Forging the Future of Monetary Union - speech by Rolf Strauch

Rolf Strauch, ESM Chief Economist

“Forging the Future of Monetary Union” 1

52nd Konstanz Seminar

Online, 9 September 2021

(Please check against delivery)

Ladies and gentlemen,

good afternoon, and thank you for being here and especially Professor Keith Kuester and Professor Jürgen von Hagen for inviting me. It is a great pleasure and honour for me to join this prestigious conference. As a PhD student of Jürgen von Hagen, two and a half decades ago, I was already aware of the great history of this seminar as a “thought platform” for monetary policy and macro topics at the very start of my career. Being able to talk to you today is also, in a very personal sense, a landmark in my “intellectual journey” in working on European issues.

What a great time to think about monetary union and its future! Reflecting the tectonic shifts in the global economy, including in Europe, that have occurred over the past two decades. In my talk today, I will outline the achievements and look at the challenges and opportunities for the euro area going forward. It is based on a policy note jointly written with Markus Rodlauer, which will be published today.

I will argue that the experience of EMU has shown that monetary union can only work successfully with further European policy initiatives. The current macroeconomic setting, and the political imperatives of the post-pandemic world, will re-inforce the quest for monetary and fiscal policy coordination and the move toward greater fiscal and regulatory centralisation. Besides these long-run forces of change, I will also present several key elements of the agenda to be addressed in the next 1-2 years to achieve these goals.

The euro at 21 - achievements

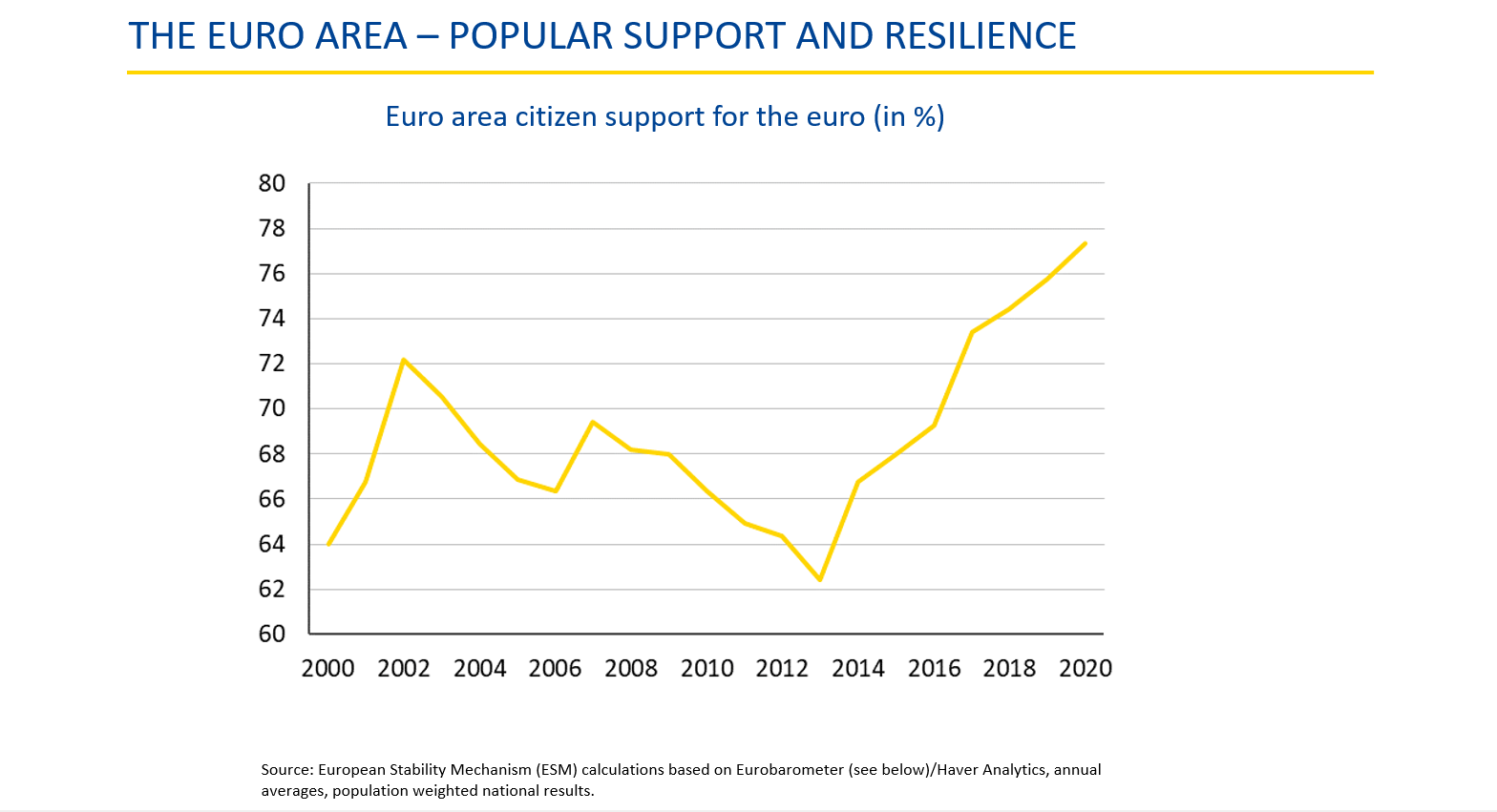

Let me first take a look back at the achievements and challenges monetary union had to master over the past two decades. Over this period, the euro has survived the global financial crisis and the European sovereign debt crisis a decade ago, and is now emerging from the Covid-19 pandemic crisis - yet the euro is more popular than ever since its introduction 21 years ago. The most recent Eurobarometer survey shows that 79% percent of euro area citizens support the single currency.

By 2024 the euro area is likely to comprise 21 of the 27 EU member states, as Bulgaria and Croatia are currently in the accession process.

The success of EMU would not have been possible without the strength and independence of the ECB and the significant institutional reforms—especially in the banking sector—after the global and European crises a decade ago. The ECB’s commanding position as an independent central bank shaping economic and policy expectations in the euro area and its ability to take actions to address major crises are remarkable. And the regulatory reforms at the European level and buffers built in the banking system served us well during the pandemic crisis.

Monetary union was initially built on a rules-based fiscal regime with budgetary means managed by countries. The level of public risk sharing was very low compared to other large currency areas. In managing the twin crises a decade ago, we have seen a significant ramp up of support capacity at the European level with the creation of the ESM – the European crisis resolution mechanism. I believe that our support made an essential contribution to each country’s adjustment and reform efforts when they ran into financial difficulties. Without the ESM, the euro area would not exist in its current form.

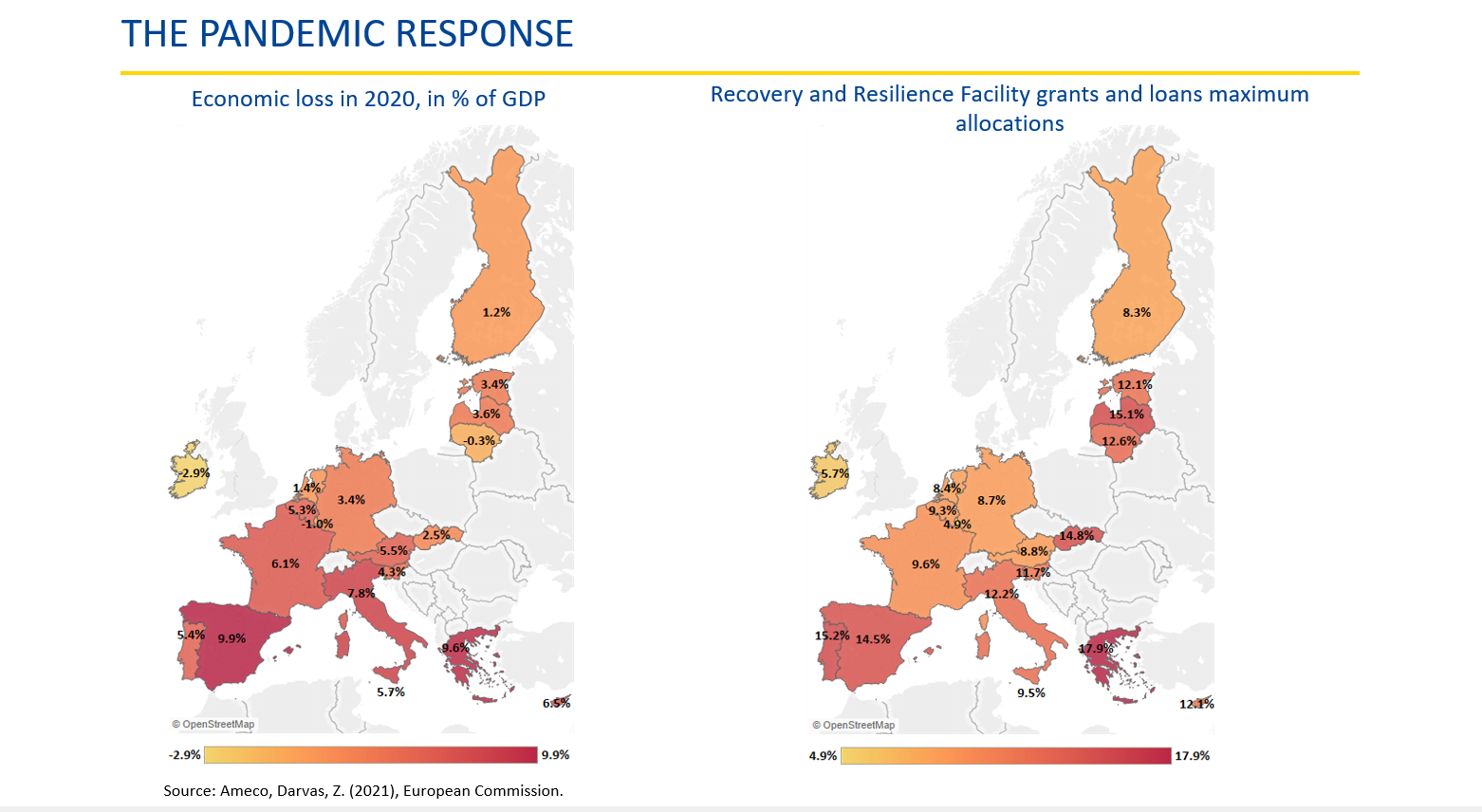

This European support was again significantly strengthened in the pandemic crisis response. Both the first package incorporating measures by the ESM, EIB and EC, and the second phase leading up to Next Generation EU recovery package, have demonstrated a willingness and capacity of the Union to act quickly, jointly, in solidarity and on a large scale. The size of support is larger for countries that suffered more due to the pandemic and those with lower per-capita income.

This sign of the EU’s ‘political maturity’ has helped to preserve the euro area’s integrity through the crisis and further buttressed the euro’s popularity.

The moment for a rethink - challenges and the need for more joint action

The overall support and resilience shown by the euro area during the last 21 years are remarkable, but challenges remain. Let me briefly point to three economic and political challenges and explain why they will imply in my view a further thrust towards fiscal and regulatory centralisation.

- Monetary union has delivered on price stability, but could not delink itself from the secular decline of interest rates and inflation. The limits of monetary policy at the zero lower bound strengthen the case for fiscal support in stabilising the economies. More capacity is needed to react to common and idiosyncratic shocks to stabilize the economy. In practice this calls for a strengthened joint fiscal capacity, as individual-country buffers and policy capacity have proven at times to be insufficient against large shocks.

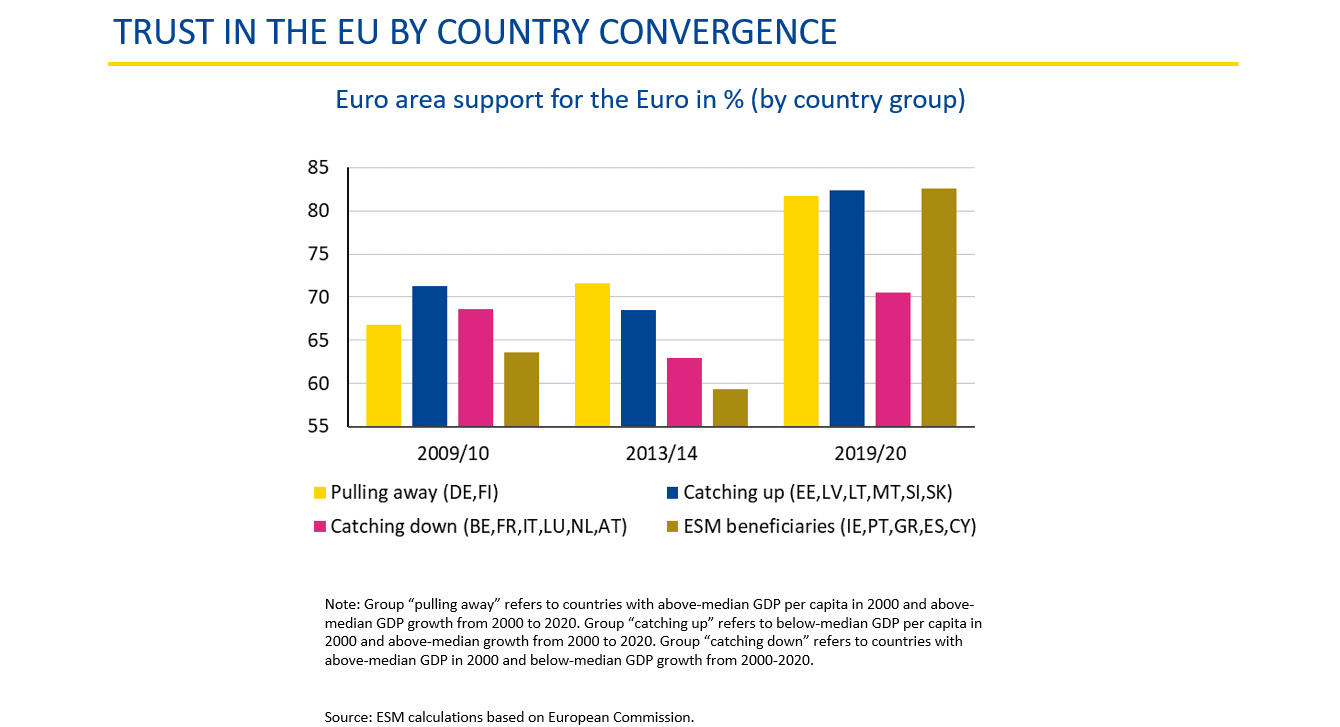

- Economically and politically, monetary union needs a common growth and risk-sharing agenda. The ongoing recovery should allow us to catch up with the past growth trend and ensure that no country or region falls behind. In the past some countries have fallen behind for structural reasons, and income divergence has increased within countries. “Falling economically behind” is the breeding ground for populism and creates a political vulnerability for the euro area. Financial markets in many areas are still segmented and need to integrate further to mobilise financial resources and raise cross-border risk-sharing.

- Climate change has emerged as the key challenge of our times. Effectively addressing it will require to tackle externalities and act globally. Scale of action is critical and there is a clear case for a European agenda and coordinated measures. Increased digitalisation is another critical objective. A common agenda and common resources are needed to stay abreast of technological change and preserve strategic independence.

Post-pandemic: New solutions, old truths

To address these challenges, a post-pandemic agenda for strengthening EMU further should focus on four areas: (1) monetary policy, including its relationship with fiscal policy and sovereign crisis management; (2) European fiscal infrastructure; (3) convergence and investment; and (4) financial markets, risk sharing, and global positioning of the euro.

I. Monetary and fiscal interaction and crisis management

The ECB recently approved a new monetary policy strategy, which is clear in its focus on euro area inflation, medium-term orientation, and primary tools; and it recognises the potential risks to medium-term price stability from financial imbalances and climate change.

While monetary policy should ensure appropriate financing conditions given the overall macro and financial context, it cannot safeguard favourable financing conditions for the sovereign under all circumstances. Country risk should be addressed by appropriate macro, structural and macro-prudential policies at the country level. When needed, official financial support (lender-of-last-resort) should remain conditional on such appropriate national policies. For euro area countries this role has been assigned to the ESM under its enhanced mandate, including joint responsibility with the European Commission for future programme design and monitoring. ESM lending instruments allow to set the policy conditionality according to the needs of the specific case. The ESM is well on track to implement the enhanced mandate, along with the ongoing ratification of the new ESM Treaty.

II. A new European fiscal policy framework—an important complement for monetary union

In a nutshell, we need to revamp and develop our fiscal framework and instruments so that they create the right conditions not only for debt sustainability, but also for sustained growth and stabilisation.

Fiscal rules

There is widespread agreement that the EU fiscal rules should be reformed and streamlined when the period of suspension ends (currently through 2022). Of course, it remains a basic truth that public finances must be sustainable. Governments remain responsible for meeting their current and future payment obligations.

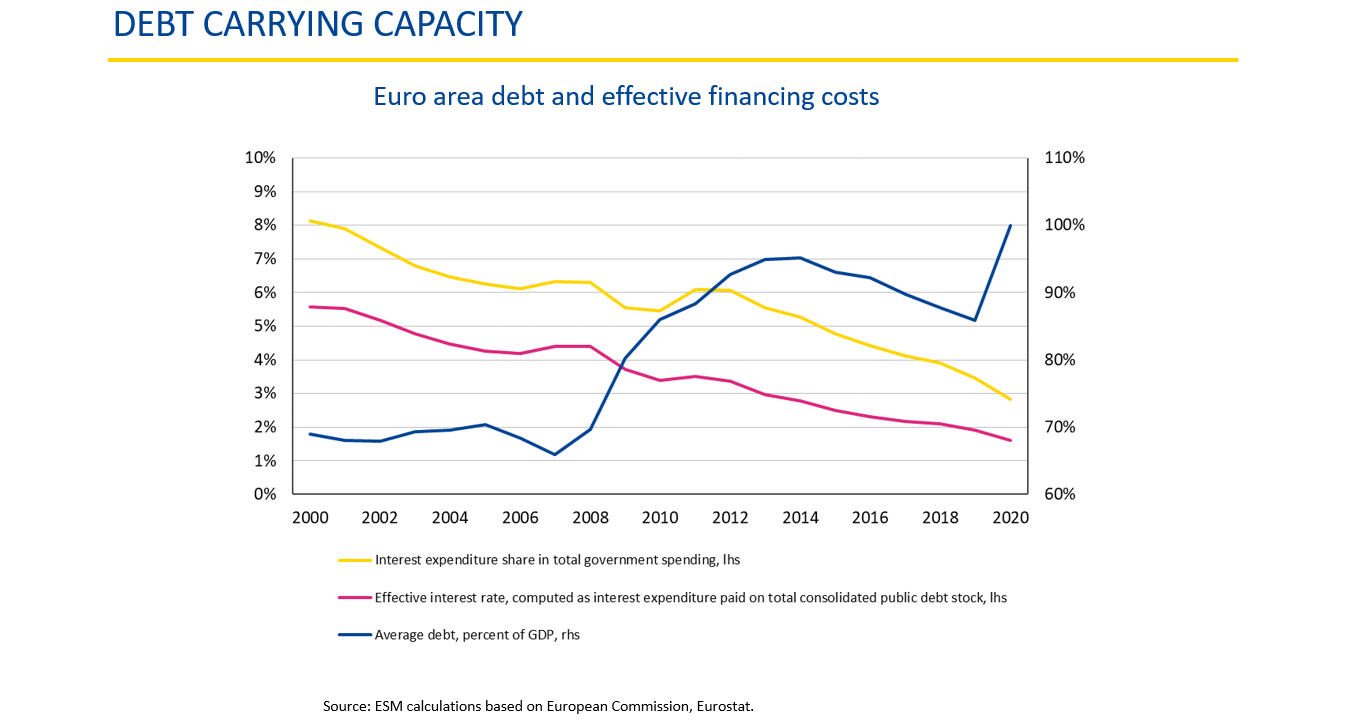

What has changed is that the debt carrying capacity of advanced economies has increased substantially, given low-for-long interest rates, innovations in financial markets, and improvements in countries’ debt management capabilities. Interest payments on public debt have declined sharply as a share of total government expenditures, despite the rise in debt levels.

I agree with the view that a simplified EU fiscal framework could be built around a 3% deficit limit and a modified reference value for the debt-to-GDP ratio. These headline values would be operationalised by an expenditure rule and a debt adjustment path.

As economic growth plays a key role in reducing government debt burdens, the redesigned fiscal rules need to allow for productive, growth-enhancing public investment. Growth-enhancing fiscal policies can be achieved through an improvement in the quality of public finances, and it does not per se require higher deficits.

Stabilisation facility

National fiscal policies often fail to build sufficient buffers during upswings, which constrains the ability to provide stimulus — or even leads to a pro-cyclical (contractionary) stance — in a downturn. It would therefore be practical to complement the reformed framework of EU fiscal rules with a new fiscal stabilisation instrument, to help address country-specific shocks, especially for sharper downturns and more vulnerable countries. As the past experience has shown, national fiscal policies may simply be overburdened when the amplitude of the downturn is substantial.

There have been many ideas and proposals for how such a stabilisation instrument could work. It could take the form of a euro-wide unemployment insurance scheme, a so-called rainy day fund, or an ESM credit line. The goal would be the same: to help smooth intra-EMU cyclical fluctuations in an enhanced, well-circumscribed, public-risk sharing framework — and thereby further strengthen EMU. A stabilisation facility could be based on a revolving fund, upon which countries draw when needed, and which avoids continuous budget transfers.

III. NGEU: convergence and investment

Next Generation EU is an EU-wide instrument, but in the ongoing European recovery efforts, it also contributes to deepening EMU. It is a one-off measure and not a permanent tool. Still, it points toward possible future union-wide solutions to promote convergence and the transformation of our economies, for example, through an enlarged EU budget based on common taxation.

There are two principles in the current setting that should be preserved:

NGEU for the first time creates positive incentives for reforms for participating EU countries. The ESM experience suggests that this is more effective than the current system of fines, which lacks credibility.

And second, focusing on “green taxation” and external trade and transactions is consistent with the EU’s competencies and common objectives. We welcome that the current proposals for new own- resources of the EU include union-wide carbon emission-related levies.

IV. Financial markets, private risk-sharing and the euro

As we are looking to restart our economies, boost investment, and aim for greener, more digital, and more resilient growth, the strong public spark that NGEU is providing must also reach private enterprises, which will inevitably have to be the backbone of future growth.

It is, therefore, a priority that we further progress toward integrated financial markets across the monetary union. European leaders and the European Commission have laid out a twin-track agenda toward this goal, i.e. banking union and capital markets union.

Banking union

Completing banking union is vital given the central role the banking sector needs to play in financing the post-pandemic recovery. A crucial step in completing banking union is the introduction of the ESM backstop to the Single Resolution Fund next year. This backstop serves as a supplemental safety net as it can lend funds to the Single Resolution Fund to finance a resolution in case failing banks deplete the Fund’s resources. A strong, well-financed, and transparent bank resolution mechanism provides prevents ripple effects for other financial institutions and helps to protect people’s deposits. It contributes to the robustness and resilience of EMU.

Additional reforms are needed to complete banking union, and the Eurogroup has been working on four key elements: a European Deposit Insurance Scheme, cross-border integration, the crisis management framework, and the regulatory treatment of sovereign exposures. Much progress has been made toward solutions in all four areas in preparatory work streams; however, political agreement among member states has so far eluded us.

Capital markets union and equity finance

Capital markets union has the potential to change the current inefficiencies in the allocation of savings in a highly fragmented EU financial sector, which hampers investment, innovation, and long-term growth. In comparison with the US, the EU lags behind in terms of use of equity to finance firms, as well as the dynamism of venture capital and initial public offerings. Debt is largely channelled via the banking system.

Strengthening European capital market supervision will boost the attractiveness of the European market for international investors. This calls for steps to facilitate securitisation, support equity finance, improve market access for small firms, and enhance the safety of market infrastructure and regulatory transparency. A safe digital infrastructure, which should eventually include a digital euro, will add to the attractiveness of the European market and the euro.

In the medium term, the integration of capital markets will facilitate cross-border investments, increase risk-sharing, and open up new financing options for companies. This will help sustain growth going forward and boost investment in a greener and more digital economy.

International role of the euro

Banking and capital market union will play a major role in strengthening the international role of the euro. European policy makers have recognised the importance of the topic, which was high on the agenda of the Euro Summit earlier this year. Apart from other benefits, the Recovery and Resilience Facility under the NGEU will sharply expand the pool of euro-denominated safe assets, which can boost the euro in international debt markets, where it lags substantially behind the dollar.

Priorities for action

Looking ahead, EMU can become a well-tuned ‘concert of policies’, national and European, supporting dynamic, sustainable growth for the well-being of citizens across the euro area. We believe that the following priorities should inform a concrete policy agenda for the next year and a half:

- For the banking union, based on the technical work already done, I believe it is time to find common ground on outstanding issues and move ahead. I hope that agreement on a clear decision-making process for the completion of banking union and the establishment of European Deposit Insurance Scheme can be achieved before the end of this year with a view to finalising the legislative work by the end of the current institutional cycle in 2024.

- The ESM will have to be ready to implement the backstop facility from January 2022 onwards. I look forward to the ratification of the new ESM Treaty (expected by the end of 2021). This new mandate will allow the ESM to identify the build-up of economic and financial risks in euro area countries, and help prevent the situation from flaring up.

- For the ECB, as it moves to implementing the new strategic review, the biggest challenge might be to find the right exit path from the extraordinary monetary accommodation employed to fight the pandemic. With the right timing and modalities of exit, we can ensure appropriate financing conditions for the recovery, achieve progress towards the medium-term inflation goal, and preserve financial stability.

- On capital markets union, harmonisation and strengthening European supervision, and ensuring sufficient equity and venture-capital financing during the recovery remains a priority.

- To effectively guide national fiscal policies, it will be important to reach agreement on the revision of fiscal rules in the European surveillance framework well before the end of 2022.

- Successful implementation of NGEU – especially its core component, the Recovery and Resilience Facility – is critical. It will boost the recovery, help set national reform policies on a dynamic and sustainable growth, and provide confidence to the markets.

I hope to see an earnest re-start of the discussion on a fiscal stabilisation tool. This would require a mandate from European leaders to work toward an agreement following an outline of issues and a timetable for completion.

This is an ambitious agenda. Despite all the hesitation we have often seen in European policy making, we have also experienced a great resolve when action was needed. I hope policy makers will live up to the challenge of guiding the euro area from the recovery phase into a modern, resilient and sustainable economy for the coming decades.

Thank you very much for your attention.

1 The views expressed in this speech are my own and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Contacts