Euronomics: Resilience and competitiveness in the euro area

The euro area economy has proven resilient against the last two crises, bolstered by swift policy responses. However, shifting geopolitical landscapes and volatile energy prices have exposed vulnerabilities that threaten Europe’s future. How can Europe secure its prosperity and global relevance in a fragmented and shock-prone world? I argue that a strong European position requires a balanced approach to ensure the success of both competitiveness and resilience without compromising either.

Euro area stands at fork in the road

Despite demonstrated resilience to the more recent Covid-19 pandemic and energy crisis, productivity, and economic growth trail behind other major economies due to long-standing structural weaknesses and elevated exposure to global shocks. Such factors as ageing populations, heavy reliance on external resources and relationships, the effects of climate change, and obstacles to technological progress all impede European growth.

Europe must tackle these challenges to sharpen its competitiveness and shore up its resilience. Without policy action, Europe will remain highly vulnerable to ongoing global developments and be left behind. The right policy mix is needed to encourage and protect European prosperity.

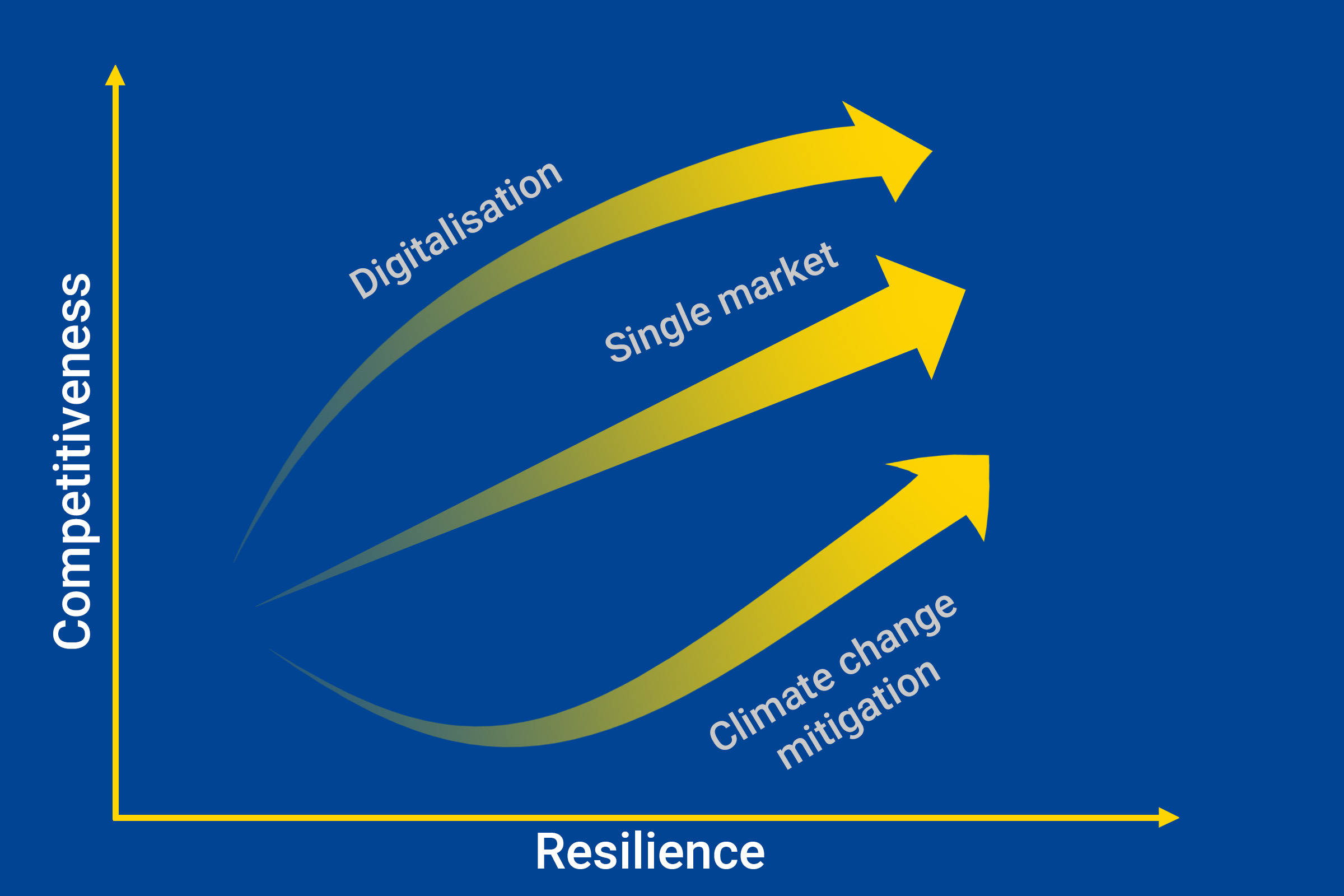

Resilience and competitiveness, strategic allies in new global era

Competitiveness and resilience can be conflicting goals. But addressing the long-term European challenges of demographics, climate change, and geo-economic fragmentation should consider both goals in tandem.

There are various elements that would help in this endeavour.

For example, the European Union (EU) single market could help overcome some aspects of geo-economic fragmentation. According to different analyses, a fully operational EU single market has the potential to unlock access to a market of around 440 million people and a diversified spectrum of firms and sectors representing around 15% of global gross domestic product (GDP). It could raise EU citizens’ welfare by between 7% to 9% of GDP in the long term [1] and strengthen European supply chains.

Additionally, digitalisation can raise productivity and growth by increasing efficiency and addressing the labour shortage that comes with an ageing society. According to available analyses, digital and high-impact technologies could bring an additional 1% annual growth to the EU in the next decade.[2] Advancing technological developments also increases strategic autonomy when it reduces reliance on global providers domiciled in the United States, China, and beyond.

Still, trade-offs that emerge need careful management, particularly in transitory periods. Policy action is needed to mitigate and adapt to the impact of climate change. Increased reliance on renewable energy and less reliance on fossil fuels reduces vulnerabilities to geopolitical turbulences and extends our economic power in the long run.[3] However, mitigating climate change and transitioning towards a net zero economy still implies sectoral shifts and costs for firms and financial institutions that will impinge on competitiveness.

Three-pronged approach to long-term success

At the European level, long-term productivity, and a stronger position from which to face challenges require three complementary and interlaced lines of action:

First, further integration of the single market with an eye towards the particularly pertinent areas of energy and finance. Though some progress has been made in the energy market as a reaction to the price shock that emerged from the Russian aggression in Ukraine, much deeper integration is necessary to exhaust its potential and increase energy efficiency and a more secure energy supply. [4] Access to finance is a necessary condition for companies to grow and invest in the green and digital transition. The well-established policy agendas for banking union and capital markets union should move to centre stage in the next institutional cycle.

Second, effective implementation of the redesigned economic governance framework to strengthen fiscal sustainability and incentivise reform and investment. Governments are set to deliver their fiscal-structural plans later this year. Once adopted, they aim to guide fiscal policy for the next four to seven years. Crisis and economic transition support can only be provided if fiscal space has been gained before such support is needed. Much of Europe’s success in dealing with long-term challenges will depend on the willingness and ability of governments to follow up on clear reform and fiscal commitments and joint ownership. Ensuring the creation of fiscal buffers for countries facing more sustainability challenges, providing the resources for investments in line with commitments under the European Green Deal, and facilitating the full implementation of the Recovery and Resilience plans are key elements adding to the quality of these plans.

Third, clarifying the European financial architecture beyond 2026 and strategic mobilisations of resources. The Next Generation EU (NGEU) initiative is the centrepiece of the joint European vision for the green and digital transition. Though NGEU will end in 2026, the need for massive investment, both public and private, and exposure to external shocks will persist, with some initiatives having extensive lead times. Building new electricity grids, for example, takes a decade. Current private investment is determined by the clarity of the future policy course. Having a view on how existing resources can be used efficiently to address the competitiveness and resilience challenges or whether more are needed is therefore a pertinent issue that needs to be resolved soon.

As a permanent crisis mechanism responsible for not only resolving but also help preventing crises, the European Stability Mechanism can advise on the build-up of vulnerabilities and risks and stands ready to provide resources when needed – making it part of the solution for a prosperous future for Europe.

Acknowledgements

The author would like to thank Pilar Castrillo and Martin Iseringhausen for valuable discussions and contributions to this blog post, and Raquel Calero for her editorial review.

Further reading

Centre for European Policy Studies (2024), “Empowering the Single Market: A 10-point plan to revive and deepen it”, CEPS In-Depth Analysis.

European Commission (2020), “Shaping the Digital Transformation in Europe”, A study prepared for the European Commission by McKinsey & Company.

European Parliament (2019), “Europe’s two trillion euro dividend: Mapping the Cost of Non-Europe 2019-24”, Study by the European Parliamentary Research Service.

European Parliament (2024), “Coordination for EU competitiveness”, Study requested by the ECON committee.

Gopinath, G. (2023), “Europe in a Fragmented World”, Remarks for the Bernhard Harms Prize.

Gourdel, R., Monasterolo, I., Dunz, N., Mazzocchetti, A. and Parisi, L. (2024), “The double materiality of climate physical and transition risks in the euro area”, Journal of Financial Stability, 71.

Kahn, M. E., Mohaddes, K., Ng, R., Pesaran, M. H., Raissi, M. and Yang, J.-C. (2021), “Long-term macroeconomic effects of climate change: A cross-country analysis”, Energy Economics, 104.

NGFS (2023), “NGFS Scenarios for central banks and supervisors”, Network for Greening the Financial System.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager