38. Debt relief: ‘real savings for Greece’

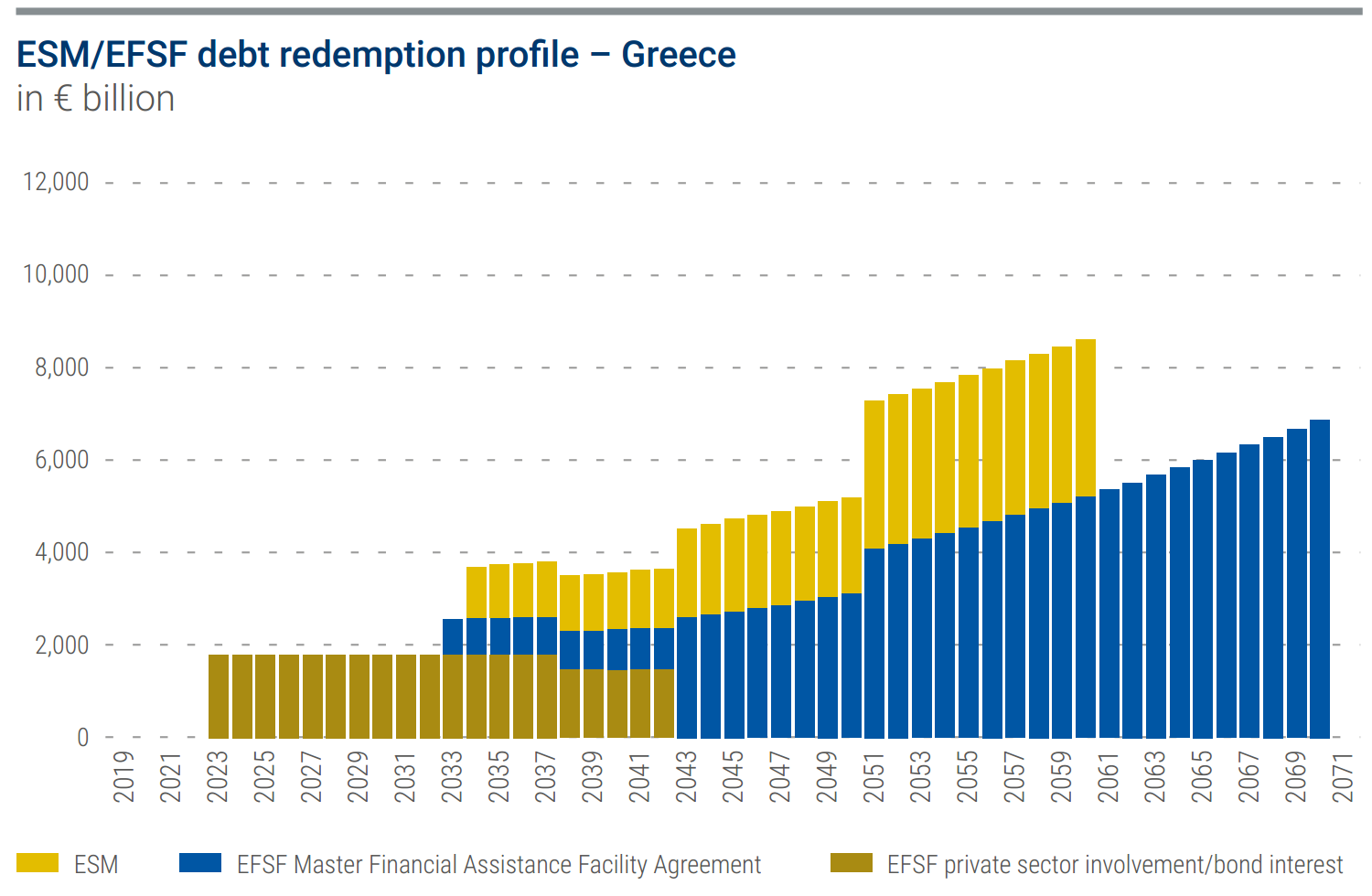

Greece emerged from its programme in August 2018 with outstanding debt of €190.8 billion to the euro area rescue funds. As holders of 53.2% of Greek central government debt at the end of 2018[1], the EFSF and ESM are by far the country’s largest creditors. Since the latest debt relief measures agreed in June 2018, the last EFSF loans are not scheduled to be retired until 2070, making Greece the longest-term partner of the firewall.

Managing and paying down debt until then – through economic and interest rate cycles that are beyond any reasonable forecasting horizon – will pose a generational challenge for Greek society. It is worth noting, however, that without the burden-sharing policies put in place by European creditors – from the first interest rate abatements in March 2011 to the later relief offered by the Eurogroup – the debt would be higher. None of these money-saving steps breaks with euro area strictures that require Greece to repay the principal amount of the loans in full.

‘When I look at what happened in the past, it’s quite significant that not everybody may be aware how much debt relief has already been granted by private and official creditors,’ ESM Managing Director Regling said. ‘These are real savings every year, and a very large amount of money. It may not be so evidently visible, but it’s really there, and therefore the debt service in the Greek budget, in terms of GDP, is less than in many other countries.’

To be sure, the debate over Greek debt sustainability looks set to continue. The IMF declined to take part in the third programme out of concern over Greece’s debt, pressing the European creditors for more concessionary terms. In the final weeks of the programme, the IMF hailed Greece’s budget-cutting efforts and virtual elimination of economic imbalances, while remaining unconvinced about the long- term debt-repayment outlook. Relief offered by European creditors ‘has significantly improved debt sustainability over the medium term, but longer-term prospects remain uncertain,’ the IMF said in an assessment published on 29 June 2018, just after the latest Eurogroup debt relief agreement[2]. ‘[I]t could be difficult to sustain market access over the longer run without further debt relief.’

From the ESM’s perspective, what matters is that the debt sustainability analysis (DSA) by European institutions concluded in June 2018 that Greece’s gross financing needs will remain manageable[3]. The DSA is conditional on Greece receiving additional savings from the medium-term debt relief measures and on Greece following through on its economic commitments.

‘We can safely say based on the DSA of the institutions that Greek debt is sustainable going forward,’ Eurogroup chief Centeno told reporters after the finance ministers met in June 2018[4].

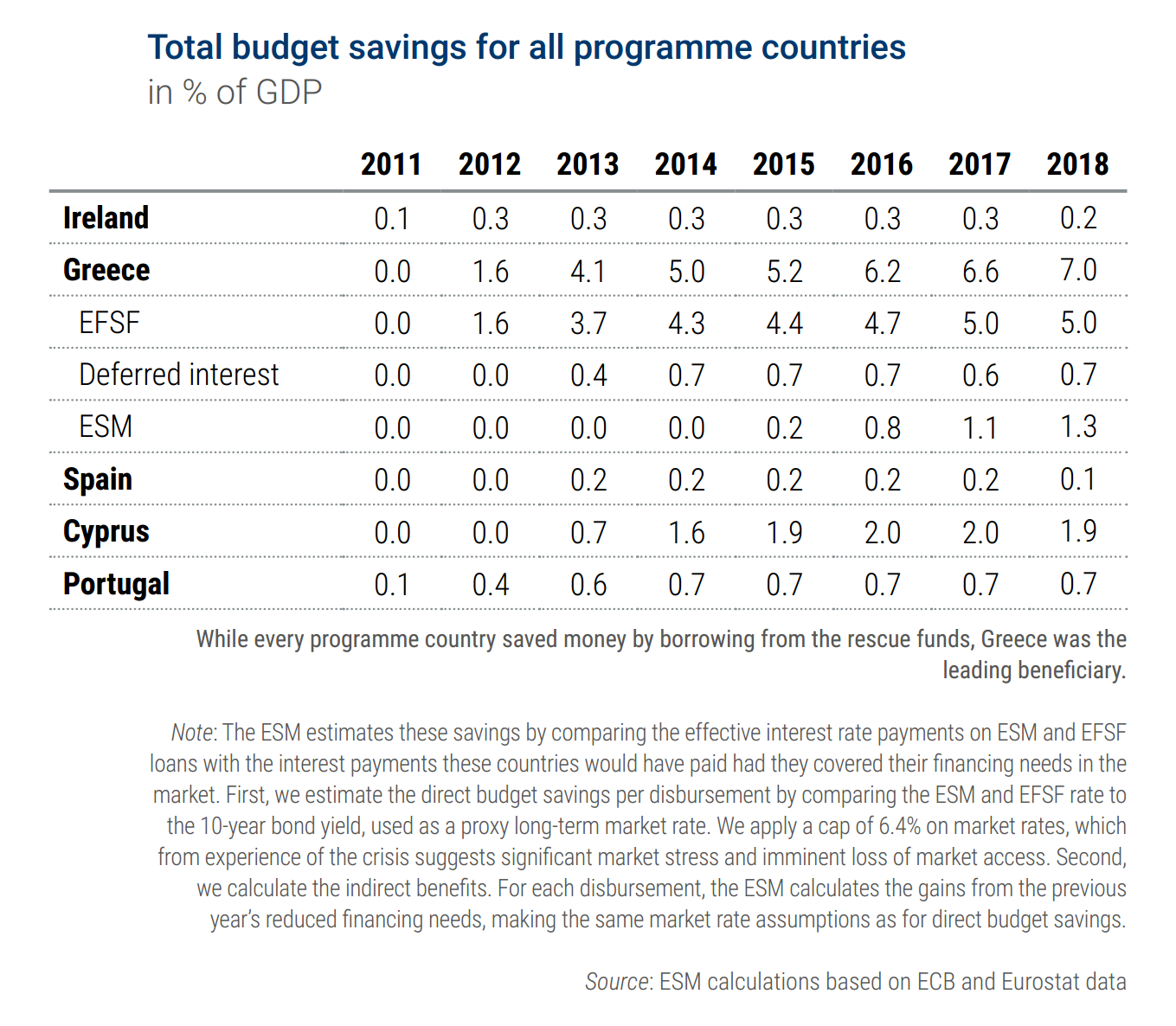

EFSF and ESM loans to Greece have over 30 years average maturity – in some cases over 40 – and carry very favourable interest rates. ESM economists estimated that these advantageous conditions alone save Greece around €12 billion in debt servicing annually, which was equal to 6.7% of GDP in 2017[5].

ESM expertise has been crucial in shaping and executing the relief policies, starting with short-term measures envisaged by the Eurogroup in May 2016 and carried out in 2017. The objective was to facilitate Greek access to the bond markets, spread out repayments over time, sustain Greece’s economic adjustment once the programme ended, and insulate Greece from the interest rate increases in financial markets that are expected in the long term[6].

‘The short-term debt measures will have a significant positive impact on the sustainability of Greek debt,’ the Eurogroup said in a 5 December 2016 announcement that entrusted implementation to the ESM[7]. There was a last-minute hitch when Greece made some spending commitments without getting clearance from the institutions. The process resumed after Finance Minister Tsakalotos said in a 23 December 2016 letter to the ESM and Eurogroup that Greece was ‘fully committed to pursue the agreed fiscal path’[8].

One feature of the short-term package was the use of a bond exchange scheme and interest rate derivatives to improve Greece’s debt sustainability and prevent future unexpected increases in the cost of its official loans, without additional costs to other programme countries. The bank recapitalisation component of the EFSF and ESM programmes, for example, had been financed with notes that came with floating interest rates. These short-term measures included an exchange of these floating-rate notes with funds backed by long-term fixed-rate issuances. For the ESM, there were also swap contracts implemented for some of the remaining ESM loan tranches, to peg Greece’s costs close to the historically low levels at which it borrowed during the crisis. These measures serve as a fiscal shield that make Greece’s budget planning more predictable.

Other measures at that time included bringing the weighted average maturity of Greece’s EFSF loans back up to the original 32.5 years and spacing out loan repayments due in the 2030s and 2040s. Creditors also waived for 2017 a scheduled ‘step-up’ interest rate margin of 200 basis points on an €11.3 billion tranche that had been connected to Greece’s debt buy-back in the second programme[9].

Greece was benefiting from the first round of cost savings when, on 15 June 2017, euro area finance ministers sketched out the medium- term measures that would be on the table once the programme ended. Already, the Eurogroup noted in a statement, the short-term measures had contributed to a ‘substantial lowering’ of Greece’s gross financing needs and the smoothing out of its future payments trajectory[10].

The medium-term proposal was part of efforts encouraging Greece to stay the course of budgetary prudence and economic modernisation beyond the life of the programme. As proposed, it covered the elimination of the ‘step-up’ interest rate margin tied to the second programme debt buy-back instalment; the release of central bank profits on Greek securities withheld in 2014; the restoration of those profit transfers as of 2017; further ‘liability management operations’ within the ESM programme envelope; and the further extension of Greece’s EFSF maturities and deferral of interest payments, as long as this didn’t create an additional burden on the countries providing EFSF guarantees.

Eurogroup ministers pledged to carry out these medium-term measures ‘to the extent needed’ at the end of the programme, and left the door open to further adjustments if the Greek economy suffered another downside shock[11]. For the long term, ‘in the case of an unexpectedly more adverse scenario, a contingency mechanism on debt could be activated,’ the Eurogroup said. Steps could include further EFSF re-profiling, as well as capping or deferring interest payments.

By the summer of 2018, all the moving parts came together when the Eurogroup made good on medium-term pledges. The new debt relief for Greece was agreed to be a further 10-year deferral of interest and amortisation and a 10-year extension of the maximum weighted average maturity on €96.4 billion of EFSF loans, and the ‘step-up’ interest rate margin on the debt buy-back instalment was conditionally scrapped until 2022 and permanently thereafter.

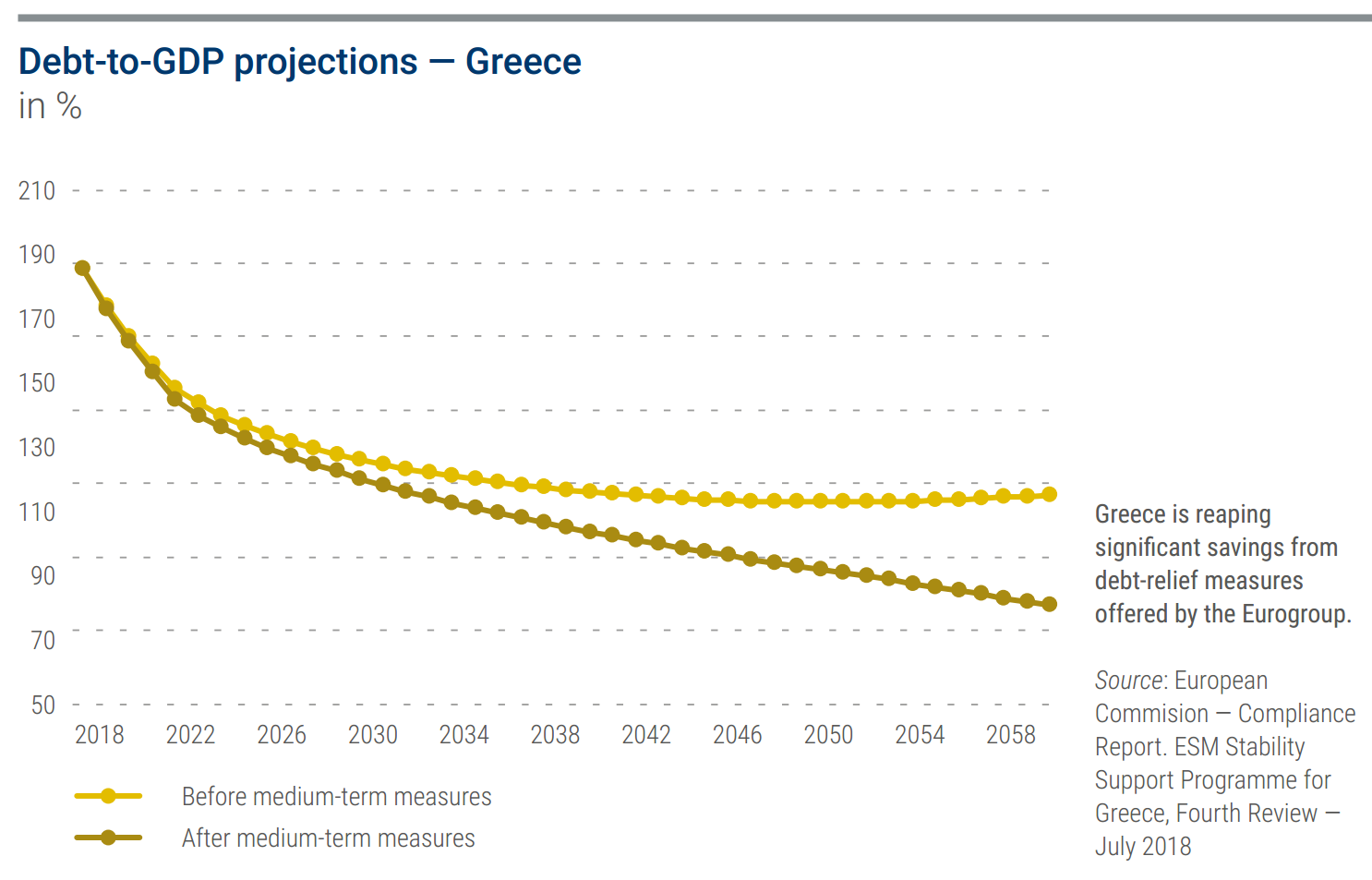

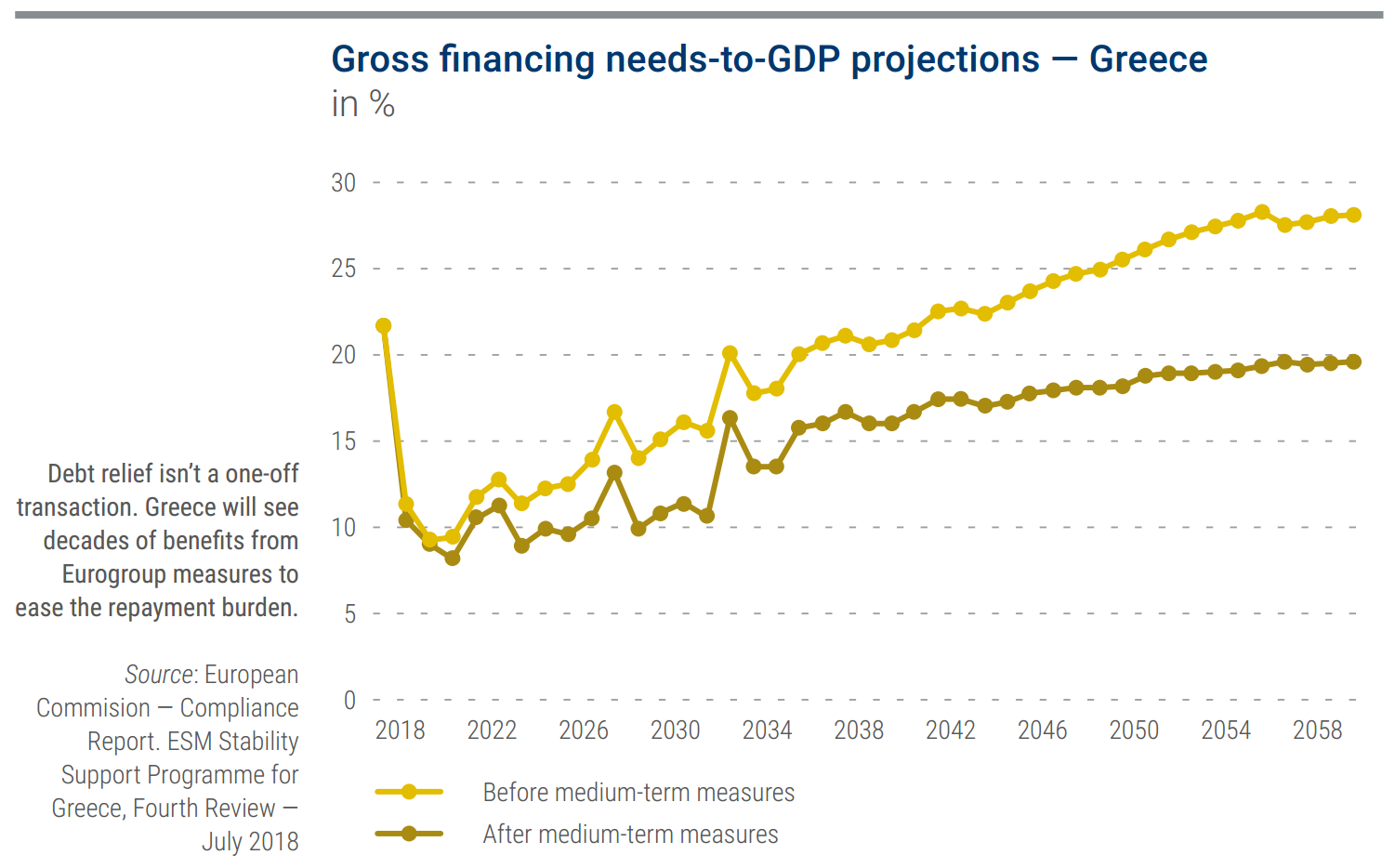

Greece, which is projected to have had debt of 188.6% of GDP in 2018[12], stands to reap considerable benefits. Building on the savings brought about by the short-term measures in 2017, the European institutions estimate that the medium-term measures of 2018 are likely to reduce Greece’s debt ratio by 30 percentage points in 2060, to 96.8% of GDP, and its gross financing needs by eight percentage points, to 19.8%[13].

But it didn’t end there: in a tribute to the long-term nature of Greece’s financial commitments, the Eurogroup pledged to examine ‘whether additional debt measures are needed’ when Greece starts paying down the principal on its EFSF loans in 2032. And it underlined a willingness to intervene earlier if the Greek economy stumbled[14].

There were, however, no giveaways. Greece will remain under surveillance by the Commission and ESM, and key features of the debt-relief package are contingent on the Greek government upholding its economic pledges. Greece’s recovery of central bank profits from its bonds, for example, hinges on the fulfilment of a host of policy commitments made at the June 2018 Eurogroup meeting[15].

Enhanced surveillance ‘is appropriate, given the large amount of money that has been disbursed, and also the unprecedented debt relief,’ Regling told the media after that meeting. ‘Therefore, the post-programme monitoring is tighter than in the other cases’[16].

The ESM’s view is that, as long as Greece remains fiscally prudent while shoring up the economy, the debt can be paid back on schedule. Eurogroup steps have eased Greece’s debt repayments, but the ultimate success of the programme lies in the Greek government’s continued reform implementation.

‘It is very unusual to make such long-term plans. But it follows from the very unusual situation in Greece. No other country has ever received so much money from its partners,’ Regling said. ‘The amounts were unprecedented – this has never happened anywhere in the world before – and the terms were extremely favourable. We want to help Greece regain debt sustainability and we want Greece to have a strong, healthy economy, with good growth, where employment is returning and jobs are created.’

Continue reading

Next chapter

Download

Order

[1] Greece (2018), ‘Hellenic Republic public debt bulletin’, No. 92, December 2018. www.pdma.gr/attachments/article/2048/Bulletin%20Νο_92.pdf

[2] IMF (2018), ‘Greece: Staff concluding statement of the 2018 Article IV mission’, 29 June 2018. https://www.imf.org/en/News/Articles/2018/06/28/ms062918-greece-staff-concluding-statement-of-the-2018-article-iv-mission

[3] Eurogroup statement on Greece of 22 June 2018, 22 June 2018. https://www.consilium.europa.eu/en/press/press-releases/2018/06/22/eurogroup-statement-on-greece-22-june-2018/

[4] Eurogroup (2018), ‘Main results’, 21 June 2018. https://www.consilium.europa.eu/en/meetings/eurogroup/2018/06/21/

[5] ESM (2018), ‘Greece successfully concludes ESM programme’, Press release, 20 August 2018. https://www.esm.europa.eu/press-releases/greece-successfully-concludes-esm-programme

[6] Eurogroup statement on Greece, Press release, 9 May 2016. http://www.consilium.europa.eu/en/press/press-releases/2016/05/09/eg-statement-greece/

[7] Eurogroup statement on Greece, Press release, 5 December 2016. http://www.consilium.europa.eu/en/press/press-releases/2016/12/05/eurogroup-statement-greece/

[8] Greece, Ministry of Finance (2016), ‘Letter from Euclid Tsakalotos to Jeroen Dijsselbloem and Klaus Regling’, 23 December 2016. http://www.tovima.gr/files/1/2016/12/27/TSAKALOTOS11.pdf

[9] Eurogroup statement on Greece, 5 December 2016. http://www.consilium.europa.eu/en/press/press-releases/2016/12/05/eurogroup-statement-greece/

[10] Eurogroup statement on Greece, 15 June 2017. http://www.consilium.europa.eu/en/press/press-releases/2017/06/15/eurogroup-statement-greece/

[11] Ibid.

[12] European Commission (2018), ‘Compliance report: ESM stability support rogramme for Greece – fourth review’, 9 July 2018, p. 42. http://www.consilium.europa.eu/media/36299/compliance_report_4r_2018-06-20-docx.pdf

[13] EFSF (2018), ‘EFSF approves medium-term debt relief measures for Greece’, Press release, 22 November 2018. https://www.esm.europa.eu/press-releases/approval-medium-term-debt-relief-measures-greece

[14] Eurogroup statement on Greece of 22 June 2018, Press release, 22 June 2018. http://www.consilium.europa.eu/en/press/press-releases/2018/06/22/eurogroup-statement-on-greece-22-june-2018

[15] Specific commitments to ensure the continuity and completion of reforms adopted under the ESM programme, Annex to Eurogroup statement on Greece of 22 June 2018. http://www.consilium.europa.eu/media/35749/z-councils-council-configurations-ecofin-eurogroup-2018-180621-specific-commitments-to-ensure-the-continuity-and-completion-of-reforms-adopted-under-the-esm-programme_2.pdf

[16] ESM (2018), ‘Klaus Regling at Eurogroup press conference’, Transcript, 22 June 2018. https://www.esm.europa.eu/press-releases/klaus-regling-eurogroup-press-conference-9