Explainers

The ESM has a total capital €708.5 billion. This consists of nearly €81 billion in paid-in capital provided by ESM Members and approximately €627.5 billion in committed callable capital.

The paid-in capital underpins the financial strength and high creditworthiness of the ESM as an issuer. It serves as a security buffer for the bonds and bills the ESM issues and is not used for lending operations.

Paid-in capital is the portion of the ESM’s total capital paid in by ESM Members. The other portion of ESM’s capital is committed but will only be called if needed.

The financial contribution of each ESM member to the ESM capital is based on the capital key of the European Central Bank (ECB). It reflects the respective country’s share in the total population and gross domestic product of the euro area. The ESM Members’ contribution keys, corresponding capital subscription, and amount of paid-in capital are found here: How we decide: ESM shareholders and their representatives in governing and oversight bodies

The ESM may require its Members to make a capital payment. In other words, it may call capital which has been committed and is part of the ESM’s total capital. Such a capital call would only happen in three specific situations:

- When the Board of Governors so decides by mutual agreement;

- to replenish paid-in capital to covers losses;

- to avoid default on an ESM payment obligation to its creditors.

The total amount of committed callable capital is €627.5 billion; each ESM Member’s share of this amount is based on the capital contribution key.

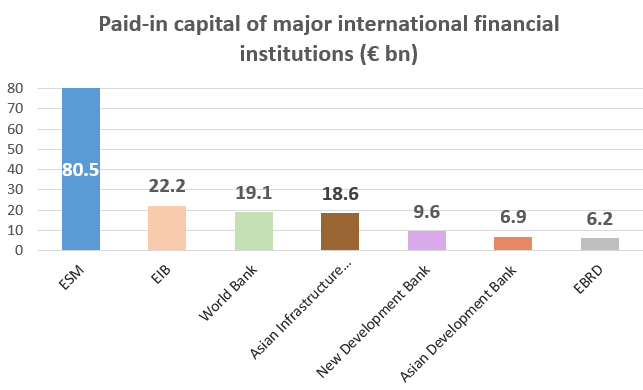

The ESM currently has the largest amount of paid-in capital among all international financial institutions in the world, as shown in the following chart:

Note: Amounts for the World Bank, Asian Infrastructure Investment Bank, New Development Bank, and Asian Development Bank converted from USD according to exchange rate of 20 March 2023.

Source: most recent financial statement of each institution

The Irish economy suffered as a consequence of a boom-bust cycle in the housing market. House prices increased four-fold from 1997 to 2007, when the bubble burst. As the property boom was financed through aggressive lending by Irish banks, the decline in property prices and the collapse in construction activity resulted in severe losses in the Irish banking system. The government of Ireland responded by injecting public funds into banks to restore their solvency (over €60 billion). This led to a huge increase in Ireland’s public debt, while the sharp decline in economic activity caused GDP to fall and unemployment to rise. The Irish government was not able to resolve the situation on its own, and therefore requested financial assistance from the euro area countries, the EU and the IMF.

The programme for Ireland was financed as follows:

- €67.5 billion in external support including

- €17.7 billion from EFSF (this was the EFSF’s first financial assistance programme);

- €22.5 billion from EFSM (European Financial Stabilisation Mechanism – an EU facility funded through bonds issued by the European Commission);

- €22.5 billion from IMF;

- €4.8 billion in bilateral loans from the UK (€3.8 billion), Sweden (€0.6 billion) and Denmark (€0.4 billion);

- €17.5 billion domestic contribution (from the Irish Treasury and the National Pension Fund Reserve)

- A financial sector strategy comprising fundamental downsizing and reorganisation of the banking sector (including recapitalisation and deleveraging);

- A strategy to restore fiscal sustainability (reducing expenditure, tax system reform, generation of additional revenue);

- A structural reform package to underpin growth, focusing on competitiveness and job creation.

The majority of the EFSF programme amount was used for budget financing needs and a smaller portion was assigned for the recapitalisation of banks.

Ireland returned to the bond market in July 2012, when it issued a 5-year bond at 5.9%. Just one year earlier, the yield on 5-year Irish bonds was above 13%, which shows how quickly Ireland managed to put its economy back on track and regain the confidence of investors. The country had been forced out of international bond markets in September 2010.

Ireland has achieved a remarkable economic recovery since the conclusion of its financial assistance programme in December 2013. Ireland’s GDP growth was the highest among all EU countries in 2014 (8.5%), 2015 (26.3%) and 2016 (5.2%). In addition, Ireland’s unemployment rate of 7.9% in 2016 was well below the euro area average (10%).

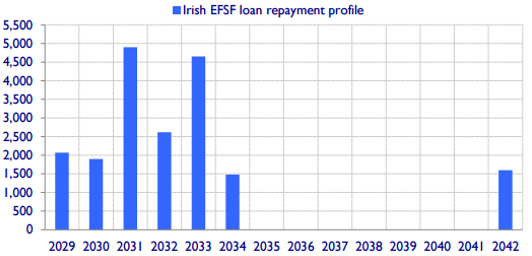

Ireland will repay the principal of the loan tranches starting from 2029, and the repayment is scheduled to end in 2042.

The extent of underlying economic problems at the beginning of the crisis in Greece was much greater than in other ESM/EFSF programme countries. Having adopted the euro in 2001, Greece was able to borrow at low interest rates despite its falling competitiveness and weak public finances. While government spending and borrowing increased, tax revenues weakened due to poor tax administration. Public debt soared quickly and investor trust in Greece was seriously undermined. The Greek economy contracted sharply (nearly 30% from 2008 to 2016) and unemployment climbed to alarming levels. Furthermore, the country’s administration was weaker than in other euro area countries. The public sector was oversized and its efficiency was well below European standards.

During the first and second programmes (bilateral loans from the other euro area countries known as the Greek Loan Facility or GLF from 2010-2011; EFSF programme from 2012-2015), wide-ranging reforms were carried out to address Greece’s problems, and in 2014, the country recorded GDP growth for the first time since 2007 and unemployment began to fall. In the first half of 2015, the country reversed very important reforms. There was an attempt to halt the reform programme Greece had agreed to. The result was that the country dropped back into recession. The third programme, agreed with the ESM in August 2015, enabled Greece to remain in the euro area in return for implementing a series of much-needed reforms. After three years, on 20 August 2018, Greece successfully completed the ESM programme. As of this date, the country is no longer reliant on ongoing external rescue loans for the first time since 2010.

Greece made major efforts to implement wide-ranging reforms, which were tied to the first financial assistance package. The challenges confronting Greece remained significant, however, with a wide competitiveness gap, a large fiscal deficit, a high level of public debt, and an undercapitalised banking system. The economic recession in Greece proved to be more serious and damaging than expected. The financial assistance provided under the first programme was not sufficient for Greece to make the necessary adjustments and to regain market access.

Furthermore, Greece’s public debt was considered unsustainable. A restructuring of debt held by private creditors became necessary to bring the total debt level back to a sustainable path. Additional time and funds were required to Greece’s fiscal consolidation efforts with structural reforms, to boost growth, and improve competitiveness. Therefore, a second programme for Greece, provided by the EFSF and IMF, was decided in February 2012.

Although Greece’s achievements in rebounding from a deep crisis have been remarkable, significant challenges remain. Efforts must continue to liberalise the economy, create an effective public administration, as well as a business-friendly environment. Unemployment remains very high (19.5% in May 2018), and sustainable growth is the only way for Greece to deliver more jobs and prosperity for its people.

Greece needs to build upon the progress achieved under the ESM programme and strengthen the foundations for a sustainable recovery, notably by continuing and completing reforms launched under the programme. In an annex to the Eurogroup statement of 22 June 2018, the Greek government committed to ensure the continuity and completion of reforms in several key areas:

- Fiscal and structural (primary surplus of 3.5% of GDP over the medium-term)

- Social welfare (modernising pension and health care systems)

- Financial stability (continued reforms aimed at restoring the health of the banking system, including NPL resolution)

- Labour and product markets (action plan on undeclared work; investment licensing reform; completing the cadastre project)

- Hellenic Corporation of Assets and Participations (HCAP) and privatisation (asset development plan; completing key transactions)

- Public administration (modernising human resource management in the public sector; new labour law code; implementing anti-corruption recommendations).

Since 2010, Greece has carried out a comprehensive range of reforms, which can be grouped into four areas (the most important examples are listed):

- Restoring the sustainability of public finances

- Personal income tax system revised

- VAT system streamlined for general efficiency and to reduce scope for fraud

- Unsustainable and fragmented pension system overhauled

- Safeguarding financial sustainability

- Governance of Greek systemic banks strengthened and brought in line with international best practice

- Structure of household and corporate insolvency legislation reviewed

- Reduction in stock of non-performing loans (NPLs)

- Structural policies to enhance growth, competitiveness and investment

- Labour market reforms – improved system of collective bargaining

- Product markets – reducing unnecessary barriers, lifting restrictions in regulated professions

- New independent fund (HCAP) for better management, improved service provision, and monetisation of key State assets

- Energy market for gas and electricity has been opened

- The functioning of Greece’s public sector

- Size of public sector reduced by 25% between 2009 and 2017

- Annual performance assessments for all public officials; competitive selection of senior management

- Reforms improving efficiency of judicial system

The ESM and EFSF have provided loans to Greece at much lower interest rates and with exceptionally long maturities compared to those that the market would offer. These favourable lending terms have generated considerable budgetary savings, facilitating fiscal consolidation and/or tax cuts. The amount of savings is calculated by comparing the effective interest rate payments on ESM and EFSF loans with the interest payments Greece would have paid had it covered its financing needs in the market. In 2017 the savings amounted to €12 billion, or 6.7% of Greek GDP. The savings take effect at similar level every year.

With a combined €190.8 billion in outstanding loans to Greece, the EFSF and the ESM are by far the country’s largest creditors. This is an amount higher than Greece’s projected GDP in 2018. The rescue funds together hold a total 55.5% of Greek central government debt.

In order to ensure that Greece and other beneficiary countries repay their loans, the ESM is obliged by the ESM Treaty to carry out its own monitoring, called the Early Warning System(EWS), until the loans have been repaid in full. This requires an assessment of the country’s short-term liquidity, market access, and the medium- to long-term sustainability of public debt.

The European Commission activated the Enhanced Surveillance framework, which implies quarterly reports of the Commission to assess its economic, fiscal and financial situation and the post-programme policy commitments. Enhanced surveillance is appropriate due to the large amount of money disbursed by the EFSF/ESM and the unprecedented debt relief. The ESM will closely collaborate with the Commission in the post-programme phase in the context of its Early Warning System.

Greece has committed to maintain a primary surplus (a national government’s budget surplus excluding interest payments on its outstanding debt) of 3.5% of GDP until 2022 and, thereafter to ensure that its fiscal commitments are in line with the EU fiscal framework (around 2%).

Further commitments are described in What challenges does Greece still face?

Due to political uncertainty and fear of a Greek euro exit, deposit holders withdrew significant funds from Greek banks in 2015, and the banks experienced an increase in payment delays as borrowers waited to see whether the government would introduce debt relief measures.

Under the programme, the ESM committed up to €25 billion to Greece to address potential bank recapitalisation and resolution costs. In December 2015, the ESM disbursed a total of €5.4 billion to the Greek government for the recapitalisation of Piraeus Bank and NBG.

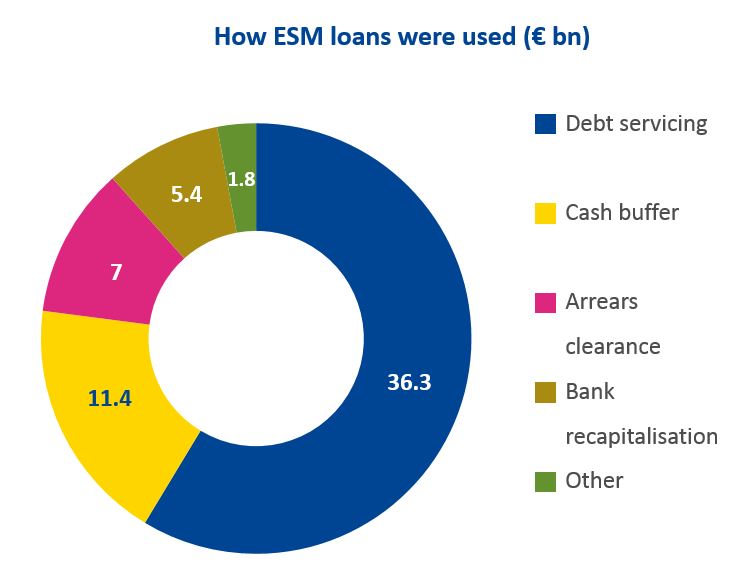

The chart below provides a breakdown of how the ESM loans were used by Greece:

The ESM disbursed a total of €61.9 billion, out of a maximum programme volume of €86 billion. The unused amount mainly derives from the substantially lower recapitalisation needs of banks compared to what was originally foreseen (€5.4 billion used out of a maximum amount of €25 billion) and from more efficient management of cash resources by the Greek government.

It should be noted that in the ESM programmes for Spain and Cyprus, the amount disbursed was also lower than the maximum amount available under their respective programmes.

The implementation of an ambitious growth strategy and prudent fiscal policies by the Greek government will be the key ingredients for debt sustainability. Through its long-term growth plan, Greece is committed to preserving its programme achievements, which includes completing the reforms that were enacted under the programme and continuing to implement further reforms designed to boost its growth potential.

In addition, the Greek government has committed to maintaining a primary surplus of 3.5 % of GDP until 2022, and around 2% in following years to continue to ensure that its fiscal commitments are in line with the EU fiscal framework.

Finally, the medium-term debt measures agreed by the Eurogroup, together with the significant cash buffer available to the Greek government, will provide strong support for Greece’s efforts. The European institutions’ Debt Sustainability Analysis, DSA, indicates that Greece’s gross financing needs are expected to remain below 15% of GDP over the medium term and to comply with the 20% threshold in the long run, and that Greece’s debt is therefore considered sustainable.

For the long-term, the Eurogroup also agreed to review at the end of the EFSF grace period in 2032, whether additional debt measures are needed to ensure the respect of these gross financing needs targets. However, additional measures can only be considered if Greece continues to respect the EU fiscal framework.

Greece will repay the ESM loans from 2034 to 2060. In November 2018, the EFSF Board of Directors approved a set of medium-term debt relief measures for Greece, which included an extension of the maximum weighted average maturity by 10 years on €96.4 billion of EFSF loans to Greece. Consequently, in April 2019, after a re-profiling of the EFSF loans to Greece, the current repayment period for the EFSF loans is from 2023 to 2070. (see detailed information on the repayment of EFSF loans)

After Greece adopted the euro in 2001, it was able to borrow at much lower interest rates despite its deteriorating competitiveness and public finances. In the decade before the crisis, Greece was able to use this cheap funding to finance a deficit which grew to unsustainable levels. Conditions in the euro area during this period facilitated such lending, despite the build-up of the unsustainable deficit. This meant that Greece could delay difficult structural reforms that had become necessary and may have been unavoidable if cheap funding had not been available during the 2000s.

While government spending and borrowing increased, tax revenues weakened due to poor tax administration. At the same time, wages rising much faster than productivity growth undermined Greece’s competitiveness, while low productivity and existing and significant structural problems also contributed to the increasing economic difficulties. As a result, Greece’s economy contracted and unemployment began to climb to alarming levels.

Greece’s reliance on external financing for funding budget and trade deficits left its economy very vulnerable to shifts in investor confidence. In 2009, the Greek government revealed that previous governments had been misreporting government budget data. Much higher-than-expected deficits eroded investor confidence, causing the yields on Greek sovereign bonds (which correspond to the cost of borrowing money) to rise to unsustainable levels. The situation worsened to the point where the country was no longer able to refinance its borrowing, and it was forced to ask for help from its European partners and the IMF.

The Eurogroup politically approved three medium-term debt relief measures for Greece on 22 June:

- The abolition of the step-up interest rate margin related to the debt buy-back instalment of the second Greek programme as of 2018;

- The use of 2014 SMP (Securities Markets Programme) profits from the ESM segregated account and the restoration of the transfer of ANFA (Agreement on Net Financial Assets) and SMP profits to Greece (as of budget year 2017). These are profits acquired by national central banks and the ECB from holdings of Greek government bonds (purchased on the secondary market). The profits will be transferred to Greece in equal amounts on a semi-annual basis in December and June, starting in 2018 until June 2022. They will be used to reduce gross financing needs or to finance other agreed investments;

- A further deferral of interest and amortization by 10 years and an extension of the maximum weighted average maturity by 10 years on €96.4 billion of EFSF loans.

Measures I and II are subject to compliance with policy commitments and monitoring. The total package of medium-term debt relief measures will reduce the Greece’s debt-to-GDP ratio by an estimated 30 percentage points by 2060, and the gross financing needs-to-GDP ratio by around eight percentage points. This comes on top of the already implemented short-term debt relief measures.

Based on a debt sustainability analysis (DSA) to be provided by the European institutions, the Eurogroup will review at the end of the EFSF grace period in 2032, whether additional debt measures are needed to ensure the respect of the agreed gross financing needs targets.

A contingency mechanism on debt could be activated in the case of an unexpectedly more adverse scenario. If activated by the Eurogroup, it could entail measures such as a further re-profiling and capping and deferral of interest payments to the EFSF to the extent needed to meet the gross financing needs benchmarks of 15 to 20% of GDP.

The ESM and EFSF Board of Directors approved a series of short-term measures for Greece in January 2017, which were implemented during the course of 2017:

- Smoothing the EFSF repayment profile (increasing the weighted average maturity of loans to 32.5 years from 28.3);

- Reducing interest rate risk for Greece:

- Exchanging EFSF/ESM floating-rate bonds for fixed-rate bonds; interest rate swaps; matched funding (issuing long-term bonds that closely match the maturity of the Greek loans) for disbursements;

- Waiving the step-up interest rate margin for 2017 on an €11.3 billion EFSF loan tranche (margin of 2% had originally been foreseen).

Thanks to these measures, Greece’s debt-to-GDP ratio will be reduced by an estimated 25 percentage points until 2060, and Greece’s gross financing needs will be lower by an estimated 6 percentage points over the same period.

In its statement of 9 May 2016, the Eurogroup informed that a package of debt measures for Greece could be phased in progressively, as necessary to meet the agreed benchmark on gross financing needs and subject to the conditionality of the ESM programme. The Eurogroup said it would consider short-, medium- and long-term debt relief measures, but nominal debt haircuts were excluded.

The Greek Loan Facility is the first financial support programme for Greece, agreed in May 2010. It consisted of bilateral loans from euro area countries, amounting to €52.9 billion, and a €20.1 billion loan from the IMF. The EFSF, which was only established in June 2010, did not take part in this programme.

The Eurogroup agreed a set of measures designed to ease Greece’s debt burden and bring its public debt back to a sustainable path. These measures included:

- reducing the interest rate charged to Greece on the bilateral loans in the context of the Greek Loan Facility (GLF) by 100 basis points;

- cancelling the EFSF guarantee commitment fee of 10 basis points (it is estimated that this will save a total of €2.7 billion over the entire period of EFSF loans to Greece);

- extending the maturity of GLF loans by 15 years to 30 years (to 2041); extending the EFSF weighted average maturities by 15 years to 32.5 years, thus significantly improving the country’s debt profile;

- deferring interest rate payments on EFSF loans by 10 years until the end of 2022 (it is estimated that this will lower the country’s financing needs by €12.9 billion);

- passing on to Greece an amount equivalent to the income of the ECB’s Securities Markets Programme (SMP) portfolio accruing to their national central bank.

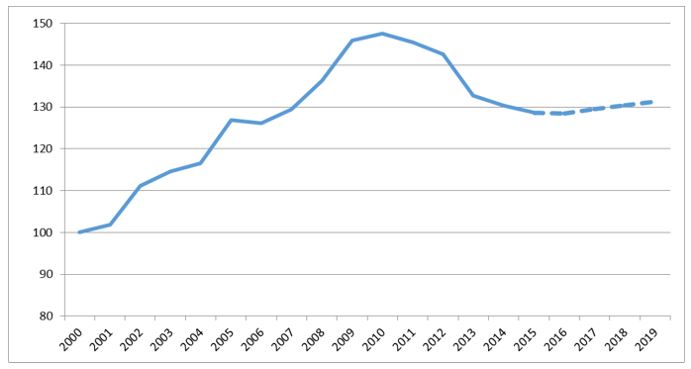

Greece has managed to significantly reduce its macroeconomic and fiscal imbalances. An unprecedented fiscal adjustment has resulted in a decline of the general government deficit by roughly 16 percentage points of GDP, to a surplus of 0.8% in 2017 from a deficit of 15.1% in 2009. Economic growth has returned as the recovery has begun to take hold, rebounding from -5.5% in 2010 to 1.4% in 2017. The Greek economy has improved its competitiveness by reducing unit labour costs.

Nominal unit labour costs in Greece (2000=100)

Source: European Commission

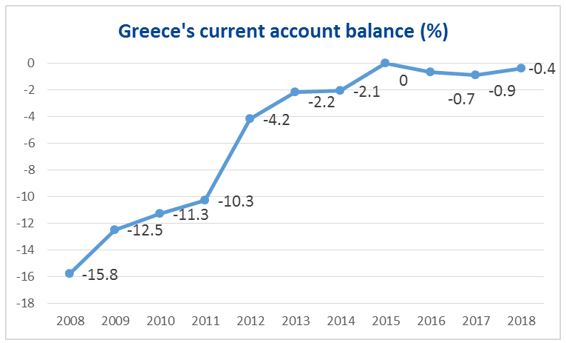

The improvement can also be seen in the falling current account deficit: to -0.4% in 2018 from -15.8% in 2008.

Greece’s current account balance 2007-2018

Source: European Commission

In 2010 unemployment was at 12.7%. After reaching a peak of 27.5% in July 2013, it has now decreased to 19.5% in May 2018. While unemployment is still the highest among all EU countries, labour market conditions continue to improve. The reduction in 2017 was the greatest single year decline since the peak in 2013. More than 100,000 new jobs have been created since the start of the ESM programme in 2015.

Yes. Before the capital raising, the banks’ bondholders and holders of preferred shares voluntarily exchanged their securities for equity capital. Another option for the banks was to sell units or wind down non-core business. These measures enabled all four systemic Greek banks to meet their capital shortfalls under the baseline scenario.

Two of the banks, Alpha Bank and Eurobank, raised enough capital to also meet the adverse scenario; they did not require further funds. Piraeus Bank and NBG required additional state aid through the Hellenic Financial Stability Fund (HFSF), which is funded by loans from the ESM.

Also known as the PSI (private sector involvement) or private sector haircut, it was a restructuring of Greek debt held by private investors (mainly banks) in March 2012 to lighten Greece’s overall debt burden. About 97% of privately held Greek bonds (about €197 billion) took a 53.5% cut of the face value (principal) of the bond, corresponding to an approximately €107 billion reduction in Greece’s debt stock.

The EFSF encouraged bondholders to participate in the restructuring. It provided EFSF bonds as part of two facilities to Greece. These were the:

- PSI facility – as part of the voluntary debt exchange, Greece offered investors 1- and 2-year EFSF bonds. These EFSF bonds, provided to holders of bonds under Greek law, were subsequently rolled over into longer maturities.

- Bond interest (accrued interest) facility – to enable Greece to repay accrued interest on outstanding Greek sovereign bonds under Greek law which were included in the PSI. Greece offered investors EFSF 6-month bills. The bills were subsequently rolled over into longer maturities.

Greece has received a total of €288.7 billion in rescue loans since 2010. The details are shown below:

Euro area, EFSF/ESM and IMF assistance for Greece

| Financial assistance programmes for Greece | Disbursed (€ billion) | |

| 1st programme | GLF (euro area) IMF Total |

52.9 20.1 73.0 |

| 2nd programme | EFSF IMF Total |

141.8 12.0 153.8 |

| 3rd programme | ESM | 61.9 |

| Total from euro area, EFSF and ESM Total from IMF Total loans disbursed |

256.6 32.1 288.7 |

|

The total amount disbursed by the EFSF and the ESM to Greece is €203.7 billion.

The EFSF disbursed €141.8 billion in loans to Greece from 2012 to 2015. The EFSF programme was part of the second programme for Greece. The IMF contributed €12 billion in loans under the programme.

The disproportionate growth in the real estate sector, along with the expansion of credit to finance it, were the main reasons behind Spain’s economic imbalances. In the real estate sector, a spiral of growth in demand, prices and supply caused a major bubble, which burst when the impact of the international financial crisis was felt in Spain. The massive scale of loans for construction and property development caused an excessive exposure of the banking industry to those sectors. In particular, Spain’s savings banks (Cajas de Ahorros) were affected by solvency problems.

A restructuring process was started by the Spanish authorities in 2010. However, the economic downturn turned out deeper and longer than expected. The funding costs for Spain as well as Spanish banks significantly increased. These market conditions raised widespread concern that private and public resources would be insufficient to support the banking system with capital.

In June 2012, the Spanish government made an official request for financial assistance for its banking system to the Eurogroup for a loan of up to €100 billion. It was designed to cover a capital shortfall identified in a number of Spanish banks, with an additional safety margin.

In December 2012, the Spanish government formally requested the disbursement of €39.47 billion via a dedicated ESM loan for the recapitalisation of the banking sector. The funds were transferred in the form of ESM notes on 11 December 2012 to the Fondo de Restructuración Ordenada Bancaria (FROB), the bank recapitalisation fund of the Spanish government. The FROB used these notes for the recapitalisation, in an amount close to €37 billion, of the following banks: BFA-Bankia, Catalunya-Caixa, NCG Banco and Banco de Valencia. Additionally the FROB was to provide up to €2.5 billion to SAREB, the asset management company for assets arising from bank restructuring.

In January 2013, the Spanish government formally requested the disbursement of €1.86 billion for the recapitalisation of the following banks: Banco Mare Nostrum, Banco Ceiss, Caja 3 and Liberbank. The funds were transferred to the FROB in the form of ESM notes on 5 February 2013.

No further requests for disbursement were made, thus the overall amount of financial assistance provided by the ESM to Spain was €41.33 billion. This was the only instance so far when the ESM indirect recapitalisation loan was used.

In the case of Spain, conditions were strictly directed to the banking sector. There were three main conditions: first, identifying individual bank capital needs through an asset quality review of the banking sector and a bank-by-bank stress test. Second, recapitalising and restructuring weak banks based on plans to address any capital shortfalls identified in the stress test. Finally, problematic assets in those banks receiving public support (without any credible plans to address their capital shortfalls by private means) were to be segregated and transferred to an external asset management company (Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria – SAREB).

In addition, conditionality was also applied in order to strengthen the banking sector as a whole. This included regulatory capital targets, bank governance rules, an upgrade of reporting requirements and improved supervisory procedures.

Yes, the European Commission was closely involved in the bank recapitalisation process and approved the state aid for the recapitalisation of the banks concerned.

No, the IMF did not make a financial contribution because unlike the ESM, it does not have a financial assistance tool related to bank recapitalisation. The IMF was only involved in an advisory and monitoring capacity.

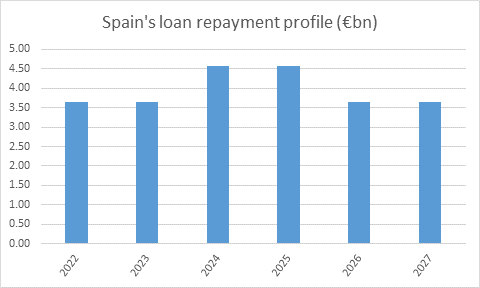

Spain was scheduled to repay the loan principal from 2022 to 2027. However, starting in July 2014, the Spanish government made the first in a series of early repayments to the ESM. To date, Spain has repaid €29.5 billion (out of the total loan amount of €41.3 billion).

ESM assistance was key in cleaning the balance sheets of troubled banks, improving their capital base, and overcoming market fears about the depth of the problems in Spain’s financial sector.

Cyprus’s accession to the EU in 2004 and its adoption of the euro in 2008 contributed to a rapid growth of the financial sector and expansion of bank lending. At its height in 2009, the Cypriot banking sector was equivalent to nine times the country’s GDP, compared to the current ratio of 3.5 times GDP (close to the EU average). In addition, high current account deficits were recorded, and exports dropped due to Cyprus’s falling competitiveness.

The banking sector was increasingly cut off from international market funding and Cyprus’s largest banks recorded substantial capital shortfalls against the backdrop of the exposure to the Greek economy and deteriorating loan quality. Bank credit policy, poor risk management practices and insufficient supervision contributed to the problems. The excessive budget deficit limited Cyprus’s ability to help when the banks were on the verge of collapse.

The total amount of financial assistance agreed in 2013, in support of Cyprus’s macroeconomic adjustment programme, was up to €10 billion. However, thanks to the rapid economic recovery made by Cyprus, the full amount was not needed. The ESM disbursed €6.3 billion, and the IMF disbursed a further €1 billion.

The key conditions of the programme were:

- to restore the soundness of the Cypriot banking sector and rebuild depositors' and market confidence by thoroughly restructuring and downsizing financial institutions;

- to continue the process of fiscal consolidation to correct the excessive general government deficit, in particular through measures to reduce current primary expenditure and to increase the efficiency of public spending; and

- to implement structural reforms to support competitiveness and sustainable and balanced growth, allowing for the unwinding of macroeconomic imbalances.

Cyprus restructured and recapitalised its banks, which are now about half the size they were before the crisis. It has also improved financial regulation and supervision. It has introduced modern insolvency and foreclosure laws to facilitate restructuring of non-performing loans in a cooperative manner.

Restrictive measures had to be introduced to protect the financial stability of the Cypriot banking system. This refers in particular to preventing large deposit outflows and preserving the solvency and liquidity of credit institutions. The capital controls were gradually eased and they were fully lifted in April 2015.

Cyprus returned to the bond market in June 2014, when it issued a 5-year bond at a yield of 4.85%. Just one year earlier, in July 2013, the corresponding bond yield had been almost 14%, which shows how quickly Cyprus regained the trust of investors thanks to the implementation of reforms.

Cyprus resumed economic growth in 2015 (1.7%) after three years of recession; growth has been strong (2.8% in 2016) and is expected to continue in 2017 (2.5%). The country reduced its public deficit from nearly 6% in 2012 to a surplus of 0.4% in 2016. The oversized financial sector was significantly downsized and restructured. Capital controls and the economic adjustment programme helped stabilise deposits and the liquidity of the banking system. Unemployment has been gradually declining since 2014. Cyprus has returned to market financing and, with a cash buffer of over €1 billion, no longer requires financial assistance.

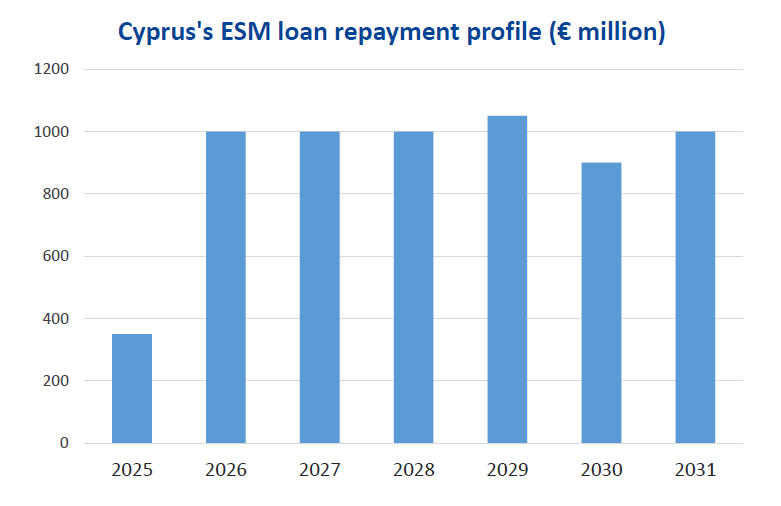

Cyprus will repay the principal on ESM loans from 2025 to 2031.

Portugal had suffered from low GDP and productivity growth for more than a decade before the crisis started. During this period, the low interest rates resulting from adoption of the euro boosted private and public consumption, but also indebtedness. Portugal’s competitiveness was undermined by rising labour costs and structural problems. Growth in public spending was much higher than economic growth. Fiscal risks intensified through the expansion of state-owned enterprises and public-private partnerships. In early 2011, rising sovereign yields drove Portugal into a severe economic crisis. The country became unable to refinance its debt at sustainable rates and therefore requested financial assistance from the EFSF, the EU and the IMF.

The programme for Portugal was agreed as follows:

€78 billion in external support over three years, comprising- €26 billion from the EFSF;

- €26 billion from the EFSM (European Financial Stabilisation Mechanism – an EU facility funded through bonds issued by the European Commission);

- €26 billion from the IMF.

No. Each of the three programme financing institutions (EFSF, IMF and EFSM) committed €26 billion to support Portugal’s programme, but the country did not request the last loan tranche from the EFSM and IMF. Additionally, Portugal has already started making loan repayments to the IMF, reducing their outstanding amount with the fund. This makes the EFSF currently Portugal’s largest creditor (€26 billion in loans).

The financial assistance provided was conditional upon the implementation of a macroeconomic adjustment programme, with reforms in three main areas:

- A fiscal consolidation strategy, supported by structural-fiscal measures, aimed at setting the debt/GDP ratio on a downward path in the medium term;

- Structural reforms to boost potential growth, create jobs, and improve competitiveness;

- Stabilisation of the financial sector strategy based on recapitalisation and deleveraging, with efforts to safeguard the financial sector against disorderly deleveraging through market-based mechanisms supported by backstop facilities.

The majority of the EFSF programme amount was used for budget financing needs, while a smaller portion was used for the purpose of recapitalisation of banks (Millennium, Banco BPI and Caixa General de Depositos).

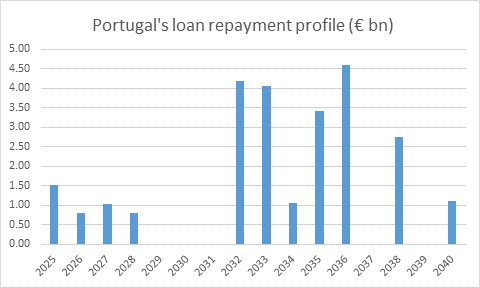

Portugal will repay the principal of the loan tranches starting from 2025, and the repayment is scheduled to end in 2040. An early repayment of €2 billion was made to the EFSF on 17 October 2019.

Portugal returned to bond markets in May 2013, when it issued a 10-year bond with a yield of 5.67%. This shows that investors had quickly regained confidence in the Portuguese economy, as Portugal’s 10-year bond yields were over 16% in January 2012.

Thanks to the implementation of reforms, Portugal has been successful in improving public finances, reinforcing the financial sector and bringing the economy back on a path of recovery. Portugal returned to economic growth in 2014 after four years of recession (1.4% in 2016, 1.8% predicted in 2017). Fiscal adjustment has been significant, with Portugal’s public deficit dropping from over 10% in 2009 to 1.8% (predicted) in 2017.