Mind the gap – how a European risk-sharing scheme could bolster private insurance coverage of natural catastrophes

Recent flooding events in Europe, as well as reports that insurers globally are becoming reluctant to offer homeowners protection against natural catastrophe losses in certain regions, have fuelled discussions about the role of insurance coverage in limiting the economic and societal consequences of climate risks.

The increasing uncertainty surrounding such risks has caused insurance premia to rise, putting further pressure on already low protection levels. The so-called protection gap, the difference between economic and insured losses, is hence likely to widen unless measures are taken to reduce it.

In addition to measures to mitigate climate change, private and public risk-sharing models can play a role in making the economy more resilient to climate risks, through reducing the insurance protection gap.

This blog discusses how private and public schemes can reinforce each other, thus reducing the fiscal burden of natural catastrophe losses. The principles that underpin the design of the ESM backstop for the Single Resolution Fund (SRF) may serve as a blueprint for developing a public scheme.

Climate change aggravates natural catastrophes

The floods in Slovenia and Greece this year are reminders of the devastating impact of natural disasters. Because of climate change, such events are becoming even more widespread and impactful. At the same time, insurance coverage against natural hazards remains low. According to the European Environment Agency, only 30% of economic losses from weather and climate-related events are insured (see Figure 1), with considerable variation, depending on the type of hazard and country. This leaves a significant protection gap that needs to be filled. In addition to the human suffering and loss of wealth that natural disasters entail, they also put a burden on governments, which are often expected to step in and compensate uninsured losses.

Figure 1: More than two-thirds of natural catastrophes remain uninsured - losses resulting from European natural catastrophes (in 2021 prices)

Note: Data cover the EU 27. Meteorological events: storms, mass movements (e.g. landslides, subsidence); hydrological events: floods; climatological events: heat waves, cold waves, droughts, forest fires

Source: European Environment Agency. The losses cover the period 1980 to 2021

Private sector solutions hampered by uncertainty

Private sector solutions are constrained by both demand and supply-side factors. When it comes to demand, consumers may underestimate the risks they are exposed to, both in terms of frequency of occurrence and impact. They may expect the government to intervene in case of a catastrophic event. On the supply side, insurers are confronted with increasing uncertainty related to the frequency and impact of natural catastrophe losses, which their analytical models do not sufficiently account for. To compensate for this uncertainty, insurers are raising insurance premia. Global property catastrophe reinsurance premia have increased by 10% to 50% in 2023 [1] and are expected to rise further in 2024.[2]

This leads to a vicious circle: The higher cost of insurance is making the public even less inclined to purchase protection against natural catastrophe losses. Low coverage, however, impairs the ability of the public to manage the associated risks, which consequently could fuel financial stability concerns.

The purpose of insurance is ultimately to pool risks, lowering the amount that individuals must set aside to cover for future losses, or the time it would take to pay for repairing the damage. Low or falling insurance coverage reflects an economic inefficiency that can weigh on an economy’s performance and ultimately make it more prone to crises.

When citizens turn to governments to step in, fill the gap and to compensate for uninsured losses, this has wider implications: low insurance coverage also raises concerns related to public debt sustainability – a key issue for the ESM. [3]

Bolstering private insurance coverage for natural catastrophes

What can be done? Solutions to this challenge should ideally fulfil the following requirements:

- They lead to efficient risk-sharing across all affected parties,

- They create incentives for climate change mitigation and adaptation measures,

- The intervention is net beneficial, i.e. the benefits outweigh the costs relative to the status quo.

Private sector solutions are key to enhancing natural catastrophe resilience. As a first resort, additional innovative solutions should hence ideally be sought by the industry.

On the demand side, such measures may include risk-based premia or deductibles that encourage policyholders to take mitigating actions to reduce their exposure. Policyholders should also be urged to adopt Environmental, Social and Governance practices. This would reduce their vulnerability to climate related risks, for instance, by investing in protection measures that limit the damage when a flood or other natural catastrophe occurs.

On the supply side, natural catastrophe insurance could be made an integral part of property, fire, or other relevant insurance, with an opt-out clause instead of an opt-in. This could help increase market coverage, along with other measures to raise risk awareness.[4]

A pan-European reinsurance pool for natural catastrophe losses is an example of a private sector initiative that could improve the risk-bearing capacity of European primary insurers. The development of capital market solutions via the issuance of insurance-linked securities (e.g. catastrophe bonds) could further contribute to the broadening of private sector risk bearing capacity.

Also, innovations such as parametric insurance, a non-traditional insurance solution that offers pre-specified payouts upon a trigger event, may deserve further consideration. A combination of all these measures, however, may still be insufficient to achieve the desired level of protection against extreme events.

A public backstop to catastrophe insurance at supranational level can serve as a reinforcement of private sector solutions. The European Insurance and Occupational Pensions Authority and the European Central Bank in their discussion of the role of public sector involvement, emphasised the need to avoid providing blanket guarantees for uninsured losses but to enhance efficiency in the use of public funds and reduce moral hazard. [5]

By reducing the cost of uncertainty, a European backstop could strengthen private sector solutions and provide coverage for risks that are considered uninsurable after all private sector solutions are exhausted. To reduce moral hazard, the public sector involvement needs to be clearly delineated, defined ex ante and credible, i.e. not renegotiable after an event.

A public backstop as a fiscally neutral and last resort measure

The immediate goal of a European backstop would be to boost private sector solutions and limit the fiscal burden for governments. The principles that underpin the design of the ESM common backstop to the Single Resolution Fund may serve as a blueprint for the design of a European insurance backstop.[6] In the case of the backstop to the SRF, the ESM will act – under certain conditions – as a “reinsurer of last resort” against an extreme event: the resolution of failing banks whose costs exceed the resources of the SRF.

Another cornerstone of the ESM backstop is the principle of “fiscal neutrality” in the medium term: interventions will allow sufficient time for the industry to absorb the costs of the required financial assistance, so that they are not borne by the taxpayer.

A similar role could be played by an insurance backstop for natural catastrophe losses. It would put a cap on the private insurance sector’s liability in the short term and provide protection against extreme events that other market participants are unable to absorb. Its availability would not only reduce sudden spikes in claims costs due to catastrophic events but may also increase market participation upfront, in both cases limiting governmental exposure and potential fiscal burden.

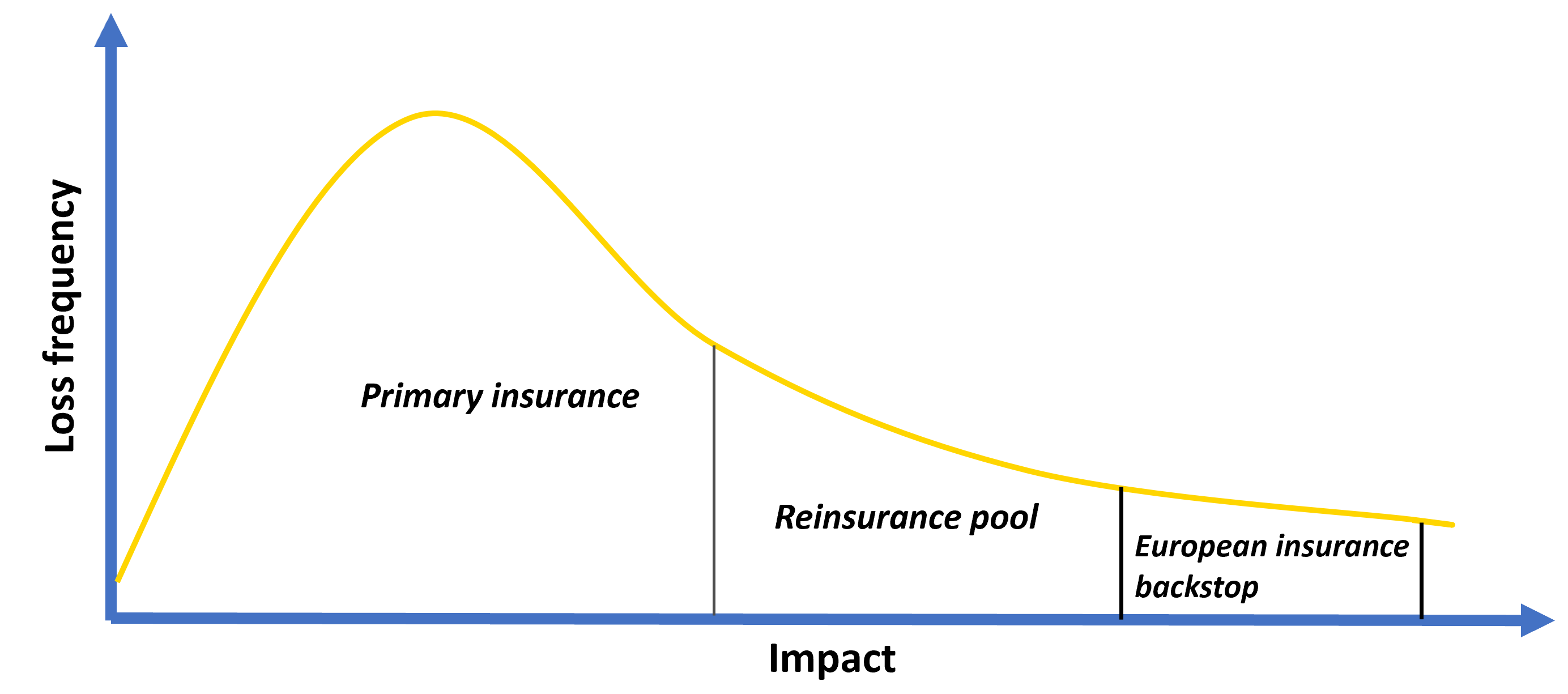

A key element in the design of an insurance backstop is the funding structure of the overall risk-sharing scheme. An upfront funded solution could involve the creation of a European reinsurance pool, whereby insurers would pay premiums into a common pool, covering losses beyond a certain threshold and up to a pre-defined maximum level (see Figure 2 for an illustration of such a loss-sharing framework). For losses exceeding the resources in the reinsurance pool, a designated European backstop authority could be mandated to grant loans to the pool, up to a pre-defined level.

Figure 2: Adequate protection rests on many shoulders – loss bearing hierarchy

(in %)

Source: ESM

The timing and impact of loss recoupment on the effectiveness of the scheme deserves further investigation. But the presence of a guaranteed public backstop would facilitate higher private sector insurance coverage by reducing uncertainty and crucially, allowing for payments of large claims to be refinanced over longer time horizons.

The proposed backstop should be seen in a broader context of both crisis recovery, as well as adaptation and mitigation measures. Both are integral parts of an overall framework, which should be urgently developed. This would be instrumental in improving the resilience of our economies and societies to natural disasters, increasingly amplified by climate change.

Acknowledgements

The authors would like to thank Nicoletta Mascher and Rolf Strauch for valuable discussions and contributions to this blog post and Karol Siskind for his editorial review.

Further reading

ECB and EIOPA (2023), “Policy options to reduce the climate insurance protection gap”, discussion paper, April 2023.

Guy Carpenter (2023), “Reinsurance market continues to recalibrate at mid-year 2023 renewals”, press release, 5 July 2023.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager