6. All eyes on Luxembourg: ‘let’s do this’

The EFSF had to move quickly: the euro area’s new fund had only a three-year lifespan. First, it needed a home.

Luxembourg was the consensus choice. Tucked away between Belgium, France, and Germany, the Grand Duchy is known for its financial savvy and stalwart support for the European project. In addition to being the home country of Juncker, the current European Commission president who was then the premier of Luxembourg and head of the euro area finance ministers’ group, the Grand Duchy was also recognised as a financial industry hub. Luxembourg is home to many banks, pension funds, and wealth managers, given its regulatory and legal framework and its status as the second-largest investment fund centre in the world. One of Europe’s smallest countries, with a population now around 600,000, it was already home to such EU institutions as the EIB, the Court of Justice of the European Union, and the European Court of Auditors.

On 7 June, less than a month after the go-ahead for the new mechanism, the EFSF was legally established by the Eurogroup. When the time came to put the paperwork in order, its birth a few weeks later was both prosaic and momentous. Its founding chief executive, Regling; its director, Heinrich, who was also Luxembourg’s treasurer-general; and Luc Frieden, then Luxembourg’s finance minister, assembled in a meeting room on the third floor of the finance ministry with a local notary, Maître Jacques Delvaux. There had been some talk of an even more ad hoc operation, but Delvaux found the occasion significant enough to hold an impromptu ceremony. ‘He said “oh, for something like that, for a historical event like that, I’m going to come down myself to the ministry,”’ Heinrich remembered. ‘Then he was reading out the acte notarié to us and setting up the company.’

For the first few weeks, Luxembourg would be the EFSF’s sole shareholder after it was incorporated as a company under Luxembourg law. Hosting the temporary firewall prompted little domestic controversy. ‘In other countries, that could have led to drawn-out parliamentary discussions. Here in Luxembourg, we decided expeditiously: “Let’s do this,” and we did,’ said Heinrich. To get the EFSF operational, Luxembourg furnished €31,000 as start-up capital and provided a loan for initial operating expenses.

The EFSF had a public service mandate from its inception, and it would grow into an international financial institution in the form of its permanent successor, the ESM.

The first EFSF meetings were an awakening for the finance ministry deputies who made up its board, many of whom were economists used to analysing data and solving thorny political problems – not running a company. In those initial weeks, Heinrich was the lone director of the EFSF until all the euro area states had joined. Later, from December 2011 to March 2014, he would serve as chairman of the EFSF’s governing body, the Board of Directors.

This corporate structure had some interesting requirements. For example, Heinrich remembers having to read speaking notes prepared by the EFSF’s legal advisors at the start of every meeting or conference call, and he said he became an overnight expert in Luxembourg’s corporate law.

Then there was the question of personal liability. Italy, which has a history of public officials serving on private boards in their official capacity, determined that EFSF directors might have personal liability if the firewall ever defaulted on one of its bonds. So, just in case, the Italians arranged to insure their representative for the princely sum of about €2 billion. Heinrich said that, paradoxically, the out-of-this-world figure took the pressure off other countries to provide similar insurance, and put him at ease about taking on personal responsibility for the fledgling fund. ‘If it were €1 million or €250,000, maybe I would be worried,’ Heinrich said. ‘But if it’s €2 billion, we’re done for anyway, so stop worrying about it. This €2 billion is an amount that is too big to rationalise,’ he said, adding: ‘We shelved that discussion.’

For legal corporate governance reasons, member states were not allowed to designate alternates but instead needed to issue proxies to each other’s representatives for meetings when their representative could not attend. Because of the urgency of the crisis, the EFSF board meetings contacted participants no matter where they were, or what the time of day.

‘Today, when I travel, I still remember all of the various places from which I’ve chaired EFSF Board of Directors conference calls: in the departure or arrivals halls of airports all over Europe, and the TGV to Luxembourg, on the beach in Borneo where there was a huge thunderstorm,’ Heinrich said. ‘We were having these conference calls, all of us, in the most unlikely places, just all over the world.’

Regling had been shepherding the new organisation from its inception, and on 1 July he officially stepped into the role of chief executive officer. On taking the helm, Regling had to deploy all of his considerable connections and management skills. Everything from trading software to the most mundane office materials needed to be bought and installed.

‘Building up the two institutions from scratch under considerable pressure is not easy work. But he did a terrific job,’ said Furusawa, deputy managing director at the IMF, who knew Regling from his early IMF days.

Regling drew on the EU’s existing expertise to set up the fund as quickly as possible. The Commission, the ECB, and the EIB all promised to lend aid and sent over one staff member each. ‘They all knew this would create a lot of work initially to set it up. They all promised to help,’ Regling said. ‘I had nothing – there was no office, no staff, no telephone number, no email address.’

The EIB was a first port of call in getting the new organisation off the ground. The EIB hadn’t wanted to take on the rescue mission in addition to its existing portfolio, but it was willing to lend a hand in the build-up phase. Regling recalls his first meeting with his new neighbours, at which about 15 EIB staffers briefed him on what needed to be done. ‘Each one explained to me what I needed to do in a different area – from recruiting staff to organising an office. And then on substance, it was rating agencies, preparing for issuing bonds and bills. It was amazing,’ he recalled.

Focus

A role for the European Investment Bank?

Early in the euro area’s crisis-fighting brainstorming, the EIB popped up as a potential vehicle for providing third-party, market-oriented aid. However, taking on an ambitious new mission would have required new capital for the EIB to ensure its hold on its essential AAA credit rating. A further complication was that the EIB is an EU institution that represents all EU Member States and operates around the world, whereas the EFSF would be designed to target the single currency area alone. The EIB’s Members were not looking for the investment bank to take on greater exposure to the euro area.

In the end, Member States decided that crisis-fighting powers weren’t a good fit with the EIB’s traditional role of financing development projects in Europe and around the world. But the EIB could offer advice, staff, and office space.

‘We had a lot of long crisis meetings with EIB risk, legal, finance, and corporate governance to decide how best to handle it. The uncertainty of the EFSF rating was a big issue for the EIB. There was a fear that the EIB’s rating could deteriorate. At the same time, the EIB wanted to help, in the end deciding to do so at arm’s length,’ recalls Secretary General Kalin Anev Janse, who worked at the EIB at the time and was coordinating the EIB’s support for setting up the EFSF.

As his second-in-command and chief finance officer (CFO), Regling hired Christophe Frankel, a Frenchman who had served in senior positions at the French government debt agency and in private sector finance. Strauch, who had been at the ECB, also joined immediately as chief economist.

Starting with a blank slate was intimidating but also offered opportunities. ‘It was a challenge but at the same time very positive,’ Frankel said. ‘We could build something that was really adapted to our needs.’

Regling outsourced whatever he could. For example, market borrowing operations would be carried out by the German Finance Agency and the EIB would handle accounting and information technology. He also turned to Anev Janse.

Only a few years out of university, where he had been active in Dutch politics, Anev Janse was working at McKinsey & Company and then moved to the EIB for a one-year secondment during the crisis. He was then assigned to the EFSF project, where he would begin building the EFSF’s internal structure while Regling, Frankel, and Strauch focused on winning over the policymakers and markets. As it happened, Anev Janse was wheeling his suitcase out the door for a trip to Amsterdam, but his supervisor stopped him: plans had changed. The call had come in to work on the EFSF, and that would be Anev Janse’s job. The temporary assignment became permanent when Anev Janse was appointed the firewall’s secretary general starting in 2011. He was impressed by Regling from the start.

‘As a boss he is great,’ Anev Janse said. ‘He trusts his staff. He can be tough and very challenging at the same time; he’s very clear about what he wants delivered.’

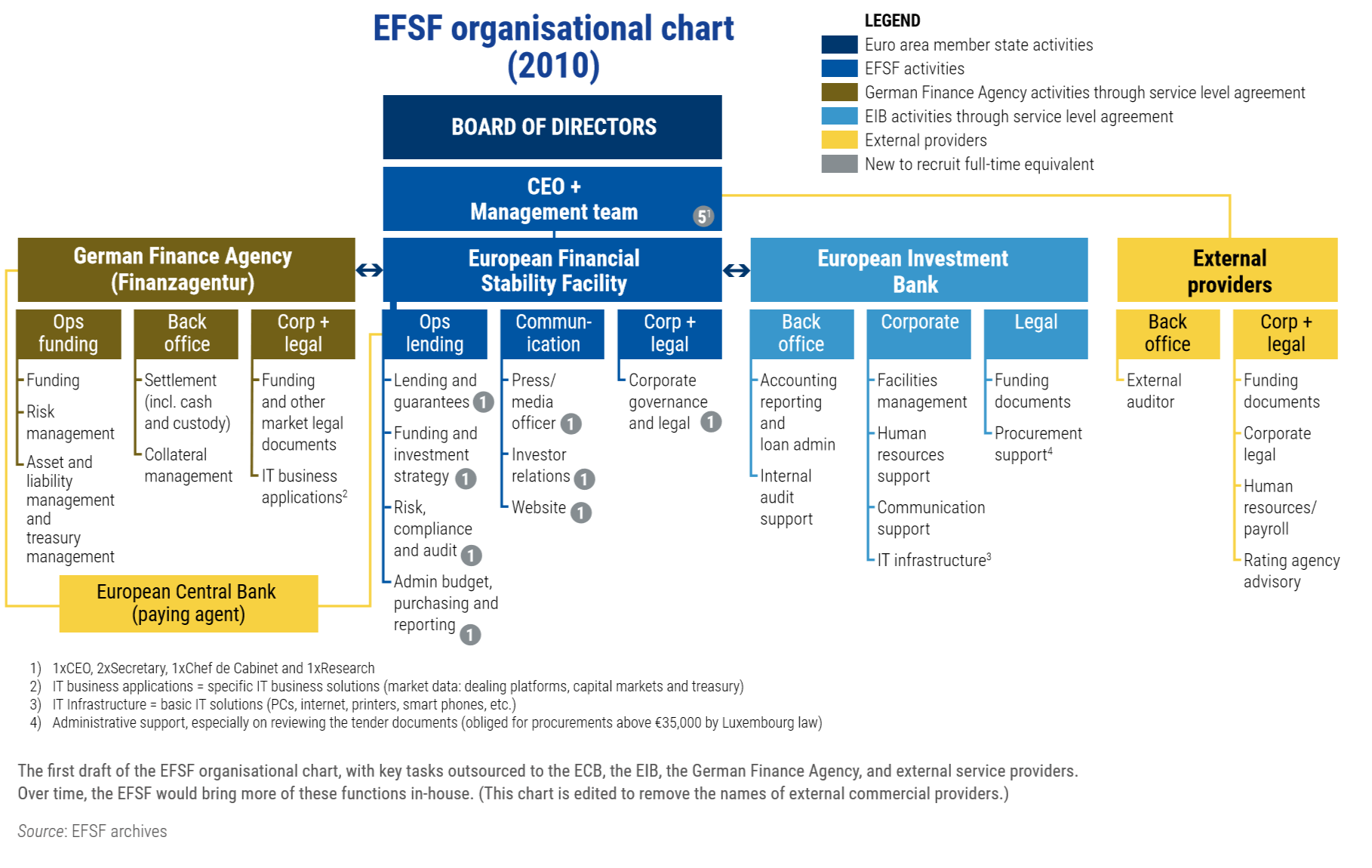

The EFSF was originally conceived of as a 12-person shop, as shown by the institution’s founding organisational chart. This staffing framework was one of the first data points Regling could show to a curious yet cautious global investor base as part of the long process of building confidence. In July 2010 – before the firewall was fully up and running – Regling took the chart to an Asian investors’ conference in Beijing hosted by Singapore’s sovereign wealth fund.

The organisational chart was never an exact model. From the very beginning, new hires took on multiple roles and dedicated their waking hours to getting the firewall off to a good start, and functions were expanded or absorbed as the organisation grew. Conceptually, however, the organisational chart was instrumental. The first step for the new firewall was literally centring itself in order to get organised.

‘When Kalin did the first organigram with me, he wanted to put the EIB in the centre and the EFSF was on one side. I said “No, no. We should change this around. The EFSF is at the centre and the EIB is on the side, alongside the German Finance Agency,”’ Regling said.

A dozen people was a lean concept for an organisation as ambitious as the EFSF, and even that number did not assemble overnight. ‘The concept of having 12 was not stupid; it was possible to do this,’ Regling said. One can do a lot with just a few people, who work very hard. And we had the support of the German Finance Agency and the EIB.’

The early team was extraordinarily dedicated – as they needed to be. The crisis was turning so many lives upside down, and everyone who signed up was motivated to do as much as they could. It certainly couldn’t be only for the money. ‘We never spent in an exaggerated fashion,’ said Ralf Jansen, the firewall’s first general counsel. ‘There was always this sense of soberness. Being down to earth. Not overdoing it. How would you talk to a Greek pensioner absorbing a cut if Klaus lived a life of luxury?’

Jansen welcomed the prospect of joining a team with a purpose larger than itself. It was a unique opportunity to do something that people might one day consider historic. There was no roadmap, no time to worry about what would happen if something went wrong. ‘We joined for the project. It’s amazing looking back – the amount of money and risk we dealt with. Coordination basically took place while we were doing it.’

As the EFSF started operations and the euro area began expanding the facility’s duties while planning for a permanent fund, it became clear that the firewall would have to be beefed up. Shareholders would expect the rescue fund to have ironclad risk management and auditing abilities, given the amount of money at stake.

Recruiting letters went out to other international financial and private sector institutions. ‘It was a call for help – we are trying to manage this crisis, we need help and we need your people,’ Anev Janse said. ‘The way we came together was a bit of coincidence, but that made us extremely strong.’

Continue reading

Next chapter

Download

Order