Less special, less contagious? US Treasury supply spillovers to Bund yields

High public debt in the United States (US) is Europe’s problem too. When the US issues more bonds (Treasuries) and US government bond yields rise, German government bond (Bund) yields tend to follow. We find that the size of these spillovers is not fixed; when investors perceive US Treasuries as less ‘special’ compared to German Bunds, spillovers weaken. Greater insulation from US fiscal dynamics comes with caveats: fragmentation risks within the euro area remain and the Bund market is too small to absorb a significant reorientation of safe-asset demand. Any window of opportunity relies on policy choices Europe has so far deferred.

High public debt in the US is Europe’s problem too

US Treasuries are the world's dominant safe asset, anchoring sovereign bond yields globally. When US Treasury supply rises and US yields follow, Bund yields tend to rise too.[1] Since Bunds serve as the euro area's own benchmark, there are ripple effects to euro area borrowing costs, fiscal sustainability, and financial stability. Given the US’s persistently high deficits[2] and repeated bouts of market volatility triggered by current US policy, quantifying how large these spillovers are – and what conditions them – has rarely been more urgent.

Several channels link US Treasury supply to Bund yields

- Duration repricing: Long-term bonds in global circulation mean investors demand higher compensation to hold them, pushing up long-term yields everywhere.

- Portfolio reallocation: In general, higher US Treasury supply raises US Treasury yields (Phillot, 2025) and attracts inflows into US Treasuries, reducing demand for Bunds and pushing Bund yields up as well.

- US dollar appreciation: Inflows strengthen the US dollar. While a stronger US dollar would increase euro area competitiveness, it would also increase import prices and inflation compensation in yields, effects we do not study here.

US Treasuries command a premium beyond their financial return

Because US Treasuries serve as the world’s main reserve asset, store of value, and collateral, investors value them above and beyond what their financial return would justify – a premium known as the convenience yield. An increase in US Treasury supply makes Treasuries less scarce and hence less ‘special’ in this sense, reducing this premium (Krishnamurthy and Vissing-Jorgensen, 2012; Jiang et al., 2025). This can have two opposing effects: if the higher supply generates investor concerns about US fiscal sustainability, safe-haven demand may tilt towards alternatives such as Bunds and dampen the spillovers of US Treasury supply shocks to Bund yields. But if a change in convenience premium makes US Treasuries more comparable to – and hence more readily substitutable with – Bunds, investors may rebalance more freely between them, amplifying spillovers. The net effect is an empirical question, addressed in this blog.

Unexpected increases in US Treasury supply raise Bund yields

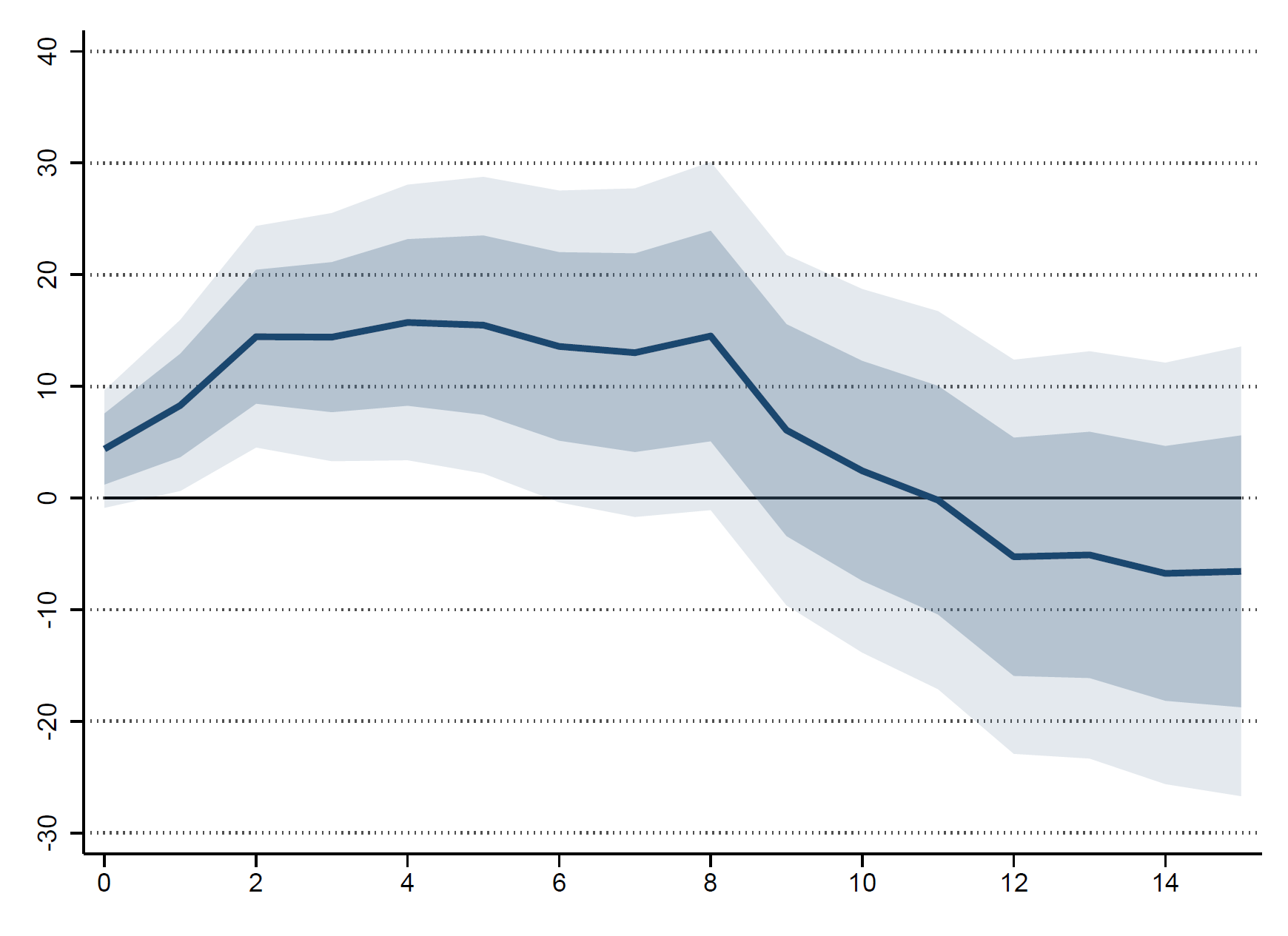

Building upon the work of Phillot (2025) – who uses future price movements around US Treasury supply announcements to isolate unexpected changes in supply – we estimate the impact of US Treasury supply shocks on Bund yields using state-dependent local projections over 1998 to 2025. We focus on the international transmission of these shocks at the long end of the yield curve.[3] We find that an unexpected USD 25 billion increase (one standard deviation, or 0.8% of US gross domestic product) in US Treasury net supply raises Bund yields by 10-15 basis points, with the effect persisting for roughly 10 days (Figure 1).

Figure 1

US Treasury supply increases raise Bund yields

Bund response to US Treasury supply shock (in basis points)

Notes: The plot shows the cumulative impulse response function of 10-year Bund yields to a one standard deviation increase (~USD 25 billion) in US Treasury net supply at daily frequency from 1998 to 2025. The shaded areas are the confidence intervals at the 68% and 90% levels, computed using Newey-West standard errors. The x-axis represents business days from impact.

Source: ESM calculations based on an extension of Phillot (2025), using data from Portara, Bloomberg, TreasuryDirect, and Deutsche Finanzagentur

US Treasury supply increases thus make it more expensive for euro area governments to borrow, all else equal. But this headline figure conceals important variation: how much investors value US Treasuries relative to Bunds beyond their financial returns determines how far any given US Treasury supply shock travels.

Lower US Treasury convenience premium dampens spillovers to Bund yields

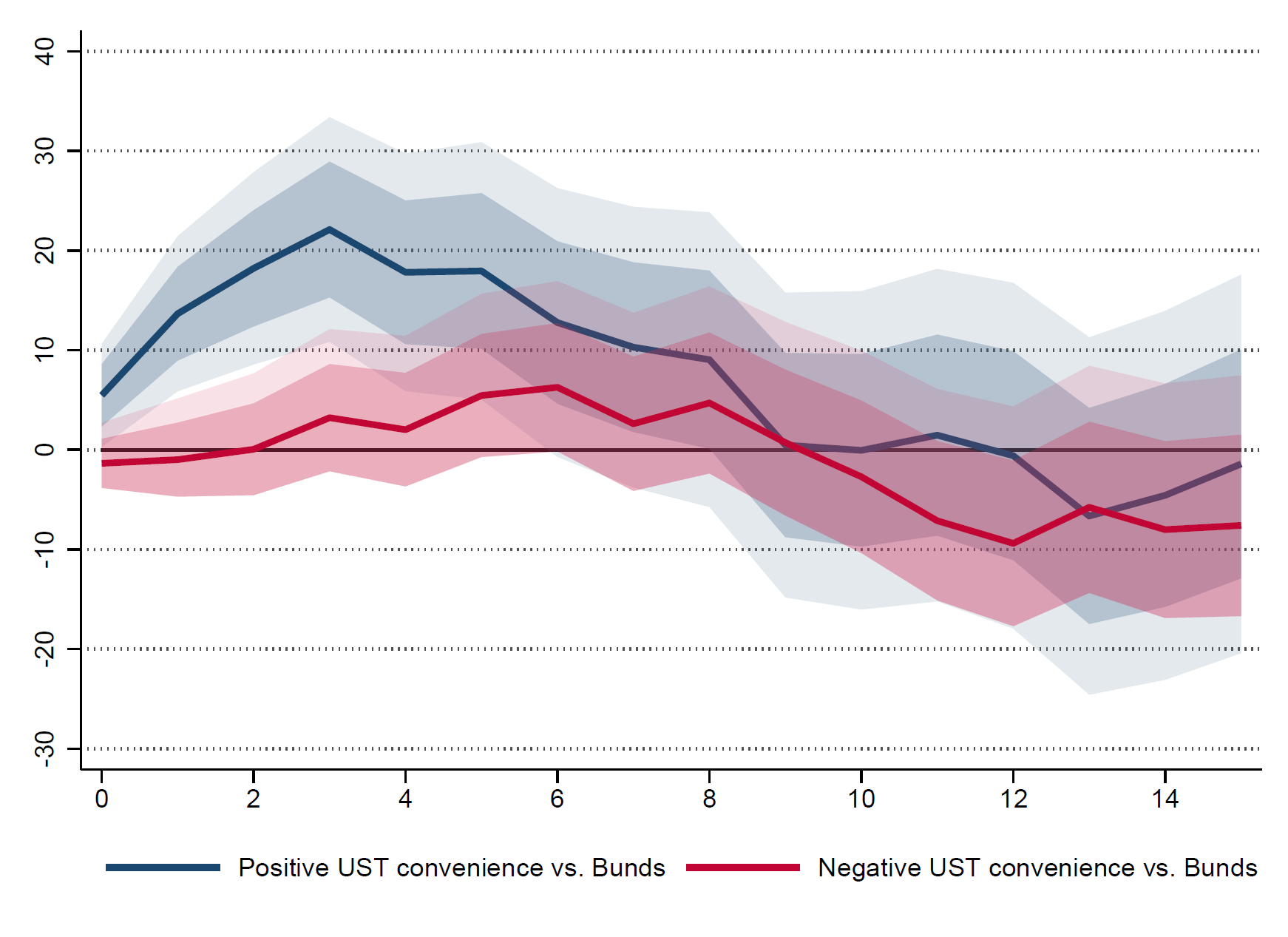

We document that spillovers depend systematically on how ‘special’ US Treasuries are perceived as compared to Bunds.[4] When investors consider US Treasuries relatively less ‘special’, Bund yields’ response to a given US Treasury supply shock is significantly weaker (Figure 2).[5]

Figure 2

A lower US Treasury convenience premium dampens spillovers to Bund yields

Bund response to US Treasury (UST) supply shock, by relative UST premium (in basis points)

Notes: The plot shows the cumulative impulse response function of 10-year Bund yields to a one standard deviation increase (~USD 25 billion) in US Treasury net supply at daily frequency from 1998 to 2025. The shaded areas are the confidence intervals at the 68% and 90% levels, computed using Newey-West standard errors. The x-axis represents business days from impact.

Source: ESM calculations based on an extension of Phillot (2025), using data from Portara, Bloomberg, TreasuryDirect and Deutsche Finanzagentur

This may be because safe-haven flows towards Bunds partially offset the upward pressure on Bund yields from a supply shock, dampening its impact.[6] Du et al. (2018, 2026) document a recent decline in US Treasury convenience relative to Bunds – suggesting that, in the current environment of elevated investor concern about the US policy trajectory, attenuation of spillovers to Bunds may already be operating.[7]

Greater insulation from US fiscal dynamics may be uneven across the euro area and mask risks

A world in which Bund yields are less tightly coupled to US fiscal dynamics would afford the euro area greater fiscal and financial autonomy, but there are two important caveats:

- Bund yield compression may coincide with euro area fragmentation risks. Any potential safe-haven flows need not benefit periphery spreads. If the decline in relative US Treasury convenience reflects US institutional deterioration rather than structural European improvement, a global risk repricing would weigh disproportionately on higher-risk euro area sovereigns.

- The Bund market alone is too small to absorb a more substantial reorientation of global safe-asset demand. The stock of European safe assets – including those issued by the ESM – has grown significantly, exceeding €1.4 trillion today. Other highly-rated sovereigns globally could absorb part of any shift – but for Europe to capitalise on changing global safe-asset preferences would require further steps to expand European safe asset issuance.

With the US fiscal trajectory showing few signs of stabilising and growing investor concern about US policy predictability, the global financial order centred on US Treasuries is under strain. This blog’s findings are a reminder that US fiscal dynamics directly affect euro area borrowing cost. Hence, how the global safe-asset landscape evolves from here looks set to shape European sovereign markets.

References

Arcidiacono, Cristian, Matthieu Bellon and Matthias Gnewuch (2024): “Dangerous Liaisons? Debt Supply and Convenience Yield Spillovers in the Euro Area”. European Stability Mechanism Working Paper No. 63. DOI: 10.2139/ssrn.5034668 Link

Cornevin, Antoine and Jemima Peppel-Srebrny (2026): “A Hierarchy of Havens: Spillovers from US Treasury Supply Shocks across Euro Area Sovereigns”. European Stability Mechanism Working Paper, forthcoming 2026.

Dilts Stedman, Karlye and Andrew Hanson (2025): “Unconventional Monetary Policy Spillovers and the (In)convenience of Treasuries”. Federal Reserve Bank of Kansas City Working Paper No. RWP 25-10. DOI: 10.2139/ssrn.5441798 Link

Du, Wenxin, Joanne Im and Jesse Schreger (2018): “The U.S. Treasury Premium”. Journal of International Economics, Volume 112, 2018, 167-181. DOI : 10.1016/j.jinteco.2018.01.001 Link

Du, Wenxin, Ritt Keerati, and Jesse Schreger (2026): "Decoupling Dollar and Treasury Privilege", National Bureau of Economic Research Working Paper No. 35000. DOI:10.3386/w35000 Link

Gourinchas, Pierre-Olivier, Walker Ray, and Dimitri Vayanos (2025): "A Preferred-Habitat Model of Term Premia, Exchange Rates, and Monetary Policy Spillovers." American Economic Review 115 (11): 3788–3824. DOI: 10.1257/aer.20220379 Link

Jiang, Zhengyang, Richmond, Robert and Tony Zhang (2025): “Convenience Lost”. National Bureau of Economic Research Working Paper No. 33940. DOI: 10.3386/w33940 Link

Krishnamurthy, Arvind and Annette Vissing-Jorgensen (2012): “The Aggregate Demand for Treasury Debt”. Journal of Political Economy, 120(2), 233–267. DOI: 10.1086/666526 Link

Nenova, Tsvetelina (2025): “Global or regional safe assets: Evidence from bond substitution patterns”. BIS Working Papers No. 1254 Link

Miranda-Agrippino, Silvia and Hélène Rey (2020): "U.S. Monetary Policy and the Global Financial Cycle". The Review of Economic Studies, vol. 87(6), pages 2754-2776. DOI: 10.1093/restud/rdaa019 Link

Phillot, Maxime (2025): "US Treasury Auctions: A High-Frequency Identification of Supply Shocks". American Economic Journal: Macroeconomics 17 (1): 245–73. DOI: 10.1257/mac.20210243 Link

Acknowledgments

The authors would like to thank Andrzej Sowinski, Konstantinos Theodoridis, Pilar Castrillo, Rolf Strauch, Raquel Calero, Cedric Crelo and Peter Lindmark for their valuable suggestions and contributions to this blog.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager