WANTED: an updated understanding of bank runs

The 2023 banking turmoil revived questions about whether bank regulation and supervision can properly mitigate new risks emerging in a highly volatile environment. While many have focused on the role of digital technology in bringing about this situation in the US, policymakers and practitioners must acknowledge the other contributing factors to best shape the appropriate policy response.

In this blog, I argue that the combination of digital technology and social media magnifies the impact of digital bank runs which, in and of themselves, are not new. Moreover, a little probing into recent research suggests other fault lines — such as corporate flight-to-quality and lack of deep banking relationships — need to be tackled too.

Digital bank runs: not so new

Digital technology is at the epicentre of today’s bank runs. Hardly anyone would disagree with one Wall Street Journal reporter stating: “Today, through an electronic button, you can empty out deposits overnight. It’s different.” [1]

But this quote dates back to May 1984, appearing in reaction to the near collapse of Continental Illinois—one of the largest US commercial banks at the time—due largely to the electronic withdrawal of large deposits (i.e. a digital run).

Since then, there have been waves of bank collapses followed by efforts to reinforce the regulatory architecture. But technology seems to have outpaced and outdated old ways of thinking about bank outflows.

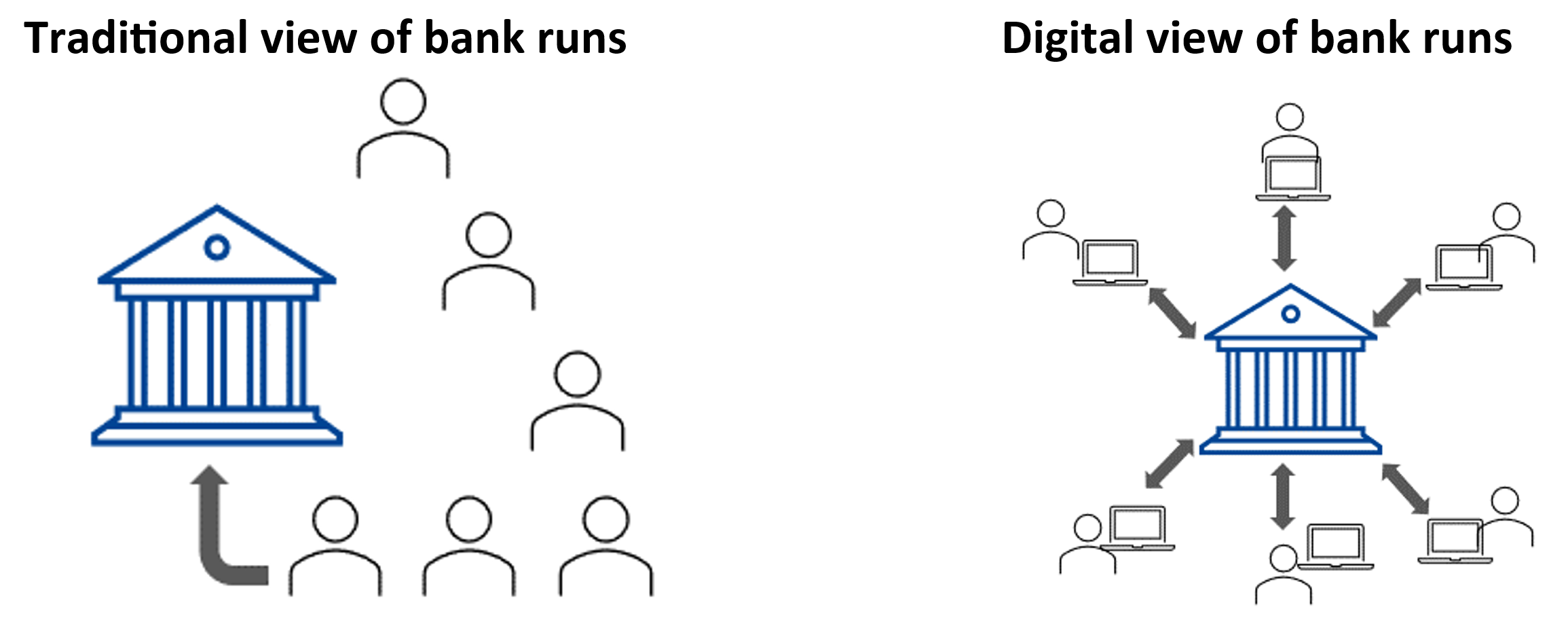

In the traditional scenario, bank runs are driven by retail depositors rushing to withdraw funds before others, thus unleashing a self-fulfilling run. In the digital era, depositors have electronic access to their accounts which, by eliminating the need to queue at the bank, exponentially multiplies the size and speed of outflows.

Source: ESM staff

Social media: a source of contagion

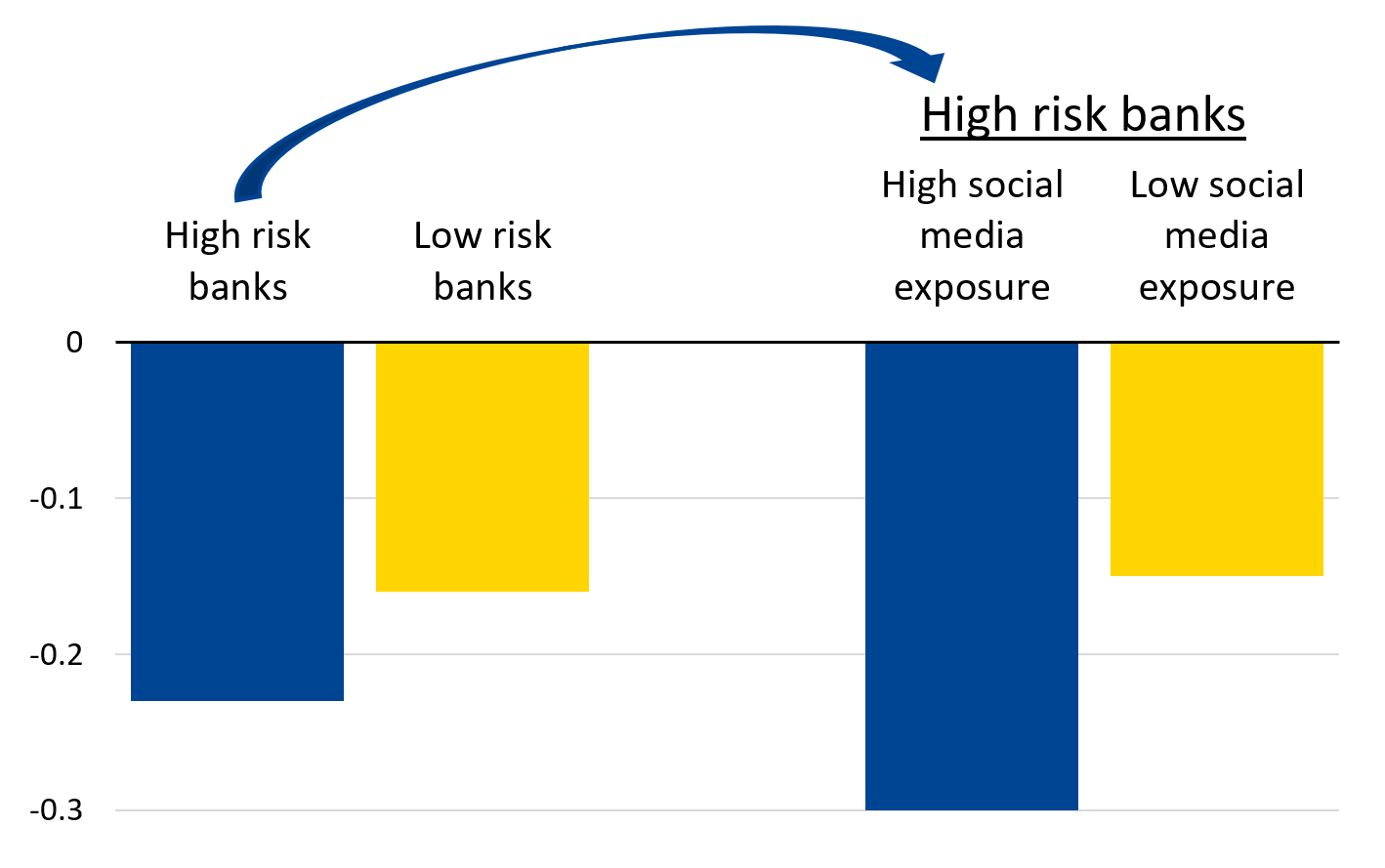

Recent studies suggest that social media has aggravated the impact on banks during runs, reporting that the stocks of banks with higher X (formerly Twitter) coverage suffered more than those with less social media exposure, even for similar levels of risk.[2]

This is not to say that markets have lost the ability to distinguish between riskier and safer banks. In fact, the studies find that “banks with more uninsured deposits and marked-to-market losses experience greater stock losses in the run period.”[3] However, within the group of riskier banks, the social media spotlight leads to larger stock market losses (see Figure 1), making such coverage a new source of contagion. Such punishment does not seem economically justified.

Figure 1: Cumulative stock market returns

(in percentage points)

Notes: Chart shows the cumulative stock returns for a sample of US banks between 6 and 14 March, 2023. Left-hand side: High risk banks are the top tercile of the sample by marked-to-market losses times the percent of uninsured deposits. Low risk banks are the bottom two terciles. Right-hand side: High risk banks are the top half of the sample by marked-to-market losses times the percent of uninsured deposits. Low risk banks are the bottom half. High media exposure are the entities in the top tercile by number of tweets; low exposure are the two bottom terciles.

Source: ESM staff based on Cookson et al. (2023)

Supervisory agencies should explore social media’s role in propagating information and consider potential countermeasures. These could include more active social media messaging to reassure the public on the soundness of the system. Statements about the compliance of specific institutions could be considered too.

Corporates' large deposits can lead to large outflows

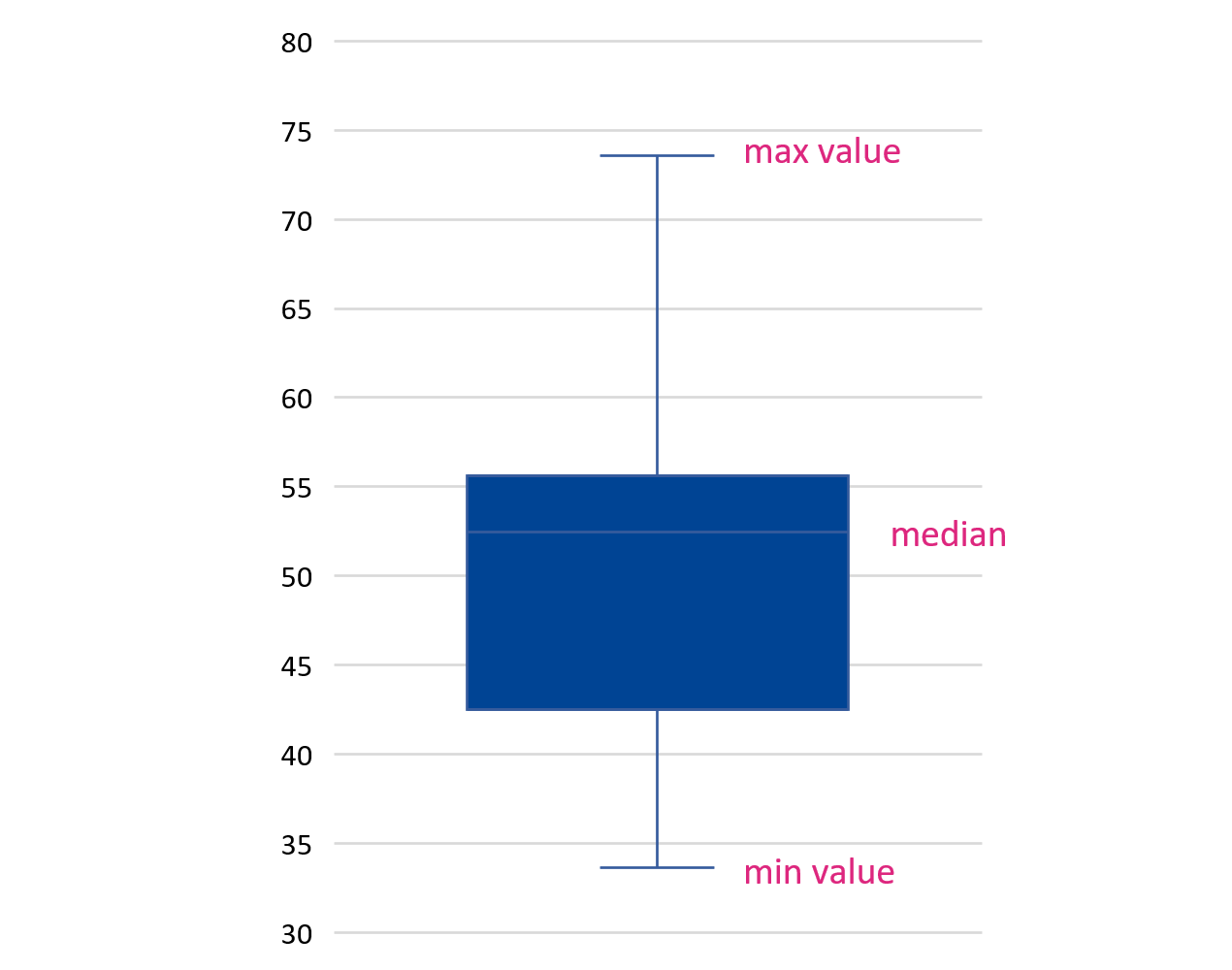

Although much is made in the press about the panic of retail depositors, the evidence suggests that corporates—given their larger deposits and range of reallocation alternatives—often spearhead the substantial outflows leading to the demise of banks. This was clearly the case for US banks in 2023. A similar dynamic could unfold in other jurisdictions where corporate deposits are large (see Figure 2).

Figure 2: Distribution of corporate deposits at selected large European banks in 2022

(in % of total deposits)

Notes: Selected European banks with assets above €300 billion. The blue box shows the range of values across banks, with the top end corresponding to the top third quartile and the bottom end corresponding to the first quartile.

Source: S&P Global Market Intelligence and ESM staff calculations

Moreover, corporate accounts can consist of a small number of entities, making a bank perilously dependent on a few decision-makers. In fact, the top 10 corporate clients accounted for at least 8% to 15% of deposits in several banks that failed in 2023. Risks are compounded further if the corporates operate in the same sector or are connected via business partnerships.[4]

Some supervisory agencies already scrutinise banks’ business models, focusing on governance and risk management practices. However, there is an opportunity to leverage this deep scrutiny to expand their risk analysis on the structure and concentration of their corporate client base.

Relationships are good for stability

Some research based on traditional banking points to deep and longstanding relationships between depositors and banks being an important stabilising factor, and finds that long-tenure depositors and depositors with loans in the same bank are less likely to run, and that members of the same social network tend to run together.[5] Importantly, some authors conclude that “(…) cross-selling [of products] acts not just as a revenue generator but also as a complementary insurance mechanism for the bank.”[6]

These findings should encourage an investigation into whether the same relationship-based dynamics apply in the European context today. Particularly because digitalisation may have made banking relationships more one-sided and fleeting.

Supervisors could consider weighing more positively business models that foster banking relationships.

What to do beyond supervision?

Besides strengthening supervision, there are interesting proposals to bolster the overall regulatory architecture.[7] In particular:

- To reduce the stigma of using the central bank lending facility, banks could be mandated to access this facility at least once a year or quarter. This would normalise the use of this facility for all banks, rather than limiting it to when a bank needs liquidity.

- Regular access to this lending facility would also ensure that the operational requirements for access are in place.

- Readiness would also entail having sufficient collateral to fend off runs. Banks could be asked to pre-position enough collateral to meet all their “runnable” liabilities.

- Extending the business hours of the central bank lending facility—e.g. to 24/7/365—may be necessary given the timeless nature of today’s instant payment systems.

- Additional liquidity buffers designed to fend off very short-term outflows (e.g. five days) may also be needed, as the existing ones cover much longer time frames.

- A further “insurance” element for large corporate deposits could be considered either in the form of additional deposit insurance or collateralisation of these accounts. Limits on large and highly concentrated deposits—e.g. mirroring those on large asset-side exposures—could also be introduced.[8]

Admittedly, all these measures have pros and cons that should be carefully weighed. The Financial Stability Board’s forthcoming report on deposit behaviour and the role of technology and social media might shed some light on these two topics. But measures to temper corporates’ flight-to-safety and the more fleeting nature of today’s banking relationships should not be neglected. In this context, banks with business models consisting of scant product and customer diversification should perhaps receive heightened supervisory scrutiny.

Acknowledgements

The authors would like to thank Paolo Fioretti, Nicoletta Mascher, and Rolf Strauch for valuable discussions and contributions to this blog post, and Raquel Calero for the editorial review.

Further reading

Bank for International Settlements (2023), “Report on the 2023 banking turmoil.”

Cookson, Fox, Gil-Bazo, Imbet, and Schiller (2023), “Social Media as a Bank Run Catalyst,” mimeo.

Cookson and Schiller (2023), “Tweeter played a role in the collapse of Silicon Valley Bank—new research,” The Conversation.

Federal Deposit Insurance Corporation (2023), “FDIC's Supervision of First Republic Bank.”

Federal Deposit Insurance Corporation (2023), “Options for Deposit Insurance Reform.”

Federal Reserve History, (2023) "Continental Illinois: A Bank That Was Too Big to Fail." May 15, 2023.

Group of Thirty (2024), “Bank Failures and Contagion: Lender of Last Resort, Liquidity, and Contagion.”

Hsu, Michael (2024), “Building Better Brakes for a Faster Financial World.”

Iyer, R. and M. Puri (2008), “Understanding Bank Runs: The Importance of Depositor-Bank Relationships and Networks,” FDCI Center for Financial Research Working Paper No. 2008-11.

Rose, J. (2015), “Old-Fashioned Deposit Runs,” Federal Reserve Board, Finance and Economics Discussion Series 2015-111.

Rose, J. (2023), “Understanding the Speed and Size of Bank Runs in Historical Comparison,” Economic Synopses, Federal Reserve Bank of St. Louis.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager