Savings and Investments Union: achieving equality and inclusion - speech by Rolf Strauch

Rolf Strauch, ESM Chief Economist

Keynote speech “Savings and Investments Union: achieving equality and inclusion”

Florence School of Banking and Finance Annual Conference 2026

Florence, 06 March 2026

(Please check against delivery)

Good morning, ladies and gentlemen. It is a great pleasure for me to speak at this conference, alongside so many distinguished experts.

The moment could not be more fitting: the Savings and Investments Union is currently the most far-reaching project designed to shape Europe’s future.

The EU needs significantly higher levels of investment to remain competitive in a confrontational world order and to grow in a sustainable and autonomous way. It also needs to address increasing climate risks and the consequences of demographic change.

The necessary expansion can only be achieved if European households change the way they allocate their savings by investing more in capital markets. A key channel for this shift is the further development of funded pension and long-term savings systems. Broad-based participation in financial markets is essential for citizens to build their wealth and secure adequate income in old age. decisive role in shaping households’ disposable income, the risks they face and the costs associated with investment.

Funded pension systems are also a budgetary imperative. Current levels of state pension systems may become unsustainable due to demographic change and competing spending pressures.1 Pension income can therefore erode over time, increasing the importance of private sources of retirement income and wealth accumulation. decisive role in shaping households’ disposable income, the risks they face and the costs associated with investment.

A substantial increase in financial market participation - through capitalised pensions and private long-term savings - requires public and private sector initiative. It also raises concerns whether the outcome will be politically and socially acceptable and sustainable. The emergence of high levels of income inequality and old-age poverty would run counter to core European values, and would risk generating political tensions in Member States. decisive role in shaping households’ disposable income, the risks they face and the costs associated with investment.

In my speech today, I will focus on the key policies and market conditions that can support broader participation in financial markets for long-term retirement savings and investments. decisive role in shaping households’ disposable income, the risks they face and the costs associated with investment.

Financial market participation is a complex decision. A substantial body of research examines why individuals decide to invest and under what conditions they are willing to bear risk.2 Public policies and market conditions play a decisive role in shaping households’ disposable income, the risks they face and the costs associated with investment.

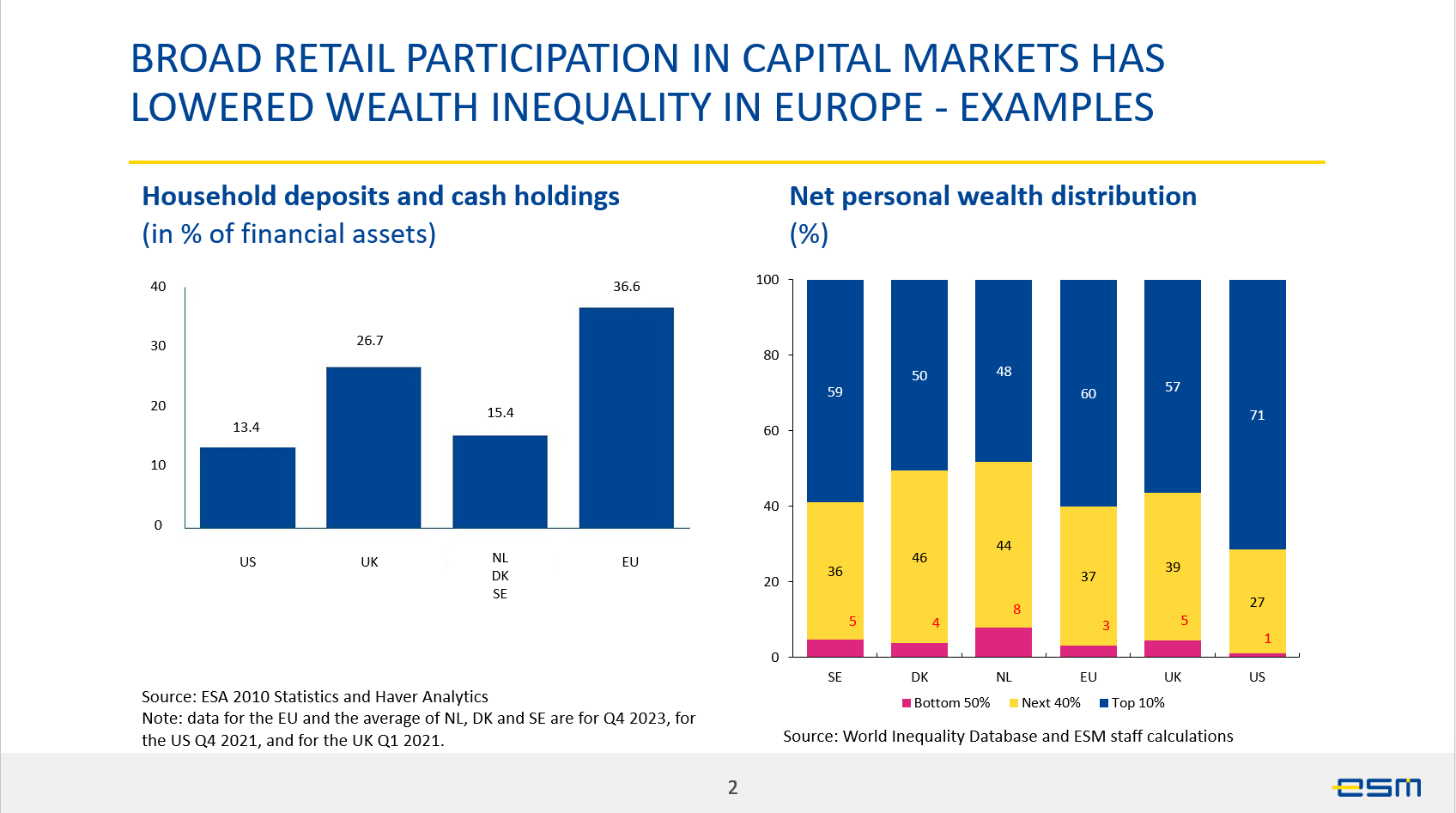

In discussing these policy and market factors, I will draw extensively on the experience of Nordic countries and the Netherlands. One consequence of limited capital market participation by European households is that a disproportionate share of their financial wealth is held in cash or low-yielding deposits.

By contrast, the Nordic countries and the Netherlands stand out in Europe for the high share of retirement savings invested in markets.

Their experience clearly shows that there are synergies between a welfare state and broad financial inclusion. Furthermore, higher capital market participation need not come at the expense of greater inequality or old-age poverty. This model stands in contrast to the political and social dynamics in the United States.

Household income, market capitalisation and growth – the role of social security systems and taxation

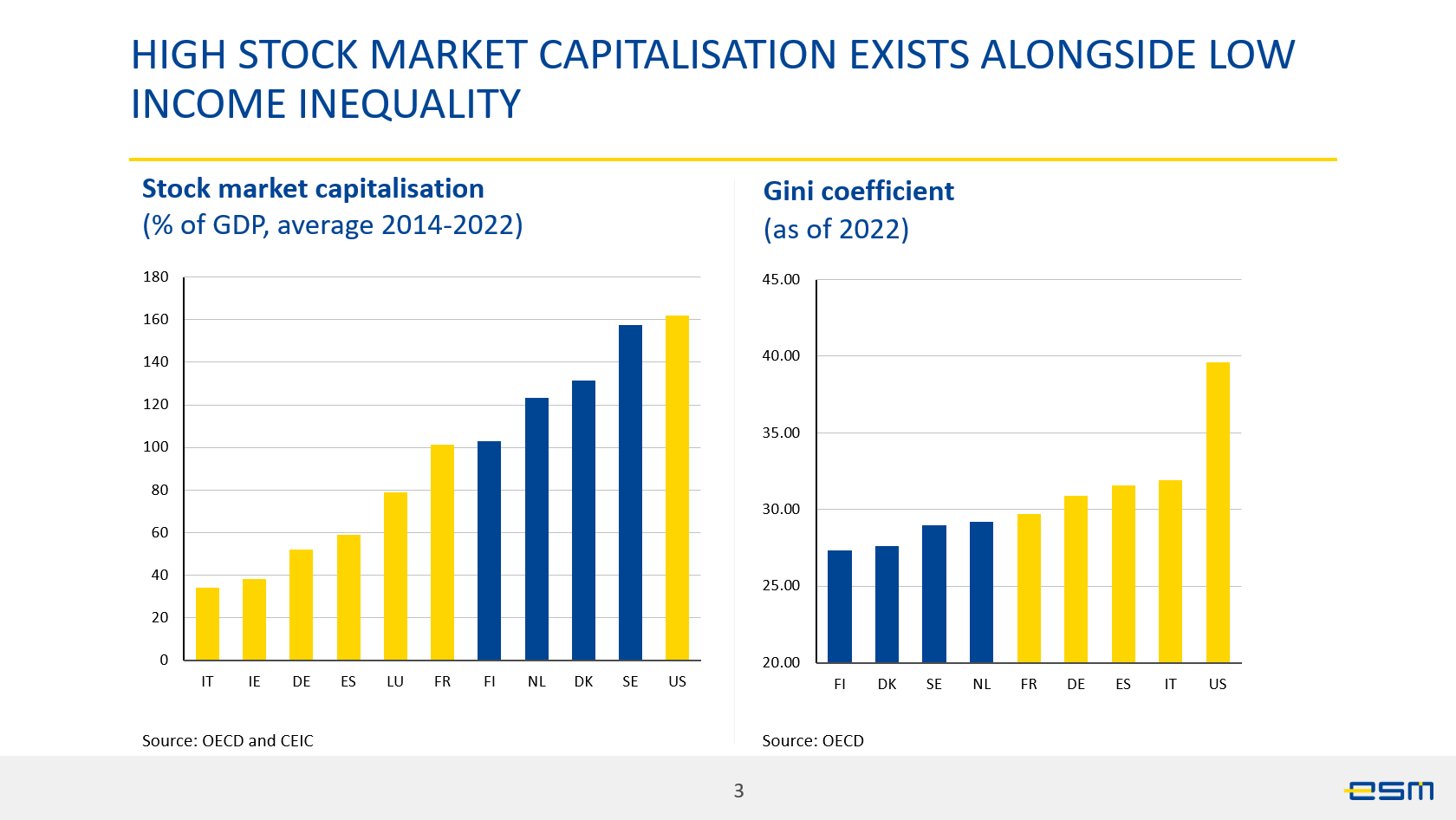

The European approach to market capitalisation differs in important respects from that of the US. The Netherlands and the Nordic countries have among the highest levels of stock market capitalisation to GDP in Europe and compare favourably to the US in this regard. But unlike the US, they also have low levels of income and wealth inequality.

Even by European standards, they perform very favourably in terms of income equality. The Netherlands and Sweden both have a Gini coefficient of around 29 (as of 2022), among the lowest in Europe and well below the US. When measuring wealth inequality, they also rank better than both the US and the EU average. The Nordic and Dutch experiences therefore point to a distinct economic model: one in which strong social policies co-exist with well-functioning capital markets and broad-based participation.

Social and tax policies are necessary determinants of capital market participation in any system that seeks to promote long-term household investment. Necessary because they allow families to save and invest and provide adequate returns. Yet economic research shows that these conditions may not be sufficient. Market participation may be limited even if people can afford to invest and it is economically advantageous. I will return later to the additional factors that can facilitate broader participation.

Social policies that provide insurance against unemployment and disability to work enable households to take on greater financial risks. Dutch and Nordic citizens – as those in many other European countries - know that they can rely on public health insurance if they fall ill, as well as unemployment benefits if they lose their jobs. In addition, active labour market policies provide retraining programmes to laid off employees, reducing the time spent in unemployment. This protection allows households to assume a longer investment horizon, as they need a smaller cash buffer for unforeseen contingencies. As such, they can afford to allocate a greater share of their savings to equities and other risk-bearing assets with higher expected returns.3

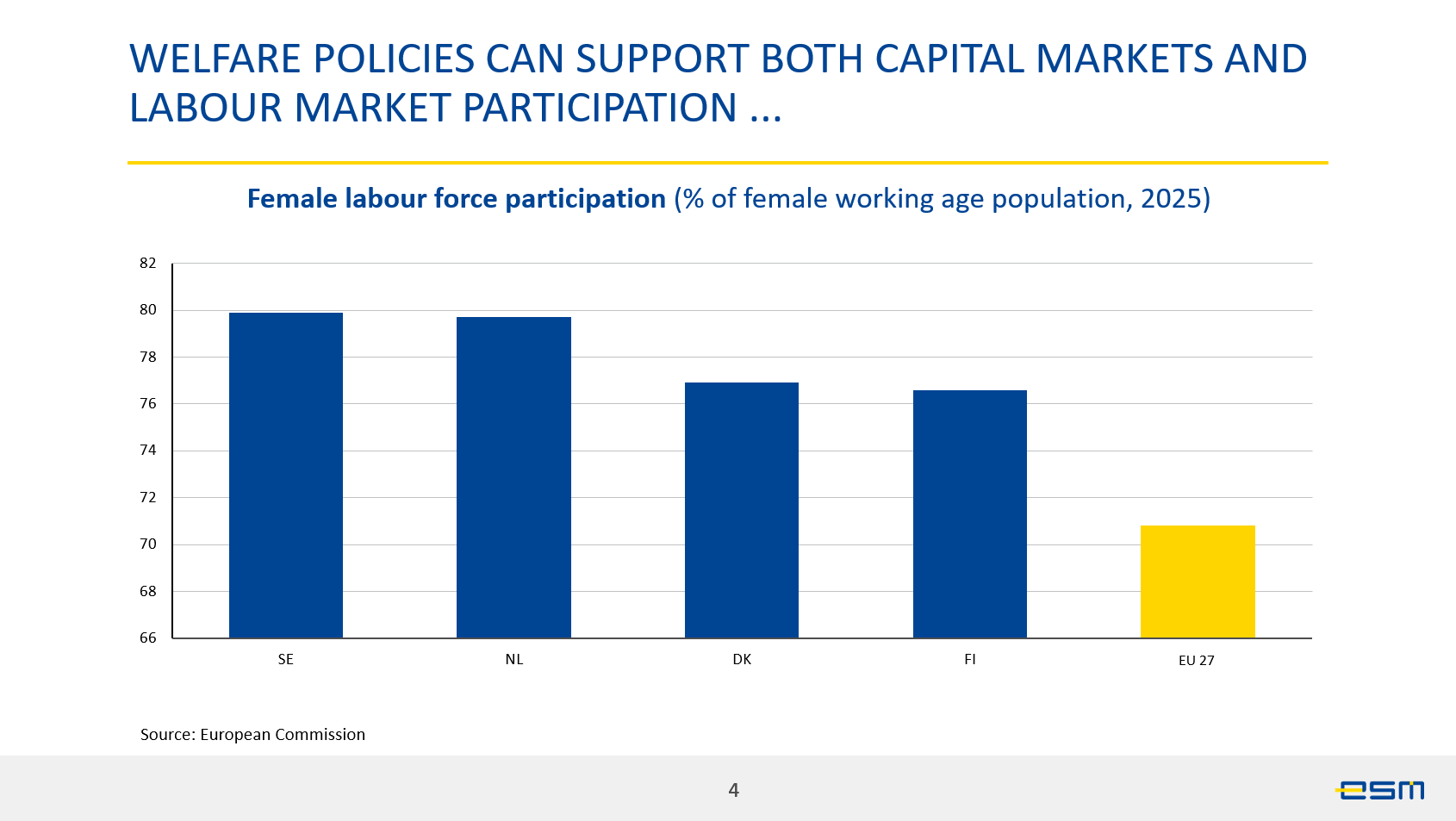

Labour market policies and family support measures allow a broader cross-segment of the population to earn income and set aside savings. Free schools and subsidised child-care contribute directly, while also facilitating labour market participation - particularly among women - and increasing income generation. In turn, these policies provide firms with access to a larger, more diverse talent pool and help broaden the tax base.

A key driver of broad capital market participation is the combination of financial incentives and attractive returns on investment. In other words, long-term savings for retirement must generate meaningful returns. The Swedish example shows that well-calibrated tax incentives can broaden retail participation without lowering revenue from capital gains taxation, as the higher returns on savings offset the lower tax rate applied in the Investment Savings Account (ISK).

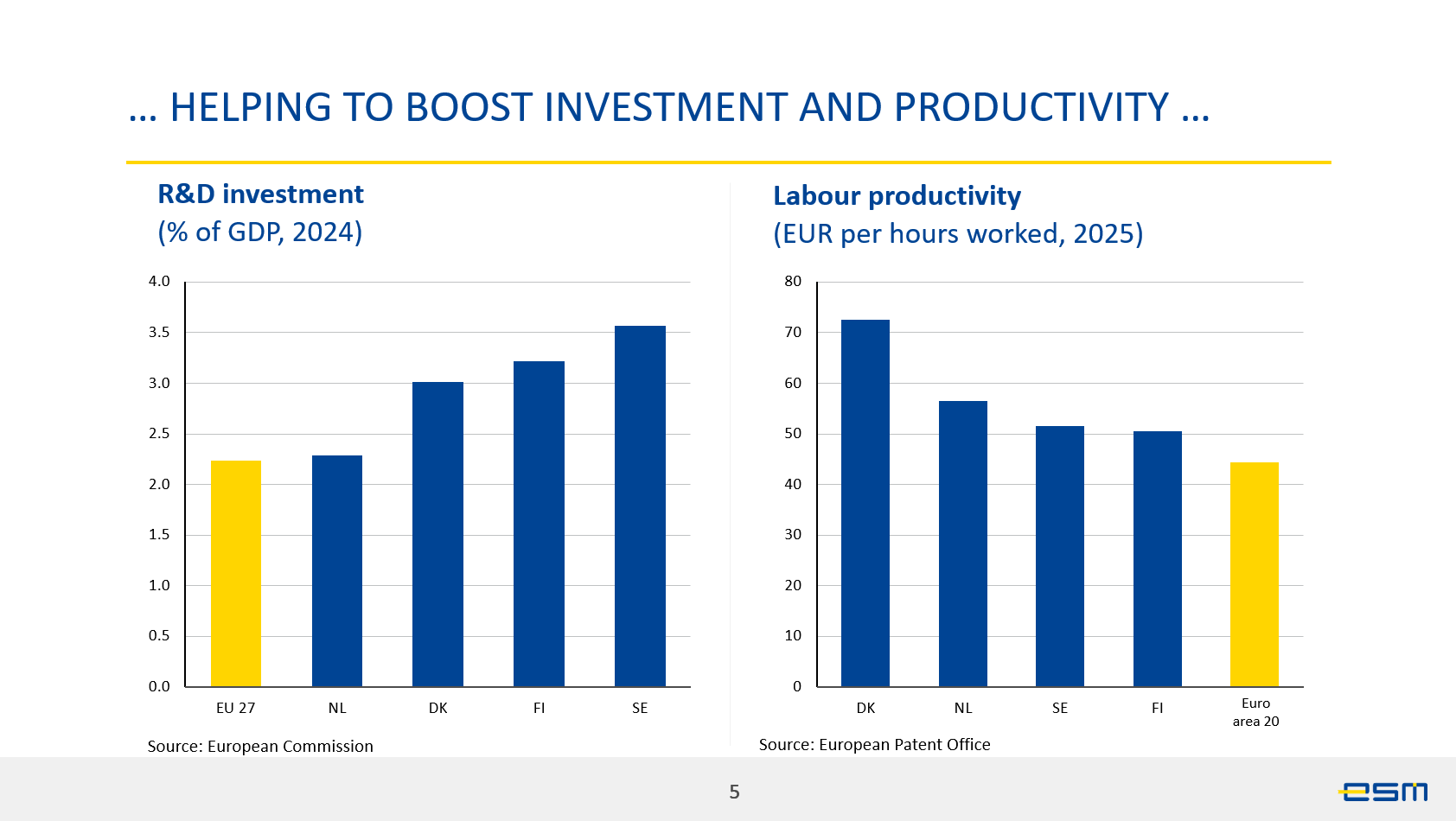

There is a virtuous circle which can be activated by creating a broad investment universe capable of generating returns. Dutch and Nordic pension funds allocate a significant share of their assets to equities. This supports more investments in R&D and innovation, which in turn enhances stock market performance and helps finance domestic firms. Higher investment returns also reduce the need to set tax incentives for investment. The resulting gains in productivity and GDP make welfare policies easier to finance and can translate into higher future pension benefits for a broad segment of the population.

Incentives for participation arise in part from limits on the state public pension pilar. Compared to the EU average, a much larger share of retirement benefits in the Netherlands and the Nordic countries come from funded pension schemes. This is because the state pay-as-you-go scheme is capped and only provides a basic retirement income, while employers are obliged to contribute to occupational pension schemes to supplement it.

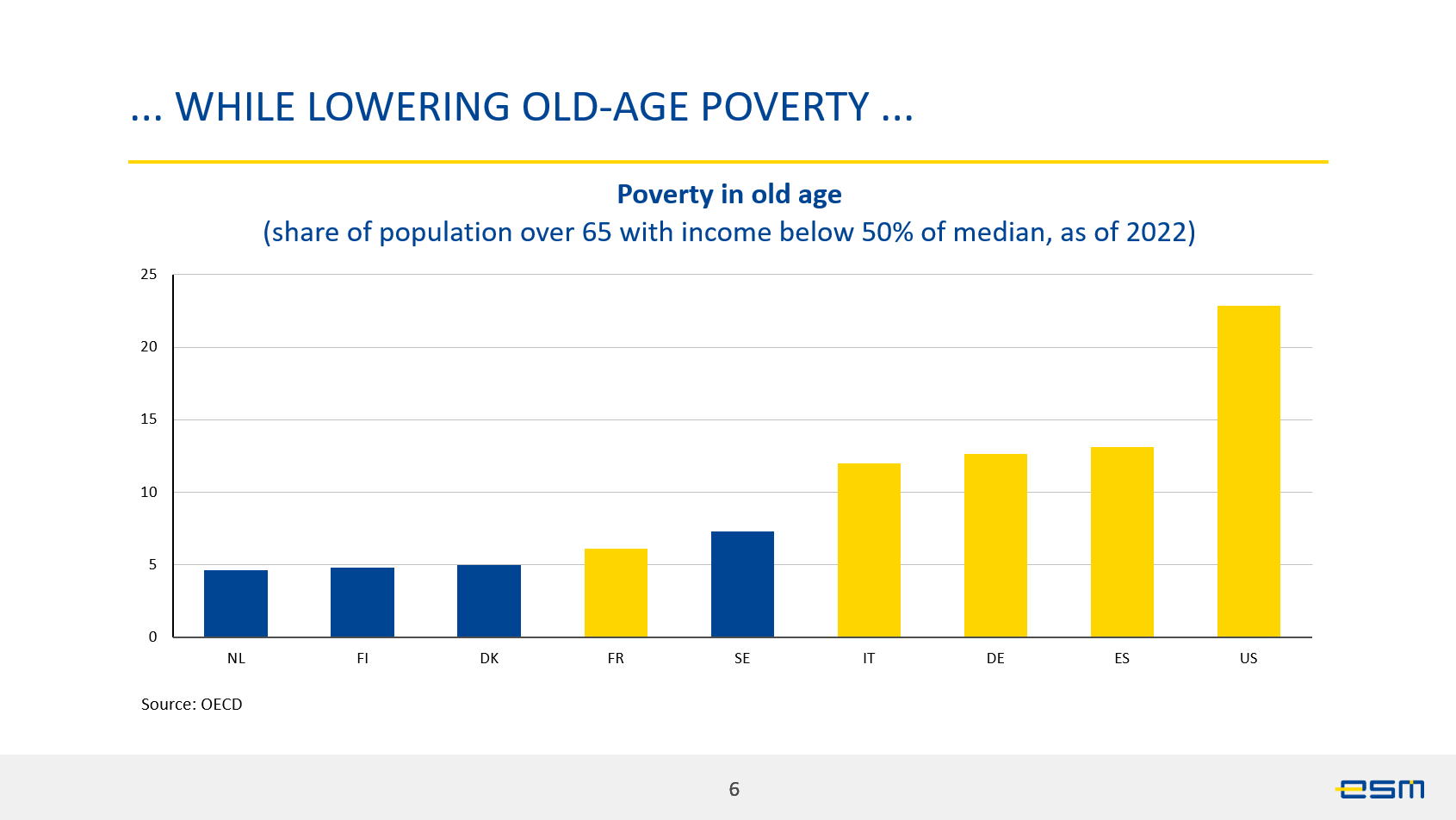

At the same time, state pensions provide broad-based income coverage to prevent old age poverty. The state pension benefit, while capped at a basic level, is nevertheless broad in terms of its coverage and not linked directly to employment and earnings to the same extent as in other Member States. For instance, residents in the Netherlands accrue a 2 percent entitlement for every year spent in the country, regardless of whether they are employed.

This ensures that households rely on a minimum guaranteed pension, even if the return on their pension fund investments falls short of expectations. This contributes to some of the lowest old age poverty rates in Europe. In Sweden, the minimum guaranteed pension benefit, although less generous, is similarly not linked directly to employment or earnings.

The reality is that European welfare states also have the most developed capital markets and rank highly in competitiveness and productivity. This is because their welfare policies support capital market participation, productivity and employment. These countries show that strong social and labour market policies can, in fact, be an enabler by shaping the necessary determinants of broad market participation.

How the private sector has acted in synergy with public initiatives to facilitate broader retail participation

Both public and private institutions can do far more to facilitate household market participation than simply providing income support or boosting investment returns. The drivers discussed earlier shape financial capabilities of individuals and families, but motivating participation often requires additional measures. Other facilitators need to set incentives by lowering information costs and building trust and financial literacy. Factors such as lower costs of entry, social acceptance and peer behaviour also play an important role in households’ investment decisions.

A key factor in broadening market participation for retirement savings is the enrolment rule in the occupational pension system. In this regard, the Swedish and the Dutch occupational pension systems are very comprehensive. In both Sweden and the Netherlands, employee contributions to occupational pension plans are either mandatory by law or through collective labour market agreements. This ensures that a broad segment of the population becomes familiar with investing in capital markets from their first employment. These systems have a long tradition that reflects a societal consensus. Any reforms to the system must secure broad-based support beyond the government, involving social partners as well.

In the UK, a more gradual form of pension enrolment was introduced in 2012. Employers are obliged to automatically enrol eligible employees into a workplace pension scheme with a minimum contribution of 8 percent of earnings. Employees can opt out but are re-enrolled every three years. This scheme has been highly successful, prompting EU Member States to consider a similar approach. Notably, Poland introduced an auto-enrolment scheme in 2019, while Ireland launched "My Future Fund" on the 1 January 2026.

The benefit of auto-enrolment is the reason why it is a key feature of the European Commission’s recommendation on supplementary funded pensions.

Transparency and trust in the system are promoted by national pension dashboards, which consolidate information from all pension funds in which employees have registered savings. The dashboard allows people to simulate their retirement income under different assumptions about retirement age and future investment returns. Since second pillar pension savings are locked in until retirement, it helps employees observe the long-term impact of taking risks, as well as the effect of compounding returns.

Public and private initiatives in financial literacy have also helped to increase retail participation. For example, in Sweden, a national network for financial literacy brings together more than a hundred national authorities, firms and non-profit institutions. They collaborate to conduct targeted education initiatives in primary and secondary schools, for senior citizens and working professionals. Based on such experiences, financial literacy features as a core priority in the European Commission’s strategy for the Savings and Investments Union.

A balanced investment mandate and a cost-efficient administration model shape the success of financial institutions in managing retirement savings. As mentioned earlier, Dutch and Nordic pension funds allocate a large share of their assets to equities, contributing to strong investment performance. They also operate highly cost-efficient administrative systems, resulting in low fees for pension beneficiaries. These features have strengthened public support for funded pension schemes.

By contrast, the Baltic countries have experienced a public backlash against funded pensions, with recent legislation in Estonia and Lithuania that allows households to withdraw part or all of their savings. This backlash is driven by poor investment performance – stemming from very prudent investment mandates – and high management fees charged by pension funds in the past. These examples show the importance of designing a robust operating model for funded pension schemes.

Digitalisation and how the private and public sector shape the business environment also play a key role in lowering barriers for households to invest.

Today, most banks and brokers provide user-friendly investment apps. They have drastically reduced transaction fees for investments in stocks, facilitating smaller ticket sizes and making investments accessible through a few clicks on a smartphone.

Beyond user-friendliness, many banks and brokers also allow investments in fractional tickets. This brings major benefits in terms of retail investor participation in capital markets because it

- further lowers the entry cost,

- enables proper diversification even with small amounts and

- facilitates the creation of automatic savings plans.

Moreover, there are a variety of options to invest in funds with more diversified portfolios, whether open-end UCITS (Undertakings for Collective Investment in Transferable Securities) funds or ETFs (Exchange-Traded Funds). These offer increasingly competitive management fees or low bid-ask spreads, even for smaller fund units.

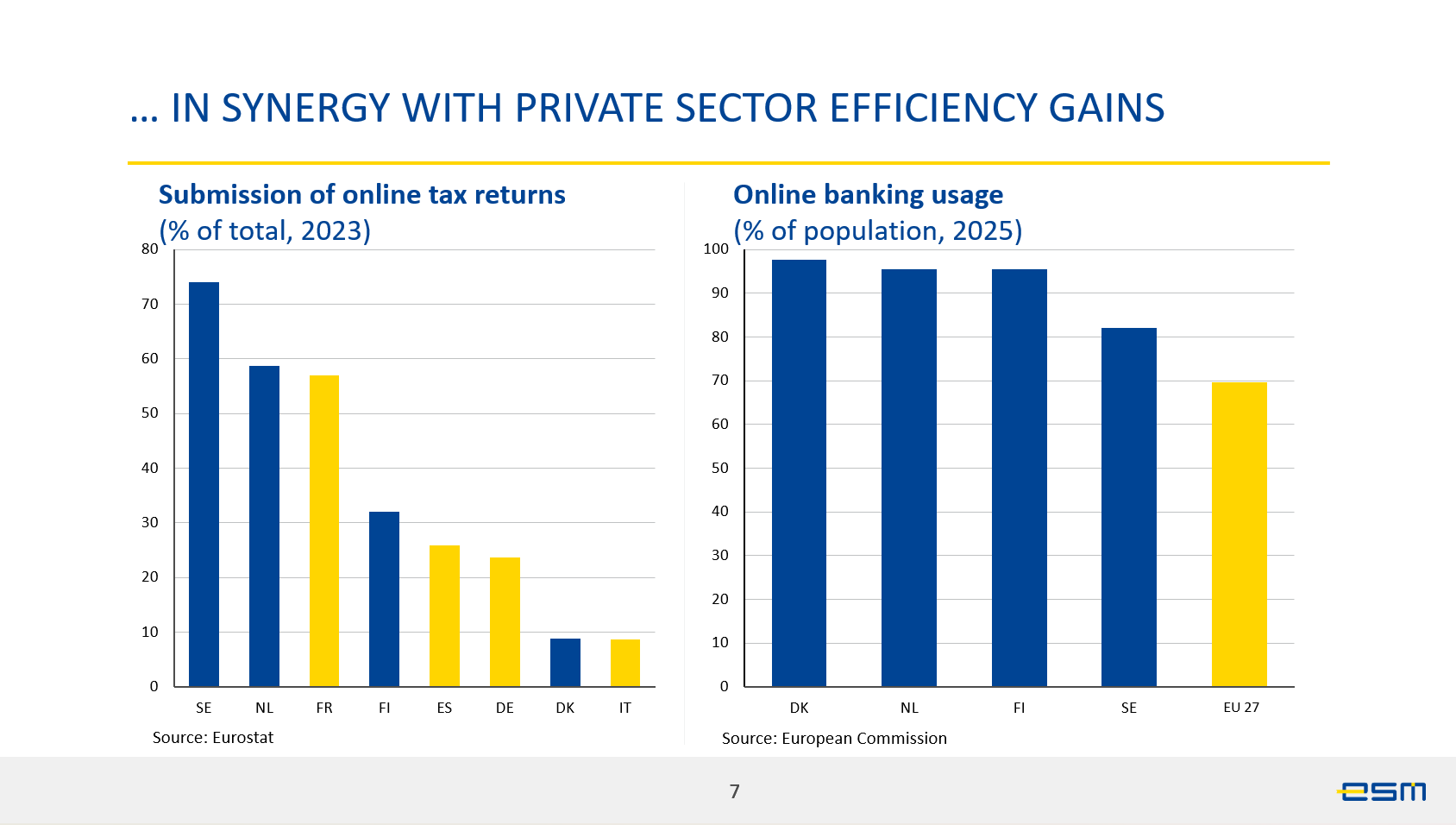

Digital and financial innovation in banks has complemented public initiatives to increase digital literacy. For instance, Sweden and the Netherlands were early adopters of online tax filing systems. Citizens were encouraged citizens to use them by offering faster processing and earlier return of tax claims. As a result, these countries have among the highest rates of digital literacy in Europe, as reflected for instance in the high share of online tax returns.

These efforts were reinforced by public education initiatives to boost digital literacy and internet usage. For example, municipal libraries provide such programmes for senior citizens and other groups less familiar with new technologies.

The example of the Nordic banking systems shows how a digitalised banking system can both facilitate and profit from broad capital market participation. Nordic banks were early adopters of digitalisation and pioneers in developing user-friendly investment apps for retail customers. In Sweden, banks provide customers with easy-to-use platforms to manage their savings and investments accounts. This has contributed to the broad acceptance of these accounts as long-term investment vehicles for households.

While online banking usage in the EU averages around 70 percent, it still varies considerably across Member States. In the Netherlands and the Nordic countries usage rates are around 95 percent, while Bulgaria and Romania lag behind at 30 percent. Low usage of online banking is an obstacle: financial innovation only supports broad retail participation to the extent that households feel confident to use digital platforms that reduce transaction costs.

Banks themselves stand to benefit from teaching and encouraging customers to use digital platforms. High levels of online banking usage have enabled Dutch and Nordic banks to operate with highly cost-efficient operating models. They also benefit from a more diversified revenue base, with a higher share of fee income from transactions. This makes their profitability more stable and resilient to shocks.

To conclude, I would like to share a vision of the future with you. Imagine a Europe where participation in capital markets is as commonplace as having a bank account and where citizens have a broader stake in the economy’s growth. A Europe where wealth accumulation is a function of accessible systems, thoughtful policy design and private sector innovation.

This future is within reach. It is one that public policy can help bring about, in synergy with private sector innovation.

- 1

For future spending pressures from demographic change see European Commission (2024) 2024 Ageing Report. Economic and Budgetary Projections for the EU Member States (2022-2070) - Economy and Finance. Brussels.

- 2

See for example, Gomes R., M. Halliasos and T. Ramadorai (2021) Household Finance. Journal of Economic Literature, vol. 59 (3), pp. 919–1000; Menkhoff L, J. Westermann (2024) Determinants of stock market participation, DIW Discussion Papers, No. 2078. For financial allocation of European Households see the fundamental work of Arrondel L. et al (2016) How Do Households Allocate Their Assets? Stylized Facts from the Eurosystem Household Finance and Consumption Survey; vol. 12(2), pages 129-220, June.

- 3

The literature on household financial market participation also indicates that individual do not invest when returns are correlated with income shocks (see Gomes et al. 2020) This may be the case for unemployment spells and equity returns. Income insurance can therefore facilitate financial market risk taking.

Author

Contacts