Resilience under strain: The euro area is exposed to risks from Middle East conflict and US asset markets

The euro area is facing an unprecedented confluence of challenges. Rising threats to security, fragmenting global trade relationships, energy disruptions, and bouts of financial market volatility place increasing strain on growth and public finances. The region has proven resilient to past shocks, but it will not be immune to those that lie ahead.

Can the euro area remain resilient as external risks intensify and fiscal buffers erode? The answer that we offer in our inaugural Euro Area Stability Watch (EASW) is clear: weaker growth and ever stronger demand for public support are putting debt sustainability under pressure, making difficult policy choices unavoidable. Many countries will need to pursue more determined fiscal adjustments to preserve the credibility of the European fiscal framework. Otherwise, as past crises have shown, financial markets will increasingly constrain their fiscal space, generating uncertainty and instability.

Reassuringly, record-high employment, well-capitalised banks, and strong common backstops remain important pillars of continued resilience. Yet, these strengths coexist with three important pockets of vulnerability.

First, fiscal space is eroding, in part driven by increased defence spending needs. Yet, the EASW shows that much of this expenditure can, over time, support long-term growth and thereby eventually pay for itself, provided it is used productively and backed by efficient European supply chains.

Second, the region remains structurally exposed to energy supply disruptions stemming from geopolitical tensions. Such shocks raise prices and uncertainty, weigh on competitiveness and investment, and risk lasting damage to productivity.

Third, close financial linkages with the United States (US) leave European investors exposed to any potential repricing of US Treasuries and equities, whose stretched valuations rest on artificial intelligence-related earnings expectations. Meanwhile, euro area sovereign markets are becoming increasingly reliant on price-sensitive investors such as hedge funds, many of them based abroad.

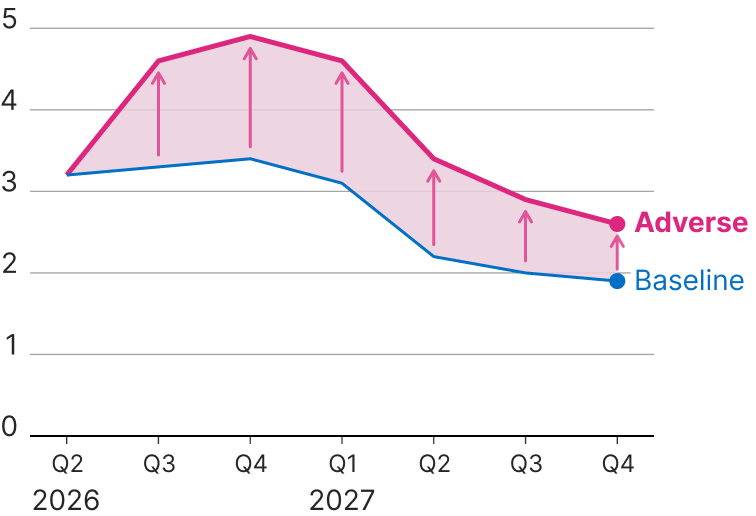

An escalation of geopolitical tensions and associated economic risks is top of mind for investors, as a recent survey of financial market participants conducted by the European Stability Mechanism (ESM) shows. To better understand these risks, the EASW presents an adverse scenario to assess the macroeconomic and fiscal outlook of euro area member states. It assumes two highly relevant risks materialising simultaneously. First, prolonged geopolitical tensions, possibly with renewed escalation in the Middle East, raise energy prices and keep uncertainty high. Second, a sharp repricing of US assets tightens global financial conditions and transmits losses to European investors. Each shock on its own would be challenging. Together, however, they could push the euro area into recession, drive annual inflation close to 5%, and put most countries on upward-trending public debt paths, assuming no monetary or fiscal policy changes. Over the long run, these shocks would cause the euro area to lose 2% of its GDP, an amount equivalent to Finland’s GDP (Figure 1).

Figure 1

Euro area growth nears recession, and inflation soars under the adverse scenario

GDP growth

(% year-over-year)

Inflation

(% year-over-year)

Source: ESM calculations and European Commission’s spring 2026 economic forecast and Eurostat data

Importantly, prolonged and severe tensions cause disproportionately larger economic damage than tensions that are contained. Persistently sluggish investment leaves lasting scars on economies.

Another insight from the analysis is that fiscal pressures under the adverse scenario are distributed differently across countries than during the sovereign debt crisis of the early 2010s. Energy dependence and trade openness, rather than initial fiscal positions, determine the impact on each country. This makes small open economies more vulnerable than others.

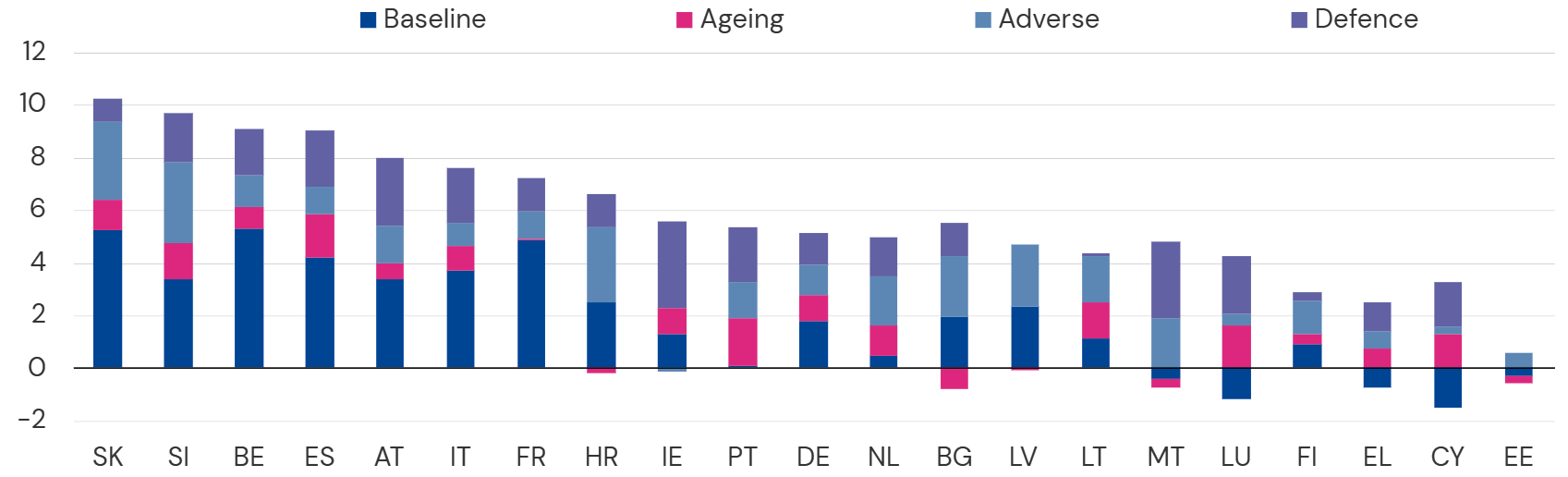

What does all this imply for fiscal policy? To paraphrase the late politician and statesman Willy Brandt, credibility is not everything, but without it, everything is nothing. Fiscal frameworks can buy time and flexibility, but only as long as markets trust that governments are willing and able to use them wisely. The required fiscal adjustments in some euro area members are large (Figure 2). Once rising spending pressures from population ageing and defence, as well as the fiscal impact of existing risks, are taken into account, these adjustment needs exceed past achievements in around half of the euro area countries.

Figure 2

Large fiscal adjustment needs require difficult policy choices

Cumulative adjustment needs over 2026–2035, including additional fiscal effort for long-term spending pressures (defence and ageing costs)

(in percentage points of GDP)

Notes: Adjustment needs are split into (i) baseline needs stemming from initial budgetary conditions (ii) additional needs to offset adverse economic conditions; and (iii) long-term spending pressures from defence to reach NATO’s 3.5% of GDP target by 2035 and costs of ageing (2024 Ageing Report). Austria, Cyprus, Ireland, and Malta are not NATO members, but an increase in defence spending up to 3.5% of GDP target is also included in the exercise.

Source: ESM calculations based on European Commission’s AMECO data, spring 2026 package data and the 2024 Ageing Report

When room for manoeuvre is limited, the quality of policy choices becomes critical, particularly at a time when political fragmentation may complicate implementation. This strengthens the case for temporary, targeted, and tailored measures to cushion external shocks. For example, tax credits or transfers to the most vulnerable are preferable to blanket cuts in petrol tax rates. Rebuilding buffers, spending efficiently, and advancing structural reforms are as essential as ever. This will also require tough choices on spending priorities. As a backstop, the euro area safety net can prevent liquidity strains from turning into solvency fears, including through credible insurance mechanisms such as ESM precautionary arrangements.

Acknowledgments

The author would like to thank Christoph Rosenberg for his valuable contribution to this blog.

Go to the report

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager