility.

Finally, the five biggest emerging market economies signed a treaty establishing the BRICS Contingent Reserve Arrangement in July 2014. The newest RFA, whose shareholders are Brazil, Russia, India, China and South Africa, is endowed with $100 billion in capital. It is composed of multilateral swap lines akin to those of the CMIM.

In addition to the creation or further institutionalisation of RFAs, G20 countries also adopted the Principles for cooperation between the IMF and RFAs in 2011. The EFSF and ESM programmes have provided good examples of how an RFA and the IMF can work together. Whenever possible, the IMF is an integral part of European financial assistance programmes. It has co-financed several programmes, conducted programme reviews and country surveillance jointly with European institutions, and has provided technical assistance. RFAs have comparative advantages in sustaining financial stability at the regional level. They have in-depth knowledge of region-specific issues and can mobilise large amounts of financing relatively quickly.#

Founded by regional members, RFAs may also enhance democratic support in regional economies. Generally, efficient coordination between the IMF and RFAs generates synergies in terms of resource allocation and surveillance capacity. It also precludes ‘programme shopping’ and the associated moral hazard by ensuring consistent sets of economic conditions linked to financial assistance.

The European experience in dealing with recent crises highlights the importance of mobilising regional financial resources to complement IMF lending. The total resources available at existing RFAs, $1.2 trillion in 2013, almost reached the IMF’s $1.4 trillion that same year. The EFSF and ESM stand out with their combined lending capacity totalling €700 billion – the biggest among RFAs – covering 6.2% of Members’ total gross domestic product and 950% of Members’ aggregate IMF quota shares.

There are eight other major RFAs in the world. Some of them, such as the Arab Monetary Fund or Fondo Latinoamericano de Reservas, were created in the immediate aftermath of past crisis episodes. A few other RFAs have been created or further institutionalised in recent years.

In Europe, several crisis resolution mechanisms with different country coverage and lending capacity precede the creation of the EFSF and ESM. The EU created a balance of payment assistance facility, raising its lending capacity to reach a maximum of €50 billion in 2009. It could provide financial assistance to nine non-euro area countries. An equivalent mechanism was reproduced for the EU in May 2010 under the name of the European Financial Stabilisation Mechanism with a lending capacity of €60 billion to help resolve the euro area crisis. It was activated for Ireland and Portugal for €48.5 billion.

Asia took a significant step towards stronger regional coordination in crisis prevention in 2010.

On 24 March 2010, the existing bilateral swap line agreements – Chiang Mai Initiative – were merged into a single contract called Chiang Mai Initiative Multilateralisation (CMIM). It covers 10 ASEAN countries plus China, Japan, and Korea. CMIM’s total size has been increased twice in the recent financial crisis, to $240 billion in 2012 from $78 billion in 2008. A surveillance unit for the CMIM was also created in 2011 to monitor and analyse regional economies.

Armenia, Belarus, Kazakhstan, the Kyrgyz Republic, Russia, and Tajikistan founded an Anti-Crisis Fund of the Eurasian Economic Community in July 2009. Uniquely financed by members’ capital contributions, this fund has a total lending capacity of $8.5 billion; Tajikistan and Belarus have both benefited from this regional facility.

Finally, the five biggest emerging market economies signed a treaty establishing the BRICS Contingent Reserve Arrangement in July 2014. The newest RFA, whose shareholders are Brazil, Russia, India, China and South Africa, is endowed with $100 billion in capital. It is composed of multilateral swap lines akin to those of the CMIM.

In addition to the creation or further institutionalisation of RFAs, G20 countries also adopted the Principles for cooperation between the IMF and RFAs in 2011. The EFSF and ESM programmes have provided good examples of how an RFA and the IMF can work together. Whenever possible, the IMF is an integral part of European financial assistance programmes. It has co-financed several programmes, conducted programme reviews and country surveillance jointly with European institutions, and has provided technical assistance. RFAs have comparative advantages in sustaining financial stability at the regional level. They have in-depth knowledge of region-specific issues and can mobilise large amounts of financing relatively quickly.#

Founded by regional members, RFAs may also enhance democratic support in regional economies. Generally, efficient coordination between the IMF and RFAs generates synergies in terms of resource allocation and surveillance capacity. It also precludes ‘programme shopping’ and the associated moral hazard by ensuring consistent sets of economic conditions linked to financial assistance.