Euronomics: A fresh look at Greek debt sustainability

Greece has come a long way in the decade that followed the sovereign debt crisis, restoring sustainability to public finances, regaining market confidence, strengthening the banking sector, and improving its economic competitiveness. Though the financial burden of the current pandemic has raised debt levels and long-term risks, we are not going through another debt crisis. Greek and European Union (EU) efforts can ensure Greece’s current debt sustainability despite the remaining, long-term challenges.

Greece emerged from the past debt crisis more resilient. It conducted a number of reforms, including making the public administration more efficient, simplifying licensing, streamlining procedures, and facilitating trade. As a result, the Greek economy was structurally more resilient at the start of the pandemic than it was prior to the sovereign debt crisis. Past consolidation efforts, though quite painful, enabled the country to enter the pandemic with a very healthy budgetary position. This allowed the government to combat the effects of the current crisis with countermeasures amounting to approximately 9.4% and 6.5% of GDP in 2020 and 2021, respectively.

A new debt sustainability environment

The structure of Greek debt has much improved. This is due in large part to the ESM’s and its predecessor, the EFSF’s, very favourable lending terms and the liability management exercises under the ESM programme. The ESM holds around 55% of Greece’s public debt and the weighted remaining maturity of the ESM/EFSF loans is 31 years – much longer than that of the remaining debt stock. Due to the low interest rate on these loans – thanks to the ESM’s own low, AAA rated cost of funding over that period – Greece’s annual costs for servicing these loans is lower than expected for its total debt level.

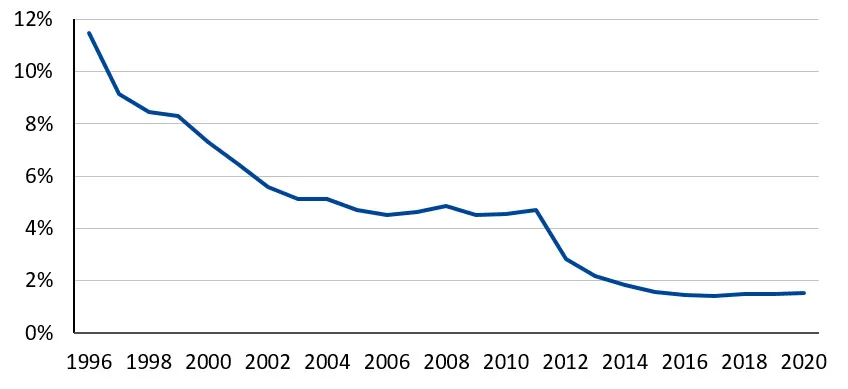

Like many other countries, Greece is benefitting from a secular decline in interest rates resulting in very favourable financing conditions. Historically low interest rates have reduced the debt service burden both as a share of overall expenditure and compared to taxation. In many respects, this is a new world for debt sustainability analyses. As we have been arguing for some time, the focus is less on the stock of debt – often measured as the debt-to-GDP ratio – but rather on budgetary flows and roll-over risks. The general decline in interest rates and the compression of risk premia has diminished the effective interest rate on Greek government debt from 7.3% in 2000 to around 1.5% in 2020. Greece is locking in current low interest rates by further extending the maturity of its issuance and through interest rate swaps.

In contrast to its situation during the financial crisis, Greece now has broader access to the European Central Bank’s (ECB) monetary policy measures. This further reduces the country’s debt servicing costs. Greece sovereign debt is now not only eligible as collateral for its main refinancing operations, but also in the ECB’s current bond purchasing programme, the Pandemic Emergency Purchase Programme (PEPP).

Effective interest rate

(in % of gross government debt)

Source: AMECO, IMF, ESM calculations

New forms of European solidarity are also benefitting Greek debt sustainability. During the financial crisis, the ESM was the main vehicle for supporting countries that lost market access at a sustainable cost. Now, the EU has added another layer of assistance to fight the current crisis with a first package of €540 billion to help countries, firms, and workers. Greece has since drawn upon the employment support scheme and participated in the guarantee scheme for firms. Additionally, EU leaders agreed upon the €750 billion Next Generation EU package to promote investment, sustainable growth, and digitalisation. Greece will receive a large share of this package, equivalent to about 17.8% of its GDP.

Both the Greek budget and its debt seem well manageable in the coming years. However, debt casts a long shadow, causing lingering challenges and risks. Future interest rates, budgetary pressure, and weak growth can lead to a higher debt-servicing burden and refinancing needs. Keeping up fiscal strength and, first and foremost, promoting growth, are the best ways for Greece to address these challenges.

Upholding market confidence and fiscal leeway

Greece needs to sustain market confidence even amidst less favourable long-term financing conditions. Once the ECB adjusts its monetary policy and asset purchasing is less available to enforce a benign market equilibrium, country risk will again play a larger role in financing costs. Interest rates will increase from their current levels. The US fiscal stimulus has already led to market volatility and somewhat higher risk-free rates in Europe. Others put forward more structural demographic changes as a possible driver of higher future interest rates.[1] Nevertheless, there are strong economic reasons to expect them to remain, on average, substantially below their levels before the introduction of the euro.

Greece will eventually have to regain its strong budgetary position and create fiscal leeway. At the moment, government support to fight the consequences of the pandemic is top priority. Support measures should remain temporary to avoid permanent budgetary pressure, and can be phased out or adjusted as the recovery gains momentum. Employment creation and the nurturing of corporate growth will need to replace the temporary measures deployed to fend off economic and social hardship. Improving the quality of public spending will play an important role during this phase.

Once recovery takes off, Greece should return to the budgetary objective agreed with euro area partners, as long as fiscal adjustments do not entrench the economic scars of the pandemic. Greece’s long-term fiscal objective of a strong budgetary position in line with the European fiscal framework will create a fiscal buffer that will prevent the country from slipping into a low-growth environment during future crises and market convolutions. This leeway will earn Greece substantial market trust.

Recovering from the pandemic and ensuring high growth potential

Enabling a strong recovery from the pandemic and therefore high growth potential is the key challenge for the Greek government. Although Greece improved its growth potential thanks to the reforms during and following the previous crisis, the pandemic may leave scars. The Greek economy is dependent on tourism – one of the sectors hit hardest by the crisis – and other service sectors that require a high a level of physical proximity. These sectors might not fully return to their pre-pandemic levels in the near future.

The €18.2 billion[2] in grants Greece will receive as part of the Recovery and Resilience Facility coupled with the National Growth Strategy should considerably help the recovery. While Greece will channel the EU funds into its economy, structural reforms under the National Growth Strategy will boost investment and growth by:

- modernising and further digitalising the public administration, especially those related to export manufacturing sectors;

- fully implementing the new insolvency framework, and settling all public-sector arrears – not only pension claims;

- improving infrastructure, particularly of transport and connectivity, through public and private investment and reducing energy costs for businesses; and

- strengthening human capital to remain competitive with extended training, upskilling, and reskilling programmes as well as vocational education.

Greece will also need to improve its absorptive capacity to make good use of EU funds and invest them in the most productive areas. This requires longer-term commitments by the Greek government beyond the current National Growth Strategy. Companies and citizens will need to maximise Greece’s growth potential and address long-term risks to debt sustainability.

Greece, like most developed economies, faces long-term population aging that increases the urgency for boosting productivity and encouraging investment, as these challenges will dampen labour’s future contribution to growth. Climate change poses other future risks.

The needs and challenges Greece and other EU countries face in the coming years will be supported by common initiatives beyond the Next Generation EU package. This includes the ESM’s new mandate as the common backstop to the Single Resolution Fund as another step towards the completion of banking union, the capital markets union, and the European Commission’s non-performing loans action plan. They will allow the financial sector to finance the recovery, which will alleviate budgetary pressures and thereby contribute to debt sustainability. The Commission is also set to review the fiscal framework to make it more effective and better suited to the current fiscal challenges.

Greek and EU efforts can ensure Greece’s debt sustainability in the coming years. Upholding fiscal strength and promoting growth potential by making the best possible use of the EU’s support are the best way to address remaining, long-term challenges.

Acknowledgements

I would like to thank Marialena Athanasopoulou, Paolo Fioretti, Brenda Nolden, and Markus Rodlauer for their valuable contributions to this blog.

Footnotes

Goodhart, Charles and Manoj Pradhan (2020) The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival. Springer Nature

According to the Greece 2.0 National Recovery and Resilience Plan

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager