Spain

PROGRAMME TIMELINE FOR SPAIN

2008

Housing bubble and construction boom

Bubble bursts; banks suffer loan losses; economic recession

Spanish government starts bank restructuring

Bank restructuring completed

Spain achieves 3.2% economic growth

2009

2010

2011

2012

2013

2014

2015

Programme overview

Years: 2012-2013

Lender: ESM (€41.3 billion for bank recapitalisation)

Addressing a crisis fuelled by the financial sector

The years 1997-2008 were a period of economic expansion in Spain, due in part to a housing boom that was fuelled by lending of the Spanish banking sector. Many banks, particularly savings banks, failed to properly manage the risks associated with the massive scale of loans to construction and property development firms. The real estate bubble burst when the impact of the global financial crisis was felt in Spain, leading to a deterioration in the quality of banks’ balance sheets and capital levels. A restructuring process was started by the Spanish authorities in 2010. However, this process overlapped with an economic downturn that turned out deeper and longer than expected. The funding costs for Spain and Spanish banks increased significantly. The uncertainty and worsening market conditions raised concern that private and public resources would be insufficient to support the banking system. Spain requested financial assistance from the EFSF/ESM in 2012.

The loans provided by the ESM were tied to the implementation of two types of measures:

Bank-specific measures:

- Identifying bank capital needs through asset quality review and stress-test;

- Bank recapitalisation and restructuring;

- Segregation and transfer of impaired assets to SAREB (asset management company).

Sector-wide measures to strengthen the banking sector as a whole, including:

- Higher capital requirements;

- Improved bank governance rules;

- Upgraded reporting requirements;

- Strengthened financial regulation and supervision.

Thanks to the implementation of measures specified in the programme, Spain’s banking sector was stabilised and consolidated. Banks strengthened their capital base and access to funding. Restoring the viability of the banking sector was a crucial element in Spain’s overall economic recovery. The country returned to economic growth in 2014, with positive developments in the areas of competitiveness, employment, and current account balance. These positive developments lasted until the pandemic crisis affected the European and global economy in 2020.

After the programme

Following the completion of Spain’s programme in 2013, post-programme surveillance (PPS) has been carried out by the European Commission in liaison with the European Central Bank. The procedure involves regular review missions in the programme country to assess its economic, fiscal situation and developments in the financial sector. The ESM participates in PPS missions to fulfil the requirements of its Early Warning System, i.e. to assess a country’s capacity to repay its outstanding loans.

Between 2014 and 2018, Spain made a series of early repayments of its ESM loans, amounting to €17.6 billion.

ESM country team coordinator for Spain: Marialena Athanasopoulou

Details of ESM financial assistance for Spain

| Date of disbursement | Amount disbursed | Type of disbursement | Final maturity | Cumulative amount disbursed |

|---|---|---|---|---|

| 11/12/2012 | €39.468 billion | Cashless | 11/12/2027 * | €39.468 billion |

| 05/02/2013 | €1.865 billion | Cashless | 11/12/2025 ** | €41.333 billion |

Weighted average maturity of loans: 12.49 years

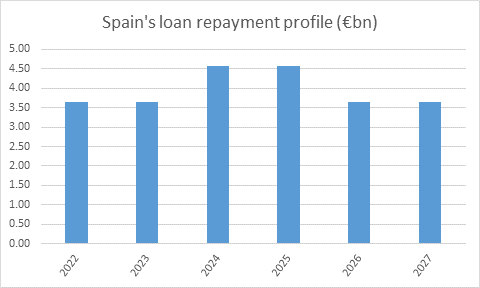

*Constant amortisation between 2022 and 2027 of €4.143 billion per year (amount adjusted following loan prepayments).

**Constant amortisation between 2024 and 2025 of €933 million per year.

Details of the notes provided by ESM

| ISIN | Issuance date | Maturity | Type | Amount |

|---|---|---|---|---|

| EU000A1U98X6 | 01/02/2013 | 05/08/2015 | 30-month FRN | €1.865 billion |

| EU000A1U97C2 | 05/12/2012 | 11/02/2013 | 2-month Bill | €2.5 billion |

| EU000A1U97D0 | 05/12/2012 | 11/10/2013 | 10-month Bill | €6.468 billion |

| EU000A1U98U2 | 05/12/2012 | 11/06/2014 | 18-month FRN | €6.5 billion |

| EU000A1U98V0 | 05/12/2012 | 11/12/2014 | 2-year FRN | €12 billion |

| EU000A1U98W8 | 05/12/2012 | 11/12/2015 | 3-year FRN | €12 billion |

Loan repayments

| Date of repayment | Amount repaid | Cumulative amount repaid | Details |

|---|---|---|---|

| 08/07/2014 | €1.304 billion | €1.304 billion | Early repayment (voluntary) |

| 23/07/2014 | €0.308 billion | €1.612 billion | Scheduled repayment of unused funds |

| 17/03/2015 | €1.5 billion | €3.112 billion | Early repayment (voluntary) |

| 14/07/2015 | €2.5 billion | €5.612 billion | Early repayment (voluntary) |

| 11/11/2016 | €1 billion | €6.612 billion | Early repayment (voluntary) |

| 14/06/2017 | €1 billion | €7.612 billion | Early repayment (voluntary) |

| 16/11/2017 | €2 billion | €9.612 billion | Early repayment (voluntary) |

| 23/02/2018 | €2 billion | €11.612 billion | Early repayment (voluntary) |

| 23/05/2018 | €3 billion | €14.612 billion | Early repayment (voluntary) |

| 16/10/2018 | €3 billion | €17.612 billion | Early repayment (voluntary) |

| 12/12/2022 | €3.643 billion | €21.255 billion | Scheduled repayment |

| 11/12/2023 | €3.643 billion | €24.898 billion | Scheduled repayment |

Related documents

Legal documents

- Financial Assistance Facility Agreement (PDF, 125 KB)

Review documents published by the European Commission

- Post-programme Surveillance Report, Spring 2022

- Post-programme Surveillance Report, Autumn 2021

- Post-programme Surveillance Report, Spring 2021

- Post-programme Surveillance Report, Autumn 2020

- Post-programme Surveillance Report, Spring 2020

- Post-programme Surveillance Report, Autumn 2019; Statement by EC and ECB, 10/10/2019

- Post-programme Surveillance Report, Spring 2019; Statement by EC and ECB, 10/05/2019

- Post-programme Surveillance Report, Autumn 2018; Statement by EC and ECB, 09/10/2018

- Post-programme Surveillance Report, Spring 2018; Statement by EC and ECB, 16/04/2018

- Post-programme Surveillance Report. Autumn 2017; Statement by EC and ECB, 23/10/2017

- Post-programme Surveillance Report, Spring 2017; Statement by EC and ECB, 28/04/2017

- Post-Programme Surveillance Report. Autumn 2016; Statement by EC and ECB, 24/10/2016

- Post-Programme Surveillance Report, Spring 2016; Statement by EC and ECB, 18/04/2016

- Evaluation of the Financial Sector Assistance Programme. Spain, 2012-2014 (Dec. 2015)

- Post-Programme Surveillance Report, Autumn 2015; Statement by EC and ECB, 12/10/2015

- Post-Programme Surveillance Report, Spring 2015; Statement by EC and ECB, 23/03/2015

- Post Programme Surveillance Report, Autumn 2014; Statement by EC and ECB, 13/10/2014

- Post Programme Surveillance Report, Spring 2014; Statement by EC and ECB, 04/04/2014

- Fifth Review – Winter 2014; Statement by EC and ECB, 16/12/2013

- Fourth Review – Autumn 2013; Statement by EC and ECB, 30/09/2013

- Third Review– Summer 2013; Statement by EC and ECB, 03/06/2013

- Second Review – Spring 2013; Statement by EC and ECB, 04/02/2013

- First review - Autumn 2012; Statement by EC and ECB, 26/10/2012

- The Financial Sector Adjustment Programme for Spain (October 2012)

Facts

Explainer

ESM assistance was key in cleaning the balance sheets of troubled banks, improving their capital base, and overcoming market fears about the depth of the problems in Spain’s financial sector.

Spain was scheduled to repay the loan principal from 2022 to 2027. However, starting in July 2014, the Spanish government made the first in a series of early repayments to the ESM. To date, Spain has repaid €24.9 billion (out of the total loan amount of €41.3 billion).

No, the IMF did not make a financial contribution because unlike the ESM, it does not have a financial assistance tool related to bank recapitalisation. The IMF was only involved in an advisory and monitoring capacity.

Yes, the European Commission was closely involved in the bank recapitalisation process and approved the state aid for the recapitalisation of the banks concerned.

In the case of Spain, conditions were strictly directed to the banking sector. There were three main conditions: first, identifying individual bank capital needs through an asset quality review of the banking sector and a bank-by-bank stress test. Second, recapitalising and restructuring weak banks based on plans to address any capital shortfalls identified in the stress test. Finally, problematic assets in those banks receiving public support (without any credible plans to address their capital shortfalls by private means) were to be segregated and transferred to an external asset management company (Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria – SAREB).

In addition, conditionality was also applied in order to strengthen the banking sector as a whole. This included regulatory capital targets, bank governance rules, an upgrade of reporting requirements and improved supervisory procedures.

In June 2012, the Spanish government made an official request for financial assistance for its banking system to the Eurogroup for a loan of up to €100 billion. It was designed to cover a capital shortfall identified in a number of Spanish banks, with an additional safety margin.

In December 2012, the Spanish government formally requested the disbursement of €39.47 billion via a dedicated ESM loan for the recapitalisation of the banking sector. The funds were transferred in the form of ESM notes on 11 December 2012 to the Fondo de Restructuración Ordenada Bancaria (FROB), the bank recapitalisation fund of the Spanish government. The FROB used these notes for the recapitalisation, in an amount close to €37 billion, of the following banks: BFA-Bankia, Catalunya-Caixa, NCG Banco and Banco de Valencia. Additionally the FROB was to provide up to €2.5 billion to SAREB, the asset management company for assets arising from bank restructuring.

In January 2013, the Spanish government formally requested the disbursement of €1.86 billion for the recapitalisation of the following banks: Banco Mare Nostrum, Banco Ceiss, Caja 3 and Liberbank. The funds were transferred to the FROB in the form of ESM notes on 5 February 2013.

No further requests for disbursement were made, thus the overall amount of financial assistance provided by the ESM to Spain was €41.33 billion. This was the only instance so far when the ESM indirect recapitalisation loan was used.

The disproportionate growth in the real estate sector, along with the expansion of credit to finance it, were the main reasons behind Spain’s economic imbalances. In the real estate sector, a spiral of growth in demand, prices and supply caused a major bubble, which burst when the impact of the international financial crisis was felt in Spain. The massive scale of loans for construction and property development caused an excessive exposure of the banking industry to those sectors. In particular, Spain’s savings banks (Cajas de Ahorros) were affected by solvency problems.

A restructuring process was started by the Spanish authorities in 2010. However, the economic downturn turned out deeper and longer than expected. The funding costs for Spain as well as Spanish banks significantly increased. These market conditions raised widespread concern that private and public resources would be insufficient to support the banking system with capital.