Europe navigating a new world: what to watch in 2026

Trade wars, real wars, and peace deals. The year 2025 has been dynamic and volatile. Amid this uncertainty and rapid change, Europe’s financial system has been standing out for its resilience and adaptability. Despite modest economic growth, European markets have been upbeat this year. The region’s robust performance has been underpinned by the critical role of strong institutions, prudent policies, and diversified investment. With a successful 2025 in the books, here are some key risks and opportunities to watch for in 2026.

Euro area outlook: stability in a shifting landscape

Despite a challenging international environment marked by geopolitical tensions, the euro area has managed to maintain positive momentum. Gross domestic product (GDP) growth is forecast at 1.3% in 2025, 1.1% in 2026, and 1.5% in 2027. While these figures do not impress, they reflect a region that has steered clear of recession in a challenging environment.

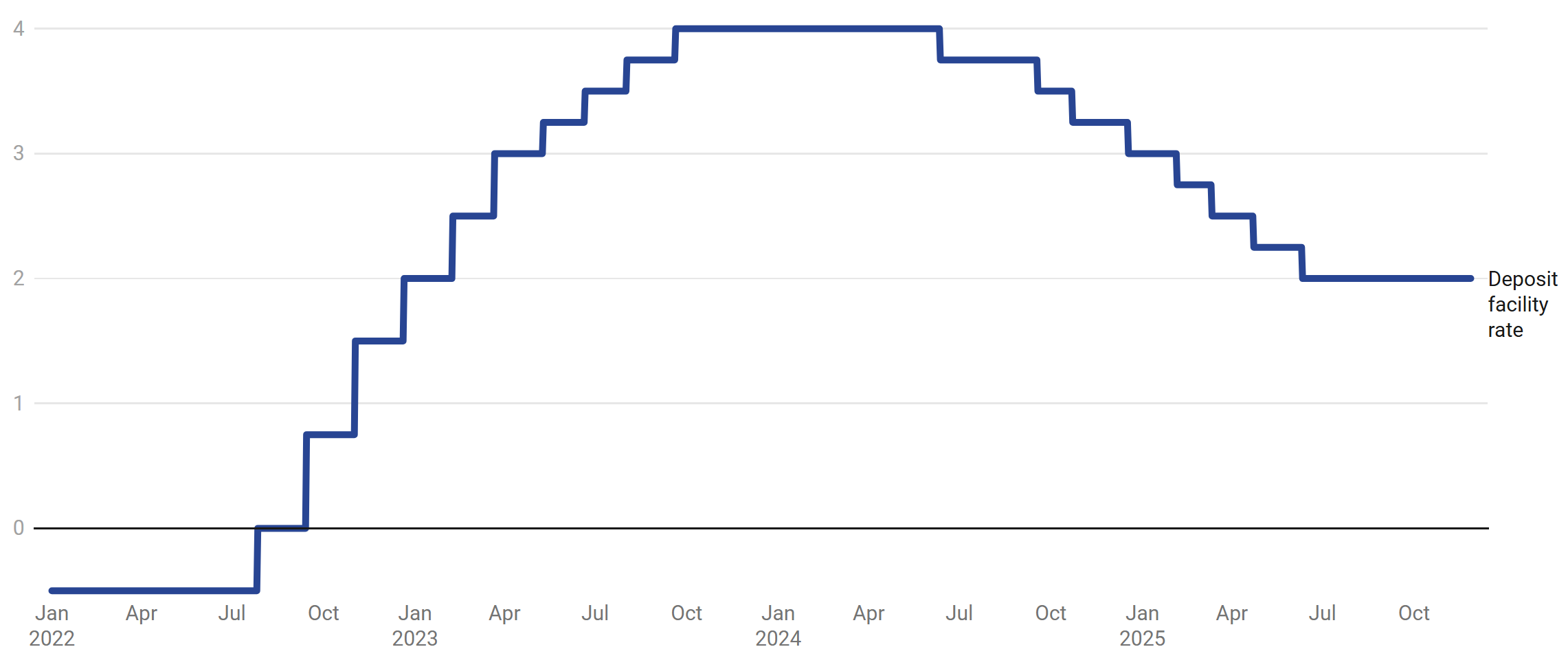

Inflation, which was a major concern in recent years, is now largely under control. The euro area’s headline inflation rate dipped and is moving closer to the European Central Bank’s (ECB) 2% medium-term target. This progress is the result of decisive ECB action: after the fastest rate-tightening cycle in history, the ECB has cut rates back to 2% (see Figure 1), signalling its confidence that price stability is ensured.

Figure 1

ECB deposit facility rate

(in %)

Source: ECB

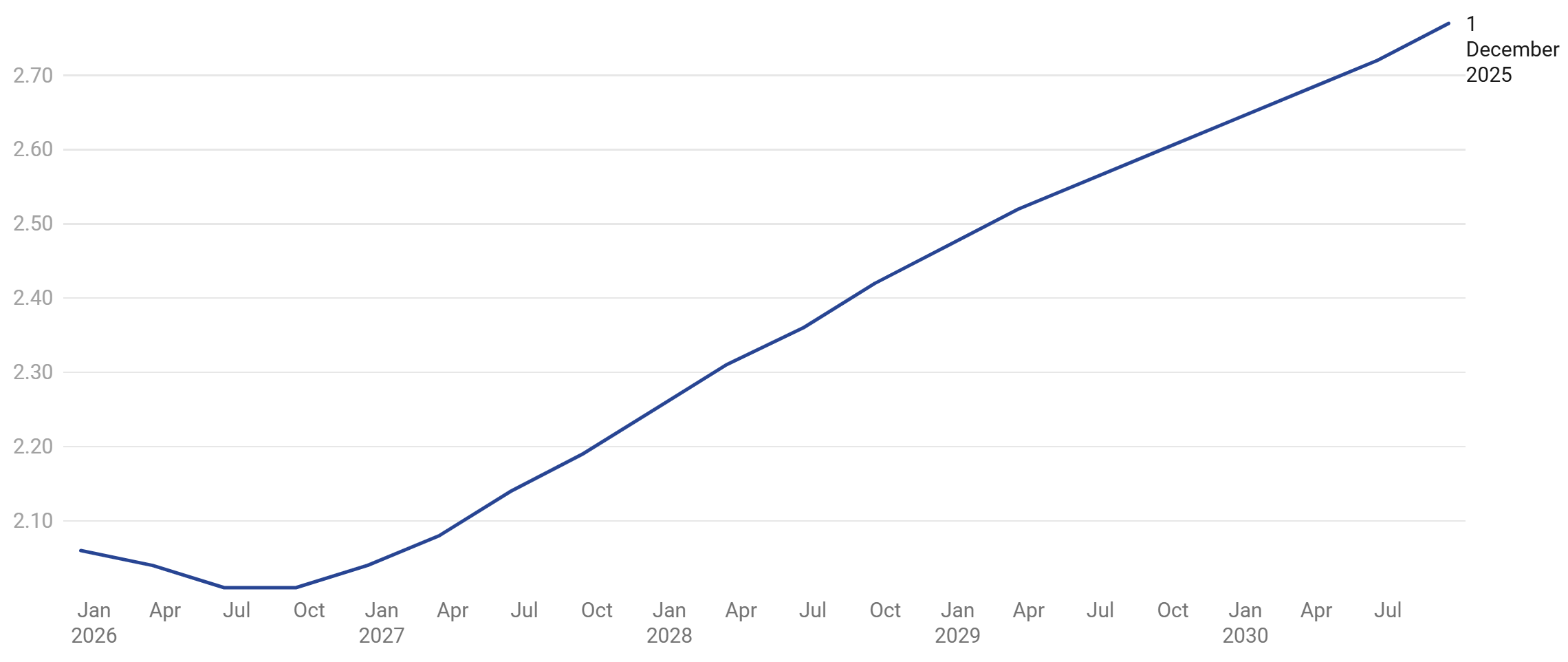

The market is pricing very little action by the ECB well into 2026 (see Figure 2). Compared to other parts of the world, Europe was quick and decisive to manage inflation down and bring rates to healthy levels – promising signs for 2026.

Figure 2

Euribor 3-month futures

(in %)

Source: Bloomberg

European financial markets performing well: strengths and opportunities

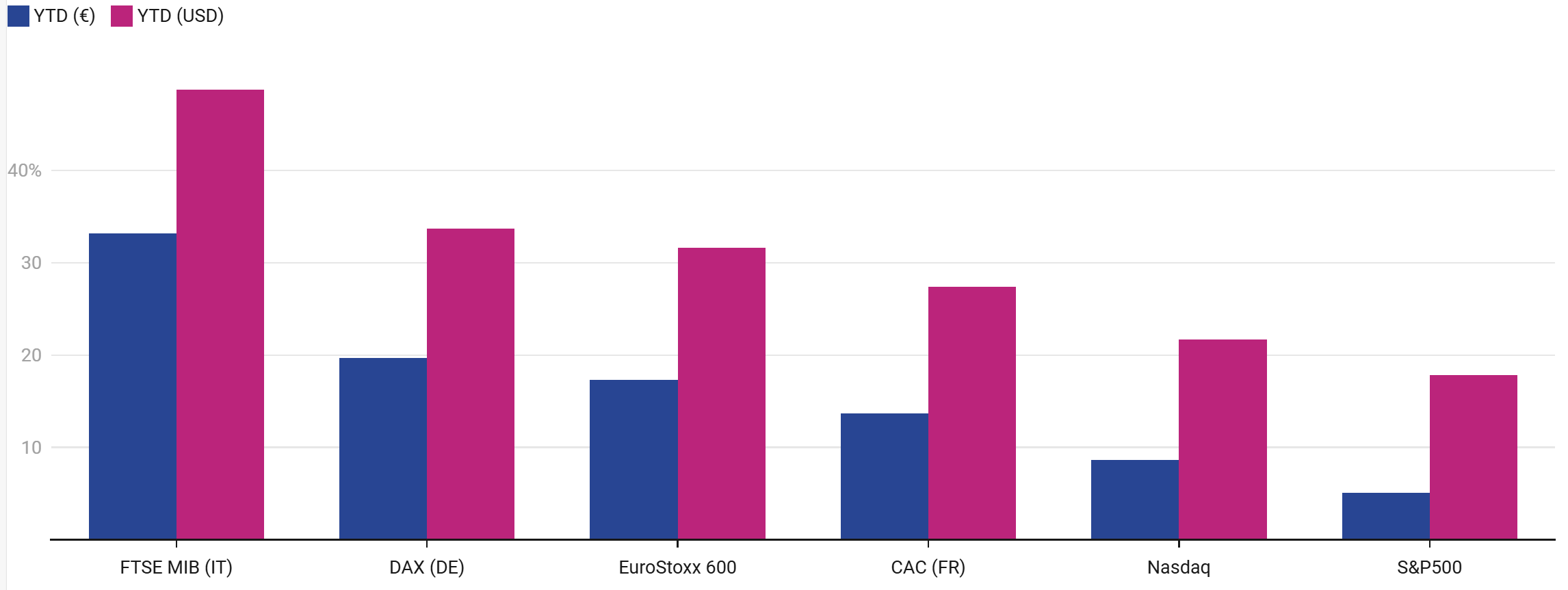

European financial markets have responded positively to these developments. Equities have performed well, with the EuroStoxx 600 index up 17.3% year-to-date and notable gains in sectors such as utilities, oil and gas, and food and beverage. Major European stock markets so far beat United States (US) stock markets in 2025, with Italy’s FTSE, France’s CAC, Germany’s DAX, and the region-wide EuroStoxx 600 all outperforming the S&P 500 and Nasdaq (see Figure 3).

Figure 3

European and US equity markets

(in %)

Note: 1 December 2025 cut off date

Source: Bloomberg

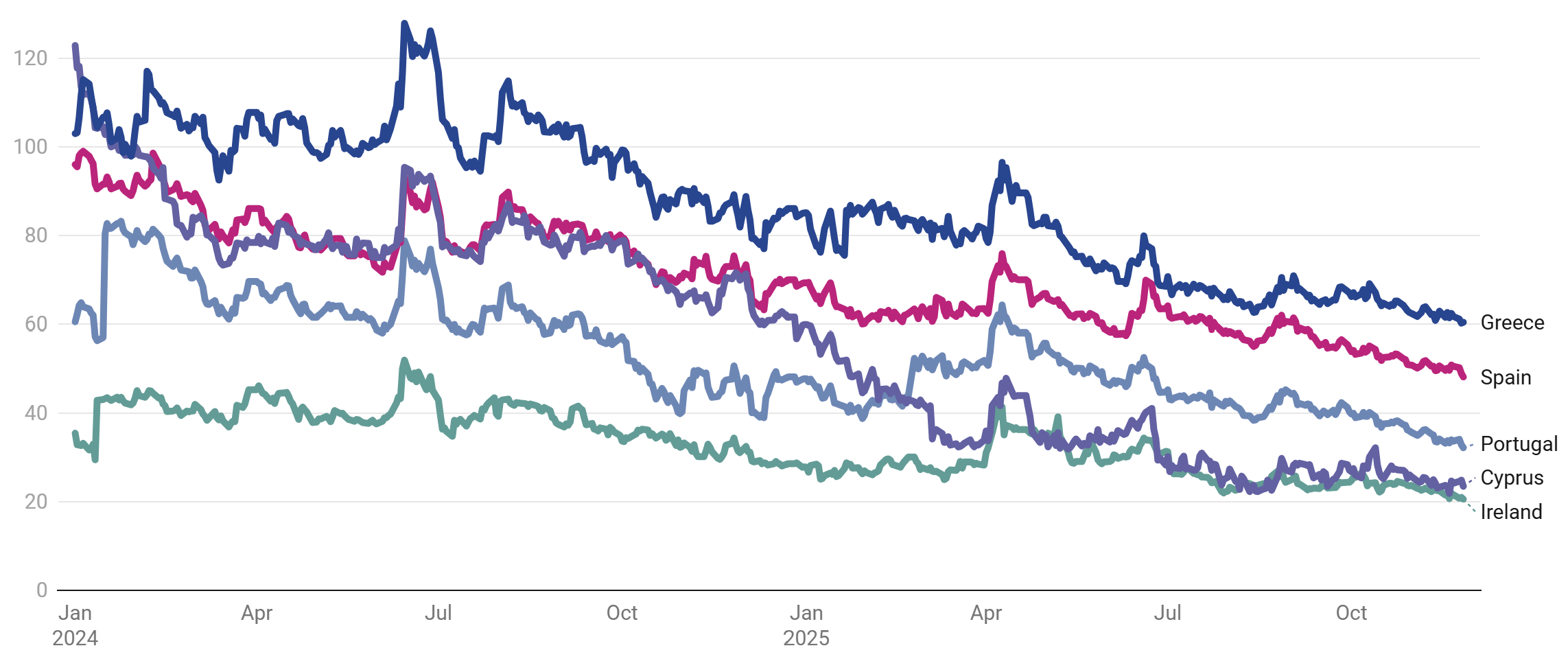

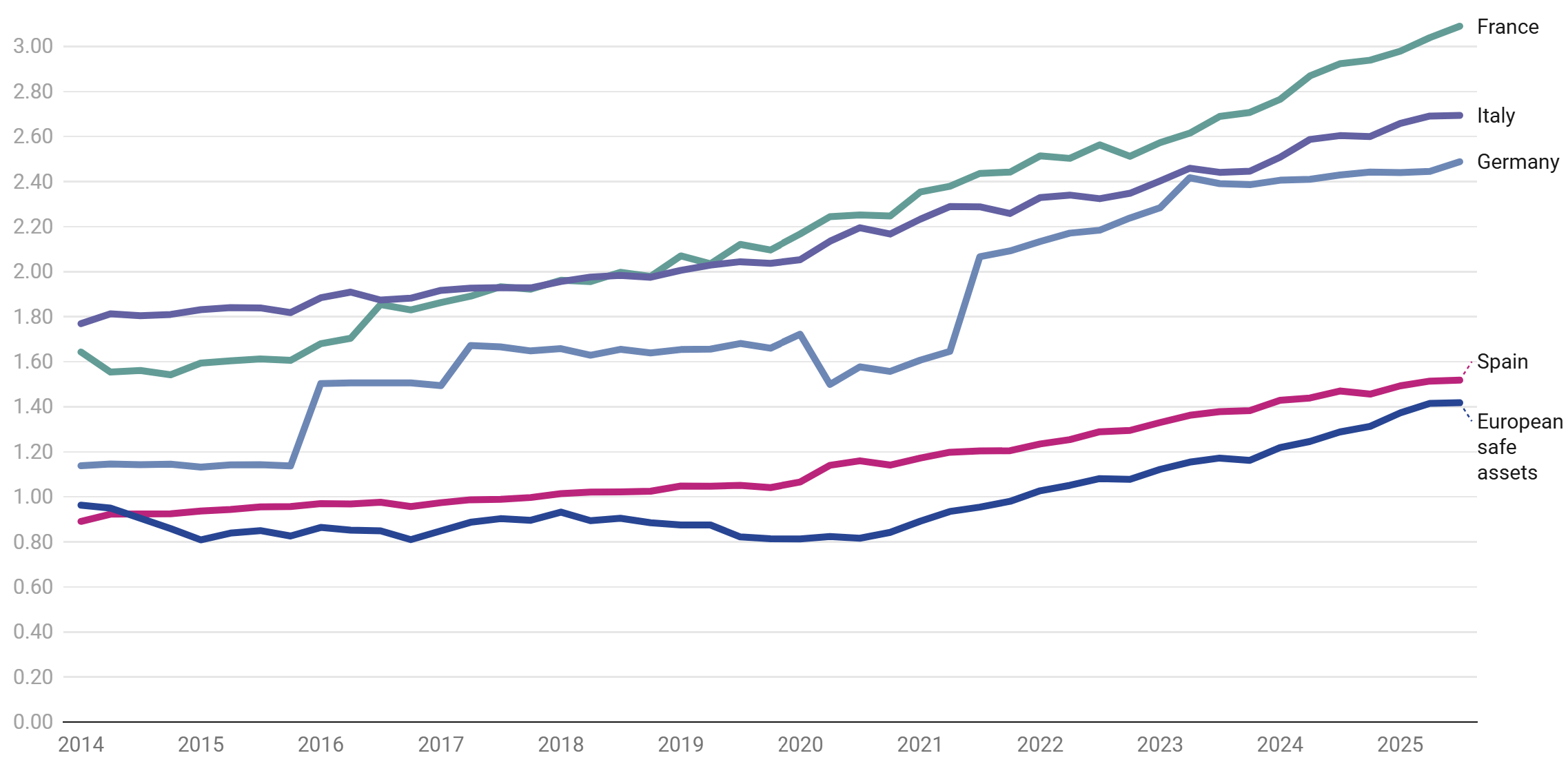

Sovereign bond spreads have tightened, particularly for countries benefitting from European Financial Stability Facility (EFSF) and European Stability Mechanism (ESM) support, with low rates and long maturities – Ireland, Spain, Portugal, Greece, and Cyprus (see Figure 4).

Figure 4

10-year yield spreads vs Germany

(in basis points)

Source: Bloomberg

This good performance reflects improved fiscal discipline and growing market confidence. These countries have seen rating upgrades. Furthermore, Portugal (1st), Ireland (2nd), Spain (4th) and Greece (6th) have again ranked in the Economist’s top 10 of best performing global economies this year.[1] It shows the countries’ success, which will continue in 2026.

Popularity of the euro growing: good signs for 2026

A key trend is the increasing demand from foreign investors for euro area bonds. Since April 2025, net buying of euro area government bonds by international investors has been strong, with higher shares of foreign holdings in German, French, Italian, and Spanish government securities. This shift is partly driven by global geopolitical developments, including tariff announcements and a search for safe, stable returns outside the US Treasury market. I expect this interest to continue, as indicated by the feedback I receive during roadshows.

In addition, issuance in euro by non-European countries is growing in popularity, with cumulative issuance reaching more than €1 trillion in 2025. Countries such as China, Chile, Indonesia, Saudi Arabia, among others, are choosing the euro as a currency for their government bonds.[2] This trend is set to continue in 2026. Diversification is the name of the game. These issuers want to open new horizons and tap new investors. This message came through in more than 100 investor meetings ESM held around the globe.

Geographical expansion is a further testament to the increasing popularity of the euro. On 1 January 2026, Bulgaria will join the single currency as the 21st member of the euro area. The euro is now more popular than it has ever been, with 83% of euro area citizens supporting it.[3]

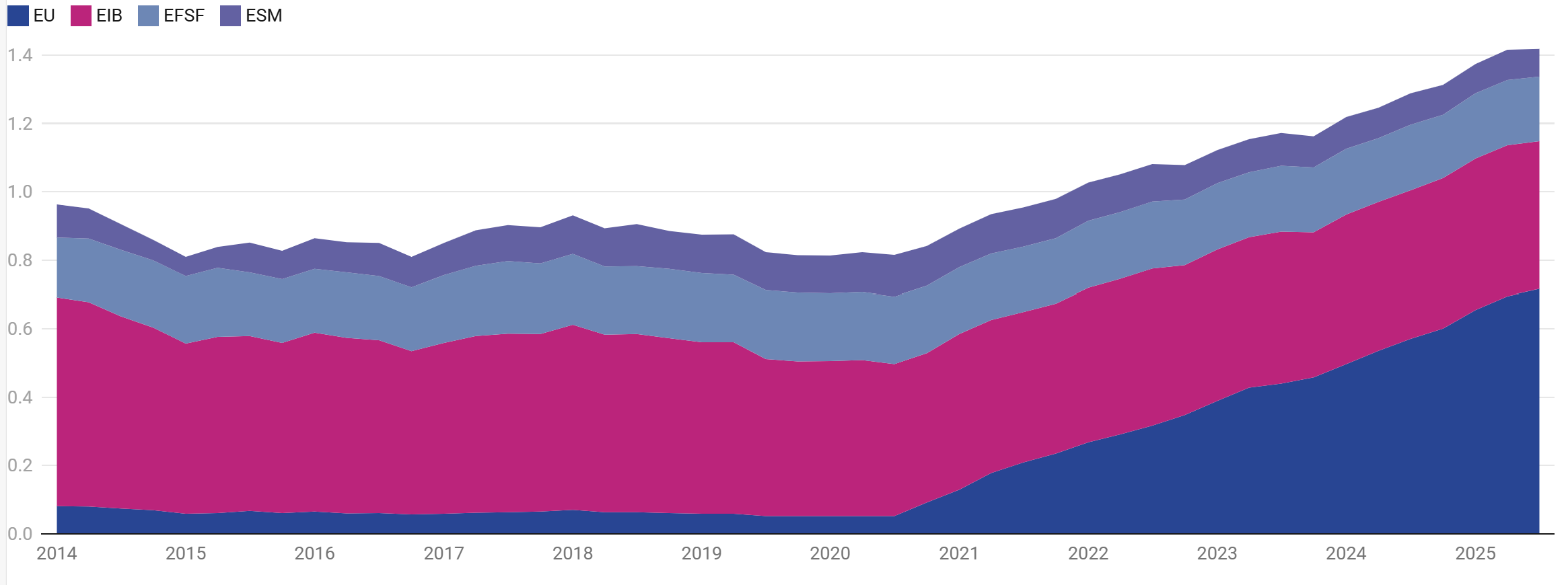

Figure 5

Outstanding European safe assets

(in € trillion)

Source: Bloomberg

European safe assets, which are issued by the European Union (EU), the European Investment Bank (EIB), and the ESM/EFSF, now total about €1.4 trillion (see Figure 5), making them the fifth largest market segment in the euro area (see Figure 6), just after Spain.

Figure 6

Debt outstanding

(in € trillion)

Source: Bloomberg

The ESM and EFSF play a central role in this ecosystem, offering highly rated and diverse investment products, and maintaining a large, global investor base. In 2026, we can expect European safe assets to grow further – especially driven by the EU Security Action for Europe (SAFE) instrument, which promotes investment and common borrowing for defence.

In terms of spreads, the assets are pricing increasingly closer to Germany (see Figure 7). These safe assets – all trading with EU ISIN codes – are the European version of the US Treasury bonds. Strong, safe, and diversified in risk. And over time: larger and deeper.

Figure 7

10-year European supranational yield spreads vs Germany

(in basis points)

Source: Bloomberg

ESM/EFSF: pillars of stability and innovation – critical for Europe in the future

The ESM is more than just a crisis resolution mechanism, it is a pillar of the euro area’s financial architecture. The accession of Bulgaria will expand ESM membership to 21 countries and increase the ESM’s shareholder base. In a speech at OMFIF in London, Bulgaria’s central bank governor, Dimitar Radev, cited ESM membership as one of the top five reasons to join the euro area.[4] With an ongoing lending toolkit review and available lending capacity of close to €430 billion, the ESM is a key pillar of financial stability in Europe.

Innovation is also at the core of the ESM/EFSF’s financing. The ESM/EFSF offer a range of flagship and strategic bond products, including highly liquid euro benchmark bonds and US dollar-denominated bonds, all designed to meet the evolving needs of global investors. In 2025, we became the first international organisation and European institution to centrally clear our derivative transactions through Eurex Clearing, following G20 and Eurogroup recommendations. This is a huge and innovative achievement. Responsible investment also remains close to our heart, with €7.4 billion allocated to environmental, social, and governance (ESG) investments, supporting green, social, and sustainable projects across Europe. This is up €2.2 billion from the year before.

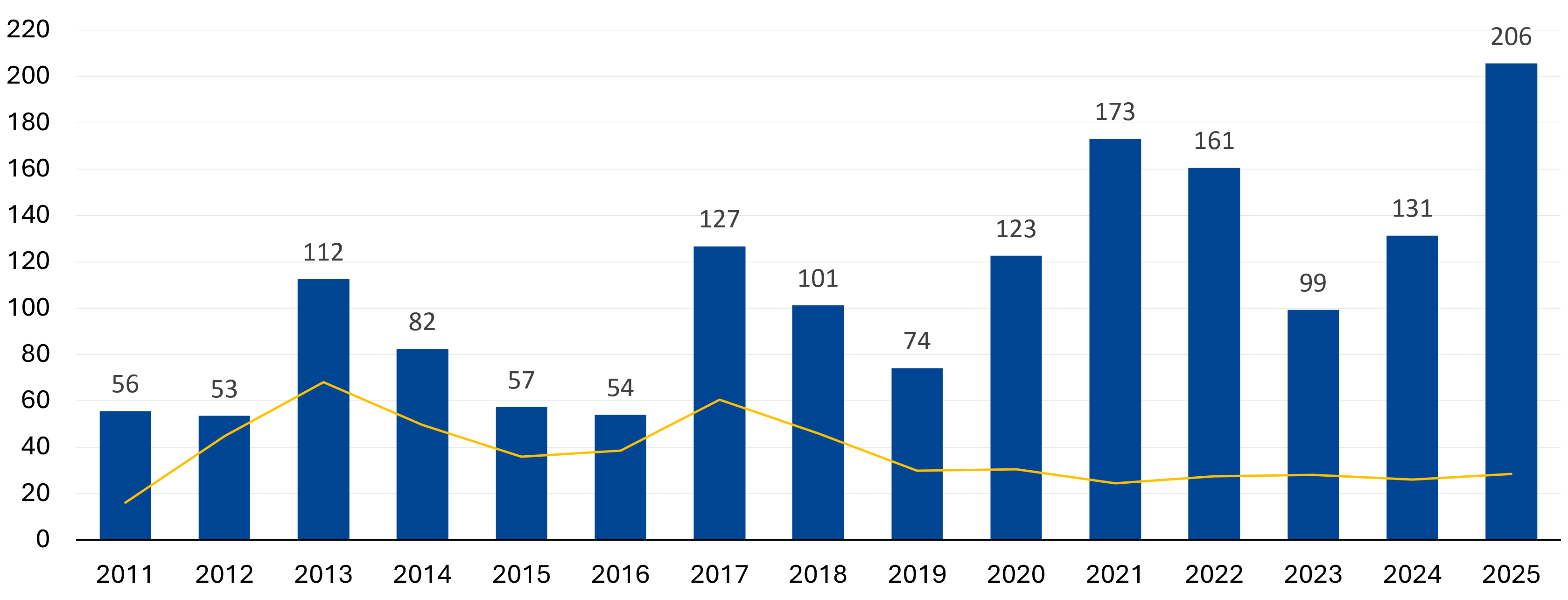

In 2025, we saw the largest order books in history for the EFSF and ESM (see Figure 8), adding almost 40 new investors, like from Latin America. This shows the strong interest for European safe assets.

Figure 8

Orderbook for ESM and EFSF bond issuances

(in € billion)

Source: ESM

Key risks and opportunities for 2026

As we look ahead to 2026, several themes will shape the economic and financial landscape for Europe and the world. Compared to previous years, the view ahead is foggier than usual. Here are the shock risks and opportunities to be on the lookout for:

- Geopolitical tensions and market volatility

Ongoing conflicts, trade disputes, and shifting alliances will continue to influence global markets. Investors should monitor developments in Eastern Europe and the Middle East, as well as the evolving relationship between the three financial power blocs US, China, and the EU. Reducing geopolitical tensions would boost business confidence. An upside is possible here in 2026, with the US’s ambition to stop ongoing wars.

- Uncertainty around tariffs and business models

The risk of new tariffs and trade barriers remains high, creating unpredictability for multinational businesses. Companies will need to adapt their supply chains and business models to navigate this environment. There is a positive angle: that the baseline for tariffs and trade barriers is set, so the worst may well be over. It is possible that these tensions will ease in 2026.

- The artificial intelligence revolution: peak, plateau, or bubble?

Artificial intelligence (AI) has driven equity markets to new highs, particularly in the US. In 2026, the key question will be whether AI is at its peak or if further breakthroughs are on the horizon. Investors should watch for signs of overvaluation and the real-world impact of AI adoption. We have the experience of 2001 and the tech bubble. For now, while companies invest enormous sums in AI, it has not (yet) delivered the macro productivity gains that boost GDP. A sharp correction could have an impact on financial stability.

On the micro level, ESM remains enthusiastic about AI and innovation at the ESM. ESM signed an agreement with the University of Luxembourg to work on enhancing our capital markets activities. Using more innovation and AI in bond markets is in the works, as early as 2026.

- Digital finance: stablecoins and the digital euro

New developments in digital finance, including the rise of stablecoins and the potential launch of a digital euro, could reshape payment systems and cross-border transactions. Regulatory clarity and technological innovation will be critical factors to watch. China and India, with close to three billion citizens, lead the way in central bank digital currencies. The US leads the way in stablecoins, which pose opportunities and (financial stability) risks. I spent time in these three countries this year and could see the progress with my own eyes. Europe is aiming for the digital euro and has opened the door to stablecoins. This space will grow in importance, with stablecoins and digital currencies playing even more important roles in 2026.

For Europe in 2026, expect more digital issuances and pilots preparing for the ECB digital euro launch.[5]

- ESG, sustainability, and strategic finance: a comeback with a twist?

After a period of uncertainty, ESG and sustainability themes may regain prominence in 2026. Policymakers, investors, and companies will need to demonstrate real progress on climate goals and social impact to maintain credibility and attract capital. The narrative might change based on new political winds: from “climate change finance” to “extreme (weather) risk mitigation”. In Asia and the Middle East, which represent more than half the global population, these topics are high on the agenda. Less talk, more action: these regions have leapfrogged into world leadership in electric vehicles and pollution reduction.

Another trend I see is a move from “sustainable finance” to more “strategic independence finance” (including defence and security). We have seen the first defence bonds issued by Bpifrance (a French public investment bank),[6] and other countries are making preparations, such as Luxembourg with a defence bond framework.[7] The International Capital Markets Association is considering a Defence Bond label and investors – who used to shy away from defence – are changing investment guidelines to allocate resources to this sector. In my view, we should rename them “Peace Bonds” to give them a more positive connotation. The “thematic investments” all aim to foster a better and safer planet for our children.

Blueprint for a stronger future

Europe’s economic resilience, strong institutions, and commitment to responsible investment provide a solid foundation for navigating uncertainty. As we move into 2026, staying alert to emerging risks and opportunities will be essential. By working together across regions, sectors, and institutions, Europe can help deliver a more stable, prosperous, and sustainable world for the next generation.

My bottom line: expect “more Europe” in 2026. Which is good news for Europeans and the rest of the world!

Acknowledgements

The author would like to thank Yasser Abdoulaye, Raquel Calero, Denver Chaplin, Cédric Crelo, Peter Lindmark, Marius Marsanu, Olivier Pujal, Stephane Vincent for their valuable suggestions and contributions to this column.

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager