Commercial real estate and financial stability – this time, it’s different

Commercial real estate markets are under pressure in Europe and beyond as prices fall and activity has stalled in many countries. The commercial real estate sector poses risks to euro area banks and financial stability. More than a decade ago, the European Stability Mechanism was called in to rescue countries drawn into a sovereign-bank doom loop caused by a bursting real estate bubble. But today, the risks appear less systemic than in the past and banks are better equipped to face the pressures. In this blog, we use our past crisis experience to examine the current situation and explain why we are not likely to face the same predicament.

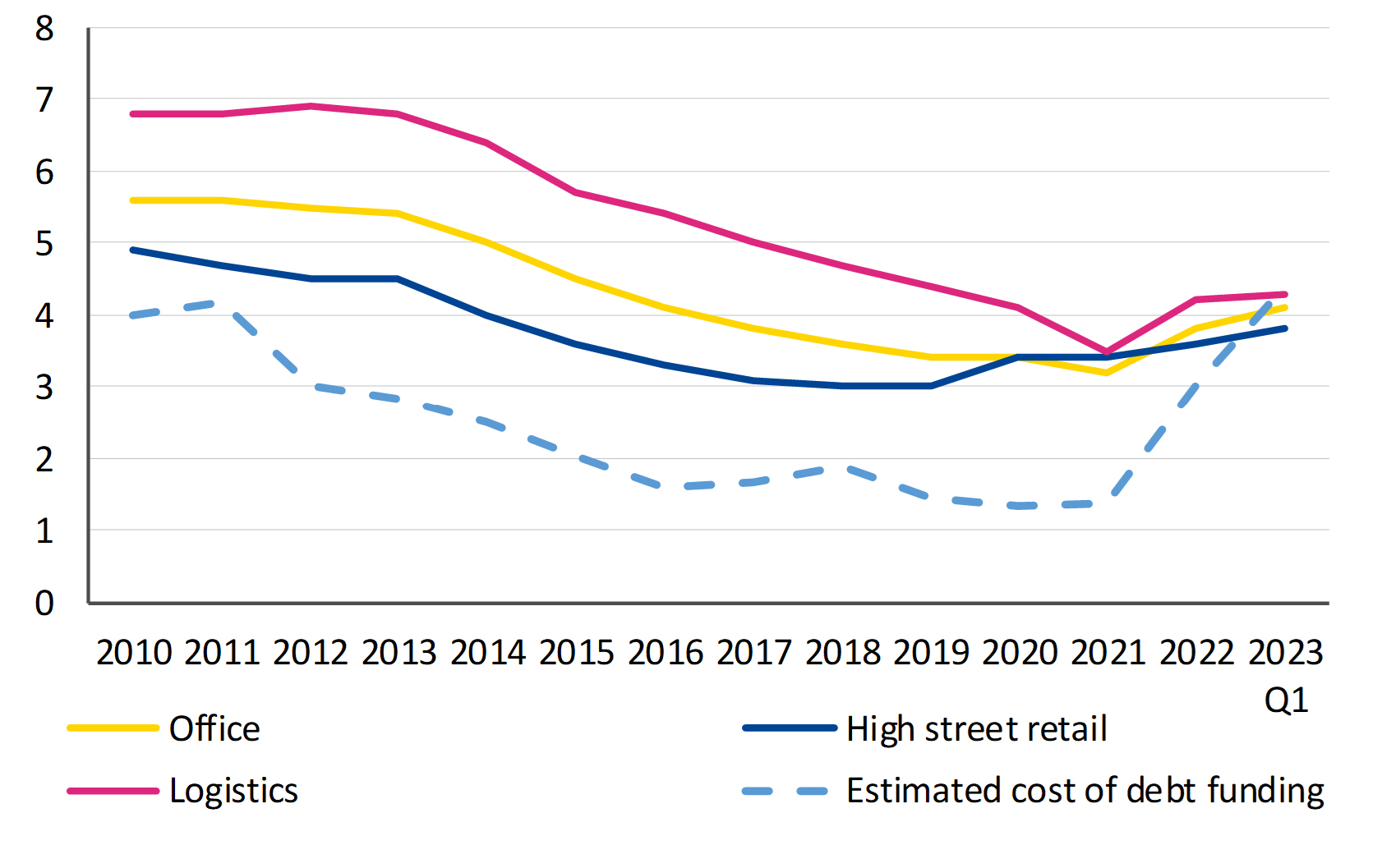

Commercial real estate woes can threaten financial stability and European banks in the current environment of high inflation and fast-rising interest rates. Rising interest rates narrow commercial real estate firms’ profits because they tend to rely heavily on debt financing and the cost of servicing debt becomes burdensome. During a decade of low interest rates from 2012–2022, investors searching for yields drove up commercial real estate property prices, compressing rental yields (see Figure 1). At the same time, commercial real estate firms in many countries increased their leverage, meaning that relatively small increases in debt servicing costs could turn profits into losses.

Figure 1: European commercial real estate property yields and estimated cost of debt funding

(in %)

Note: The cost of commercial real estate debt funding has been estimated by adding an assumed 200 basis point spread to the five-year benchmark government bond yield for the euro area.

Sources: BNP Paribas Real Estate, European Central Bank, ESM calculations.

Heavy reliance on debt financing at high costs squeezes profits, pressurising real estate prices and freezing the market in some countries. Commercial real estate prices tend to be more volatile and adjust faster than residential house prices. This accelerates the impact for financial institutions. The price correction has been relatively orderly compared to the past, with commercial real estate prices in the euro area starting to fall in 2022 and the trend continuing in the first quarter of 2023. This has caused rental yields to recover somewhat, but the adjustment has been slower than the increase in interest rates, with yields still below their historical margin to the risk-free interest rate (see Figure 1). This indicates there is further room for price adjustments.

The profitability of commercial real estate firms is generally closely linked to the value of the properties they hold, which are in turn used as collateral for bank loans. An increased risk of defaults by commercial real estate counterparties on their bank loans correlates to a devaluation of the assets held as collateral for those loans, increasing the scale of credit losses should banks need to repossess the collateral and sell it.

Structural factors have further reduced the demand for commercial real estate properties in subsegments such as retail and office space. E-commerce and teleworking have reduced demand in the retail and office sectors, while climate regulations have increased costs for new construction projects and lowered demand for existing spaces with lower energy efficiency. These factors have been at work for some time, but their impact on profitability has been magnified by the onset of monetary policy tightening.

Banks and commercial real estate exposures – past and present

Euro area banks, a key financing source for the commercial real estate sector, are exposed to financial stability risks posed by the sector. During the sovereign debt crisis, this risk materialised when a concentration of real estate lending across the banking system and rapid credit growth launched by a structurally flawed banking sector soured markets, eventually causing banks to collapse. [1]

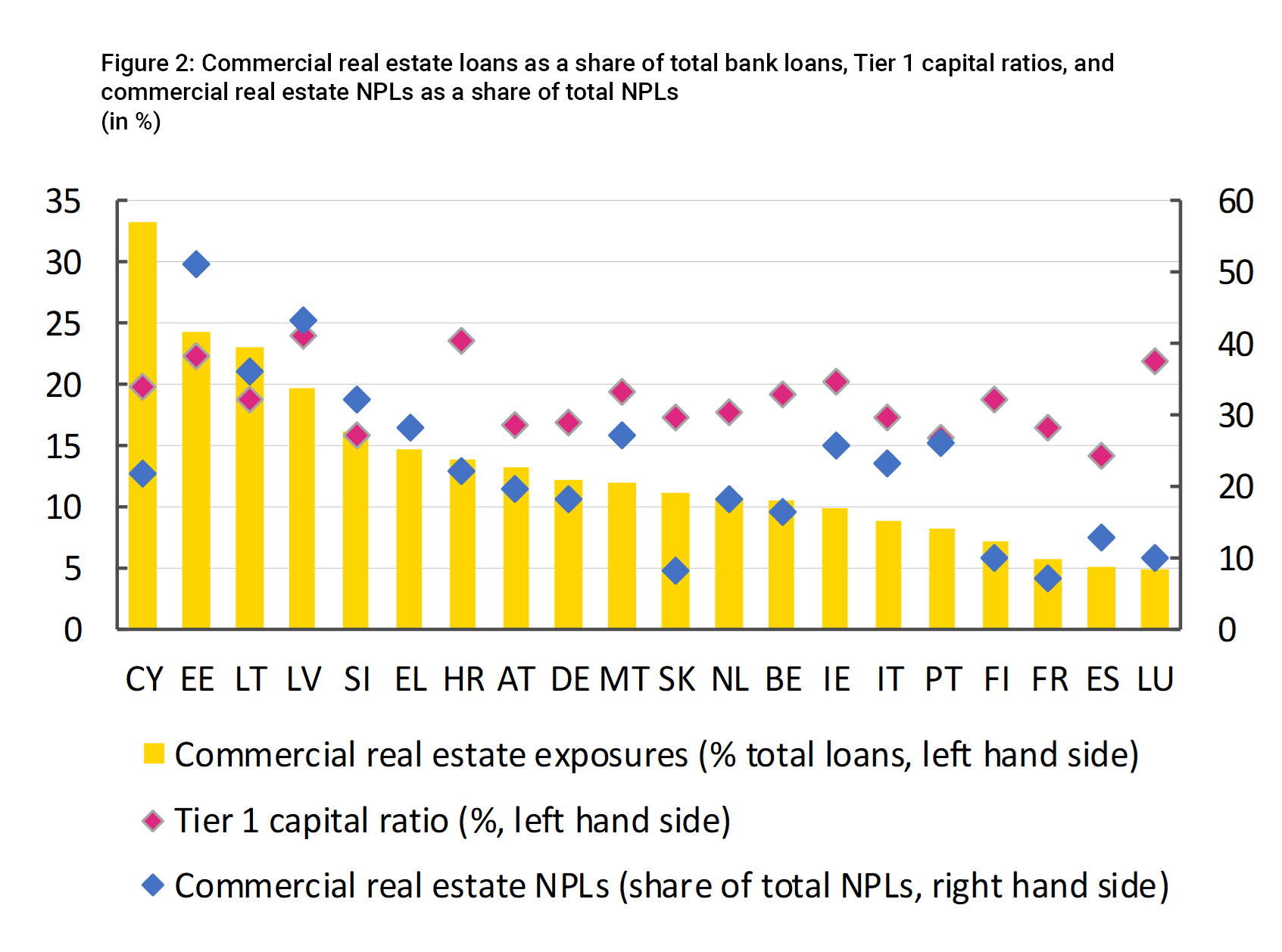

Today’s commercial real estate exposure in the banking sector shows some countries’ magnitudes comparable to the past, but banks are much better placed to absorb losses. Baltic banks have particularly high exposure to the commercial real estate sector, and the sector’s share of non-performing loans (NPLs) is also high (see Figure 2), although overall NPL ratios in the Baltic region are low. These extreme levels of concentration match those in Ireland and Spain 15 years ago.[2] For most countries, the exposure to the commercial real estate sector is much smaller. More importantly, banks nowadays have more capital and can absorb larger losses than in the past. Overall, the capital base of euro area banks has doubled. Banks are also required to issue additional instruments that can absorb losses in a crisis. This makes a systemic crisis much less likely.

Figure 2: Commercial real estate loans as a share of total bank loans, Tier 1 capital ratios, and commercial real estate NPLs as a share of total NPLs

(in %)

Source: European Banking Authority Risk Dashboard. Data as of December 2022.

Asset quality in commercial real estate portfolios remains relatively high. The level of NPLs is at or below historical averages for most countries, and credit losses related to commercial real estate exposures are likely to be manageable for the respective banking systems. The commercial real estate sector, however, accounts for a relatively high, and in some cases an increasing, share of NPLs in countries with highly concentrated exposures (see Figure 3). Estonia, Ireland, and Malta stand out as countries with a relatively high and sharply increasing share of NPLs.

Figure 3: Change in commercial real estate NPLs as a share of total NPLs 2019–2022

(in %)

Source: European Banking Authority Risk Dashboard.

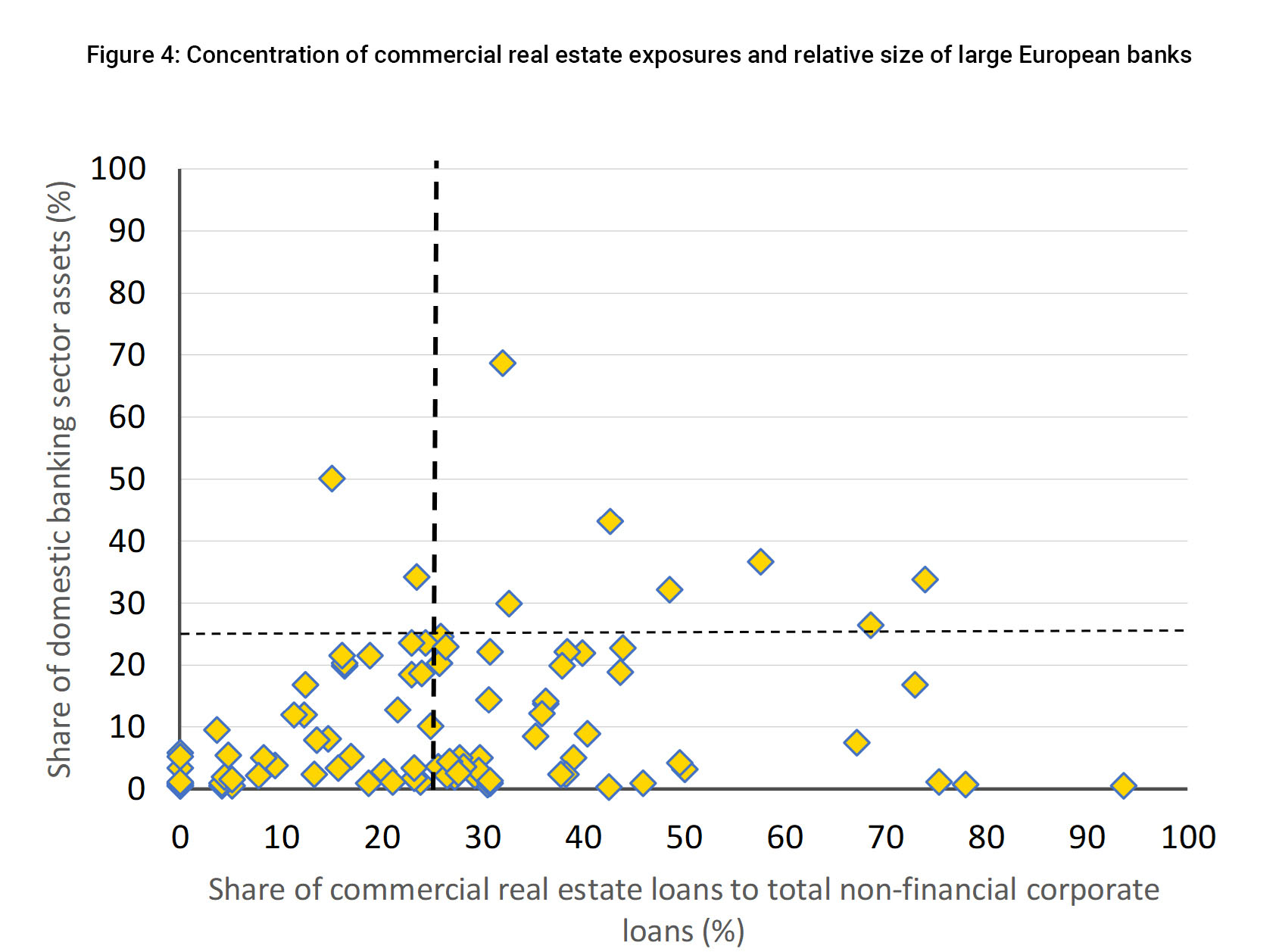

A subset of banks in the euro area have exceptionally high exposures to the sector (see Figure 4). In some cases, they represent banks that are systemically important in their domestic national market in terms of share of total banking sector assets. This matters for the aggregate risk as problems or even failures of bigger banks are more likely to affect market sentiment than those of smaller institutions.

Figure 4: Concentration of commercial real estate exposures and relative size of large European banks

Notes: The y-axis shows the relative size of each bank, measured as the proportion of its assets to total domestic banking sector assets, for a sample of 92 large euro area banks. Data as of June 2022.

Sources: European Banking Authority Transparency Exercise, European Central Bank, and ESM calculations.

Interconnectedness with the investment fund sector

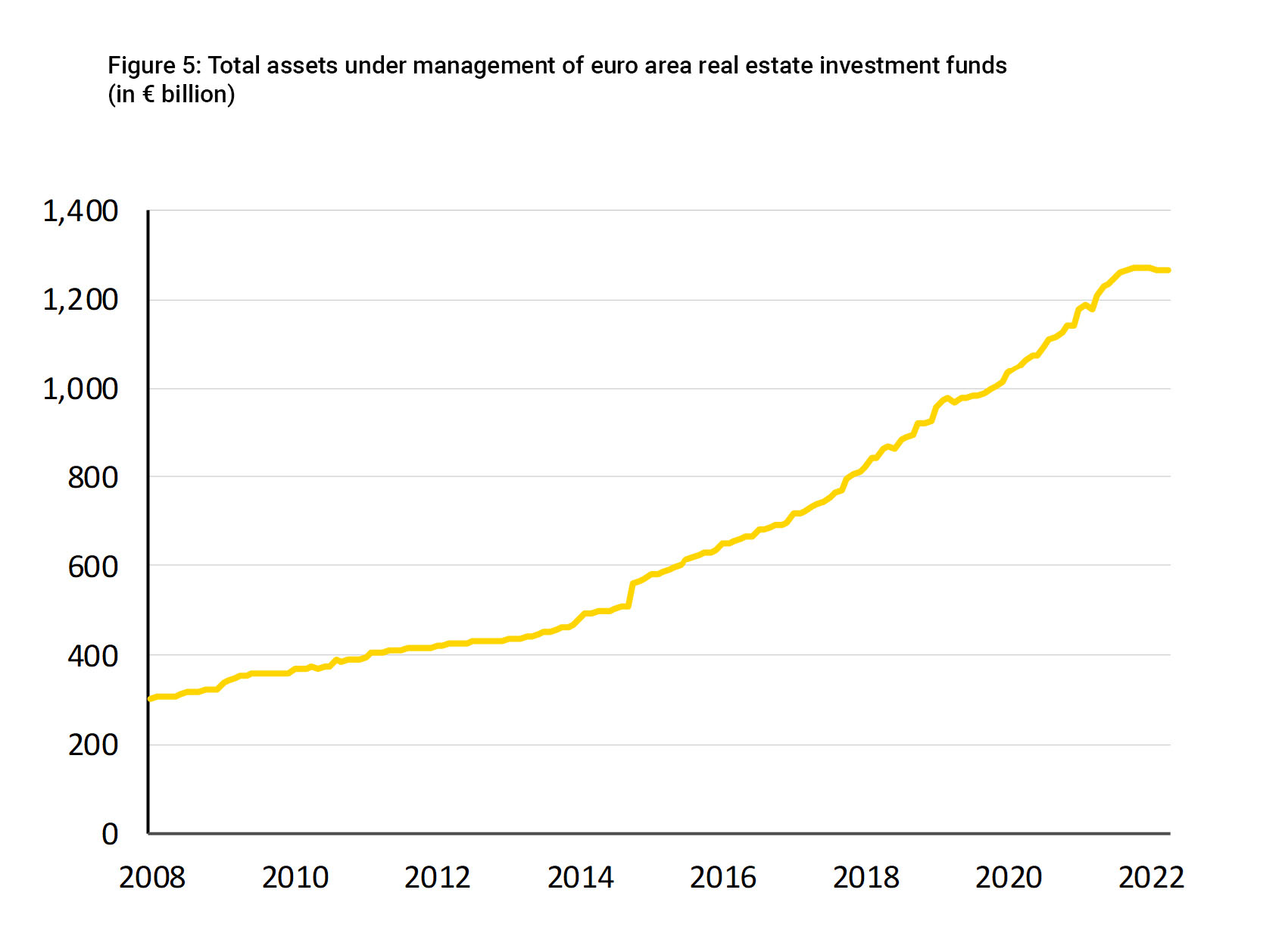

Over the past decade, investment funds have grown to become a major source of financing for commercial real estate projects. Since 2008, total assets under the management of euro area investment funds that invest in real estate properties have more than quadrupled (see Figure 5).

Figure 5: Total assets under management of euro area real estate investment funds

(in € billion)

Source: European Central Bank.

In the euro area, a significant share of the total assets under management are managed by open-end funds. Open-end real estate funds manage assets worth around €1 trillion, which represents 80% of total assets under management. Open-end funds are a source of vulnerability for the sector due to the mismatch between the liquidity of the assets and the redemption terms. This mismatch also creates a first-mover advantage, which can give rise to a spiral of redemptions and falling asset values. However, fund managers have recourse to means for reducing this risk, e.g. redemption fees and gates.

An increase in redemptions from real estate investment funds can create spillovers to the banking sector. If funds must sell commercial real estate properties to finance redemptions, it could create an excess of supply on the market. This makes it harder for banks to sell properties repossessed as collateral for defaulted loans. Redemption volumes from euro area real estate funds have been increasing in recent years, but the levels are not alarmingly high.

Financial stability at risk?

Although the commercial real estate sector represents a risk to financial stability in the current economic environment, it appears less of a systemic threat than in the past. Regulators and supervisors have forced banks to hold more capital to absorb losses and higher liquidity buffers to manage deposit outflows, along with hybrid instruments that can be written down in a crisis. This is confirmed by the recently published results of the 2023 European Banking Authority stress test, which show that European banks remain resilient under an adverse scenario that combines a severe EU and global recession.[3] In addition, commercial real estate firms rely more on market-based debt financing now than in the past. Bonds and commercial paper issued by commercial real estate firms are typically unsecured and thus sit lower in the hierarchy of claims compared to secured bank loans. This means that the cost of an increase in insolvencies in the sector may be borne more heavily by investors in capital markets this time around.

Market intelligence we have gathered also suggests that banks have learned from past crises and now have more prudent lending standards in place. Banks now put more emphasis on cash flow and income-generating capacity, and less on collateral values. This does not mean that commercial real estate risk management and underwriting standards in banks are without flaws. The European Central Bank’s commercial real estate campaign still found significant shortcomings in the areas of loan origination, monitoring, and collateral valuation, among others.[4]

While the banking sector is more resilient overall, banks with concentrated exposures to the sector may still be vulnerable. And banks with loans to commercial real estate firms that also rely heavily on market-based financing might face a difficult dilemma whether to refinance this funding as it falls due, as the cost of issuing corporate bonds has risen steeply, particularly for non-investment grade issuers. While doing so could break the covenants of existing loan terms, banks may be tempted to practice forbearance to avoid a default. If the borrower is under strain, doing so may help to buy some time, but there is also a risk that the loan will turn into a larger credit loss at a later stage.

National authorities could help to further mitigate the risk through more proactive use of the macroprudential toolkit. For instance, the Capital Requirements Directive (art. 133) has recently (as of 2022) been amended to include a sectoral systemic risk buffer that can be used explicitly for real estate exposures. National authorities could also consider encouraging more broad-based adoption of liquidity management tools by open-end real estate investment funds.

Acknowledgements

The authors would like to thank Cédric Crelo, José Cunha, and Nicoletta Mascher for valuable discussions and contributions to this blog post and Raquel Calero for her editorial review.

Further reading

Baudino, P., Herrera, M. and Restoy, F., “The 2008–14 banking crisis in Spain”, FSI Crisis Management Series no 4, July 2023.

European Banking Authority, “2023 EU-wide stress test results”, July 2023.

European Central Bank, “Commercial real estate: connecting the dots”, Supervision newsletter, August 2022.

Regling, K. and Watson, M., “A Preliminary Report on The Sources of Ireland’s Banking Crisis”, Report commissioned by the Government of Ireland, May 2010.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager