Assessing macro-financial risks: a look under the hood of the ESM’s country-level “Growth-at-Risk” model

Abstract

Financial conditions contain information about the economic outlook and downside risks. This brief presents the ESM’s “Growth-at-Risk” model, which translates changes in financial conditions into risks to expected GDP growth. These risks to growth vary significantly across euro area member states, reflecting both different dynamics in key asset prices – bonds, stocks, and real estate – and credit growth, as well as different levels of market stress. Before the war in the Middle East, financial conditions (especially equity valuations) were favourable and volatility low, signalling contained near-term risks to growth. Market stress has increased since the end of February 2026 and a re-escalation of the conflict leading to long-lasting war could further adversely affect global investor sentiment and lead to a persistent deterioration of macro-financial conditions. Both could generate additional downside risk to economic growth. We conclude by outlining the scope for extensions and refinements of the tool.

The author would like to thank Matthias Gnewuch and Mathias Skrutkowski for valuable discussions and input, as well as Rolf Strauch, Pilar Castrillo, Andrzej Sowiński, and Konstantinos Theodoridis for helpful comments. Karol Siskind and Raquel Calero provided excellent editorial support.

A brief introduction to Growth-at-Risk analysis[1]

Financial conditions and market sentiment can be informative about future economic growth and the risk of adverse growth surprises. Economic growth depends, among other factors, on financial conditions that allow households and firms to borrow, invest, and spend. Economic activity tends to pick up when credit is readily available, financing costs are low, and the market environment is stable. However, favourable financial conditions can also encourage excessive borrowing and inflate asset prices. Over time, these imbalances can make the economy prone to sharp downturns when conditions change, as exemplified by the Global Financial Crisis of 2007–2009.

The Growth-at-Risk approach models the link between financial conditions and the range of possible future growth outcomes, focusing on the risk of large negative growth surprises. Popularised by the International Monetary Fund (IMF, 2017) and now widely used by other policy institutions (e.g. European Systemic Risk Board (ESRB), 2021), Growth-at-Risk refers to the lower end of the possible GDP growth range as signalled by current macro-financial conditions (typically the 5% or 10% quantile of the predicted distribution). It thus quantifies adverse growth realisations that could materialise in a worst-case scenario. By extending the analysis to other parts of the range, the approach can also be informative about the broader set of possible growth outcomes. This tool helps economic policy institutions to assess the risks surrounding growth forecasts as well as their balance, that is the relative prominence of downside compared to upside risks.

The current ESM model is a traditional application of “at-Risk” approaches, focusing on risks to GDP growth signalled by financial conditions and market stress. We also discuss the implications of this in case of a “macro-financial disconnect”, i.e. a situation where asset prices and market stress measures potentially do not fully reflect certain prevailing risks, for example stemming from high levels of policy uncertainty. Moreover, while Growth-at-Risk remains the main application, the conceptual framework underlying the analysis has been used to also study risks to other economic variables, for example, public debt-to-GDP (Furceri et al., 2025). In either case, “at-Risk” approaches in their standard form are purely statistical models, mainly developed for monitoring and forecasting purposes. They do not reveal the channels through which financial or other factors affect risks to economic outcomes.

A model for macro-financial risk analysis across euro area member states

Extending its toolbox for macro-financial risk analysis, the ESM has developed a country-level framework to quantify risks to economic growth. Having applied a Growth-at-Risk model at the aggregate euro area level in the past (see this ESM Blog), the ESM has extended this analysis to the country level. The model enables consistent analysis and comparability of financial conditions and associated risks across euro area countries, being aware of the caveats when estimating cross-country regressions. The model’s output, alongside the findings of many other tools, feeds into regular internal risk assessments and provides quantitative support for discussions.

The model is a multi-country extension of the standard Growth-at-Risk framework (Adrian et al., 2019), providing results for all 21 euro area countries. Our use of this tool focuses on analysing risks over a relatively short horizon of four quarters ahead. We estimate a cross-country quantile regression model (see Canay, 2011) with quarterly data for a subset of 11 countries: the four largest economies (Germany, France, Italy, and Spain) as well as Austria, Belgium, Greece, Finland, Ireland, the Netherlands, and Portugal. The estimated coefficients are then used to compute the quantiles for all euro area countries.[2] Data availability of financial indicators varies across countries, and our dataset, for some countries, starts as early as 1997. The Annex contains a table with all variables used in the analysis and their respective data sources, our empirical specification, and the estimated coefficients.

For a comprehensive assessment of the financial environment, we include two conceptually different indicators. The first measure is a simple financial conditions – or cycle – index (FCI), which is a summary measure of price changes in major asset classes as well as credit growth. The index is calculated as the average of private sector credit growth, house price growth, stock market returns, and the (short-term) interest rate, all deflated by HICP inflation and normalised (Schüler et al., 2020; Arrigoni et al., 2022).[3]

The second measure quantifies financial market stress and is the European Central Bank’s country-level indicator of financial stress (CLIFS). Unlike the FCI, which measures swings in asset prices and credit growth, the CLIFS mainly captures volatility in financial markets. It is extracted from a total of six measures, covering the equity, government bond, and foreign exchange market, while also taking the common movement across variables into account (Duprey et al., 2017). The CLIFS peaks during periods of heightened uncertainty and sudden shifts in investor sentiment, while staying low during calm periods. Together, both indicators provide a more complete view of a country’s financial conditions, which is also in line with the approach proposed by the ESRB (2021).

As a general remark, booming asset prices and resilient credit growth tend to signal reduced downside risk in the short term but can lead to vulnerabilities and increased risks in the longer term.[4] This is especially true if rapid growth in asset valuations becomes detached from economic fundamentals and is largely fuelled by investors’ expectations of future price increases. This phenomenon seems to have at least partly contributed to the recent rally of AI-related stocks (see also IMF, 2026). Similarly, credit growth can be concerning if it is largely driven by borrowers with low creditworthiness. In these cases, economic shocks or shifts in investor sentiment can trigger sudden price corrections, reigniting market volatility and putting economic growth in jeopardy.

Euro area and country-level results and assessment

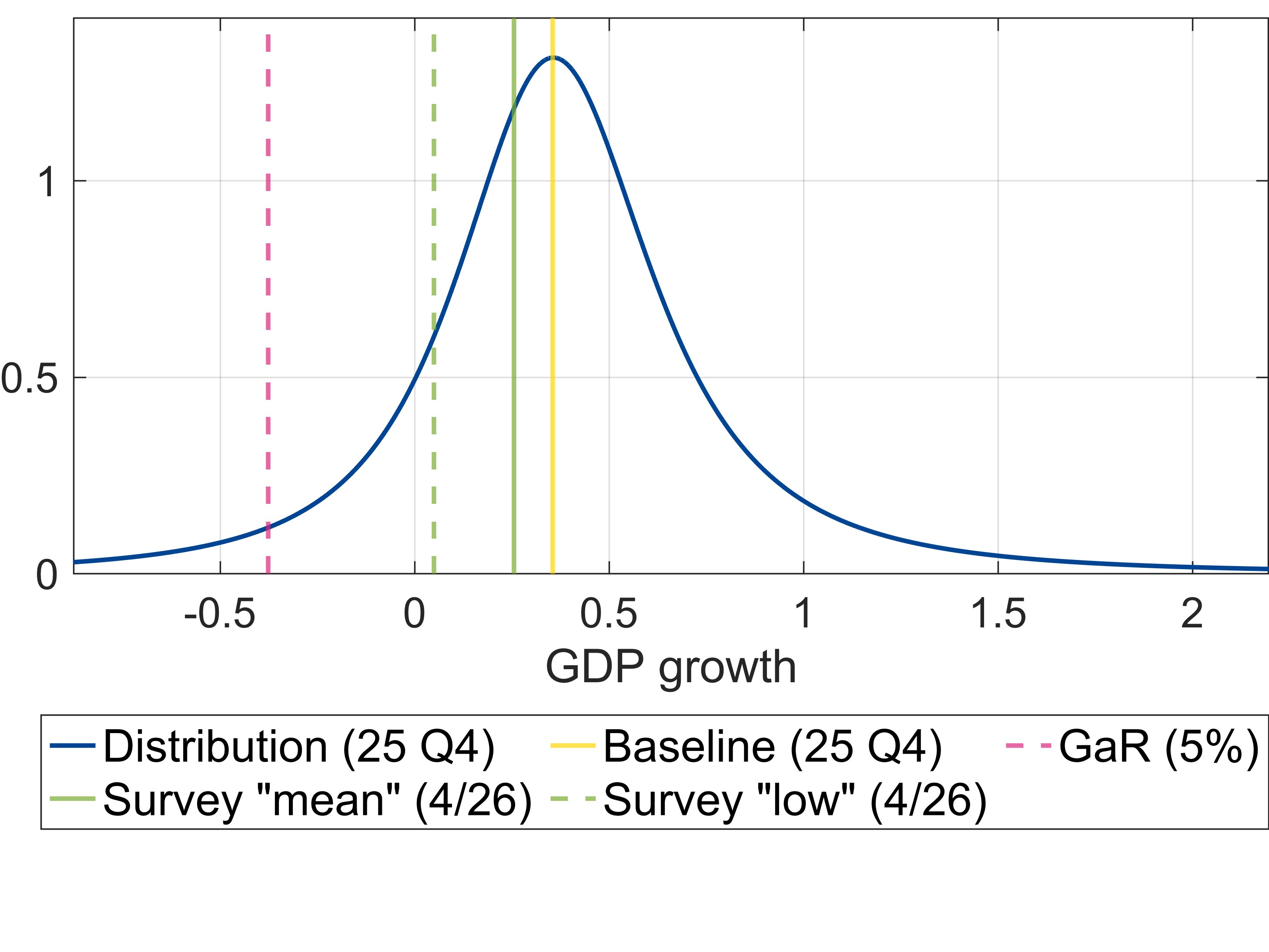

At the euro area level, financial indicators – prior to the war in the Middle East[5] – signalled limited downside risk to GDP growth compared to past episodes. This reflected the generally benign conditions in different asset classes, despite the elevated geopolitical tensions and policy uncertainty that prevailed already before the outbreak of the war. We aggregate the country-level model results using GDP weights to ensure consistency between the euro area and country-specific risk assessments (Furceri et al., 2025). The “pre-war” distribution for average quarter-on-quarter euro area GDP growth in 2026, centred around the latest forecast from the European Commission (Autumn 2025), suggests that risks were broadly balanced (Figure 1).

The negative impact of the war in the Middle East on euro area growth forecasts is apparent but does not yet constitute a low-probability extreme adverse event given the “pre-war” outlook. While the latest quantification of risks to growth does not incorporate the impact of the war on the outlook for the euro area, it can be useful to benchmark the war’s preliminary impact on growth prospects. The latest private sector forecasts (from Bloomberg’s regular survey as of 22 April) show that average growth expectations deteriorated compared to the European Commission’s Autumn 2025 forecast. The most pessimistic forecasts clearly expect lower growth but are, for now, not in the left tail of the pre-war distribution (Figure 1).[6] However, if the conflict continues for much longer and potentially escalates, this assessment can change rapidly.

Figure 1

Risks to euro area growth in 2026

(as of 2025 Q4)

Notes: Distribution (as of 2025 Q4) of four-quarter-ahead average quarter-on-quarter growth centred around the European Commission’s Autumn Forecast 2025. GaR (Growth-at-Risk) is the 5% quantile. Survey “mean” refers to the average forecast from Bloomberg’s survey while “low” indicates the average of the two most pessimistic forecasts.

Sources: ESM calculations, European Commission, and Bloomberg

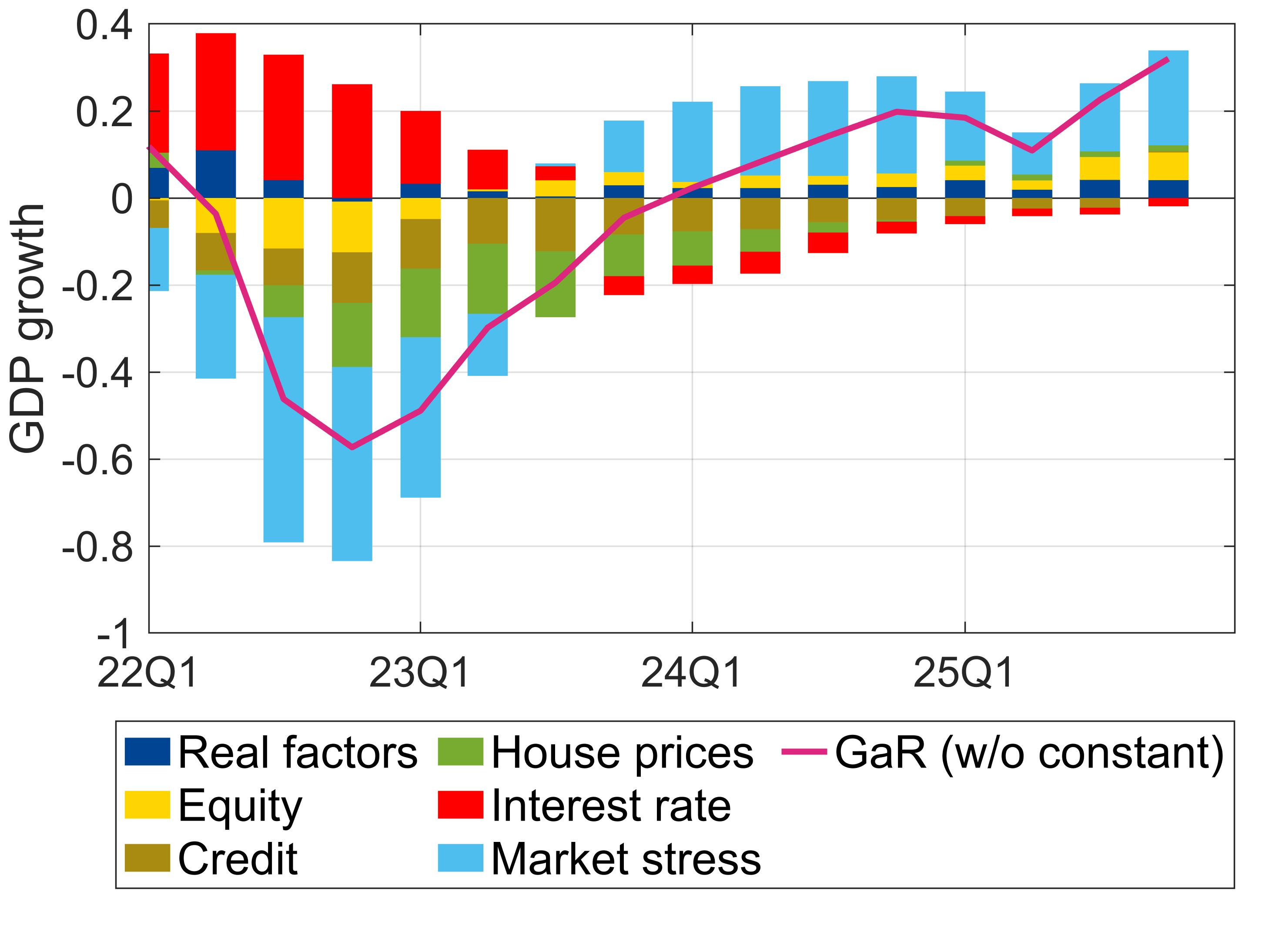

Figure 2

Decomposition of euro area downside risk

(until 2025 Q4)

Notes: A negative (positive) contribution indicates that a variable contributes to increasing (reducing) risk compared to the historical average. Real factors are captured by current real GDP growth. Based on data until 2025 Q4.

Source: ESM calculations

Broadly speaking, financial conditions improved steadily since the end of 2022, but recent war-related turmoil may end this trend. The improvement until the end of 2025 occurred thanks to a rise in asset prices and (real) credit growth as well as subdued market stress, which increased only temporarily due to tariff-related financial market turmoil in 2025 Q2 (Figure 2). The model indicates that the pre-war risk signal from financial conditions for future growth was more benign than its historical average. Following the outbreak of the war at the end of February, stock markets have declined and been very volatile, bond yields went up, and broader market stress increased. While the overall impact of the war on euro area financial conditions depends on its duration and intensity, the model-based risk outlook is likely to deteriorate.

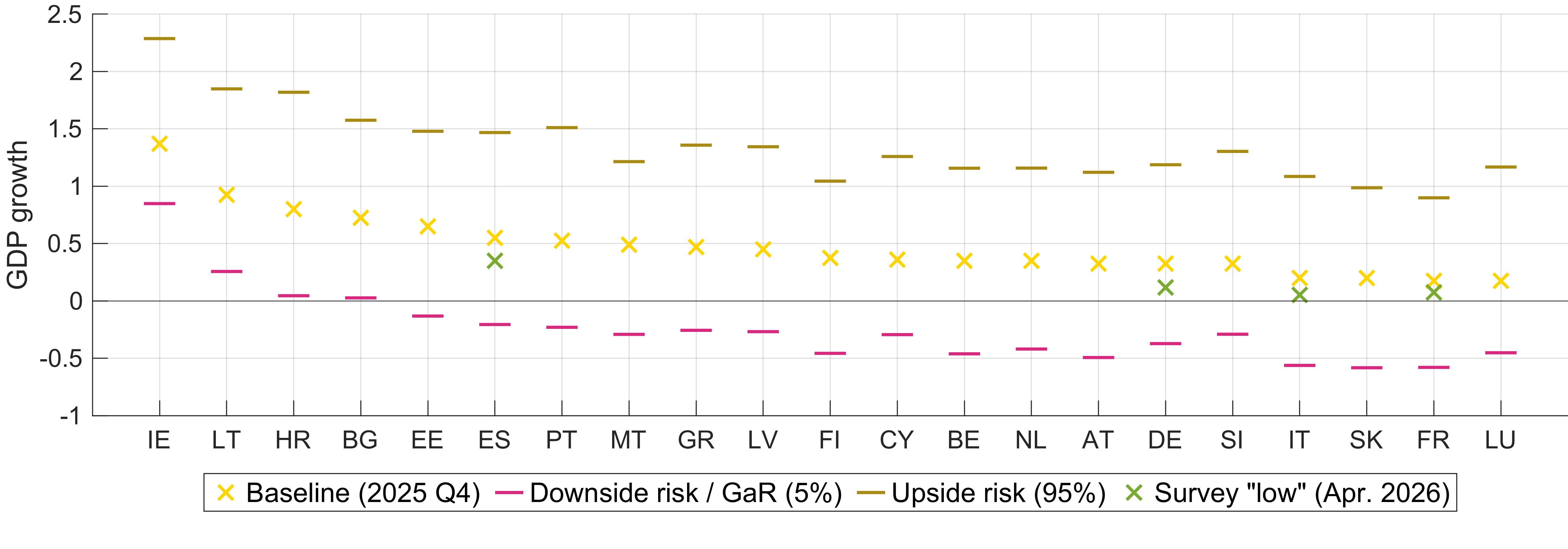

Already before the outbreak of the war in the Middle East, forecasts of economic growth and surrounding risks varied widely across euro area countries. While only mild growth for several (larger) euro area member states was foreseen, many smaller member states were projected to continue growing strongly (Figure 3). The differences in pre-war baseline forecasts overall translate into different levels of Growth-at-Risk, i.e. low-probability adverse growth outcomes. However, there are also countries with comparable baseline forecasts, but sizeable differences in Growth-at-Risk, suggesting that country-specific financial conditions and associated risks vary. Similarly to the aggregate euro area picture, also more pessimistic forecasts, while often reflecting sizeable downward revisions, are for now not in the left tail of the pre-war distributions.

Figure 3

Risks to GDP growth in 2026 across euro area countries

(as of 2025 Q4)

Notes: The figure shows the lower and upper 5% quantiles of the forecasted real GDP growth distribution (4-quarter-ahead average q/q), based on data until 2025 Q4 and centred around the European Commission’s Autumn Forecast 2025. Survey “low” indicates the average of the two most pessimistic forecasts from Bloomberg’s survey. We report results for countries with at least ten survey contributors.

Sources: ESM calculations, European Commission, and Bloomberg

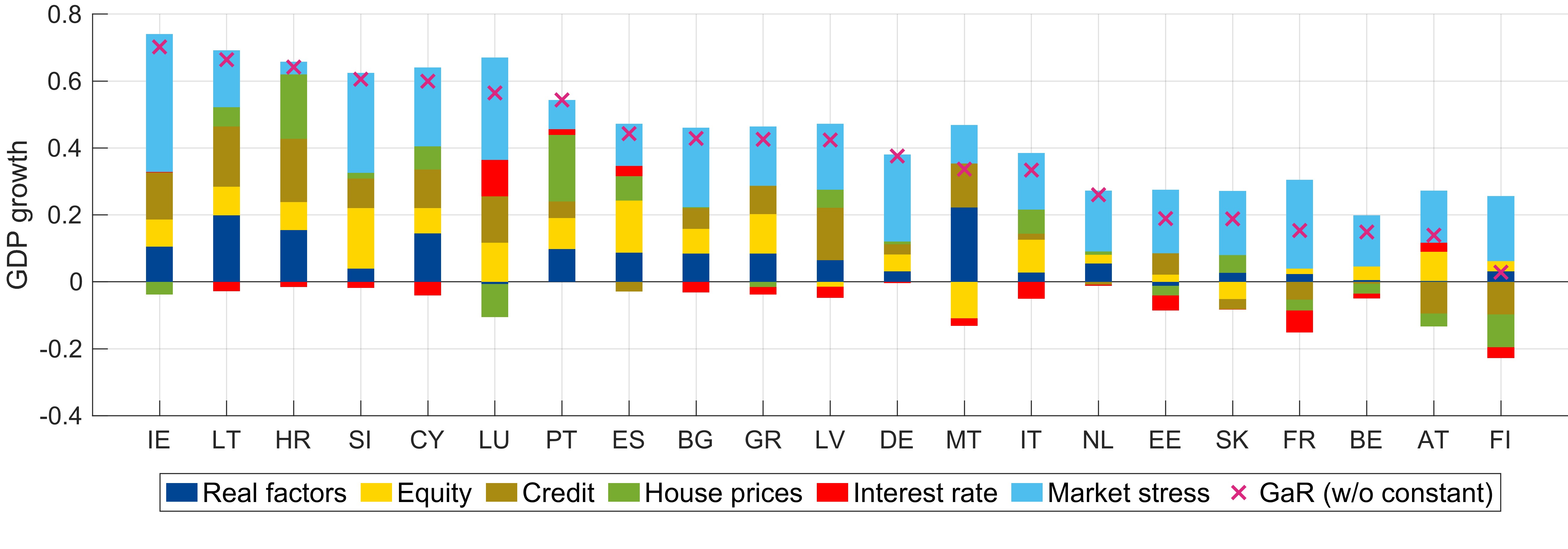

Despite geopolitical uncertainty already prior to the war in the Middle East, financial conditions remained favourable until the end of 2025 in most euro area countries. While economic activity is always at risk of negative surprises, financial indicators signalled that these risks were lower than their historical averages (Figure 4). In all countries, this reflected relatively low levels of volatility and market stress which, however, partly reignited in the first quarter of 2026. Moreover, robust credit growth and house price dynamics help contain near-term risks in several countries. Similarly, rising valuations in equity markets so far benefitted many euro area countries, but stock prices could suffer a lasting blow if there is a re-escalation of the conflict in the Middle East leading to a much longer war. In addition, there is a risk that investors may lose trust in growth prospects related to the booming artificial intelligence sector. Lastly, favourable growth outcomes in 2025 helped reduce several countries’ short-term risk.

Figure 4

Decomposition of downside risk across euro area countries

(as of 2025 Q4)

Notes: The figure shows the decomposition of Growth-at-Risk (5%-quantile) in 2025 Q4. A negative (positive) contribution indicates that a variable contributes to increasing (reducing) risk compared to the historical average. Real factors are captured by current real GDP growth.

Source: ESM calculations

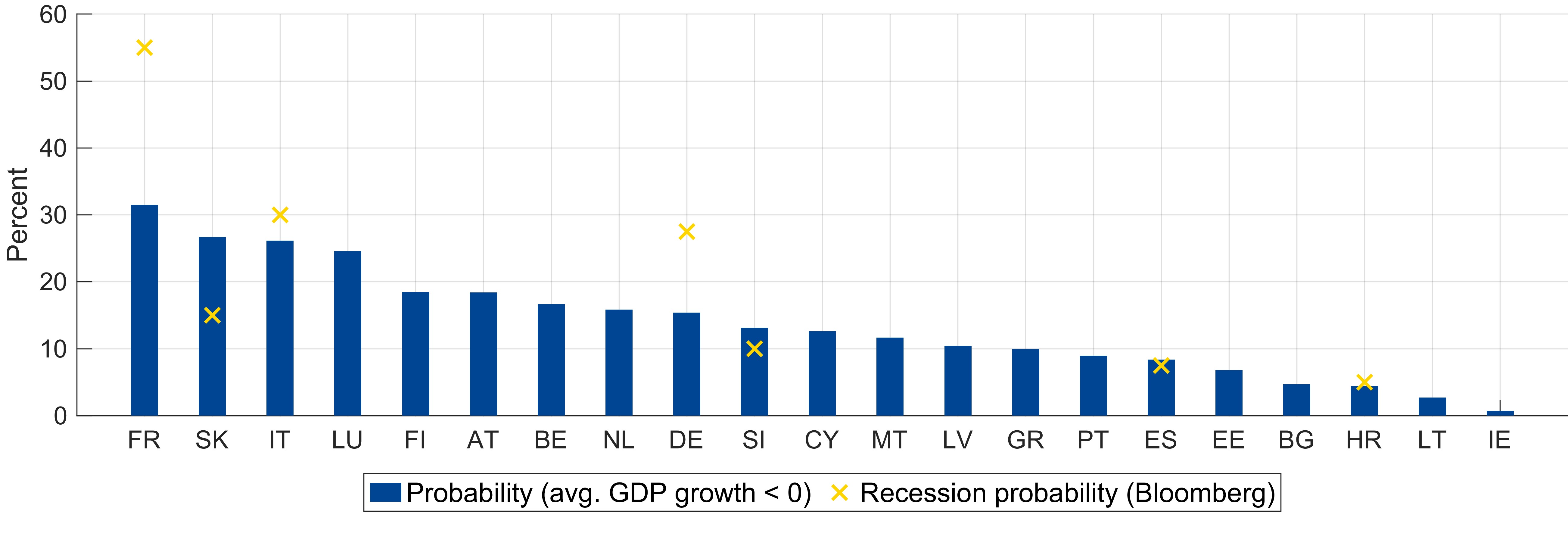

Despite robust financial conditions, relatively low baseline forecasts mean that several countries face a sizeable chance of economic contraction. Since the Growth-at-Risk approach can derive the full range of possible growth outcomes from a few key predicted points, we can calculate the probability of GDP growth falling below any given level. Figure 5 shows that the differences in pre-war forecasts and downside risks result in a wide range of contraction probabilities over the next year. We compare these with Bloomberg’s latest surveyed probabilities of recession. While our model-based numbers do neither reflect the likelihood of a recession – defined as two consecutive quarters of negative growth – nor include the impact of the war in the Middle East, we observe similarities between both numbers in some cases, but differences in others. These probabilities of negative growth are likely to increase as market stress in the first quarter of 2026 rose and baseline growth forecasts weakened.

Figure 5

Probability of negative GDP growth across euro area countries

Notes: The figure shows the probability of negative average (quarter-on-quarter) real GDP growth over the next four quarters (as of 2025 Q4) along with the latest surveyed recession probability from Bloomberg, if available.

Sources: ESM calculations and Bloomberg

Caveats and scope for improvement

Practitioners working with analytical tools like this model need to be aware of the underlying assumptions and shortcomings to assess their value and use cases. First, the results based on our current model only reflect risks to economic activity to the extent that these affect the variables behind the FCI, cause market stress, or already impact a country’s current growth performance. Second, in the case of our sample of euro area countries, the model’s estimates are largely shaped by the link between financial conditions and growth outcomes observed during the Global Financial Crisis and the European Sovereign Debt Crisis. Finally, the model assumes that a given change in financial conditions or market stress has the same impact across countries.

More generally, the model cannot capture the vulnerability of high levels of market optimism that may potentially reflect a “macro-financial disconnect”. In this regard, sharp shifts in market sentiment can not only stem from conflicts and geopolitical tensions but also a correction of high equity valuations if doubts about the growth-igniting potential of artificial intelligence (AI) were to arise.[7] This would signal increased downside risk to the economy.

We are working to refine our Growth-at-Risk framework with the main priority of increasing the timeliness of some input data. Due to the substantial publication lag of some series feeding into the FCI – most notably house prices[8] – the analysis cannot always reflect the most recent developments. This limitation is particularly important during periods of rapidly changing financial market conditions, where developments since the end of February 2026 provide a prime example. In the case of house prices, release dates of different indices by national sources vary widely. One way to address this issue is to combine already available data with ad-hoc assumptions for other countries. An alternative could be to use survey data, for example, covering consumers’ house price expectations or developments in the construction sector.[9] Moreover, Growth-at-Risk models can be extended beyond financial variables by including non-financial factors, for example economic policy uncertainty (see ESRB, 2025, for a recent example).

Conclusion

The Growth-at-Risk framework – combined with other analytical tools and expert judgement – contributes to the ESM’s holistic analysis of risks across the euro area. The model translates changes in macro-financial conditions into risks to economic growth and allows for a transparent cross-country assessment. When financial variables, and in particular indicators of financial stress, foreshadow increased downside risk to economic activity, the model can help to provide an early warning signal for policymakers. To achieve this objective as effectively as possible, we continuously seek to enhance this type of analysis, for example, by incorporating new data sources and more timely information.

Risks to growth before the war in the Middle East appeared overall contained and its impact on financial conditions and the outlook hinges on the duration and escalation. Before the war in the Middle East, financial conditions, especially equity valuations, were favourable and volatility low, signalling contained near-term risks to growth. Financial markets have experienced turmoil since the end of February, and a re-escalation of the conflict leading to long-lasting war could further adversely affect global investor sentiment. This could generate additional downside risk to economic growth. The negative impact of the war in the Middle East on euro area growth forecasts has been apparent but does not yet constitute a low-probability extreme adverse event given the “pre-war” outlook.

Beyond geopolitical shocks, uncertainties surrounding the continued strong performance of technology (AI) stocks could lead to a sharp correction in valuations, which in turn could signal sizeable downside risk to economic growth. Policymakers should therefore stay vigilant in countries with more pronounced near-term risks, but also in those with strong asset price and credit dynamics, where vulnerabilities may build up over time.

REFERENCES

Adrian T., Boyarchenko, N. and Giannone, D. (2019). “Vulnerable Growth”. American Economic Review, 109(4).

Adrian, T. and Gourinchas, P.-O. (2026). “Global Economy Shakes Off Tariff Shock Amid Tech-Driven Boom”, IMF Blog, International Monetary Fund.

Adrian, T., Grinberg, F., Liang, N., Malik, S., and Yu, J. (2021). “The Term Structure of Growth-at-Risk”. American Economic Journal: Macroeconomics, 24(3).

Arrigoni S., Bobasu, A. and Venditti, F. (2022). “Measuring Financial Conditions using Equal Weights Combination”. IMF Economic Review, 70.

Canay, I. A. (2011). “A simple approach to quantile regression for panel data”. The Econometrics Journal, 14(3).

Duprey T., Klaus, B. and Peltonen, T. (2017). “Dating systemic financial stress episodes in the EU countries”. Journal of Financial Stability, 32.

ESRB (2021), “Report of the Expert Group on Macroprudential Stance – Phase II (implementation): A framework for assessing macroprudential stance”, European Systemic Risk Board.

ESRB (2025), “Navigating tail risks: assessing euro area economic growth and equity market vulnerabilities”, Macroprudential Commentaries, European Systemic Risk Board.

Furceri, D., Giannone, D., Kisat, F., Lam, W. R. and Li, H. (2025). “Debt-at-Risk”. IMF Working Papers, International Monetary Fund.

IMF (2017). “Is growth at risk?”: Global Financial Stability Report (Chapter 3), October 2017, International Monetary Fund.

Iseringhausen, M. (2024). “A time-varying skewness model for Growth-at-Risk”. International Journal of Forecasting, 40(1).

Schüler, Y. S., Hiebert, P. P. and T. A. Peltonen (2020), “Financial cycles: Characterisation and real-time measurement”, Journal of International Money and Finance, 100.

[1] The development of Growth-at-Risk was inspired by a financial risk metric known as Value-at-Risk, which quantifies severe losses, for example to an investment portfolio, that could occur in a “worst-case scenario”.

[2] Obtaining the fitted quantiles based on the full set of countries gives broadly similar results, as those omitted from the estimation often have more limited data availability. However, the average fit (in terms of quantile scores) of the 5% quantile is slightly worse in this case. Moreover, we also fit a distribution to the predicted quantiles to obtain the full country-specific distributions of future growth.

[3] The sign of the real interest rate is inverted so that an increase of each variable corresponds to a loosening of financial conditions.

[4] See, for example, Adrian et al. (2021) and Iseringhausen (2024).

[5] The main results presented in this brief rely on data until 2025 Q4 and were produced in early April 2026.

[6] The same holds for the “adverse” and “severe” scenarios published by the ECB as part of the March 2026 staff projections.

[7] A sharp re-pricing of (technology) stocks may also create large liquidity risks in non-bank financial institutions (NBFIs). However, a deeper analysis of this goes beyond the scope of this brief.

[8] Consistent house price data for all euro area member states is currently released by Eurostat around three months after the reference quarter.

[9] In this regard, valuable data sources include the ECB’s Consumer Expectation Survey as well as the European Commission’s Business and Consumer Surveys.

Author

Manager ESM Briefs