Euronomics: Déjà vu? How the euro area confronts another energy shock

As geopolitical tensions in the Middle East trigger severe disruptions in global oil and gas markets, concerns are rising once again about the euro area’s vulnerability to energy price shocks. Europe remains highly dependent on imported energy, leaving its economy and financial stability exposed to global price swings. Compared to the shock triggered by Russia’s invasion of Ukraine, the euro area economy enters this episode in a better position, although not immune. The policy challenge now is twofold: stabilising the economy amid renewed price turbulence and advancing the structural reforms needed to strengthen Europe’s long-term energy resilience.

Global energy price shock from Middle East conflict: déjà vu for Europe?

The sharp increase in global energy prices triggered by the US-Iran conflict and the ensuing closure of the Strait of Hormuz has sounded the alarm bells of a renewed global energy crisis. As in 2022, a geopolitical conflict is causing significant disruptions to the global economy. Since the start of the military engagement, oil prices have risen above 50%, a pace comparable to that at the outset of Russia’s invasion of Ukraine, and natural gas prices have soared by over 65% amid concerns about the lowest reserves since 2022.[1]

For the euro area economies this represents a renewed terms-of-trade shock, although energy prices – particularly for gas – still have not reached levels attained in 2022. The past experience is still fresh in our memories. With almost 60% of the euro area’s energy needs imported from abroad[2] (and around 90% for gas and oil), rising energy prices will not only lead to higher inflation but also transfer income from euro area citizens abroad, to the energy exporting countries.

Today’s situation is similar to 2022, yet distinct in several ways: the structure of energy use moderates the impact of the current energy shock. At the same time, the consequences of a more sustained rise in energy prices will further undermine the competitiveness of energy-intensive sectors and the overall economy. The policy reaction – particularly fiscal measures – has to adjust to the new constraints posed by higher interest rates and defence spending. Fiscal measures need to reflect the lessons of the inflationary surge of 2022.

Revisiting the 2022 episode: lessons learned and increased resilience

The 2022 energy shock hit the euro area hard. The crisis exposed a core external vulnerability: Europe’s overreliance on Russia as a single supplier of energy, and the risks that arise when that dependency is weaponised. In the first quarter of 2022, oil prices rose by over 35%, and fears of gas shortages drove wholesale gas prices to all-time highs. Higher energy prices, combined with pent-up demand from the pandemic and fiscal support at the time, drove inflation into double digits, and the European Central Bank (ECB) responded with the fastest tightening cycle in the history of the euro, 450 basis points of hikes between July 2022 and September 2023. It also interrupted the post-pandemic rebound, pushing the economy to the brink of stagflation.

The shock prompted Europe to adapt quickly, and many of those adjustments have strengthened resilience for the current situation. First, Europe’s dependence on Russian energy has fallen dramatically.[3] Gas and oil suppliers today are well diversified. In the current situation, direct exposure is limited, with around 12% of Europe’s oil imports and 6% of liquefied natural gas (LNG) imports originating from Middle Eastern suppliers. At the same time, this diversification of energy towards global gas markets implies a larger exposure to global price swings than long-term fixed-price contracts. Price shocks and geopolitical shocks, like the current conflict, are less likely to disrupt the entire system for an extended period barring the destruction of crucial infrastructure, such as refineries and gas plants, which take long to be rebuilt.

Households and firms proved far more agile than many anticipated. They reduced their energy demand, switched energy sources, and increased efficiency measures. Energy intensity (energy consumed per unit of real GDP) is 13% lower than in 2021, and about 40% lower than in the United States (US). As demand becomes more elastic, future price spikes should translate into smaller macroeconomic shocks.

The policy response improved energy security and affordability. Since 2022, EU LNG regasification capacity has risen by 32%,[4] and the energy transition contributed to enhancing energy security. Wind and solar capacity has grown by 58% since 2021,[5] and in 2024, renewables generated more electricity than gas for the first time. This shift is helping reduce structural vulnerabilities in the sector and materially affects energy pricing. When renewables are the marginal resource of electricity generation, the result is lower electricity prices.

In addition, several European market-level safeguards are now structurally embedded to dampen extreme price volatility. The EU has moved to a reformed market design in which joint gas purchasing, coordinated storage commitments (pre-winter target of filling gas storage to 90% of capacity), and price-correction mechanisms are permanent features. Enhanced cross-border coordination and codified solidarity arrangements also limit the risk of market fragmentation during supply disruptions. These measures and further progress towards decarbonisation remain essential as Europe’s fossil fuel dependence remains high despite the above-mentioned improvements.

Managing the current shock: economic vulnerabilities and potential implications

Despite this progress, Europe is still vulnerable to global energy disruptions and price fluctuations. Although renewables now account for a larger share of electricity production, gas remains a relevant price setter in these markets, with differences across countries.[6] When LNG prices increase, electricity prices generally follow – and so does inflation.

For energy-intensive industries – chemicals, basic metals, among others – the pain from 2022 has not fully healed. These firms remain highly exposed to energy price spikes, and many are still adjusting business models and production processes. Industrial electricity prices in Europe are between two and three times higher than in the US or China. The medium-term competitiveness challenge is far from being resolved and has actually increased in light of US protectionism and China’s excess supply of manufactured goods. A new, more persistent shock to energy prices might trigger employment adjustments[7] as well. Beyond the pure energy terms‑of‑trade shock, the global nature of the episode implies additional effects through weaker global growth and tighter financial conditions.

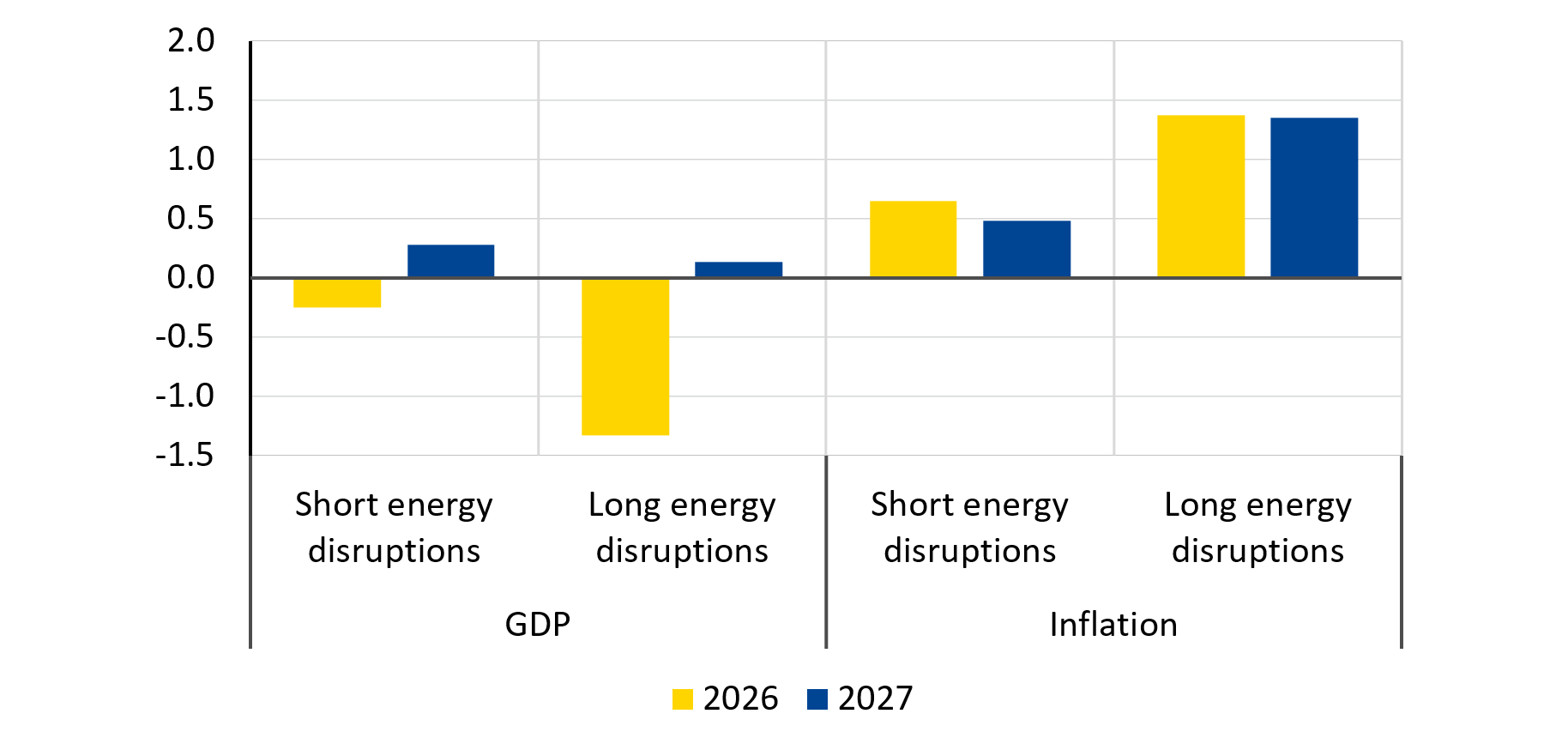

The overall economic consequences of the current global energy price shock will depend not only on the size of the price shock but also on how long the disruption lasts. Using a model-based approach that examines how energy prices directly affect production costs and terms of trade, an oil and gas price rise of 100% and 200% respectively from pre-US-Iran conflict levels could reduce euro area GDP by 0.3% in 2026 in case of a short energy disruption and by 1.2% by the end of 2027 in case of a longer one. Average annual inflation would increase by 0.5 and 1.4 percentage points respectively, depending on whether prices gradually return to previous levels in early 2027 or remain elevated for an extended period (Figure 1). Reasons for higher-for-longer oil and gas scenarios include a protracted conflict as well as the implications of infrastructure damage that prolongs the supply disruption. These simulations focus on demand-side effects and allow for an economic rebound when uncertainty vanishes and prices start falling. A more structural loss of competitiveness would undermine long-term growth.

Figure 1

Impact of oil and gas price shock on euro area GDP and inflation

(annual growth deviation from baseline in percentage points)

Source: ESM calculations. Note: Assumptions about energy prices: (a) “Short energy disruptions”: oil and gas prices peak in March, to fall afterwards, reaching pre-conflict levels in early 2027. (b) “Long energy disruptions”: oil price remains in Q2 2026 at 120 USD/barrel and gas prices at €80/MWh (both quarterly averages), to fall gradually in the second half of the year until end-2027. Oil price and gas price stay in 2026 and 2027 on average around 60% and 150% above pre-conflict levels (December 2025), respectively. The longer conflict case also assumes higher uncertainty that resolves in 2027. The impact on GDP growth and inflation is relative to the pre-conflict baseline macro scenario.

Policy response: constraints and strategic choices

Policymakers face this global shock with some constraints but also with the benefit of experience and established emergency frameworks.

The experience of 2022 and of the years that followed offers an important cautionary lesson. While higher inflation temporarily reduced debt ratios in the wake of the energy shock, these gains cannot be replicated without costs. Inflation driven by adverse supply shocks undermines competitiveness and purchasing power, and its fiscal effects are asymmetric over time: interest expenditure rises only with a delay, but eventually weighs heavily on public finances.

Indeed, the higher interest rates of the post-2022 period are starting to hit public finances now. This factor and the long-term defence spending needs have created a less favourable environment. Sustainable debt reduction must therefore rest on growth‑enhancing policies and higher primary surpluses, not on inflation surprises.

In the short term, policymakers should be prepared to respond swiftly and stabilise the economy. For a cost-push shock, the interaction between monetary and fiscal policies is particularly relevant and complex, as growth and inflation tend to pull in opposing directions. With policy interest rates close to neutral levels, inflation near the ECB’s target, and growth in the vicinity of potential, monetary policy has room to react if any signs of de-anchoring of medium-term inflation expectations arise.

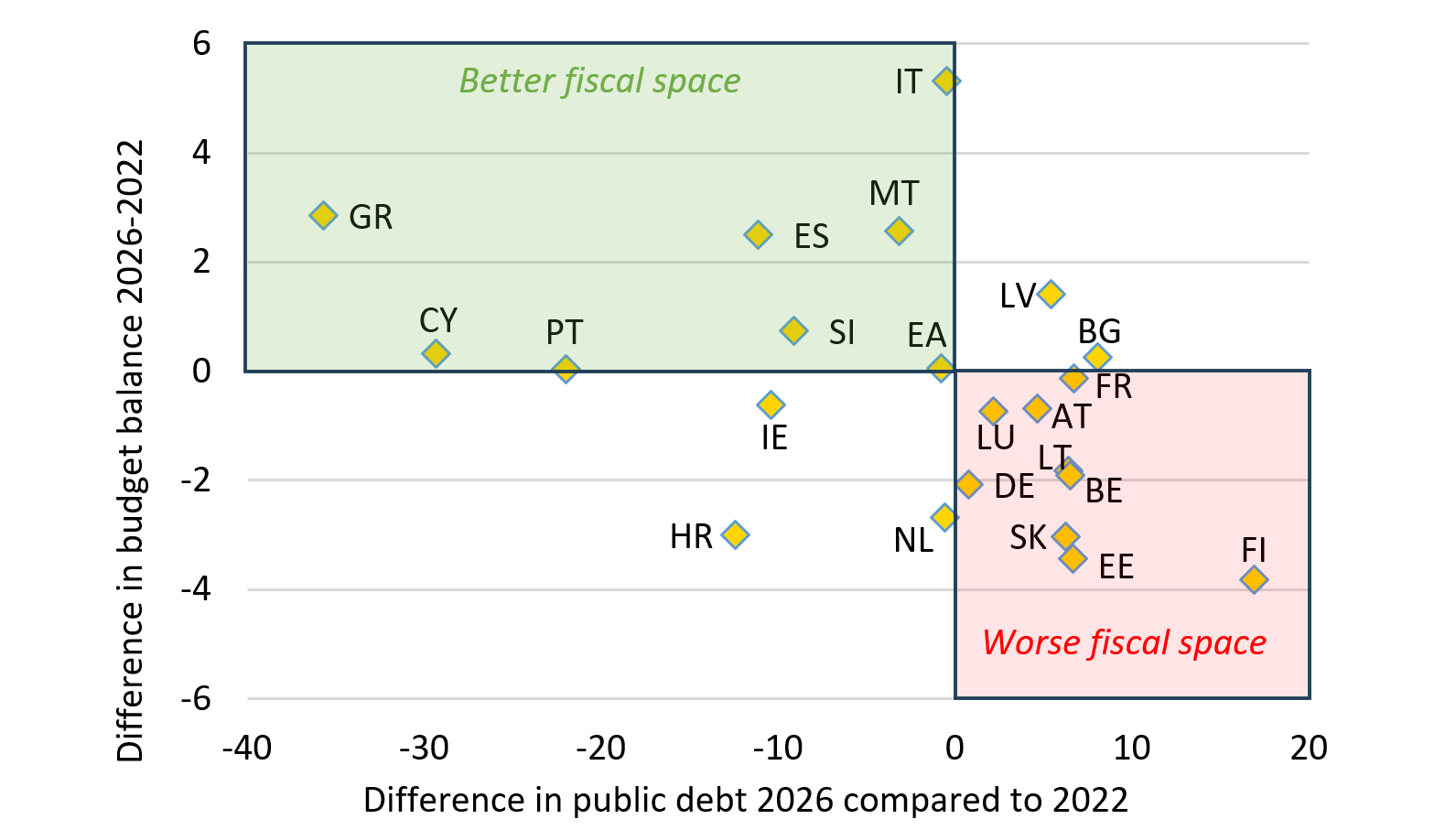

The overall euro area budget balance is almost identical to 2022, but there are notable differences across countries (Figure 2). Since 2022, some euro area governments have experienced robust growth and consolidated their finances, making fiscal space to cushion the impact of another shock. However, others have run large deficits – in part related to higher defence commitments – and therefore have less fiscal capacity to absorb another crisis.

Figure 2

Difference in government budget balances and public debt 2026 compared to 2022

(% GDP)

Source: ESM calculations based on AMECO, Autumn 2025. Note: 2026 is a forecast while 2022 is an outcome.

For all these reasons, the nature of the energy price shock calls for a timely but also temporary and targeted policy response. As we have argued in previous terms-of-trade shocks, the cost-of-living crisis affects less affluent households more, as they consume a higher share of their income. Targeted transfers or subsidies can help mitigate costs and effectively support consumption and growth. At the same time, households and firms can exploit margins to save energy as a mitigating strategy, as was done successfully during the energy price hike following the attack on Ukraine.

In the medium term, the current shock clearly underscores the urgent need to strengthen Europe’s strategic energy autonomy. The objective of permanent tax measures and structural reforms at the national and European level should be to accelerate the green transition and expand and modernise energy infrastructure and cross-border interconnections, in line with the proposals in the Draghi and Letta reports. These steps are essential to reduce dependencies and build a resilient, stable, and sustainable energy system capable of withstanding global shocks and addressing one of the structural factors weighing on Europe’s competitiveness.

Acknowledgments

The author would like to thank Pilar Castrillo, Michael Kühl, Vasiliki Michou, Lorenzo Ricci for their valuable contributions to my column.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager