Euro area countries forged a new shield for monetary union over the course of 2018, making the most of a period of reflection on how to deepen and strengthen their ties. Work that began in 2015 with the EU’s ‘Five Presidents’ report’[1] progressed through a series of proposals that culminated in an important step to enhance Europe’s Economic and Monetary Union.

European leaders, at a summit in December 2018, endorsed a wide-ranging push to deepen Economic and Monetary Union that broadens the ESM’s mandate and will require euro area member states to change the treaty governing the firewall. The plan includes steps to adapt the firewall’s toolkit, strengthen the way the firewall works with its fellow institutions, and create a backstop for helping the financial sector handle a major bank failure. When these steps are implemented, the firewall will become an important part of the euro area’s banking union and it will continue to be a provider of last-resort financing for countries that lose their ability to borrow on private markets.

European Council President Tusk hailed the agreements on banking and crisis prevention: ‘These two decisions – which mean changing the ESM Treaty as soon as possible – significantly strengthen the monetary union,’ he said after the meeting[2].

The December decisions showed the growing political support for the ESM from member states across the euro area, drawing support from countries that received aid as well as countries that had been sceptical of the whole process.

Slovakia, an early critic of the rescue funds, is now one of the voices calling for the ESM to play a central role in constructing a stronger euro area financial architecture. In 2016, Slovakia spearheaded a discussion on shock-absorbing mechanisms during its time at the helm of the EU’s rotating presidency, and the country has since continued to advocate euro area integration.

The currency union needs institutions, rules, and instruments designed to fortify all of the euro area, in order to shield economies and financial sectors in the member states from harm, according to Slovak Finance Minister Peter Kažimír. ‘We need to transform the ESM,’ he said. ‘What we need to achieve is a more resilient, better functioning euro area with a clear strategic direction.’

The firewall should be at the heart of the monetary union’s next steps, said Albuquerque, former finance minister of Portugal, which was one of the pioneers in undergoing a rescue programme. ‘We would like to see the evolution of the ESM as the central element of a new institutional framework inside Europe and particularly in the euro zone – clearly continuing to exist and becoming more relevant, with a bigger role than it has now,’ she said. ‘There is the need to create a different institutional framework making ESM evolve into something that could be called European Monetary Fund or anything else. This is for lack of a better designation and so that people understand what we are talking about.’

In 2016, momentum was building towards strengthening the euro area. As former European Commissioner Rehn, now governor of the Bank of Finland, said at the time: ‘The future of the ESM is related to the overall reform of euro zone governance. We have to continue the reconstruction of the euro zone even though for the moment there is not much appetite for that because of several immediate pressing concerns.’

Heading into 2019, the appetite for positive change is much improved. The ESM is a well-established firewall, all euro area countries that received aid have exited their rescue programmes, and the banking union is off to a solid start. The next challenge will be to strengthen the foundations of the euro – to prepare for the next crisis before it hits instead of after the fact.

‘The European reaction to the crisis was arguably slow at first, but when you look back you see we have come a long way in filling in the holes of the initial set-up of the euro,’ said Centeno, chairman of the ESM Board of Governors and Eurogroup president. ‘In times of crisis, the temptation to look inwards is strong. But European governments agreed to pool resources at the ESM to defend our currency in a way that was unimaginable at the onset of the euro. That boosted confidence in our currency. No wonder the ESM became a beacon for further integration in the euro area.’

The achievements of 2018 bear this out. Over the course of the year, the euro area was able to break deadlock on a wide range of policy issues. The Eurogroup assembled all the elements of the deal in early December, meeting in an inclusive format that includes non-euro countries as well.

One of the biggest steps forward involves the euro area’s banking union, which began in 2012 when countries agreed to create a common bank supervisor to oversee cross-border, systemic banks – and to create a new framework for dismantling them safely if needed. The ESM has in parallel stood by to help safeguard the euro area’s financial sector, and now it stands poised to join forces formally with the banking union’s other main institutions.

Banking union depends on three main elements: supervision, resolution, and deposit insurance. The euro area has harmonised its rules on how countries must provide deposit insurance, and it created a pair of new institutions to handle the other duties: the Single Supervisory Mechanism to keep an eye on the big banks, and the Single Resolution Mechanism to stand ready to take them apart. To help prevent a liquidity crunch, the Single Resolution Board is collecting fees from banks to build up a resolution fund that can be tapped in an emergency. However, this fund on its own was not seen as a strong enough bulwark.

At the start of the euro area effort, the ESM was directed to develop the capacity to provide targeted aid to a country’s financial sector, either by offering government aid with a banking focus or by stepping in to help banks directly. Between 2012 and 2014, the ESM made sure that all of its tools would be fully operational when called upon, and in the process it acquired substantial expertise. Once the heat of the crisis had passed, euro nations sought to harness these capabilities more fully.

In June 2018, euro area leaders struck a provisional deal for the ESM to take over permanent bank backstop duties, which had been temporarily assigned to a series of national credit lines. At that meeting, leaders also agreed to ‘start on a roadmap for beginning political negotiations’ on a European deposit insurance scheme, another important pillar of the banking union project[3]. The speed at which this can be implemented will depend on the progress made by euro area governments in other areas, such as dealing with non-performing loans.

By December 2018, euro area resolve had solidified around the plan. The ESM and the European Commission had worked out how they will cooperate going forward, in times of calm as well as times of turmoil, and the euro area had also delved more deeply into the various proposals for shoring up the monetary union. Not only would the ESM take on a new role regarding banking, it also would take a fresh look at its lending toolkit to make sure it could offer the euro zone the best possible help.

‘It was important for us to have a comprehensive reform, not only focusing on the operation of the ESM in connection with what’s being called a backstop, but also encompassing things that will enable the ESM in the future to address debt sustainability and will see to it that the ESM’s precautionary instruments can be designed more effectively,’ Germany’s Chancellor Merkel said at a press conference after the meeting[4].

Only two of the ESM’s six available aid tools have been used so far: long-term loans for Greece, Ireland, Cyprus, and Portugal and indirect aid to help Spain recapitalise its banking sector. Euro area leaders used their December summit to reach agreement on how they want that toolbox to look in the future.

The precautionary tools – which are similar to instruments that the IMF has – were at the centre of a vigorous debate about how they should be used and what changes might be needed. Although they have not been used yet, they may some day be needed and the euro area has embarked on a plan to bolster their capabilities. The goal is to help the euro area stave off a crisis before it becomes entrenched, allowing the euro zone to bounce back more quickly and avoid the worst parts of the cycle.

Before the summit, Eurogroup finance ministers released ‘term sheets’, or technical blueprints, for the ESM enhancement proposals. In the case of the precautionary tools, the aim was to make them more effective for countries that have well-managed economies but are nevertheless hit by an adverse shock beyond their control.

As a result, the euro area has pledged to clarify how it determines whether or not a country has pursued sound economic and financial policies, and it affirmed that countries will always need to show the sustainability of their general government debt.

‘The eligibility process will be made more transparent and predictable,’ the Eurogroup said. In its term sheet[5] on ESM reforms, it said eligibility for such a credit line would be reviewed at least every six months, and if conditions worsened then the country needing support might have to move to an enhanced conditions credit line or a full macroeconomic adjustment programme.

Coupled with the bank backstop, the strategy when implemented promises to offer an additional level of protection and cooperation.

The euro area’s plan for the ESM also calls for changes to other rescue offerings. When the ESM takes over the bank backstop, that mission will replace direct bank recapitalisation in the firewall’s toolkit. The ESM will provide a credit line for the Single Resolution Fund when needed, to make sure the resolution fund has enough cash to handle the meltdown of a large financial firm. Any non-euro countries that join the banking union would be expected to provide their own revolving credit lines alongside the euro area bank backstop[6].

Should the resolution fund or its backstop ever be used, outlays would be paid back by raising levies on European banks. If called upon, the ESM could make the difference in helping the system work as designed. The new system will be up and running no later than 2024, or earlier, depending on how other elements of the strategy progress.

‘With the highest paid-in capital of all international financial institutions and substantial firepower, the ESM can also provide a credible backstop to banking union,’ Centeno said already in a message in the 2017 ESM annual report[7].

In their summit statement[8], euro area leaders asked their finance ministers to prepare the necessary ESM Treaty amendments by June 2019. They said the ESM enhancements would be a core element of an effort to ‘significantly strengthen’ monetary union. Their comprehensive package also directed the Eurogroup to design a euro area budget instrument for competitiveness and convergence that could be incorporated into the EU’s multi-year fiscal framework, and it endorsed Commission efforts to strengthen the role of the euro in the international financial system.

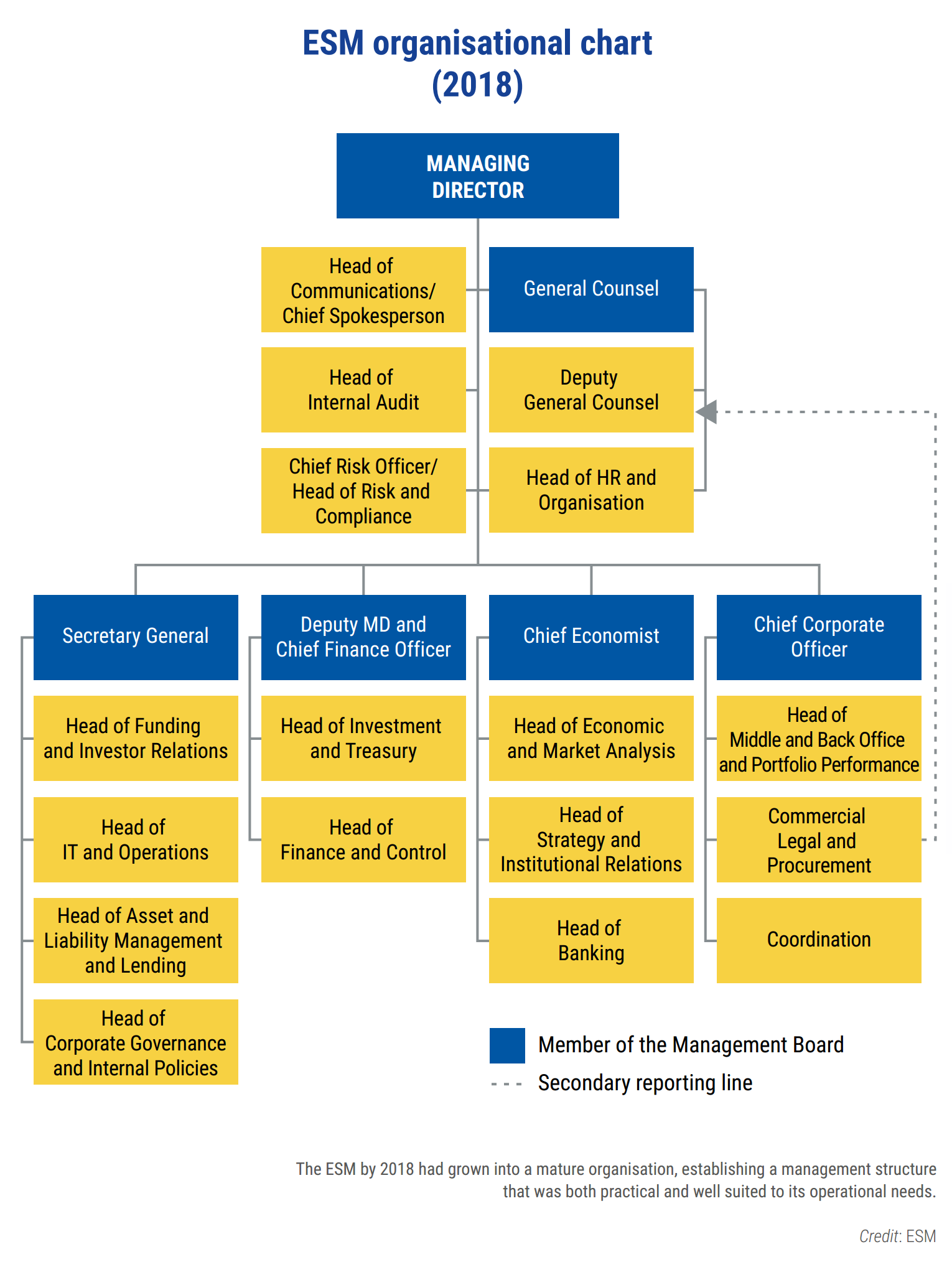

ESM management board and heads of division

Credit: Steve Eastwood/ESM

Taken together, all these developments will strengthen the euro area and its firewall, and set the stage for future considerations.‘This is part of a wider debate about fiscal risk sharing,’ Regling said during a July 2018 workshop at the ECB[9]. While controversial, there is also talk about common area fiscal tools such as a rainy-day fund or a joint fund for investments. These are all linked to discussions about a possible future sovereign debt restructuring framework, which would make settlements with private creditors more transparent and more predictable. The ESM could play a constructive role by providing debt sustainability analyses and by facilitating talks between creditors and debtors. ‘In my view, we don’t need to have a more rigid approach but a more transparent one,’ he said.‘ And the ESM can play a role in such a framework.’

The December 2018 decisions will allow the euro area to make the most of the strength it built during the crisis years. Even so, there remains room for the ESM, and the euro area’s overall architecture, to develop further. To prepare, the euro area has embarked on an ambitious period of reflection and change. The monetary union’s recent achievements are significant, but the euro area’s defence system is still not as solid as it could be. Those who lived through the crisis negotiations know the euro area would be better served if the remaining deficiencies were fixed now, rather than when the next crisis hits. This includes building public support for euro area reforms, as well as designing better rules and sturdier safeguards.

‘Our Economic and Monetary Union remains incomplete. There is a need to consolidate and complement the unprecedented measures we took during the crisis and make them more socially and democratically legitimate,’ said European Commission President Juncker.

The ESM has plenty to do in the meantime. The firewall must continue to manage the financing and repayment of the rescue programmes that took place, and it must consider how best to rebalance its workforce as it takes stock of its expanded mandate. The ESM also will continue to develop its investment and funding side, and to adjust its workforce to best handle the fund’s ongoing duties.

‘We have to prepare for a steady-state period where there is less excitement, more routine work,’ Regling said.

From the outset, the ESM has been mindful of attracting a diverse range of investors and it is constantly looking for ways to tap new funding sources. It has added private placements and non-euro issuance to the regular presence with liquid euro benchmarks. These are needed not only to keep up with their current liquidity needs, but also so that the ESM can offer a new programme at a moment’s notice. ‘We are a crisis mechanism,’ said Ruhl, ESM head of funding and investor relations. ‘We have to be ready and able to act in difficult market situations to raise additional money.’

The investment team aims to expand its capacity by making use of additional financial instruments, such as non-euro assets and short money market futures. The team also continuously aims to refine its asset allocation and benchmarking to improve the quality of its asset management. In parallel, it participates in discussions with shareholders to explore potential framework revisions, to increase the ESM’s long-term investment performance. Finally, the team is adjusting to ongoing changes: the reduced liquidity of the European bond market requires improved monitoring of market conditions; the development of responsible investment may lead to the introduction of new investment principles, and; regulatory changes, such as the revision of Libor rates, lead to the adaptation of existing instruments and contracts.

‘Our responsibility to our shareholders is to make the most of the funds we manage, within a tight framework,’ said Frankel, ESM deputy managing director and CFO. ‘We don’t want to shut ourselves off from opportunities by not having the right product mix.’

Given its crisis experience, the ESM is now better placed than ever to monitor all of the countries that received financing support during the crisis, to make sure they can repay their loans as agreed, and to assist in the euro area’s efforts to protect the monetary union from future shocks. This reflects the institution’s growth since its inception on the way to its current maturity.

Managing Director Klaus Regling and the ESM staff at the fund's fifth anniversary. The team is ready to take on new mandates following the December 2018 euro summit

Credit: Steve Eastwood/ESM

‘It has earned its credibility,’ said Malta’s Camilleri. ‘The ESM is an institution which is alive and kicking, quite dynamic, and it is growing over time. Initially its participation in certain negotiations was substantially less than it is now. Its presence is much more visible now.’

The rescue fund fits in a broader framework of strengthening growth, increasing resiliency and protecting against future shocks, said Dijsselbloem, former chairman of the ESM Board of Governors and former Dutch finance minister. ‘All that would make it less likely that ESM programmes are needed again anytime soon,’ he said. ‘However, as crises do happen in our economic system, it is good to know that the ESM is the euro area’s stability anchor – an anchor the euro area will always be able to rely on.’

One day, the ESM may be fully integrated in the EU framework, through an amendment of the EU treaties. Like the EIB, the ESM could have its own protocol within the EU Treaty, while also keeping its capital and key features of its governance structure. In the meantime, the firewall will continue to strengthen and improve, in order to fulfil all of the missions its Members have envisaged.

‘The ESM’s place is in the EU treaties and I’m sure that one day it will be,’ said Regling. ‘Although we are intergovernmental for the time being, at our core, we are an EU institution. Created by a great showing of European solidarity, we are one of the Union’s key defences and will remain so for the future.’